When you’re traveling or living abroad, accessing money during emergencies can be tricky. From unexpected medical bills to frozen bank accounts, financial challenges can arise when you least expect them. Here’s how to ensure you’re prepared:

- Open an International Bank Account: These accounts offer access to global ATM networks, multi-currency options, and higher withdrawal limits. Some, like Charles Schwab, even reimburse ATM fees worldwide.

- Use Multi-Currency Wallets: Platforms like Wise or Revolut let you store, convert, and manage over 40 currencies at low fees. They also provide virtual and physical debit cards for global use.

- Plan for ATM Use: Choose ATMs inside bank branches for lower fees and better security. Always withdraw in the local currency to avoid hidden conversion fees.

- Notify Your Bank Before Travel: This prevents account freezes due to suspicious activity.

- Diversify Funds: Carry at least two cards (Visa and Mastercard) and keep some cash ($100 in USD) for emergencies.

- Understand Reporting Requirements: U.S. residents with over $10,000 in foreign accounts must file an FBAR annually.

- Prepare for Emergencies: Keep a backup plan like Western Union or embassy assistance for urgent situations.

Setting Up International Bank Accounts

Having an international bank account ensures quick access to cash during emergencies abroad. For instance, HSBC offers access to over 55,000 ATMs worldwide, while Citibank supports transactions in 144 currencies. Premium accounts often come with perks like higher withdrawal limits – up to £1,000 (around $1,250) daily – and local bank details for fee-free transfers.

Modern security features include two-factor authentication, real-time transaction alerts, and instant card freezing through mobile apps. If your card is compromised, you can lock it immediately and request a replacement. Additionally, some accounts allow you to set up a notarized Power of Attorney, enabling a trusted individual to manage your funds if you’re unable to do so.

Benefits of International Bank Accounts

The main advantage of an international account is access to funds across borders. This reduces the risk of being stranded without cash. For example, Charles Schwab reimburses all international ATM fees and charges no foreign transaction fees, while Capital One 360 Checking offers similar benefits.

Another benefit is multi-currency flexibility. Accounts like Wise let you hold and convert over 40 currencies at mid-market exchange rates, with conversion fees starting at just 0.41%. This feature allows you to exchange money when rates are favorable, avoiding the typical 3–5% markup charged by traditional banks. Wise also offers a 3.14% APY on USD balances for eligible customers as of December 2025, helping your funds grow while they sit idle.

Diversifying your finances by holding funds in different jurisdictions also protects against economic instability in your home country. If a banking crisis, currency devaluation, or political unrest occurs, having an international account ensures access to your money. This is especially important for expatriates or anyone with long-term commitments abroad.

How to Open an International Bank Account

To open an international account, you’ll typically need a valid passport, proof of address (like a utility bill or bank statement), and your Social Security Number or Tax Identification Number to meet FATCA requirements. Some banks may also ask for proof of income or a reference from your current bank.

Digital providers like Wise and Revolut make the process simple, allowing you to upload documents via smartphone. Accounts are often ready within one to two days. Over 60% of Wise transfers are completed instantly, with more than 90% processed within 24 hours.

Traditional banks such as HSBC or Citibank may require you to have an existing relationship – like Premier or Jade status – to open an overseas account from the U.S.. This process can take up to 14 days and may involve notarized documents or in-person visits. However, these banks provide physical branches for in-person support when needed.

"US citizens can open foreign bank accounts with no legal barriers. However, banks themselves decide who they’re willing to offer services to – and not all will serve US customers." – Wise

Before applying, ensure the bank accepts U.S. residents. Some foreign banks avoid U.S. clients due to the reporting obligations under FATCA. Digital platforms like Wise and Revolut are designed to handle compliance for U.S. customers seamlessly.

What U.S. Residents Need to Know

U.S. residents must meet specific regulatory requirements to stay compliant. If the total value of your foreign accounts exceeds $10,000 at any point during the year, you must file an FBAR (Report of Foreign Bank and Financial Accounts) with the Financial Crimes Enforcement Network (FinCEN). This filing is separate from your regular tax return, and failing to file can result in severe penalties.

Under FATCA (Foreign Account Tax Compliance Act), foreign banks are required to report account details of U.S. taxpayers to the IRS. You’ll need to provide your Social Security Number or Tax ID when opening an account to help the bank fulfill these obligations. Choosing a FATCA-compliant institution is crucial to avoid issues like withheld taxes or account closures.

