Living abroad as a US citizen complicates estate planning due to global taxation, conflicting laws, and reporting requirements. Here’s what you need to know:

- Global Taxation: The US taxes citizens on worldwide assets, even after death. In 2026, the federal estate tax exemption is $15 million per individual ($30 million for couples). Assets above this are taxed at 40%.

- Double Taxation: Without treaties, your estate could face taxes in both the US and your host country. The US has treaties with 15 countries to mitigate this.

- Spousal Rules: Non-US citizen spouses don’t qualify for unlimited marital deductions, potentially triggering immediate estate taxes. A Qualified Domestic Trust (QDOT) may help.

- Foreign Laws: Many countries, like France or Germany, don’t recognize US trusts and impose forced heirship rules dictating inheritance shares.

- Probate Delays: Dual wills and situs wills can speed up probate across jurisdictions but must be carefully coordinated to avoid conflicts.

Key Tools:

- Dual Wills: Separate wills for US and foreign assets streamline probate.

- Trusts: Irrevocable trusts reduce taxable estates, but foreign recognition varies.

- Tax Treaties & Credits: Treaties and the Foreign Death Tax Credit offset double taxation.

- Advance Directives: Powers of attorney and healthcare directives tailored to each jurisdiction ensure smoother administration.

Proactive planning helps expats reduce taxes, avoid legal conflicts, and ensure assets are distributed as intended. Seek expert advice to navigate these complexities effectively.

US Estate Tax Rules and Global Asset Taxation

US Estate Tax Rules Explained

The United States follows a unique approach to taxation, imposing taxes on its citizens’ worldwide assets, regardless of where they are located. This differs from the residency-based tax systems used by most other countries. Kevin Anderson, Managing Director at BDO USA LLP, explains:

"Domicile and residence are irrelevant for U.S. citizens, who are subject to income tax on their worldwide income, to gift tax on their worldwide gifts, and to estate tax on their worldwide estate".

For 2026, the federal estate tax exemption is set at $15 million per individual or $30 million for married couples who take advantage of portability. Any assets exceeding these limits are taxed at a top marginal rate of 40%. The scope of your taxable estate is broad, including foreign real estate, overseas bank accounts, stakes in foreign businesses, pensions, and personal property like artwork or jewelry.

For expatriates, state-level taxes add another layer of complexity. Even after living abroad for years, you could still be considered domiciled in a U.S. state. Twelve states and the District of Columbia impose their own estate taxes, often with much lower exemption thresholds – like Oregon’s $1 million and Massachusetts’ $2 million limits. Unless you formally sever state ties, such as by canceling voter registration or relinquishing a driver’s license, you could face both federal and state estate tax obligations.

These intricate rules create a challenging framework for U.S. expats, especially when global taxation comes into play.

How Global Taxation Affects US Expats

For U.S. expats, double taxation is a major concern when both the U.S. and the country of residence claim the right to tax the same assets. To address this, the U.S. has estate tax treaties with 15 countries, including France, Germany, the UK, Canada, Australia, and Japan, which help coordinate these overlapping claims. In countries without such treaties, expats may rely on the Foreign Death Tax Credit to offset taxes already paid to the foreign government.

The situation becomes even trickier if your spouse isn’t a U.S. citizen. The unlimited marital deduction – which allows assets to pass tax-free to a surviving spouse – only applies if the surviving spouse is a U.S. citizen. Without a Qualified Domestic Trust (QDOT), transferring assets to a non-citizen spouse could trigger immediate estate taxes, even if the estate’s total value is below the $15 million exemption threshold. On top of that, annual gifts to a non-U.S. citizen spouse are capped at $194,000 for 2026, compared to unlimited gifting between U.S. citizen spouses.

These rules highlight the intricate planning required for U.S. expats to navigate both domestic and international tax obligations effectively.

sbb-itb-39d39a6

Estate Planning Tools for US Expats

Navigating estate planning as a US expat can feel like solving a puzzle with pieces scattered across borders. The process requires tools that work seamlessly within both US and foreign legal frameworks. Your choice of tools will depend on factors like the location of your assets, your spouse’s citizenship, and the laws in your host country.

Using Dual Wills for US and Foreign Assets

Managing assets in multiple countries often complicates probate. Dual wills, also known as "situs wills", offer a practical solution. Instead of relying on a single US will that may not be enforceable abroad, you create separate wills for assets in different jurisdictions. This approach allows probate to proceed simultaneously in each country, speeding up the process.

