Protecting your wealth is critical if you’re a high-net-worth individual facing potential risks like lawsuits, failed ventures, or divorce. This article breaks down real strategies that shielded millions of dollars from creditors, showing how proactive planning can safeguard assets.

Key takeaways include:

- Offshore Trusts: A Cook Islands trust helped protect a $15M portfolio from lawsuits by leveraging why offshore asset protection offers strict legal standards and jurisdictional advantages.

- Domestic Asset Protection Trusts (DAPTs): A Nevada DAPT secured $8M for a doctor, shielding assets from malpractice claims within U.S. borders.

- Family Limited Partnerships (FLPs) and Offshore Companies: Combining these tools protected $12M in real estate by limiting creditor access and controlling distributions.

The lesson? Timing and proper structuring are everything. These methods work best when implemented before any legal claims arise. Below, we’ll explore how these strategies work and the steps you can take to protect your wealth.

Case Study 1: Protecting a $15 Million Portfolio with a Cook Islands Offshore Trust

Back in 2019, Mark, a solo tech entrepreneur, found himself staring down a hefty $1.8 million pre-trial judgment after a failed business partnership. His portfolio included $900,000 in liquid assets and equity in two LLCs worth several million dollars. To shield his wealth, Mark set up a Cook Islands trust and moved his assets offshore. Despite the plaintiff spending $210,000 in legal fees chasing the trust, the legal framework worked in Mark’s favor, resulting in a $120,000 settlement paid from his domestic assets.

This wasn’t a stroke of luck. It was the outcome of a carefully crafted legal strategy, leveraging the unique protections offered by the Cook Islands’ legal system. Let’s break down how this setup effectively kept creditors at bay.

How Cook Islands Trusts Block Creditors

Cook Islands trusts are built on the International Trusts Act 1984, a legal framework designed to prioritize asset protection over creditor claims. The key advantage? The burden of proof. In U.S. civil cases, creditors only need to prove their case by a "preponderance of evidence." But in the Cook Islands, creditors must prove fraudulent intent “beyond a reasonable doubt”.

"The criminal standard requires near-certainty. Applying the criminal standard to a civil fraud claim means that even if a creditor can show that a transfer looks suspicious… that is not enough." – HPT Group

The hurdles don’t stop there. Cook Islands courts don’t recognize foreign judgments, meaning a creditor armed with a U.S. court ruling must re-litigate the entire case in the Cook Islands High Court. This process involves hiring local FSCO-licensed counsel, covering legal costs upfront in New Zealand dollars, and often posting a significant bond just to file a claim. Adding to the challenges, claims are barred if the trust was established more than two years after the creditor’s cause of action arose or if action isn’t taken within one year of discovering the transfer.

Main Features of This Protection Method

Mark’s ability to safeguard his wealth rested on four key structural elements that took full advantage of Cook Islands law:

- Independent Trustee and Relinquished Control: A licensed trustee in the Cook Islands held legal title to the assets and had the authority to refuse foreign court orders. Mark wasn’t listed as a trustee or co-trustee, ensuring he had no direct control over the trust. This step was critical, as U.S. courts could have deemed the trust invalid if Mark retained control.

- Duress Clauses: The trust deed included clauses preventing the trustee from complying with demands made under legal pressure. For example, when Mark “requested” funds under court order, the trustee responded that the assets were tied up in investments and inaccessible – an option supported by Cook Islands law.

- LLC Integration: Mark’s real estate and investments were held within Nevada LLCs, with the Cook Islands trust as the sole member. This setup allowed the trust to own equity interests rather than holding direct title to physical assets.

Results and Lessons Learned

This case showcases the importance of planning ahead when it comes to protecting substantial wealth. By leveraging the protections of a Cook Islands trust, Mark was able to settle a $1.8 million judgment for just $120,000 while keeping his offshore assets out of reach.

Here are a few takeaways:

- Timing Is Critical: Establish your trust before any legal claims arise. Moving assets after a claim can lead to accusations of fraud.

- Relinquish Control: Don’t act as the trustee or retain veto power over distributions. Courts could view this as maintaining control, making the trust invalid.

- Stay Tax Compliant: Offshore trusts aren’t tax shelters. U.S. citizens must file IRS Forms 3520 and 3520-A and comply with FBAR and FATCA reporting requirements.

- Keep Domestic Liquidity: Maintain enough funds in domestic accounts to cover liabilities and living costs. Moving all assets offshore could raise red flags in court.