"If you hold over USD10,000 in total in foreign bank accounts at any point in a given year, you need to file a report of Foreign Bank and Financial Accounts – known as FBAR." – Wise

It’s also important to understand deposit insurance. While U.S. accounts are FDIC-insured up to $250,000 per depositor, this protection doesn’t extend to offshore accounts. Check the local deposit insurance policies in the country where you’re opening an account, as coverage limits and terms can vary.

Lastly, be aware of minimum balance requirements. Traditional banks like HSBC Expat may require deposits or investments of £75,000 (about $93,750) to waive their £35 monthly fee. On the other hand, digital providers like Wise and Revolut have no minimum balance requirements, making them more accessible for most people.

sbb-itb-39d39a6

Using Multi-Currency Wallets for Flexibility

A multi-currency wallet acts like a digital bank, letting you store, convert, send, and receive multiple currencies all in one place. Think of it as a streamlined way to handle money across borders without needing to open separate foreign accounts. These wallets often provide local account details for currencies like USD, EUR, GBP, and CAD, making it easy to receive payments as if you were a local in those regions.

The real magic of these wallets shines when you’re traveling or managing international finances. Many are linked to global debit cards, usable at ATMs in over 160 countries. They also feature automatic conversion, which pulls from the most cost-effective currency balance for your transaction – saving you the hassle and expense of manual conversions.

How Multi-Currency Wallets Work

Multi-currency wallets are controlled through mobile apps, giving you instant access to your money. You can hold and manage over 40 different currencies at once. Currency conversions happen instantly at mid-market rates, with fees as low as 0.41%.

Need immediate access to funds? You can generate digital cards in the app and use them right away with Apple Pay or Google Pay. Physical cards are available for a one-time fee of $9, while digital cards are free.

When you’re abroad, these wallets automatically use the correct currency balance for purchases or withdrawals. If the local currency isn’t available, the wallet will convert funds from another balance in a way that minimizes costs.

"Nothing makes cross-border currency management easier than a multi-currency wallet." – Wise

This seamless functionality not only cuts costs but also enhances security, as we’ll explore next.

Advantages of Multi-Currency Wallets

The benefits of multi-currency wallets go beyond convenience – they can save you serious money. Traditional U.S. banks like Bank of America, Chase, and Wells Fargo typically charge $5 plus 3% for international ATM withdrawals. Multi-currency wallets avoid these hefty fees, offering transparent pricing instead.

Another perk? You can convert funds between currencies when exchange rates are favorable and hold onto them until needed. Some providers even offer interest on balances – for example, 3.14% APY on USD balances for eligible users. This means your emergency fund can grow while staying accessible.

Security is another strong point. These wallets let you freeze or unfreeze your card instantly, set custom ATM withdrawal limits, and receive real-time transaction alerts. Plus, they work in over 160 countries and territories. Providers like Wise handle $49 billion every quarter for 14.8 million customers, showcasing their reliability.

One key tip for international transactions: always pay in the local currency instead of USD. Paying in USD often triggers Dynamic Currency Conversion (DCC), which applies inflated exchange rates from merchants or ATM operators, leading to higher costs.

"Always pay in the local currency to get the best available deal with no nasty surprises." – Wise

