When international assets are involved in a divorce, the process becomes significantly more complex. U.S. courts can order transfers of foreign assets but lack the authority to directly enforce these rulings abroad. Privacy laws, currency fluctuations, and differing legal systems further complicate the division of property. Here’s what you need to know:

- Challenges: Locating assets, enforcing U.S. rulings overseas, and navigating tax and privacy laws.

- Key Strategies: Offshore trusts, holding companies, and jurisdiction selection (e.g., Anguilla) can protect assets.

- Legal Tools: Use Mareva injunctions, TROs, and local legal experts to secure and trace assets.

- Tax Compliance: Properly report foreign accounts (FBAR, FATCA) and plan for potential double taxation.

- Timing: Early planning, ideally years before divorce proceedings, ensures better outcomes.

With 21% of U.S. marriages involving a foreign-born spouse, understanding these strategies is crucial for protecting cross-border wealth.

Identifying and Protecting Cross-Border Assets

Finding and Valuing International Assets

To locate cross-border assets, start by reviewing existing documentation. U.S. tax returns – specifically Schedule B, Schedule D, and Form 8938 – can provide valuable clues. Loan applications are another useful resource since they often require a full disclosure of global wealth.

Certain red flags might indicate hidden international assets. Look out for unexplained wire transfers, ownership of offshore shell companies, or irregular payments to foreign professionals. Credit card statements revealing unexpected travel expenses or payments to foreign lawyers and accountants could suggest the setup of offshore structures. Forensic accountants play a key role here, as they can trace financial records, uncover discrepancies, and follow money trails.

Formal legal tools are also essential for uncovering assets. Attorneys may employ interrogatories, depositions, and subpoenas, including those directed at U.S.-based banks with international branches, to access records tied to foreign accounts. Additionally, international reporting frameworks like FATCA and the Common Reporting Standard (CRS) facilitate financial data sharing between governments. For countries that are part of the Hague Evidence Convention, the process of gathering evidence is streamlined through designated Central Authorities.

When it comes to valuing international assets, it’s important to differentiate between "official" valuations, often lower and used for tax purposes, and "commercial" real estate valuations, which reflect actual market value. Other factors such as foreign property transfer taxes, capital gains taxes, and restrictions on repatriating funds can significantly impact an asset’s net value. Currency fluctuations further complicate matters, so settlement agreements must clarify whether currency conversion is based on the judgment date or the distribution date. Engaging local legal experts in the relevant jurisdiction is often necessary to navigate privacy laws and property regulations effectively.

Once assets are valued, the focus shifts to protecting these resources through legal measures.

Legal Tools for Securing International Assets

After identifying and valuing international assets, the next step is to secure them using legal mechanisms. Acting quickly is critical, and tools like Mareva injunctions and Temporary Restraining Orders (TROs) can be highly effective. Mareva injunctions, common in jurisdictions like the UK, Canada, and Australia, freeze a defendant’s assets worldwide before a judgment is enforced. Similarly, TROs in the U.S. can prevent the transfer or encumbrance of assets, though enforcing these orders internationally may require their registration in the relevant foreign jurisdiction.

If there’s a suspicion that assets are being moved to more secretive jurisdictions, immediate action is crucial. A notable example is the 2016 case of UVW v. XYZ, where a British Virgin Islands court allowed a third party to assist a foreign judgment creditor in tracing assets. The debtor’s history of evasive behavior demonstrated that offshore courts are willing to cooperate in such cases when bad faith is evident.

Since international asset tracing can be expensive, it’s essential to weigh the cost of pursuing these efforts against the potential recovery. This ensures that extensive searches across multiple countries are only undertaken when financially justified.

