Offshore companies must follow strict Anti-Money Laundering (AML) rules to avoid severe penalties like fines, jail time, or losing banking access. Here’s a quick overview of how they manage compliance:

- Customer Due Diligence (CDD): Verifying identities, tracking funds, and screening for risks.

- Global Standards: Following FATF’s 40 Recommendations, transparency rules, and the Common Reporting Standard (CRS).

- Jurisdiction-Specific Rules: Regulations differ by location (e.g., Cayman Islands, UK, Singapore), with varying fines and prison terms.

- AML Programs: Companies appoint compliance officers, monitor transactions, and file Suspicious Activity Reports (SARs).

- Technology Use: AI and machine learning improve monitoring, reduce errors, and speed up compliance tasks.

- Training: Employees are trained to spot risks and follow reporting procedures.

Non-compliance risks include fines reaching millions, up to 20 years in prison, and reputational damage. Offshore companies need a mix of advanced tools and skilled professionals to meet evolving global standards.

Global AML Standards and Regulations

International AML Frameworks

The Financial Action Task Force (FATF) sets the global standard for anti-money laundering (AML) practices with its 40 Recommendations. These guidelines serve as a foundation for offshore companies, including those managed through a private family office, no matter where they operate. According to FATF:

The FATF Recommendations are the basis on which all countries should meet the shared objective of tackling money laundering, terrorist financing and the financing of proliferation.

Key requirements include Customer Due Diligence (CDD), Enhanced Due Diligence (EDD) for high-risk clients like Politically Exposed Persons (PEPs), and a mandate to retain records for at least five years. FATF Recommendations 24 and 25 emphasize transparency, requiring countries to ensure "adequate, accurate, and up-to-date" beneficial ownership information is accessible to authorities.

Complementing FATF guidelines, the Common Reporting Standard (CRS) supports automatic tax information exchange. Most offshore jurisdictions define a beneficial owner as anyone owning or controlling 25% or more of an entity.

In 2023, the Court of Justice of the European Union (CJEU) ruled that unrestricted public access to beneficial ownership registers was excessive. The court explained:

Full public access [to beneficial ownership registers] is neither ‘strictly necessary nor proportionate to the objective pursued’, and it may not even add anything to the fight against financial crime.

This decision led jurisdictions like Jersey, the British Virgin Islands (BVI), and the Isle of Man to adopt a "legitimate interest" approach instead of full public disclosure. Starting February 2025, the Cayman Islands will allow journalists and researchers to request access to beneficial ownership data if they can demonstrate a connection to money laundering or terrorist financing. Fees for these requests are $37 for one legal entity or $122 for multiple entities.

These global frameworks provide a baseline, but individual jurisdictions interpret and implement them differently, as explored below.

AML Regulations by Jurisdiction

Before diving into jurisdiction-specific rules, it’s important to understand how these international standards influence local regulations. Offshore companies must navigate these requirements to align with broader AML principles.