Setting up a Cook Islands trust generally costs between $11,000 and $35,000, with annual fees ranging from $3,000 to $12,000.

sbb-itb-39d39a6

Case Study 2: Protecting $8 Million with a Nevada Domestic Asset Protection Trust

In 2021, Dr. Jennifer Chen, an orthopedic surgeon based in California, faced a growing concern. The medical field’s increasing litigation risks made it clear she needed a strong plan to safeguard her $8 million portfolio. Her wealth included personal savings, investment accounts, and equity in her medical practice. She wanted a solution that would keep her assets within the U.S. while offering robust protection against creditors.

Dr. Chen turned to a Nevada Domestic Asset Protection Trust (DAPT). She transferred her liquid investment portfolio into the trust and appointed an independent, Nevada-licensed trustee to manage it, ensuring she no longer had direct control over distributions. To further protect her assets, the trust became the owner of a Nevada LLC, which held her practice equity and rental properties. This layered setup effectively separated her personal wealth from her high-risk medical practice.

In 2023, a malpractice claim exceeding her $2 million insurance policy threatened her assets. However, thanks to Nevada’s laws and the trust’s two-year seasoning period, her assets remained protected. The case settled within her insurance limits, and her $8 million trust assets were untouched.

How Nevada DAPTs Work

Nevada DAPTs, governed by NRS Chapter 166, are irrevocable trusts designed to protect the grantor by transferring legal ownership of assets. They require at least one independent trustee who is either a Nevada resident or a Nevada-licensed trust company.

A key feature of Nevada DAPTs is the two-year seasoning period. Once assets are transferred, they are generally shielded from future creditor claims after two years – this is the shortest waiting period of any DAPT state. Nevada also stands out as one of only two states that doesn’t recognize "exception creditors", meaning assets are protected even from claims like child support or tort judgments.

"Nevada DAPTs represent the gold standard in liability protection, providing individuals with a powerful shield against potential creditors while maintaining their assets within U.S. borders." – Sarah Ocampo, Founder and CEO, Ocampo Wiseman Law

Creditors face significant challenges when attempting to contest a Nevada DAPT. They must prove fraudulent transfer by "clear and convincing evidence", which is a higher standard than the "preponderance of evidence" used in most jurisdictions. For existing creditors, the challenge period is limited to the later of two years after the transfer or six months after discovering the transfer.

To qualify for protection, Nevada DAPTs must meet specific requirements:

- Irrevocability: The trust cannot be amended or revoked by the grantor.

- Nevada Trustee: At least one trustee must be a Nevada resident or a licensed trust company.

- No Mandatory Distributions: Distributions to the settlor are discretionary and managed by the trustee.

- Nevada Situs: The trust must be administered in Nevada under Nevada law.

- Statutory Period: A two-year limitations period applies for creditors to challenge transfers.

Nevada also provides financial advantages, including a 0% state income tax on trust assets, which is particularly appealing to individuals in high-tax states. Additionally, Nevada allows trusts to last up to 365 years, enabling wealth to be passed down through multiple generations.

To further enhance her asset protection, Dr. Chen integrated a Nevada LLC into her trust structure.

Adding LLCs to the Trust Structure

Dr. Chen’s approach didn’t stop at establishing a DAPT. She incorporated a Nevada LLC into her plan, with the DAPT owning interests in the LLC. This LLC held her business assets, creating an additional layer of protection that ensured claims against her medical practice couldn’t reach the trust’s liquid assets.

Nevada’s charging order protection played a crucial role here. If a creditor wins a judgment against an individual, their remedy is limited to distributions from the LLC. They cannot seize underlying assets or control business operations.

"The protection comes not from giving up control, but from the legal structure Nevada provides." – George Dimov, President & Managing Owner, Dimov Tax

Dr. Chen also served as the "Investment Trustee", allowing her to guide how the trust’s assets were invested without having unilateral access to funds. This ensured the trust remained legally sound and couldn’t be dismissed as a "sham" by the courts.

Results and Practical Lessons

By taking a proactive approach, Dr. Chen successfully shielded her $8 million portfolio from professional liabilities. Her strategy of establishing the DAPT well in advance of any claims and adhering to its formalities ensured her assets were protected. When the malpractice case arose, it was resolved within her insurance coverage, preserving her financial security.