sbb-itb-39d39a6

Using Jurisdiction Selection for Asset Protection

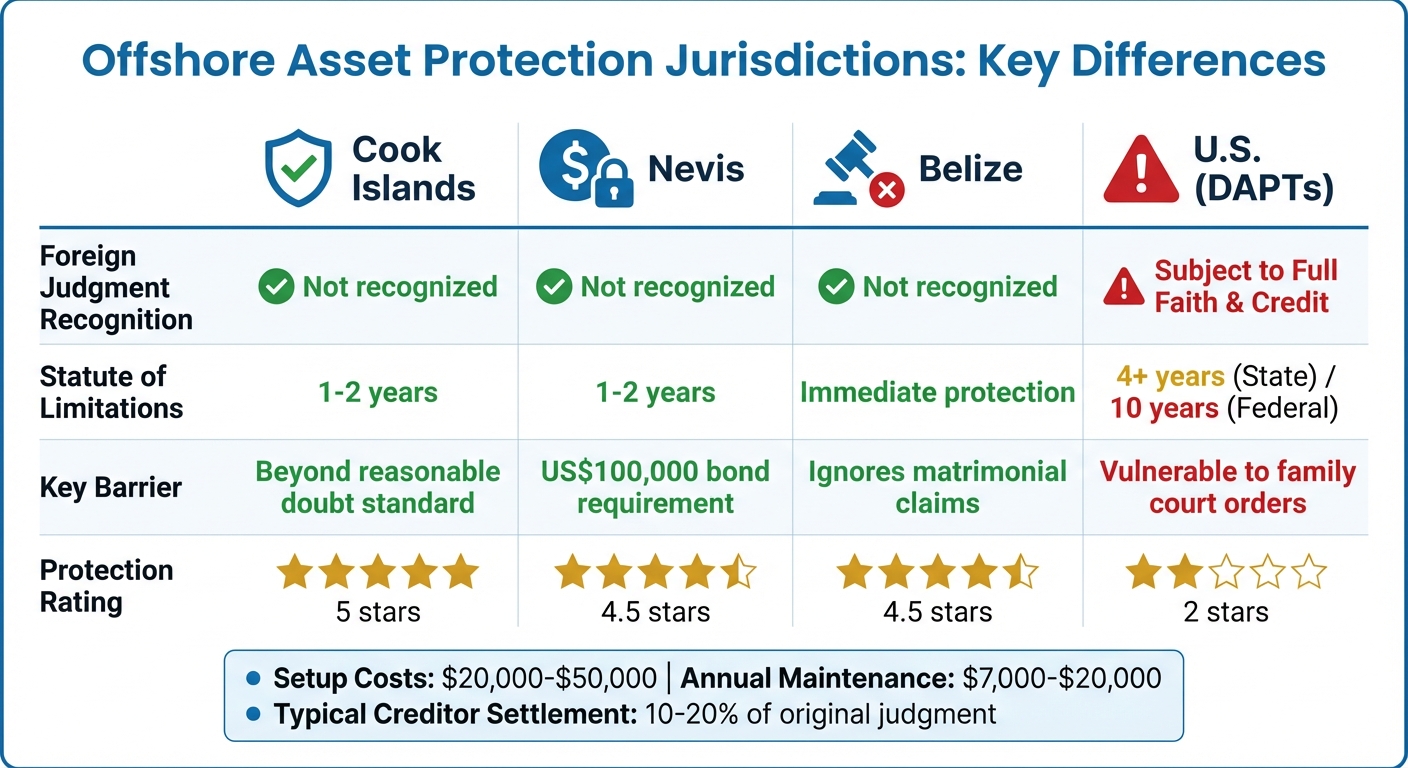

Offshore Asset Protection Jurisdictions Comparison for Divorce

Selecting the Right Jurisdiction

Picking the right jurisdiction is a critical step in creating a solid asset protection strategy during divorce. Building on cross-border asset protection strategies, choosing a jurisdiction with strong legal safeguards can help prevent asset loss.

The Cook Islands is often regarded as a top choice. It doesn’t recognize U.S. divorce decrees, requires proof of fraudulent intent beyond a reasonable doubt, and enforces a short statute of limitations – just 1–2 years.

Nevis stands out for its upfront US$100,000 bond requirement for filing claims. Like the Cook Islands, it disregards foreign judgments and has a similarly brief 1–2 year window for contesting asset transfers. Belize offers immediate asset protection upon lawful transfer, explicitly rejecting trust challenges tied to foreign divorce proceedings. This can be particularly advantageous when quick action is needed.

Other jurisdictions to consider include Saint Vincent and the Grenadines, which has enhanced trust laws, and Seychelles, known for its firewall provisions that protect trust assets from foreign matrimonial claims. For those prioritizing privacy, Hungary provides a unique asset management foundation tailored for high-net-worth individuals.

For U.S.-based options, Domestic Asset Protection Trusts (DAPTs) in states like Nevada or Alaska may seem appealing, but they come with risks. Courts often override these trusts using Full Faith and Credit arguments. For instance, in Dahl v. Dahl, a Utah court allowed access to assets in a Nevada DAPT. Similarly, in In re Huber, an Alaska DAPT was invalidated when Washington law was applied.

"DAPTs fail when tested outside their home state." – Brian T. Bradley, Esq.