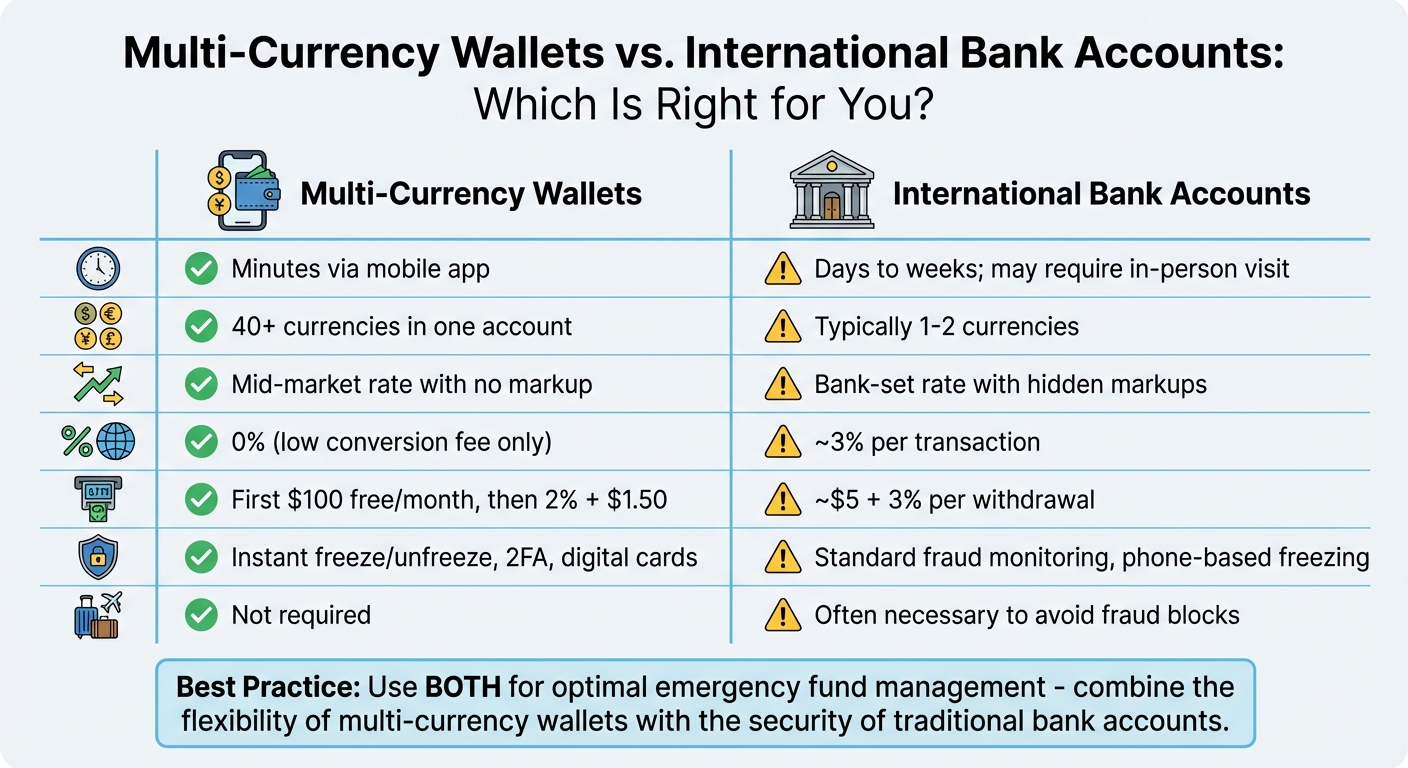

Multi-Currency Wallets vs. International Bank Accounts

Both multi-currency wallets and international bank accounts have their place in managing global finances. Here’s how they compare:

| Feature | Multi-Currency Wallets | International Bank Accounts |

|---|---|---|

| Setup Time | Minutes via mobile app | Days to weeks; may require an in-person visit |

| Currency Support | 40+ currencies in one account | Typically 1–2 currencies |

| Exchange Rate | Mid-market rate with no markup | Bank-set rate with hidden markups |

| Foreign Transaction Fees | 0% (low conversion fee only) | Around 3% per transaction |

| ATM Fees | First $100 free per month, then 2% + $1.50 per withdrawal | About $5 + 3% per withdrawal |

| Security Features | Instant freeze/unfreeze, 2FA, digital cards | Standard fraud monitoring, phone-based freezing |

| Travel Notices | Not required | Often necessary to avoid fraud blocks |

Multi-currency wallets are quick to set up and perfect for fee-efficient, everyday use – an essential tool for emergencies. On the other hand, international bank accounts may provide higher withdrawal limits, in-person support, and FDIC insurance up to $250,000 per depositor. Combining both solutions can give you the best of both worlds: the flexibility of a multi-currency wallet and the security of a traditional bank account. Many people find this dual approach ideal for managing their emergency funds effectively.

Using Global ATM Networks

When you’re abroad and need cash in a pinch, ATMs are a dependable option. Most debit cards are linked to global networks like PLUS (Visa) or Cirrus (Mastercard), giving you access to millions of ATMs worldwide. For example, the Visa Global ATM Locator alone covers over 2 million machines across more than 200 countries and territories.

Before traveling, it’s a good idea to use Visa or Mastercard’s official online locators to find compatible ATMs at your destination. These tools can save you time and frustration. Let’s dive into how you can locate secure ATMs while abroad and avoid unnecessary risks.