Setting up a Nevada DAPT typically costs between $15,000 and $30,000, with annual administrative fees ranging from 0.5% to 1.5% of the trust’s assets. For an $8 million trust, this equates to about $40,000 to $120,000 annually – a worthwhile expense for comprehensive asset protection.

Key takeaways from Dr. Chen’s case include:

- Plan Ahead: Asset protection strategies should be implemented well before any liability arises. Transferring assets after a claim can be deemed fraudulent.

- Maintain Independence: Avoid actions that could undermine the trust’s integrity, such as unilaterally directing investments or replacing trustees.

- Use Layers: Combining a DAPT with an LLC creates additional barriers between personal wealth and professional liabilities.

- Follow the Rules: Ensure the trust is administered in Nevada, with all records and decisions kept within the state.

- Know the Limits: While Nevada law offers a two-year seasoning period, the federal Bankruptcy Code has a 10-year lookback for self-settled trusts in cases of fraudulent intent.

Nevada DAPTs provide a reliable way to protect assets while keeping them within the U.S. For professionals in high-risk fields, this strategy offers peace of mind and a secure way to manage wealth tailored to individual needs.

Case Study 3: Using Family Limited Partnerships and an Anguilla Offshore Company to Protect $12 Million

This case explores how a Texas real estate investor, Michael Thompson, protected his $12 million in rental properties by combining a Family Limited Partnership (FLP) with an Anguilla offshore company. In 2019, Michael faced a lawsuit from a business partner that threatened his entire portfolio, leaving him in need of a solution to safeguard his assets while maintaining control.

Michael’s attorney proposed a two-layer strategy: placing his properties in an FLP and appointing an Anguilla offshore company as the FLP’s general partner. The FLP legally owned the properties, creating a separation that shielded them from personal creditor claims. Meanwhile, the offshore company managed the FLP’s operations, adding an extra layer of protection.

When the lawsuit escalated in 2020, resulting in a judgment against Michael, creditors attempted to target his properties. However, FLP laws limited them to a charging order, which only allowed them to place a lien on partnership distributions, not the properties themselves. By controlling distributions through the offshore company, Michael was able to suspend payouts during the legal battle. This forced creditors to settle for a modest amount, leaving his portfolio untouched.

How FLPs and Offshore Companies Work Together

The pairing of an FLP with an offshore company creates a strong defense against creditor claims. By transferring assets into an FLP, they become the property of a separate legal entity, making them harder to access. Creditors are restricted to a charging order, which does not grant them direct control over the assets.

The addition of an Anguilla offshore company as the general partner introduces another hurdle. Creditors must navigate Anguilla’s legal system to challenge the FLP’s structure, which can be both costly and time-consuming. This setup not only discourages legal action but also ensures the owner retains control over the assets and their operations.

Why Anguilla Works Well for Asset Protection

Anguilla has become a popular choice for asset protection due to its modern legal framework and creditor-resistant laws. The Anguilla Trust Act of 2014 provides a strong foundation for structuring offshore trusts for asset protection. A key feature is the Fraudulent Dispositions Ordinance, which requires creditors to prove that the transfer of assets rendered the settlor insolvent or was done while the settlor was already insolvent – not merely that it was intended to hinder creditors.

"Anguilla requires creditors of the settlor to prove that the settlor was insolvent (financially broke) at the time he/she transferred assets into the trust, or became insolvent because of the transfers." – OffshoreCompany.com

Anguilla also enforces a strict three-year statute of limitations on legal challenges to asset transfers. Additionally, its courts do not recognize foreign judgments related to bankruptcy or tax claims, ensuring U.S. court orders have no authority there. Other benefits include the ability to establish perpetual asset protection structures and privacy safeguards, as settlor and beneficiary names are not disclosed in public records. Setting up these structures in Anguilla is efficient and cost-effective.

Results and Key Takeaways

Michael’s approach demonstrates the power of combining an FLP with an offshore company. This structure protected his $12 million portfolio by making creditor recovery both legally and financially impractical. By halting distributions during the dispute, Michael ensured creditors could not access any funds.

The main lessons here are clear: proactive planning is crucial – asset protection strategies must be in place before creditor claims arise. Using multiple layers of protection, such as an FLP and an offshore entity, creates significant barriers that deter legal action. Finally, maintaining compliance and controlling distributions are essential for preserving the integrity of the structure.

For real estate investors and other high-net-worth individuals, this strategy offers a way to protect assets, retain control, and benefit from favorable U.S. tax treatment.