For example, without a US-resident executor, the IRS requires a transfer certificate to confirm estate taxes are paid before releasing US assets. This step can delay the process by over a year. A well-structured US will can help avoid such delays.

However, dual wills come with risks. As attorney Allison E. Dolzani from Ruchelman PLLC points out:

"A foreign Will alone may not effectively administer U.S. assets, while a U.S. Will drafted in isolation can unintentionally disrupt an existing foreign estate plan".

To prevent issues, your US will should clearly state it applies only to US-based assets. Similarly, any new will – whether in the US or abroad – should explicitly confirm it does not revoke the other.

| Feature | Single Will (Global) | Dual/Situs Wills |

|---|---|---|

| Probate Speed | Slower; often requires translations and sequential processing | Faster; allows simultaneous administration in different countries |

| Legal Recognition | May face challenges in civil law jurisdictions | Tailored to specific local laws for better recognition |

| Administrative Cost | Higher ongoing costs due to legal complexities | Higher initial drafting costs but lower probate expenses long-term |

Revocable and Irrevocable Trusts, Including Offshore Options

Trusts play a key role in estate planning, offering benefits like probate avoidance and asset management. However, their effectiveness depends on the type of trust and where it’s used.

- Revocable Trusts: These allow flexibility and control but do not reduce your taxable estate. With the federal estate tax exemption set at $15 million per individual in 2026, high-net-worth expats above this threshold won’t see tax benefits from a revocable trust.

- Irrevocable Trusts: These remove assets from your taxable estate, potentially reducing exposure to the 40% federal estate tax. However, they require you to give up control over the assets.

If your spouse isn’t a US citizen, you may need a Qualified Domestic Trust (QDOT) to defer estate taxes, as the unlimited marital deduction only applies to US citizen spouses.

It’s important to note that many civil law countries – such as France, Germany, Spain, and Italy – don’t recognize trusts as legal entities. Nicola Saccardo, a partner at Charles Russell Speechlys LLP, explains:

"In some countries the creation of a revocable trust may be taxed as a gift, despite the fact that in the USA it will be treated as a grantor trust".

For example, in the UK, a US revocable trust could be treated as a non-grantor trust, subjecting worldwide income to immediate UK taxation. Because restructuring trusts after moving abroad can be difficult, it’s crucial to consult legal experts familiar with both US and foreign laws before setting up a trust.

Powers of Attorney and Advance Health Care Directives

Wills and trusts are just part of the estate planning equation. Powers of attorney and advance health care directives are equally important, especially for expats. These documents ensure your financial and medical affairs are handled if you become incapacitated.

- Power of Attorney: Grants someone authority to manage your financial matters, such as paying bills, accessing accounts, or selling property.

- Advance Health Care Directive: Specifies your medical treatment preferences and appoints someone to make health decisions on your behalf.

For expats, the challenge lies in jurisdictional recognition. Local institutions may not accept US documents without proper authentication, and US institutions might reject foreign documents for assets located stateside. To avoid complications, it’s wise to maintain versions tailored to each jurisdiction where you have significant assets or spend considerable time. Keep originals accessible in each country to ensure quick action during emergencies.

Using Offshore Trusts for Asset Protection

Offshore trusts can be a powerful tool for safeguarding assets, thanks to the protection offered under foreign jurisdictions. Setting up an offshore trust in places like the Cook Islands, Nevis, or Anguilla involves transferring ownership of your assets to a foreign trustee. These trustees manage the assets under local laws, creating a legal barrier – or "jurisdictional firewall" – that U.S. courts generally cannot penetrate. This makes it much harder for creditors to seize those assets.

Here’s how it works: If a creditor secures a judgment in the U.S., they often need to re-litigate the case in the foreign jurisdiction where the trust is established. Many offshore trust jurisdictions, such as the Cook Islands, do not recognize U.S. court orders. Additionally, creditors face significant hurdles. For example, in the Cook Islands, they must post a $50,000 litigation bond and prove fraudulent transfers under strict legal standards – all within a very short one- to two-year timeframe.

Attorney Brian T. Bradley from Bradley Legal Corp highlights the importance of functionality over appearance when it comes to asset protection:

"The key question is never whether a structure looks impressive in an estate planning binder. The real question is whether it survives when a creditor’s attorney, a federal bankruptcy trustee, or a family-court judge attempts to enforce a judgment."