Location plays a big role in cost and safety. ATMs located inside bank branches typically have lower fees than those in convenience stores, malls, or airports. Plus, bank branch ATMs offer better security. Concerns about safety are common – 76% of global consumers report feeling uneasy about making cash withdrawals due to security risks.

If your U.S. bank is part of the Global ATM Alliance, you can save significantly on fees. This partnership includes major banks like Bank of America, Barclays, Deutsche Bank, and Scotiabank. For instance, Bank of America customers can use Barclays ATMs in the UK or Westpac ATMs in Australia without paying the usual $5 international withdrawal fee. Now, let’s explore how to locate secure ATMs in foreign destinations.

Finding ATMs in Foreign Countries

When you arrive, GPS-enabled apps can help you quickly locate nearby ATMs. Some fintech apps even include filters for surcharge-free machines, making your search easier. Planning ahead can save you from scrambling for cash in unfamiliar areas.

Stick to ATMs inside bank branches whenever possible. These machines are more secure and often charge lower fees. Before using an ATM, check for signs of tampering, such as loose card slots or unusual attachments. When entering your PIN, cover the keypad with your hand to block hidden cameras or prying eyes.

Be cautious of distractions or unsolicited offers of help near ATMs. If you encounter a problem, stay with your card until the issue is resolved.

How to Minimize ATM Fees

ATM fees can add up quickly, so it’s important to be strategic. U.S. banks like Bank of America, Chase, and Wells Fargo typically charge $5 per international withdrawal, plus a 3% foreign transaction fee. Out-of-network fees range from $2 to $5 per transaction, often with additional operator surcharges.

Always choose to withdraw in the local currency. ATMs may offer to charge you in USD through Dynamic Currency Conversion (DCC), but this often comes with hidden markups as high as 13%. Selecting the local currency ensures your bank handles the conversion, usually at a better rate.

To minimize fees, withdraw larger amounts less frequently, but stay within your daily withdrawal limit for safety. Some banks, like Charles Schwab, reimburse ATM fees worldwide, while Capital One 360 doesn’t charge out-of-network or foreign transaction fees at in-network ATMs.

Avoid using credit cards for ATM withdrawals. These are treated as cash advances, which come with high fees (often 5%) and immediate interest charges. Stick to debit cards linked to your checking account or a multi-currency wallet for ATM transactions.

Here’s a tip: in some countries, you can request "cash back" during a debit card purchase at a retail store. This can bypass ATM fees entirely and is especially useful for smaller amounts when you’re already making a purchase.

Emergency Scenarios and Financial Preparedness

Emergencies – whether it’s a missed flight, a natural disaster, or something in between – often require quick access to cash. Being prepared can make all the difference when systems fail or unexpected expenses arise. Strategies like maintaining international accounts and using multi-currency wallets can help ensure you’re never caught off guard. Let’s explore how to handle some common emergency scenarios.

Travel Emergencies

Travel mishaps like losing your wallet, canceled flights, or medical issues abroad can drain your funds quickly. If you can’t access your accounts, services like Western Union or MoneyGram allow family or friends to send money. These transfers, which typically require a valid ID or passport for pickup, are completed in minutes to hours, making them a fast option for urgent situations.

If commercial services aren’t an option, the U.S. Department of State offers the "OCS Trust" program. This service allows funds to be sent through an embassy or consulate for a $30 fee. Transfers usually take at least 24 hours during regular business hours (Monday–Friday, 8:00 a.m. to 5:00 p.m. ET). Western Union’s "Quick Collect" service also works with the State Department using the code OVERSEASEMERGENCY DC.

To avoid account freezes while traveling, notify your bank and credit card companies of your travel plans in advance. A Harvard student shared this advice:

"Have at least two credit/debit cards abroad. One of my card accounts was frozen, and I would have been in trouble if I hadn’t had a backup".

Carrying at least two cards – one Visa and one Mastercard – is a smart move. Store them separately to avoid losing both at once. It’s also a good idea to keep around $100 in U.S. dollars handy for essentials like transportation or meals if card payments aren’t available. For U.S. citizens, repatriation or EMDA II loans might cover return travel or medical emergencies, but unpaid loans could lead to passport restrictions until they’re repaid.