Offshore structures come with significant costs. Setting up a foreign asset protection trust can range from US$20,000 to US$50,000, with annual maintenance fees between US$7,000 and US$20,000. Despite the expense, these trusts can often push creditors to settle for just 10–20% of the original judgment amount.

| Jurisdiction | Foreign Judgment Recognition | Statute of Limitations | Key Barrier |

|---|---|---|---|

| Cook Islands | Not recognized | 1–2 years | Beyond reasonable doubt standard |

| Nevis | Not recognized | 1–2 years | US$100,000 bond requirement |

| Belize | Not recognized | Immediate protection | Ignores matrimonial claims |

| U.S. (DAPTs) | Subject to Full Faith & Credit | 4+ years (State) / 10 years (Fed) | Vulnerable to family court orders |

Carefully choosing a jurisdiction lays the groundwork for using legal tools specifically designed to resist foreign matrimonial claims. After this step, selecting the right legal structure becomes the next priority.

Offshore Trusts and Foundations

Once a secure jurisdiction is selected, the next step is choosing the right legal structure to protect your assets. Offshore trusts and private interest foundations are two of the most effective tools for shielding assets from divorce claims.

Offshore trusts work by transferring legal ownership of assets to a trustee in a protective jurisdiction. Importantly, these trusts should include a duress clause, which prevents trustees from repatriating assets under foreign court orders. For example, in FTC v. Affordable Media (the "Anderson case"), assets in a Cook Islands trust remained secure despite a U.S. federal court’s repatriation order. The trust’s protective provisions ensured the assets were safeguarded.

"The Cook Islands International Trusts Act was built specifically to defend assets from foreign judgments." – Brian T. Bradley, Esq.

Another example is United States v. Grant (2008–2013), where the IRS failed to recover US$36 million from trusts in the Cook Islands and Jersey because the foreign trustees weren’t subject to U.S. jurisdiction.

For those who want more control, a trust-plus-LLC structure is a popular choice. Here, the offshore trust owns 100% of an offshore LLC. While the trustee holds legal title, you manage day-to-day investments as the LLC manager. This setup combines strong asset protection with operational flexibility.

Private interest foundations offer another layer of protection. These entities, particularly those in Anguilla, function like trusts but operate as separate legal entities, providing added privacy and control. Hungary’s asset management foundation is also an option for those seeking high levels of confidentiality.

Timing is everything. Asset protection works best when implemented three to five years before any legal claims or divorce filings. This reduces the likelihood of fraudulent transfer accusations. Some jurisdictions, like the Cayman Islands and Nevis, even allow for perpetual trusts with no mandatory distribution deadlines, ensuring long-term security. However, setting up these structures after divorce proceedings begin can lead to unfavorable legal outcomes.

International Legal and Tax Requirements

Enforcing U.S. Divorce Decrees Abroad

Trying to enforce a U.S. divorce decree in another country can be a daunting process. Unlike child custody cases, which are often covered by the Hague Convention, there’s no universal treaty that governs the division of marital property internationally. Each country has its own legal framework, and many won’t recognize U.S. court orders outright.

Here’s the challenge: while U.S. courts can demand compliance from individuals, they don’t have direct authority over assets located in foreign countries. For example, a judge might order your spouse to transfer funds from a Swiss bank account or sign over the deed to a villa in France, but the court itself can’t make those changes happen. The success of enforcement depends on the foreign jurisdiction’s willingness to cooperate and whether the spouse complies voluntarily.

"A Florida judge might order your spouse to sign over a deed, but enforcing that order relies on the spouse’s compliance and the foreign country’s willingness to recognize the Florida judgment." – C. Alvarez Law

Foreign banks and property registries aren’t obligated to follow U.S. court orders. To access or divide these assets, you’ll need to register your U.S. judgment with the local courts in that country, a process often referred to as obtaining a "mirrored order." This step involves hiring local legal experts and navigating unfamiliar legal systems, which can take months – or even years.

Real-world cases highlight these difficulties. For example, in Botwe v. Brifa, the U.K. Supreme Court refused to recognize a Ghanaian divorce due to procedural issues. Similarly, in Hussein v. Parveen, an English court rejected an Islamic "taleq" divorce from Pakistan, showing how religious-based decrees can run into roadblocks in secular legal systems. Even in countries with similar legal traditions, enforcement isn’t guaranteed. Civil law jurisdictions, for instance, may dismiss U.S. judgments if they believe proper notice wasn’t given or if the ruling conflicts with local property laws.

Obtaining financial records from countries with strict privacy laws – like Switzerland or the Cayman Islands – requires formal legal channels, such as those outlined in the Hague Evidence Convention. This process can be time-intensive and add another layer of complexity.