While offshore trusts offer asset protection, they come with compliance obligations. U.S. citizens must file several IRS forms, including Forms 3520, 3520-A, FinCEN Form 114 (FBAR), and Form 8938, as they remain subject to worldwide taxation. Additionally, the costs can be significant. Offshore trusts typically require at least $250,000 in assets to justify the upfront legal fees, ongoing trustee expenses, and tax preparation costs.

Timing is crucial. To avoid legal complications, establish the trust before facing any legal threats, as transferring assets after a claim arises could be deemed fraudulent. It’s also essential to appoint a licensed, independent foreign trustee – not a U.S. citizen or entity connected to the U.S. – to maintain the "impossibility defense" if repatriation of assets is demanded. Jurisdictions like Anguilla, the Cook Islands, and Nevis are often chosen for their political stability, strong legal frameworks, and effective asset protection measures.

Reducing Double Taxation Through Tax Treaties and Credits

The United States taxes its citizens on worldwide assets, no matter where they live. This approach can lead to estates being taxed twice – once in the US and again in another country. Thankfully, tax treaties and foreign tax credits offer ways to ease or even eliminate this issue.

The US has estate and gift tax treaties with only 15 countries, a much smaller network compared to its 60+ income tax treaties. These treaties help determine your primary domicile, define where assets are located (known as their "situs"), and decide which country has the right to tax those assets. For instance, under the US-UK treaty, UK residents can see their unified credit increase from $60,000 (the standard exemption for foreign residents) to the full amount available to US citizens – $13.99 million in 2025. Additionally, treaties with countries like the UK, Denmark, and Germany may allow marital deductions for transfers to non-US citizen spouses, a benefit not typically available otherwise. These provisions are crucial in reducing overlapping taxes.

When tax treaties aren’t in place, foreign tax credits become essential. Without a treaty, you can use the Foreign Tax Credit (filed on Form 1116) to offset US estate tax. Unused credits can even be carried back one year or forward for up to 10 years. This credit directly reduces your US tax liability on a dollar-for-dollar basis, which makes it significantly more advantageous than a deduction.

International Tax Attorney Anthony Diosdi highlights the issue:

"One of the main arguments against an inheritance tax is that it, and the estate tax, essentially serves as double taxation on a deceased person’s wealth."

To utilize treaty benefits, filing Form 8833 (Treaty-Based Return Position Disclosure) with your estate tax return is required – these benefits aren’t granted automatically. This process is a critical part of a well-thought-out multi-jurisdictional estate plan. It’s also vital to coordinate your wills carefully to ensure they align with treaty provisions. Additionally, be mindful of local "deemed domicile" rules, as spending too much time in certain European countries could subject your worldwide assets to local inheritance taxes, even if you’re a US citizen.

Dealing with Probate Delays and Forced Heirship Laws

Handling assets across multiple countries can lead to some frustrating hurdles, especially when it comes to probate and inheritance laws. Here’s the deal: if you own assets in more than one country, you’re looking at separate probate processes for movable assets (which follow the laws of your domicile) and immovable assets (which require local probate). Add to that the complications of forced heirship laws – rules that might dictate who inherits your estate, regardless of your wishes – and things can get even trickier. On top of it all, conflicting document requirements between jurisdictions can slow everything down even further.

These challenges mean you need to plan carefully, keeping the specific laws of each jurisdiction in mind. For example, forced heirship laws in many countries ensure that a significant portion of your estate is automatically reserved for certain heirs, potentially overriding your intentions. Courts in these jurisdictions may divide your property based on their rules, not your preferences. In the UAE, for instance, Sharia-based inheritance laws apply by default, though expats may have the option to opt out under certain conditions.

So, how do you navigate these roadblocks? Strategic planning tools can help you minimize delays and ensure your wishes are respected. One option is drafting separate situs wills for each key jurisdiction. These wills should comply with local laws and include provisions to prevent a foreign will from invalidating your US will. If you’re an expat in most EU countries, you might benefit from the European Succession Regulation (Brussels IV), which allows you to elect your US state’s law to govern your entire estate. This can help you avoid local forced heirship rules.

For assets that can bypass probate altogether, consider setting up beneficiary designations, Transfer-on-Death accounts, or joint ownership with survivorship rights. Just make sure your host country recognizes these arrangements to avoid any surprises.

How to Create a Multi-Jurisdictional Estate Plan

Start by making a detailed inventory of your assets across different countries – this includes real estate, bank accounts, investments, pensions, and business interests. This step helps you pinpoint which jurisdictions apply to your estate planning needs. Next, determine your legal domicile and residency. These factors usually dictate which succession and tax laws will govern your estate, as your domicile serves as your permanent home.