These steps can help you navigate travel emergencies effectively and lay the groundwork for handling financial challenges when relocating abroad.

Expatriation and Relocation

Moving to a new country comes with its own set of financial hurdles, particularly in the first few weeks before you set up local banking. To avoid being cut off from your funds, consider maintaining accounts with multiple banks and networks.

Daily ATM withdrawal limits, often capped at $500, might not meet your needs in a crisis. Ask your bank for a permanent limit increase or use joint accounts and strategic timing (withdrawing just before and after your bank’s daily reset time) to access more cash. Ideally, aim to have $10,000 available within 24 hours.

Some foreign hospitals may demand full payment upfront for emergency surgeries, even if you have international health insurance. Credit cards can help cover these large expenses, while debit cards are crucial for cash-heavy situations.

To prepare for unexpected events, establish a notarized power of attorney so a trusted family member can manage your accounts if you’re incapacitated. Update your two-factor authentication (2FA) settings to use an app or a phone number that works internationally, ensuring you’re not locked out of your accounts while abroad.

While these tips help with the financial challenges of daily life abroad, broader crises require additional preparation.

Natural Disasters and Crisis Situations

Natural disasters or geopolitical crises can disrupt financial systems, making it essential to have a backup plan. Start by assembling an Emergency Financial Kit with key documents like insurance policies and bank records. This complements earlier advice about secure banking tools, reinforcing your overall preparedness.

Enroll in the Smart Traveler Enrollment Program (STEP) to receive security updates and ensure the U.S. embassy or consulate can contact you or your emergency contacts during a crisis. In many cases, text and data services remain operational even when voice calls fail.

Keep a small reserve of cash – around $100 in U.S. dollars and some local currency – in a secure but discreet location, like a hollowed-out book or a mislabeled container, to cover immediate needs during outages.

If traditional wiring services are unavailable, the OCS Trust program can facilitate money transfers through the State Department. For evacuation scenarios, the U.S. government may offer reimbursable loans to cover essential costs. However, unpaid evacuation debts over 90 days old can accrue penalties of 6% annually, along with a $50 administrative fee.

Finally, check if your bank has international branches or partnerships to minimize withdrawal fees during emergencies. Always maintain multiple payment methods – cash, debit cards with EMV chips, and credit cards from major networks like Visa and Mastercard – to ensure you have options no matter the situation.

Securing Your Funds: Best Practices

Having an emergency fund is essential, but keeping that money safe from theft, fraud, and cyber threats is just as important. A few smart precautions can help you protect your funds and ensure uninterrupted access to cash, no matter where you are.

Protecting Digital Wallets and Bank Accounts

Start by using strong passwords and enabling two-factor authentication (2FA) on all your financial accounts. Many banking apps let you lock your debit card when it’s not in use, adding an extra layer of security. You can unlock it only when you need to make a transaction, preventing unauthorized use if your card details are compromised.

Before you travel, notify your bank and credit card companies about your plans. Banks often flag international transactions as suspicious, which can lead to frozen accounts – something you definitely don’t want while abroad.

When withdrawing cash, choose ATMs located inside bank branches or in well-lit, busy areas. These are less likely to have card skimmers – devices that steal your card information – compared to standalone ATMs in convenience stores or on the street. Always inspect the ATM for anything unusual, like loose parts or suspicious attachments, before inserting your card.

Make sure your credit or debit cards have EMV chip technology, as these are more secure than magnetic stripe cards. Also, ensure your PIN works internationally – most foreign ATMs require a 4-digit PIN, and some won’t accept PINs starting with "0". Keep photocopies of your cards (front and back) in a secure place separate from the physical cards. This will help you quickly report and replace them if they’re lost or stolen. Save your bank’s international customer service number in your phone for immediate access during emergencies.

Finally, consider spreading your funds across multiple locations to reduce risk and improve your financial flexibility.

Diversifying Emergency Fund Storage

Securing your digital accounts is crucial, but organizing your physical assets is just as important. By spreading your funds across multiple accounts, currencies, and locations, you create a safety net. If one account freezes, a card is lost, or a currency devalues, you’ll still have access to money.

Carry at least two credit or debit cards from different issuers, such as one Visa and one Mastercard, since these networks are widely accepted globally. Store them in separate locations – for example, keep one in your wallet and another in a hotel safe. This way, losing one card doesn’t leave you stranded. A Harvard student shared this advice:

"Have at least two credit/debit cards abroad. One of my card accounts was frozen, and I would have been in trouble if I hadn’t had a backup".