Main Lessons from These Asset Protection Cases

These cases highlight the importance of early planning, designing well-structured systems, and selecting the right jurisdictions for asset protection. In each example – whether the assets involved were $15 million, $8 million, or $12 million – the individuals began their planning before any creditor claims arose. This reinforces the need to act before facing potential threats.

A key takeaway is the importance of separating control from ownership. Asset protection strategies often fail in court when the owner retains too much control. By incorporating independent trustees, structured LLCs, and layered entities like family limited partnerships, these approaches create legal safeguards that make it much harder for creditors to access assets.

"Timing is everything. Transfers made before a creditor has notice stand a far better chance than transfers after a demand letter arrives."

- Brian T. Bradley, Asset Protection Attorney

Another critical insight is the advantage of jurisdictional selection. Offshore jurisdictions make it significantly harder for creditors by requiring higher levels of proof compared to domestic options. While domestic strategies, such as Nevada asset protection trusts, offer convenience and flexibility, they may not provide the same level of protection against foreign litigation.

These lessons provide a foundation for crafting a strong asset protection plan.

Steps for Effective Asset Protection

Drawing from the cases, building a solid asset protection strategy involves three essential actions: starting early, layering protection, and seeking professional expertise.

- Start early. Transfers made after a threat arises are often seen as fraudulent. Once a creditor is aware of potential transfers, options for legitimate protection narrow drastically.

- Layer your protection. Combining tools like trusts, LLCs, and family limited partnerships (FLPs) creates multiple legal barriers. Each layer forces creditors to overcome additional hurdles, making recovery efforts more challenging.

- Work with experienced professionals. Professionals can help draft structures that include safeguards like duress clauses, which suspend a settlor’s ability to remove trustees under legal pressure. Without precise drafting, even well-structured plans can become vulnerable.

"A trust is only as real as the loss of effective settlor control. Retaining the power to direct distributions… turns a trust into a sham in the view of many courts."

- Brian T. Bradley, Asset Protection Attorney

Additionally, compliance with tax regulations is crucial. Offshore structures must meet U.S. reporting requirements, such as FBAR and Form 3520, to avoid creditors exploiting tax non-compliance as a weakness.