When drafting wills, ensure they are coordinated. You can either create an international will that covers everything or separate wills for specific jurisdictions. Just make sure they don’t conflict or accidentally revoke one another.

If your estate involves US trusts, check how foreign countries recognize them. Some civil law nations may either disregard these trusts or impose steep taxes on them. Additionally, review estate or gift tax treaties to avoid double taxation. To prevent your heirs from facing financial strain, maintain liquidity through cash reserves or life insurance to cover probate fees and inheritance taxes. Lastly, establish universally valid Powers of Attorney and healthcare directives for smoother administration across jurisdictions.

Revocable vs. Irrevocable Trusts Comparison

Here’s a quick breakdown of the differences between revocable and irrevocable trusts:

| Feature | Revocable Trust | Irrevocable Trust |

|---|---|---|

| Tax Benefits | Minimal; assets stay in the settlor’s taxable estate | Can remove assets from the estate, reducing estate tax |

| Asset Protection | Weak; creditors can access the assets | Strong; generally protected from creditors |

| Flexibility | High; can be modified or revoked anytime | Low; changes are challenging once established |

| Best Use Case | Avoiding probate and retaining control over US-based assets | Long-term wealth transfer and reducing estate tax exposure |

| Foreign Recognition | Often ignored or heavily taxed in civil law countries | May trigger immediate gift taxes in some jurisdictions |