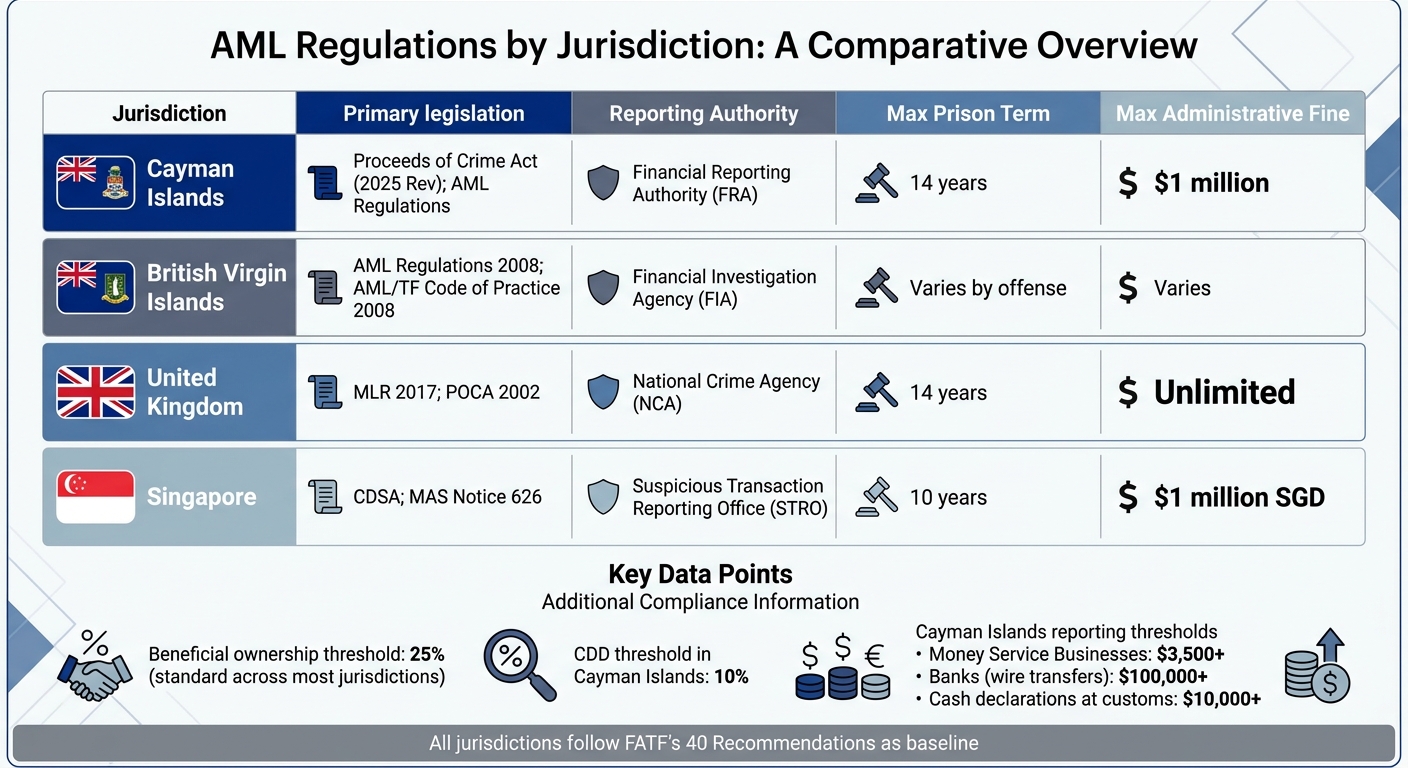

While most offshore jurisdictions adhere to FATF’s 40 Recommendations, their local applications vary. Here’s a snapshot of how some key jurisdictions structure their AML frameworks:

| Jurisdiction | Primary AML Legislation | Reporting Authority (FIU) | Max Prison Term | Max Administrative Fine |

|---|---|---|---|---|

| Cayman Islands | Proceeds of Crime Act (2025 Rev); AML Regulations | Financial Reporting Authority (FRA) | 14 years | $1 million |

| British Virgin Islands | AML Regulations 2008; AML/TF Code of Practice 2008 | Financial Investigation Agency (FIA) | Varies by offense | Varies |

| United Kingdom | MLR 2017; POCA 2002 | National Crime Agency (NCA) | 14 years | Unlimited |

| Singapore | CDSA; MAS Notice 626 | Suspicious Transaction Reporting Office (STRO) | 10 years | $1 million SGD |

The Cayman Islands, under its 2025 Revised Proceeds of Crime Act and AML Regulations, highlights how requirements can differ even within a single jurisdiction. For instance, while CDD applies to stakes as low as 10%, beneficial ownership registration is set at a 25% threshold. Reporting thresholds also vary: Money Service Businesses must report transfers over $3,500, while banks report wire transfers exceeding $100,000.

In November 2022, the Grand Court of the Cayman Islands fined a mutual fund administrator $5.1 million for AML violations. This case underscores the financial risks of non-compliance. A review by the Cayman Islands Monetary Authority (CIMA) revealed that 79% of securities investment businesses had policy gaps, and 33% lacked adequate AML training programs.

The Cayman Islands has also introduced a "Restrictions Notice" system. If a company fails to provide beneficial ownership information, this notice makes any transfer of interest void and blocks payments except in liquidation. Companies must update their Beneficial Ownership Register within 30 days of any change to avoid penalties.