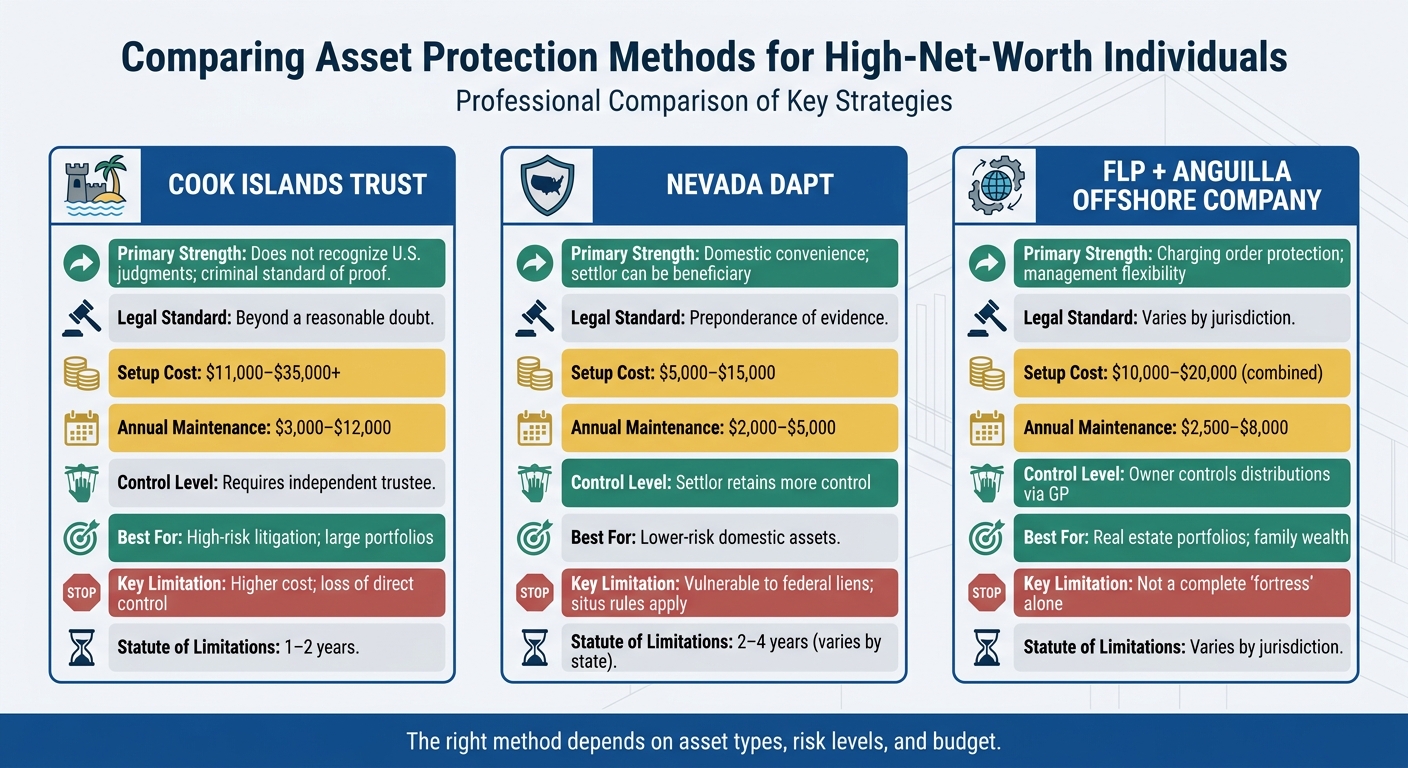

Comparing Different Asset Protection Methods

The table below breaks down the features of various asset protection methods, helping to clarify which approach might suit different needs:

| Feature | Cook Islands Trust | Nevada DAPT | FLP + Anguilla Offshore Company |

|---|---|---|---|

| Primary Strength | Does not recognize U.S. judgments; criminal standard of proof | Domestic convenience; settlor can be beneficiary | Charging order protection; management flexibility |

| Legal Standard | Beyond a reasonable doubt | Preponderance of evidence | Varies by jurisdiction |

| Setup Cost | $11,000–$35,000+ | $5,000–$15,000 | $10,000–$20,000 (combined) |

| Annual Maintenance | $3,000–$12,000 | $2,000–$5,000 | $2,500–$8,000 |

| Control Level | Requires independent trustee | Settlor retains more control | Owner controls distributions via GP |

| Best For | High-risk litigation; large portfolios | Lower-risk domestic assets | Real estate portfolios; family wealth |

| Key Limitation | Higher cost; loss of direct control | Vulnerable to federal liens; situs rules apply | Not a complete "fortress" alone |

| Statute of Limitations | 1–2 years | 2–4 years (varies by state) | Varies by jurisdiction |

The right method depends on factors like asset types, risk levels, and budget. For instance, while a Nevada trust may work well for domestic liquid assets, those facing higher litigation risks or managing significant real estate holdings might benefit from the added protection of offshore structures.

How Global Wealth Protection Fits Into Your Strategy

The case studies highlight the importance of precise execution when it comes to tools like offshore trusts, domestic asset protection trusts, and family limited partnerships. Global Wealth Protection specializes in creating these structures, drawing lessons from high-profile cases involving Cook Islands trusts, Nevada Domestic Asset Protection Trusts, and Anguilla offshore company formations. Let’s take a closer look at how their services can help turn these strategies into actionable defenses.

Services Global Wealth Protection Offers

Global Wealth Protection provides tools that mirror proven strategies. Their offerings include offshore asset protection trusts, with a focus on Cook Islands trusts. These trusts stand out due to their strong jurisdictional benefits, such as non-recognition of foreign court orders, short statutes of limitations (often just two years), and high evidentiary requirements for creditors.

One of their standout solutions is The Bridge Trust®. This trust starts as a U.S. grantor trust, avoiding complicated IRS filings, and can seamlessly transition to offshore protection when necessary.

For clients seeking multiple layers of protection, Global Wealth Protection also facilitates private U.S. LLC formation in states with asset-friendly laws. These LLCs can hold assets like real estate or business receivables and are often owned through an offshore trust, creating significant hurdles for creditors. Additionally, the firm handles offshore company formation, particularly in Anguilla, leveraging its favorable asset protection laws and operational flexibility.

Each trust instrument includes critical protective features like duress suspension clauses, which proved pivotal in the "impossibility defense" during the United States vs. Grant case. In that instance, an offshore trust successfully shielded assets from a $36 million IRS claim for over a decade.