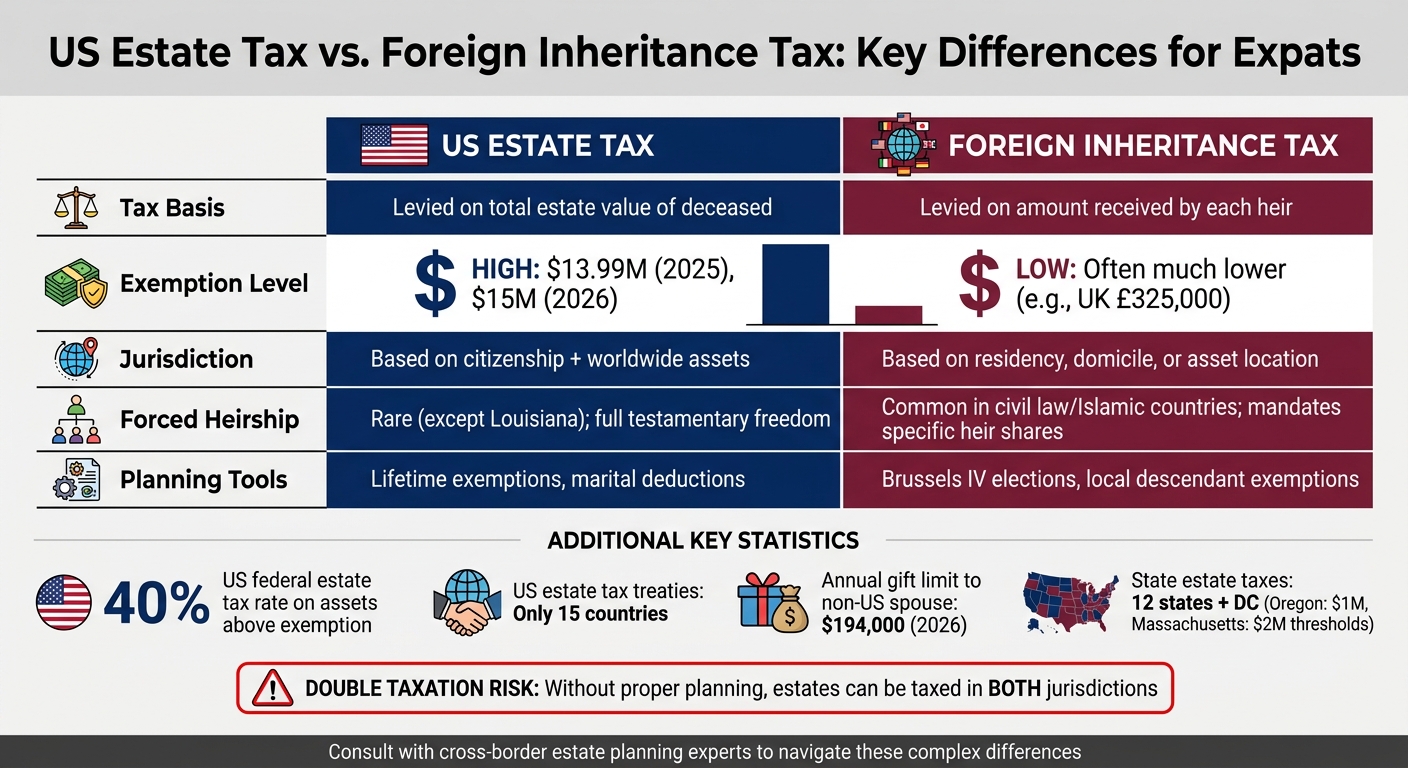

US Estate Tax vs. Foreign Inheritance Tax Comparison

Understanding the differences between US estate tax and inheritance taxes in other countries is crucial for effective planning:

| Feature | US Estate Tax | Foreign Inheritance Tax (Common Expat Destinations) |

|---|---|---|

| Tax Basis | Based on the total value of the deceased’s estate | Typically levied on the amount received by each heir |

| Exemption Level | High (e.g., $13.99 million in 2025; projected $15 million in 2026) | Often much lower (e.g., UK threshold is £325,000) |

| Jurisdiction | Applies to citizenship and worldwide assets | Usually tied to residency, domicile, or asset location |

| Forced Heirship | Rare (except in Louisiana); allows full testamentary freedom | Common in civil law or Islamic countries; mandates specific shares for heirs |

| Planning Opportunity | Use lifetime exemptions and marital deductions | Options like "Brussels IV" elections or local exemptions for descendants |

This information highlights the importance of understanding local laws and tax systems when managing an international estate. Thoughtful planning can help you navigate these complexities and ensure your assets are distributed according to your wishes.

Conclusion

International estate planning requires careful attention to detail and a well-coordinated approach. For U.S. expats, the challenges are unique and often complex. From managing situs wills across multiple jurisdictions to utilizing the 15 U.S. estate tax treaties to avoid double taxation, the stakes are high and demand specialized strategies. Without proper coordination, your heirs could face unnecessary delays in probate, forced heirship complications, and steep tax liabilities.

The urgency of proactive planning cannot be overstated, especially with the federal estate tax exemption set to change in 2026, likely reducing current protections significantly. Tools like Qualified Domestic Trusts (QDOTs), offshore trusts, and jurisdiction-specific Powers of Attorney – discussed earlier – are essential for safeguarding your assets and ensuring your wishes are respected across borders.

"International estate planning helps expatriates protect property, manage cross-border assets, and secure their legacy worldwide." – Premier Title, DK Law Group

Your global estate requires a customized plan that accounts for changing tax laws and the complexities of multiple legal systems. The intersection of U.S. taxation and foreign inheritance laws makes this process challenging, but it’s critical to act decisively. With U.S. worldwide taxation, foreign inheritance rules, and reporting requirements like FBAR and FATCA in play, expert advice tailored to your situation is essential. Global Wealth Protection offers personalized consultations to assess your global assets, coordinate with local legal experts, and implement strategies to reduce taxes while maintaining compliance in every jurisdiction where you hold assets.

Don’t wait – take steps now to secure your legacy and protect your heirs from unnecessary legal and financial hurdles. Schedule a complimentary consultation with Global Wealth Protection to create a comprehensive, cross-border estate plan tailored to your goals.

FAQs

How do I know which country can tax my estate?

The country that can tax your estate is influenced by three main factors: your domicile, the location (situs) of your assets, and any relevant tax treaties. Your domicile typically determines whether a country can tax your entire estate globally. Meanwhile, the situs of specific assets, such as real estate or bank accounts, may expose them to local taxation. Tax treaties can play a crucial role in clarifying or mitigating the risk of being taxed in multiple jurisdictions. It’s always wise to seek professional advice for tailored guidance.

Do I need two wills if I own assets in another country?

Yes, if you own assets in another country, having two wills can often be a smart move. A will drafted in a foreign country may not adequately cover assets located in the U.S., and the reverse is also true. By creating separate wills tailored to each jurisdiction, you can ensure your assets are managed correctly, avoid potential legal disputes, and prevent one will from unintentionally canceling out the other.

What happens if my spouse isn’t a U.S. citizen?

If your spouse isn’t a U.S. citizen, they may not be eligible for the unlimited marital deduction. This can complicate estate tax planning and potentially increase tax liabilities. To address this, you might need to explore options like creating specific types of trusts to help reduce U.S. gift and estate taxes. It’s essential to work with a qualified professional to ensure your plan aligns with legal requirements and meets your financial goals.