For offshore companies operating across multiple jurisdictions, conducting gap analysis is essential to comply with varying local laws. For personalized guidance on navigating these complexities, consider private consultations to ensure your structure remains compliant. Banks often enforce stricter CDD processes than formation agents, resulting in account opening timelines of 4 to 12 weeks for offshore structures. Meanwhile, recent EU directives (5th and 6th AMLD) have expanded AML regulations to include crypto-asset service providers.

sbb-itb-39d39a6

Building an AML Compliance Program

Every offshore company must have a structured Anti-Money Laundering (AML) compliance program in place to meet regulatory requirements and avoid hefty penalties. A key step is appointing a compliance officer, often referred to as a Money Laundering Reporting Officer (MLRO). This individual has the authority to enforce policies, manage audits, and act as the primary contact for regulators.

Clear internal policies are essential and should cover areas like customer identification, due diligence, transaction monitoring, and reporting procedures. A risk-based approach is critical, meaning risks are assessed and mitigated based on factors like customer profiles, geographic exposure, and the types of products or services offered.

To ensure the program is effective, periodic independent audits are vital. These audits, typically conducted every 12 to 18 months, help identify any gaps. For instance, TD Bank faced penalties of $3.1 billion in 2024 for failing to meet AML requirements. Similarly, NatWest was fined £264 million in 2021 by the UK Financial Conduct Authority for inadequate controls.

Regular staff training is another critical component, ensuring employees can recognize red flags and understand their legal responsibilities. Most jurisdictions require financial institutions to retain customer due diligence (CDD) and transaction records for at least five years. Additionally, companies generally have 30 to 60 days to file a Suspicious Activity Report (SAR) once suspicious activity is detected.

Customer Due Diligence (CDD) Procedures

Customer Due Diligence (CDD) is the process of verifying the identities of customers and beneficial owners before establishing a business relationship. For offshore companies, this verification happens at multiple stages, such as entity formation, bank account setup, and ongoing monitoring. Typically, a beneficial owner is anyone with 25% or more ownership or control of an entity.

Verification should rely on trustworthy, independent sources like government-issued IDs, passports, or notarized documents. To reduce errors and prevent fraud, the "four-eye" principle is recommended, where a second person reviews identification documents and data entries. Always trace ownership back to a natural person; a legal entity cannot be the final beneficial owner.

Offshore companies must also document both Source of Funds (SoF) and Source of Wealth (SoW). SoF refers to the origin of the funds used in specific transactions, while SoW explains how the beneficial owner accumulated their overall wealth. For higher-risk clients, such as Politically Exposed Persons (PEPs) or entities in regions flagged by the Financial Action Task Force (FATF), Enhanced Due Diligence (EDD) is required. This involves more in-depth investigations and more frequent reviews.

| Feature | Customer Due Diligence (CDD) | Enhanced Due Diligence (EDD) |

|---|---|---|

| Applicability | Standard for all new clients/entities | Required for high-risk clients (PEPs, high-risk jurisdictions) |

| Verification | Identity and UBO (25% threshold) | Deeper dive into Source of Wealth and complex structures |

| Monitoring | Periodic review (every 3–5 years) | Frequent or continuous review (annually) |

| Documentation | Passport, proof of address, bank reference | Professional references, detailed business plans, SoW evidence |

CDD information should be updated regularly based on risk levels: annually for high-risk clients, every three years for medium-risk, and every five years for low-risk.

Transaction Monitoring Systems

Once clients are verified, the next step is implementing systems to monitor transactions for suspicious activity. These systems combine automated tools and manual reviews to detect unusual patterns. Automated monitoring can identify behaviors like structuring (breaking large transactions into smaller amounts to avoid reporting limits) and layering (transferring funds through multiple accounts to obscure their origin). Manual reviews are essential for handling more complex cases that require judgment.

In the Cayman Islands, banks must report all wire transfers of $100,000 or more monthly, while money service businesses report transactions exceeding $3,500 – either as a single transfer or cumulative transactions by the same individual within a month. Additionally, individuals carrying $10,000 or more in cash when entering or leaving the Cayman Islands must declare it to customs.

Monitoring systems should also screen all counterparties against sanctions lists, including those maintained by OFAC, the UN, and the EU, in real time. For cross-border wire transfers, intermediary service providers must flag transactions that lack required payer or payee details. Internal reporting processes should allow employees to quickly alert the MLRO about suspicious activities.

Keep due diligence records updated whenever there are material changes, such as new beneficial owners or negative media coverage. Document every decision, whether a transaction is cleared or reported, to demonstrate compliance during audits. Importantly, never inform customers that a SAR has been filed or that their transactions are under review, as "tipping off" is a criminal offense in most jurisdictions.