And if legal enforcement wasn’t enough of a challenge, tax issues can make dividing international assets even trickier.

Tax Consequences of Cross-Border Asset Division

Dividing international assets doesn’t just involve legal hurdles – it also comes with a host of tax complications. For instance, Internal Revenue Code (IRC) Section 1041, which allows for tax-free transfers between spouses, might not apply if one spouse is a nonresident alien.

One of the biggest concerns is double taxation. A transfer that’s tax-neutral in the U.S. could be treated as a taxable event in the country where the asset is located. This could result in immediate capital gains taxes, even if no cash changes hands. Imagine transferring a property overseas – without proper planning, you could end up paying taxes in both countries. Using foreign tax credits can help, but failing to plan for this situation could leave you facing significant financial losses.

"Ignoring the tax consequences of transferring international assets is a financial error you cannot afford." – C. Alvarez Law

U.S. reporting requirements add another layer of complexity. If the total value of your foreign accounts exceeds $10,000 at any point during the year, you’re required to file a Foreign Bank Account Report (FBAR). Additionally, Form 8938 must be submitted for certain foreign financial assets. Missing these filings could lead to steep civil and even criminal penalties.

Currency fluctuations can also complicate settlements. To avoid disputes down the line, settlement agreements should clearly outline how and when currency conversions will be calculated.

To navigate these challenges, it’s crucial to have a team of experts. This might include U.S. family lawyers, local attorneys in the relevant countries, forensic accountants, and international tax specialists. Together, they can help structure asset transfers in a way that minimizes tax exposure, secures foreign tax credits, and ensures judgments are properly recognized overseas. With roughly 21% of U.S. married couples including at least one foreign-born spouse, these issues are far from uncommon.

Implementing Asset Protection Strategies

Using Offshore Companies and Trusts

When it comes to offshore asset protection, combining an offshore trust with an offshore LLC is one of the most effective strategies. Here’s why: the trust owns 100% of the LLC, creating a separation of control and ownership. This setup allows you to manage daily investments as the LLC manager, while an independent foreign trustee retains ultimate ownership. This separation is key because assets governed by foreign laws are typically out of reach for U.S. courts.

Here’s how the system works: you handle routine financial decisions and investments as the LLC manager. Meanwhile, the trustee holds the membership interests and has the final say. To add another layer of security, the trust deed usually includes anti-duress clauses, which protect your assets if you’re under legal pressure.

Jurisdictions like the Cook Islands and Nevis are especially attractive for such structures. They impose steep requirements on creditors, such as bonds of $25,000 to $50,000 just to file a claim. Even then, creditors must prove fraudulent intent beyond a reasonable doubt – a much tougher standard than in the U.S..

"Offshore asset protection is not a tax strategy. It requires full compliance with all U.S. tax and reporting obligations." – Jon Alper, Asset Protection Attorney

Timing is crucial. These structures are most effective when established 3 to 5+ years before any legal claims or divorce proceedings arise. Setting them up too late – such as when a divorce is already on the horizon – can lead to fraudulent transfer challenges, jeopardizing the entire structure. Additionally, compliance with U.S. tax laws is non-negotiable. You’ll need to file Forms 3520, 3520-A, and FBAR annually to stay on the right side of the IRS.

Costs for setting up these structures range from $20,000 to $50,000, with annual maintenance fees between $7,000 and $20,000.

How Global Wealth Protection Can Help

Global Wealth Protection (GWP) offers comprehensive services to streamline the formation and maintenance of offshore asset protection structures. Specializing in jurisdictions like Anguilla, the firm ensures that your setup is both compliant and secure.

Their services include offshore company formation, covering everything from filing paperwork to connecting you with offshore banking partners. For high-net-worth individuals, GWP provides offshore trusts and private interest foundations, complete with ongoing trust administration and asset management.

Through their GWP Insiders membership program, clients gain access to personalized internationalization strategies. This includes guidance on tax minimization, jurisdiction selection, and actionable advice tailored to individual circumstances. Whether you’re safeguarding current assets or planning for future risks, this program provides the tools you need.

For those requiring tailored solutions, GWP also offers private consultations. These sessions focus on your unique financial profile, risk exposure, and timeline. They help you determine which structures are appropriate and how to implement them without triggering fraudulent transfer laws. With expert guidance, you can move forward with confidence.

Steps to Start Protecting Your Assets

Begin with a risk assessment. Evaluate your net worth and the likelihood of facing legal claims. Offshore protection generally makes sense for individuals with at least $1 million in liquid assets, given the associated costs.