Keep about $100 in U.S. dollars for emergencies, like paying for transportation or food when cards aren’t accepted.

Consider using multi-currency accounts to hold funds in different currencies. This can protect you from local currency fluctuations and reduce conversion fees during emergencies. Divide your emergency fund between highly liquid accounts (like savings or money market accounts) and slightly less liquid options (like short-term CDs or treasuries) to maintain your purchasing power.

Preventing Fraud and Cybersecurity Threats

Once your funds are secure, it’s essential to guard against fraud and cyber risks. Travelers are often targeted by scammers who exploit distractions or unfamiliarity with local conditions. For example, avoid Dynamic Currency Conversion (DCC) when using ATMs or paying at terminals. Always choose to be charged in the local currency, as DCC almost always comes with unfavorable fees and exchange rates.

Use contactless payment methods like Apple Pay or Google Pay when available. These digital wallets generate unique transaction codes, making them safer than physical cards. However, cash is still necessary in rural areas or for small purchases, so carry only what you need for the day and store backup cards and extra cash securely.

Be cautious of common scams, such as distraction techniques, fake "wallet drops", or inflated bills at bars and cafes. If someone claiming to be a U.S. citizen abroad asks for money, verify their story by contacting the Department of State’s Overseas Citizens Services at 888-407-4747. The Federal Trade Commission advises:

"The FTC will never threaten you, say you must transfer your money to ‘protect it,’ or tell you to withdraw cash or buy gold and give it to someone. That’s a scam".

For extended travel or relocation, consider setting up a notarized power of attorney. This allows a trusted family member to manage your accounts if you’re unable to do so yourself. It’s a legal safeguard that can be a lifesaver in emergencies.

Offshore Structures in Emergency Fund Planning

When looking for added security beyond domestic options, offshore structures can provide a reliable alternative. Offshore accounts and trusts offer key advantages such as privacy, asset protection, and multi-currency liquidity. These features become especially valuable during times of domestic instability or disruptions in financial systems.

Benefits of Offshore Accounts for Emergency Funds

Offshore accounts operate outside U.S. jurisdiction, making it harder for creditors or litigants to access your funds. They also allow you to hold money in over 40 currencies, offering immediate access to local markets without the burden of high conversion fees. This flexibility can be a lifesaver in situations like political unrest or sudden currency devaluation.

For instance, professional firms like Dominion Capital Strategies have managed over $500 million in trust assets across more than 20 countries, showcasing the scale and dependability of these structures. Additionally, many offshore jurisdictions enforce strict confidentiality rules, making it difficult for outsiders to identify account holders or beneficiaries. However, U.S. residents must comply with FBAR (Foreign Bank Account Report) filing requirements. As Ora Partners highlights:

"Offshore trusts provide a secure and legal way to diversify the jurisdictions where wealth is held and protect assets from lawsuits, creditors, and unstable geopolitical climate".

For those seeking even greater long-term protection, offshore trusts offer an additional layer of security.

Using Trusts for Long-Term Security

structuring offshore asset protection trusts (APTs) step up the level of security by transferring ownership of assets to an independent trustee. This means the funds are no longer considered part of your direct ownership, shielding them from domestic court orders. Dominion explains:

"The cornerstone of an offshore asset protection trust (APT) is that the trustee, not the grantor, holds legal title to the assets".

Trustees often have discretionary powers, enabling them to release funds during emergencies while keeping the assets protected from claims. Additional safeguards like anti-duress clauses (which prevent distributions under legal pressure) and flight clauses (allowing the trust to relocate to a different jurisdiction if conditions worsen) further enhance security.

Setting up an offshore trust is not an overnight process – it typically takes one to three months and requires expert guidance to ensure compliance with legal standards. Popular jurisdictions, such as the Cayman Islands, British Virgin Islands, and Nevis, are known for their strong legal frameworks and creditor protections. It’s essential to establish these structures well ahead of any potential legal or financial crisis, as courts may view trusts created during ongoing disputes as fraudulent transfers.

How to Build a Worldwide Emergency Fund

Creating a worldwide emergency fund takes careful planning and the right financial setup. Breaking it down into three key steps can help ensure your funds are accessible wherever you are.