Record-Keeping and Reporting Requirements

Effective AML programs depend on thorough record-keeping and timely reporting of suspicious activities. Financial institutions are typically required to retain CDD and transaction records for at least five years. These records include identification documents, correspondence, account files, and details about the business relationship.

When suspicious activity is identified, companies must file a Suspicious Activity Report (SAR) or Suspicious Transaction Report (STR) with the appropriate regulatory body. The specific authority varies by country – for example, the National Crime Agency (NCA) in the UK, the Financial Reporting Authority (FRA) in the Cayman Islands, and FinCEN in the US. Companies generally have 30 to 60 days to file once a suspicion arises.

Failing to maintain proper records can lead to severe penalties. For example, in 2019, Westpac was fined $1.3 billion for failing to report 23 million AML violations, while Capital One faced a $390 million fine for unreported transactions totaling $16 billion. In the UAE, fines for non-compliance with record-keeping can range from AED 50,000 to AED 5,000,000.

To ensure compliance, companies should appoint both an Anti-Money Laundering Compliance Officer (AMLCO) to oversee procedures and an MLRO to handle suspicious activity reports. As HPT Group aptly puts it:

Anti-money laundering compliance is the operating system of the offshore world. – HPT Group

Offshore entities are strictly barred from forming correspondent banking relationships with "shell banks" – institutions that lack a physical presence or proper supervision in their licensed jurisdiction. In the Cayman Islands, fines for serious regulatory breaches can reach up to $1 million, and money laundering offenses carry a maximum sentence of 14 years imprisonment.

Technology and Training for AML Compliance

After setting up sturdy AML systems, offshore companies are now leaning on advanced technology and targeted training to strengthen compliance efforts. Tools like artificial intelligence (AI) and machine learning (ML) are becoming indispensable for managing the massive data requirements of modern AML processes. AI, for example, can process intricate ownership structures with 10+ layers in under 60 seconds, a task that could take a human analyst 40 to 60 hours to complete manually. This speed matters, especially since opaque ownership structures contribute to 70% of global money laundering transactions.

Machine learning, on the other hand, helps reduce false positives by learning from past data and adapting to new criminal tactics. These systems boast accuracy rates above 95% and can cut false positives by as much as 85%. A KPMG report highlights the role of AI in AML:

AI is best understood as a powerful tool that enhances human capabilities – freeing professionals from routine tasks so they can focus on higher-order analysis and decision-making.

This blend of technology and human oversight is reshaping compliance strategies and making room for more focused training programs. Employees now need to understand not only how to respond to flagged transactions but also why alerts are triggered. Training must emphasize KYC (Know Your Customer) and CDD (Customer Due Diligence) principles while addressing risks unique to offshore operations, such as identifying Ultimate Beneficial Owners (UBOs) in layered structures and handling Politically Exposed Persons (PEPs).

AI-Powered Compliance Tools

Natural Language Processing (NLP) has revolutionized how offshore firms gather intelligence on UBOs. By scanning news articles, corporate registries, and even social media, NLP tools can flag potential red flags with over 90% accuracy. This is especially helpful when dealing with deliberate obfuscation tactics like misspelled names or the use of shell companies.

Another game-changer is entity resolution, which links records of individuals appearing under slightly varied names or addresses across multiple databases. Paired with network graph analysis, these tools map out indirect control structures, revealing hidden relationships through shared directorships, addresses, or shareholdings. For offshore companies navigating multiple jurisdictions, these technologies are vital for meeting varied compliance thresholds.

Real-time sanctions screening is now a standard feature. AI tools continuously check counterparties against sanctions lists from OFAC, the UN, and the EU, adapting to shifting geopolitical landscapes. The EU’s centralized UBO registries and new Anti-Money Laundering Authority (AMLA) streamline this process by providing standardized data sources, eliminating the need to rely on fragmented manual records. For cryptocurrency transactions, AI-driven blockchain analytics help offshore firms comply with the FATF "Travel Rule", which mandates sender and recipient details for cross-border payments exceeding $1,000.

However, effective AI implementation requires a "human-in-the-loop" approach. While AI handles data collection, pattern recognition, and risk scoring, compliance officers provide critical judgment and ethical oversight. Embedding IT experts within compliance teams ensures proper model validation and data accuracy. Additionally, platforms with configurable thresholds and explainable AI (XAI) features are becoming essential, as regulators increasingly demand transparency in how automated systems flag high-risk activities.