Next, choose the right jurisdiction. The Cook Islands offers the highest level of protection for those in high-risk scenarios, while Nevis provides a more cost-effective option. Both jurisdictions have short statutes of limitations for fraudulent transfer claims – usually just 1 to 2 years.

Once you’ve selected a jurisdiction, work with professionals to draft a trust deed that includes spendthrift and anti-duress clauses. Establish an LLC in the chosen jurisdiction and transfer 100% of its membership interests to the trust. Open offshore accounts in the LLC’s name and transfer your liquid assets. Throughout this process, keep detailed records to demonstrate legitimate business purposes.

Finally, set up compliance systems for annual IRS reporting. Obtain an Employer Identification Number (EIN) for your offshore entities and ensure all required forms are filed correctly.

The best time to act is before legal proceedings begin. Once a divorce or lawsuit is underway, your options become limited, and every transfer is closely scrutinized by the courts. Planning ahead is key.

Conclusion

Key Points to Remember

Protecting assets during an international divorce goes far beyond basic legal preparation. Understanding why offshore asset protection is necessary can help you navigate these complexities. Full disclosure is non-negotiable – attempting to hide offshore assets can lead to criminal charges, steep penalties, and unfavorable asset division outcomes. This issue impacts countless families navigating cross-border divorces.

Choosing the right jurisdiction is a critical step. Filing first in a favorable jurisdiction can prevent your spouse from securing an advantage in a less favorable forum. While U.S. courts can order property transfers, enforcing those orders internationally depends on cooperation from local authorities. Without careful planning and coordination with local counsel in each country where assets are held, enforcement can become a major obstacle.

Tax compliance is another essential factor. Filing FBAR and Form 8938 when required is not optional. Non-compliance can result in IRS penalties that exist separately from divorce settlements. Additionally, currency fluctuations can impact the value of international assets during settlement negotiations.

Early and thorough planning is your best defense. Ideally, this should start years before any legal claims arise. Prenuptial and postnuptial agreements remain the most effective tools for clearly defining how international assets will be divided. However, once divorce proceedings are underway, every asset transfer comes under intense scrutiny, leaving little room for flexibility.

Next Steps for Protecting Your Wealth

With these insights in mind, it’s time to take actionable steps. Start by assembling a team of experts to safeguard your international assets. This team should include specialized divorce attorneys, forensic accountants to trace assets, and tax professionals well-versed in FATCA and FBAR regulations. Proactively gather documentation – such as deeds, titles, bank statements, and tax records for all foreign holdings – long before any disputes arise.

For tailored strategies, Global Wealth Protection offers expert consultations. Their team evaluates your financial situation, risk factors, and timeline to recommend the best asset protection measures for your needs. Through their GWP Insiders membership program, you can access personalized support for jurisdiction selection, tax planning, and other internationalization strategies.

"Identifying and locating marital assets is one of the biggest challenges practitioners will face." – Joan K. Crain, Global Family Wealth Strategist at BNY Mellon Wealth Management

The key takeaway? Act early – before legal proceedings begin – to protect your wealth and secure your financial future.

FAQs

How can I tell if my spouse is hiding offshore assets?

If you suspect your spouse might be hiding offshore assets, there are a few key signs to watch for. These can include unusual secrecy around finances, significant transfers to foreign accounts or entities, ownership of international businesses or trusts, or unexplained foreign tax filings.

To dig deeper, start by reviewing financial records like tax returns and bank statements for any irregularities or suspicious activity. Spotting something unusual can be a critical first step.

When things get complex, forensic accountants and legal tools, such as financial disclosures, can play a vital role in uncovering hidden assets. Enlisting professional help can significantly improve your chances of identifying concealed offshore holdings, especially during divorce proceedings.

Can a U.S. divorce order force a foreign bank or property registry to act?

In the U.S., a divorce order usually doesn’t have the power to directly force a foreign bank or property registry to comply. However, it can sometimes be enforced internationally through legal avenues such as mutual recognition and enforcement of foreign judgments. The success of this process depends on the specific jurisdiction and the degree of cooperation between the countries involved.

When is it too late to set up an offshore trust for divorce protection?

When divorce proceedings are already underway, setting up an offshore trust for asset protection is often too late. Courts tend to scrutinize these trusts and may treat their assets as part of the marital estate, particularly if the trust appears to be a tactic to conceal wealth. The timing matters immensely – planning ahead is essential to safeguard assets effectively.