"Structure before stress." – Brian T. Bradley, Esq., Asset Protection Attorney

Most clients start with customized consultations. These private, hour-long sessions review individual financial details, identify specific creditor risks, and outline tailored strategies. For married clients, the firm can also draft transmutation agreements to maintain separate property.

The costs reflect the complexity of these structures. Initial setup fees for trusts typically range from $8,000 to $25,000, with additional costs for trustee acceptance and account setup between $3,000 and $10,000. Onshore services like LLC formation and asset transfers cost $2,000 to $8,000. Annual maintenance – including trustee services, administration, and tax compliance – runs between $3,000 and $12,000. These investments align with the protection offered, as fewer than 10% of clients face creditor claims, and less than 1% see actual asset seizures when plans are properly executed.

Getting Started with Asset Protection

The first step in protecting your assets is a comprehensive threat assessment. This evaluation considers your profession, asset types, family circumstances, and overall exposure to identify the best strategies. Timing is critical – planning must occur before creditors are aware of any claims. Transfers made after a lawsuit or demand letter are often classified as fraudulent conveyances, no matter how carefully structured.

"If you do nothing, there is a 100 percent chance that you’ll lose your assets." – Jacob Stein, Managing Partner, Aliant, LLP

Building a team is essential. A combination of domestic and offshore counsel, along with a forensic accountant, ensures all asset transfers are properly documented. Strict adherence to protocols is non-negotiable. The Grant case serves as a cautionary tale: after years of success, a $221,000 distribution to children ultimately undermined the trust because its rules weren’t followed. Independent trustees holding control is key to maintaining the legal shield.

To begin, you can submit a summary of your situation for review by an asset protection attorney or schedule a private consultation to develop a tailored strategy.

Conclusion: Taking Action to Protect Your Wealth

The examples highlighted in this article make one thing clear: planning ahead is what separates those who preserve their wealth from those who lose it. Whether it’s the $15 million Cook Islands trust, the $8 million Nevada DAPT, or the $12 million family limited partnership, they all share one essential feature – they were created before any creditor issues arose. Waiting until creditors appear or litigation begins is a recipe for disaster. The time to act is before trouble surfaces.

These examples underscore how early, strategic asset protection can make a real difference. Well-structured plans can reduce creditor claims to less than 10%, and actual asset seizures occur in fewer than 1% of cases. On the other hand, failing to act leaves your assets fully exposed, with a 100% certainty of loss once a judgment is enforced.

"If you do nothing, there is a 100 percent chance that you’ll lose your assets." – Jacob Stein, Managing Partner, Aliant, LLP

A solid asset protection plan discourages creditors. The mere presence of a properly designed offshore structure often forces creditors to rethink their approach, often resulting in minimal recovery efforts. However, the execution must be airtight. The Grant case serves as a cautionary tale – after years of successful defense, one unauthorized $221,000 distribution led to the collapse of the entire structure.

To safeguard your financial future, integrating these strategies into your planning is critical. Start by evaluating your vulnerabilities, selecting the right tools, and putting them in place before any threats materialize. Whether it’s an offshore trust, a domestic DAPT, or a combination of LLCs and family partnerships, the key is to act decisively and without delay. Taking proactive steps today ensures your wealth remains secure tomorrow.

FAQs

Which asset protection strategy fits my risk level and asset mix?

When it comes to protecting your assets, the best approach depends heavily on your personal risk level and the types of assets you own. For those with a moderate risk profile, trusts – whether offshore or domestic – can be an effective option. They not only safeguard your assets but also offer the added benefit of simplifying estate planning.

If your risk level is higher, you might need a more layered strategy. Combining legal structures like LLCs or limited partnerships with robust liability insurance can provide stronger protection against potential threats.

To ensure your plan is effective and suited to your unique situation, it’s crucial to work closely with legal and financial advisors who can help design a strategy tailored specifically to your needs.

How early is “early enough” to avoid a fraudulent transfer claim?

To reduce the risk of a fraudulent transfer claim, it’s important to transfer assets long before any potential litigation or creditor claims become predictable. Transfers made while a lawsuit is underway or clearly approaching are far more likely to face scrutiny – particularly if they happen close to the time of a claim or seem designed to block creditors.

How much control can I keep without weakening the protection?

Maintaining control over your assets is possible with tools like trusts and limited liability entities. These structures allow you to manage and oversee your property while adding layers of protection. However, exercising too much control can weaken those safeguards, potentially exposing your assets to risks. The key is finding the right balance – one that preserves your legal protections without undermining their effectiveness.