Employee Training Programs

Even with cutting-edge AI tools, well-trained employees remain critical to effective AML compliance. Offshore companies must offer role-specific training tailored to the needs of front-line staff, accountants, and senior management. As Visbanking notes:

Generic, check-the-box training is no longer a defensible position.

For instance, customer service representatives should be trained to spot structuring and layering tactics in real time, while compliance officers need to know how to file Suspicious Activity Reports (SARs) and avoid "tipping off" clients.

Training programs must also address emerging threats. By 2025 and 2026, modules on AI-driven fraud schemes and cryptocurrency risks will become standard, as criminals begin leveraging the same technologies used by compliance teams. Scenario-based learning and gamification are proving effective in boosting retention, immersing employees in realistic scenarios like identifying a PEP attempting to obscure their status through layered ownership.

Given the fast-changing nature of regulations and criminal tactics, training needs annual updates to stay relevant and audit-ready. Online learning platforms provide global teams with flexibility, allowing for remote, self-paced education while maintaining consistent standards. Digital tracking systems ensure 100% verifiable completion data, which regulators often require during inspections. For key personnel, obtaining certifications like the Certified Anti-Money Laundering Specialist (CAMS) – priced around $1,199 to $1,499 – demonstrates "fit and proper" status to regulators and reinforces an institution’s commitment to compliance.

Visbanking emphasizes this point:

Effective anti money laundering training is not an HR function; it is a core component of risk management and institutional stability.

With financial institutions facing $8.9 billion in AML penalties in 2019 alone, investing in robust training programs is more than just a good idea – it’s a necessity. For offshore companies, especially those in high-risk jurisdictions, treating employee education as a mere formality could lead to costly regulatory and reputational fallout.

AML Compliance Best Practices

Offshore companies must adopt AML frameworks that go beyond superficial compliance. As Miriam Smyth from Appleby points out:

AML/CFT compliance cannot be a ‘box-ticking’ exercise. CIMA expects firms to have a robust and effective AML/CFT compliance framework in place.

True compliance integrates across the entire lifecycle of a company – from formation and bank account setup to continuous monitoring and reporting. This includes verifying the identities of beneficial owners, directors, and officers, as well as documenting the Source of Wealth (how overall wealth was accumulated) and the Source of Funds (origin of specific money used).

A risk-based approach is crucial. Offshore firms should allocate more effort and resources to high-risk clients, such as Politically Exposed Persons (PEPs), entities in high-risk jurisdictions, or those with complex, layered structures. Standard controls can be applied to low-risk clients. For example, Customer Due Diligence (CDD) documentation should be refreshed:

- Annually for high-risk clients

- Every three years for medium-risk clients

- Every five years for low-risk clients

Automated systems can also flag "event-driven" reviews when significant changes – like new ownership or negative media coverage – occur. Meanwhile, manual processes are better suited for periodic updates. This approach ensures AML compliance stays consistent from onboarding through ongoing client monitoring.

Dedicated officers play a key role in maintaining compliance. Every offshore company should appoint an Anti-Money Laundering Compliance Officer (AMLCO) and a Money Laundering Reporting Officer (MLRO). These officers oversee compliance, file Suspicious Activity Reports (SARs), and ensure employees avoid "tipping off" clients under investigation – a serious offense in jurisdictions like the UK, Cayman Islands, and BVI. Regular independent audits of both automated tools and manual policies can help close gaps. Additionally, AML policies should be reviewed at the board level at least once a year.

The risks of non-compliance are severe. As noted, "Non-compliance does not merely result in fines – it creates criminal liability for the individuals involved, loss of banking relationships, and potential dissolution of the structure itself". With criminals laundering an estimated €715 billion to €1.87 trillion annually (about 2-5% of global GDP), offshore companies cannot afford to cut corners on AML frameworks.

Manual vs. Automated Compliance Processes

Effective AML compliance requires a balance between automation and human judgment. Automated systems excel at processing large data sets, monitoring transactions in real time, and screening against global sanctions lists – tasks where human error is common. For instance, software can instantly check all parties against OFAC, EU, and UN sanctions lists, ensuring up-to-date compliance as global conditions change. Automation works well for low- to medium-risk tasks like initial Know Your Customer (KYC) checks and routine screenings, leaving compliance teams free to handle complex cases.