Calculate Your Financial Needs

Start by setting an initial goal of $1,000 to cover smaller emergencies, then work toward building a full emergency fund. For individuals, aim for three months of essential expenses; for families or those with unpredictable income, six months or more is ideal.

When calculating your needs, focus on core expenses like housing, utilities, food, transportation, and insurance. If you plan to live abroad, research the cost of living in your destination, as places like Western Europe or Japan can be notably more expensive. Don’t forget to account for typical fees, such as a 3% transaction charge or $5 per international ATM withdrawal. Medical expenses are particularly important – many international hospitals require full payment upfront, even in countries with public healthcare systems that may not cover foreign nationals.

Select the Right Tools and Accounts

Once you know how much you need, choose financial tools that make your funds easily accessible. Multi-currency platforms like Wise and Revolut let you hold balances in over 40 currencies, helping you avoid losses from currency fluctuations. For example, as of December 17, 2025, Wise offers a 3.14% APY on USD balances, making it a strong option for storing emergency funds. Their Multi-Currency Card costs $9.00 for the first card and allows two fee-free withdrawals totaling up to $100.00 per month.

To ensure redundancy, carry at least two debit or credit cards from different providers – such as one Visa and one Mastercard – and keep photocopies in a secure place. While traditional bank accounts can serve as backups, be mindful of their higher fees.

Review and Optimize Your Strategy Regularly

Your emergency fund requires ongoing attention. As Synovus explains:

"Creating a target for your emergency fund is not a one-and-done event. You’ll need to periodically evaluate how much you need – and make changes accordingly".

Life events like buying a home, having a child, or changes in educational costs should prompt a reassessment. Even without major changes, inflation can reduce your fund’s value over time, making it necessary to adjust for rising costs in essentials like food, rent, and insurance.

Automate your savings by setting up direct transfers from your paycheck into a high-yield savings or money market account. This helps your fund grow and keeps pace with inflation. Aim to cover 3–12 months of essential expenses while balancing other financial goals. These practices will help you stay prepared for financial challenges on a global scale.

Conclusion

Creating a global emergency fund takes careful planning, smart diversification, and regular updates. The approaches outlined here – like using multi-currency wallets, international bank accounts, global ATM networks, and offshore options – help ensure you can access cash whenever and wherever you need it. Whether you’re dealing with a travel hiccup, moving abroad, or preparing for unforeseen events, having funds spread across multiple platforms and currencies ensures you’re never left stranded.

Diversifying access points is key. Keep accounts with different banks and payment networks, and always have around $100 in U.S. cash on hand for immediate needs. By spreading your funds across various providers, you’re better protected against issues like frozen accounts due to fraud alerts or network outages.

Planning ahead before traveling is equally important. Research the financial systems in your destination and confirm that your cards and accounts work with local networks. Opt to pay in the local currency rather than U.S. dollars to avoid Dynamic Currency Conversion fees, which can climb as high as 4.5%.

Your emergency fund isn’t a set-it-and-forget-it solution. It needs regular updates to reflect changes in your life, the economy, and evolving payment technologies. Use mobile banking apps to monitor transactions and make sure you know how to lock your card immediately if it’s lost or stolen.

FAQs

How much cash should I keep when traveling?

It’s a good idea to keep $100–$300 in local currency on hand when traveling. The exact amount depends on your destination and how comfortable you feel carrying cash. This can help you handle unexpected expenses, like transportation or basic necessities, without any hassle. Be sure to adjust based on factors like ATM availability, how often cards are accepted, and your personal spending habits.

What’s the safest way to get cash from an ATM abroad?

When withdrawing cash from an ATM abroad, the best option is to use machines within your bank’s partnership network. These ATMs usually provide clearer fees and more favorable exchange rates. Steer clear of ATMs located at airports or exchange bureaus, as they often come with higher fees and poor currency conversion rates. Before completing a transaction, always review the fee details displayed on the screen to avoid surprises.

How do I avoid getting my bank account frozen overseas?

To avoid the hassle of having your bank account frozen while overseas, make sure to notify your bank or credit card company about your travel plans. This helps prevent their security systems from flagging your transactions as suspicious. Stick to using well-established and trustworthy banks, steering clear of those flagged on financial watch lists, as they are more likely to face regulatory problems. Also, ensure your accounts meet local legal requirements and take the time to understand your bank’s rules regarding international transactions.