However, manual oversight is vital for nuanced decision-making, especially in complex offshore structures where ownership may be hidden behind layers of entities. While automated tools can flag suspicious activity, decisions like filing a Suspicious Activity Report require careful review by an MLRO to ensure proper reasoning and avoid accidental "tipping off". High-risk scenarios – like those involving PEPs or countries on the FATF grey or blacklists – demand human expertise to interpret complexities that algorithms may overlook.

A hybrid model is the most effective strategy. Automation provides speed and consistency, while human analysts bring ethical oversight and contextual understanding, which regulators increasingly expect. The table below compares the strengths and challenges of each approach.

Markdown Comparison Table

| Tool Type | Features | Compliance Benefits | Implementation Challenges |

|---|---|---|---|

| Manual | Human oversight, flexibility, context-based analysis | Ideal for complex cases and interpreting unusual circumstances | Time-intensive (4-12 weeks for bank onboarding), prone to error, hard to scale |

| Automated | AI-driven, scalable, real-time monitoring | Fast anomaly detection and consistent sanctions list screening | Expensive upfront, requires technical expertise, needs human input for final decisions |

Conclusion

Offshore companies are now required to meet stringent AML (Anti-Money Laundering) compliance standards to operate within today’s increasingly transparent financial systems. The era of anonymous corporate structures has passed. Modern offshore entities must maintain clear records of beneficial ownership, demonstrate genuine economic activity through physical offices and local employees, and implement monitoring systems that go far beyond superficial compliance checks.

Failing to comply with these regulations carries severe consequences. Penalties include lengthy prison sentences – up to 14 years in the UK and Cayman Islands, and up to 20 years in the US – as well as fines that can reach millions of dollars. Beyond the legal risks, companies may lose critical banking relationships or even face dissolution. For instance, in December 2021, the UK Financial Conduct Authority imposed a £264.8 million fine on NatWest for failing to monitor a client who deposited around £365 million over five years.

Effective compliance requires a balanced approach that combines advanced technology with human expertise. AI-powered tools can handle tasks like real-time transaction monitoring, sanctions screening, and identifying suspicious patterns. Meanwhile, trained professionals are essential for making judgment calls in high-risk situations. Offshore firms should also regularly update Customer Due Diligence (CDD): annually for high-risk clients, every three years for medium-risk clients, and every five years for low-risk entities. This dual approach is essential as regulatory requirements grow more complex.

The regulatory landscape itself is constantly evolving. Global standards, such as the CRS and FATF Travel Rule for crypto-assets, require offshore companies to continually adapt their compliance practices. As Angel Gurría, former Secretary-General of the OECD, aptly noted:

Offshore tax evasion is over. Countries are now exchanging financial account information automatically.

To stay ahead, offshore companies must invest in advanced technology, experienced compliance personnel, and ongoing AML measures. Those who prioritize transparency and proactive compliance today will be better equipped to navigate tomorrow’s regulatory challenges. These efforts not only ensure adherence to global standards but also lay the groundwork for long-term operational stability and success.

FAQs

What AML tasks do banks require that formation agents may not?

Banks are known for conducting thorough anti-money laundering (AML) due diligence. This includes steps like verifying customer identities, monitoring accounts regularly, and reporting any suspicious activity. On the other hand, formation agents might not follow these processes with the same level of detail or consistency.

When do I need Enhanced Due Diligence (EDD) instead of CDD?

Enhanced Due Diligence (EDD) comes into play when working with customers considered high-risk. This includes groups like politically exposed persons (PEPs), offshore entities, or transactions connected to countries classified as high-risk.

EDD requires a deeper dive into the customer’s profile. This means verifying the source of funds, conducting a more detailed review of their activities, and maintaining ongoing monitoring to ensure compliance with regulatory standards. The goal is to identify and mitigate potential risks tied to these customers effectively.

What AML mistakes most often lead to offshore account closures?

Failing to meet Anti-Money Laundering (AML) requirements can lead to offshore account closures. The most frequent mistakes include skipping proper customer due diligence (CDD), poor record-keeping, and weak transaction monitoring. These missteps often violate international standards like the FATF (Financial Action Task Force) recommendations, exposing accounts to heightened scrutiny or even closure.