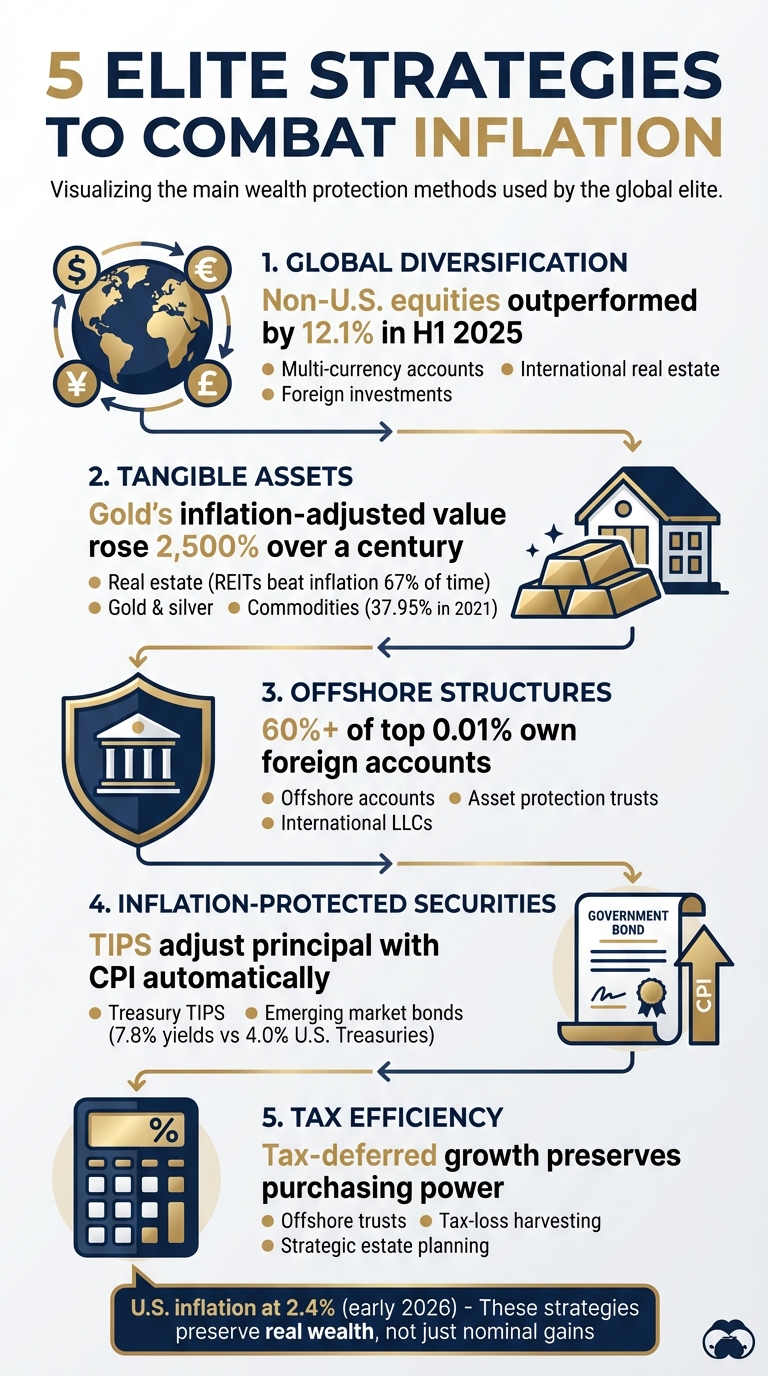

Inflation can quietly erode your wealth, but the world’s wealthiest individuals use specific strategies to protect and grow their purchasing power. Here’s what they do:

- Diversify Globally: Spread investments across countries to reduce risks tied to one economy. This includes holding foreign currencies, investing in international real estate, and using multi-currency accounts.

- Invest in Tangible Assets: Real estate, gold, silver, and commodities often perform well during inflation. These assets retain value over time and hedge against rising costs.

- Leverage Offshore Accounts and Trusts: Offshore asset protection and trusts provide legal tools to protect wealth, minimize taxes, and shield assets from lawsuits.

- Use Inflation-Protected Securities: Treasury Inflation-Protected Securities (TIPS) and emerging market bonds offer returns that account for inflation while diversifying portfolios.

- Focus on Tax Efficiency: Wealthy individuals reduce tax burdens by using tax-deferred accounts, tax-loss harvesting, and offshore structures.

These strategies aim to preserve wealth in real terms, not just nominal gains. With inflation at 2.4% in the U.S. as of early 2026, these tools are vital for maintaining financial stability. Let’s explore these approaches in detail.

Spreading Assets Across Multiple Countries

Wealthy investors rarely keep all their assets in one country. This strategy, called geographic diversification, helps protect purchasing power and reduce risks tied to inflation. By spreading investments across borders, they can avoid overexposure to a single country’s economic troubles, policy changes, or currency fluctuations. This approach often includes holding foreign currencies and investing in international real estate.

The importance of this strategy became evident in 2025 when the U.S. dollar dropped over 10% against a group of major foreign currencies. At the same time, non-U.S. equities outperformed U.S. equities by 12.1% during the first half of the year. These figures highlight how international investments can safeguard wealth when domestic markets face challenges.

Holding Multiple Currencies

Diversifying currency holdings is another way to manage the risks of inflation and currency devaluation. When your home currency loses value, assets held in foreign currencies may retain or even grow in worth. This effect, known as the currency translation effect, can amplify returns when converting foreign earnings back into U.S. dollars during periods of dollar weakness.

"A weakening dollar would be a tailwind for investors in non-US stocks who may benefit from the currency translation effect of converting non-US portfolio returns into the US dollar."

- Anu Gaggar, Vice President of Capital Markets Strategy, Fidelity

One practical tip is to align your currency exposure with your spending patterns. For instance, if you spend 40% of your time in Europe, consider allocating 40% of your assets in Euros. Multi-currency bank accounts are increasingly popular for this purpose, allowing investors to hold funds in various currencies and convert them at favorable rates.

When it comes to fixed-income investments like bonds, experts usually recommend fully hedging foreign currency exposure. Over the past 20 years, exchange rate volatility has consistently been higher than bond return volatility. However, for international equities, leaving positions unhedged can often be more beneficial, as the cost of hedging may outweigh its advantages.

International real estate is another effective way to diversify and protect against inflation.

Buying Real Estate in Different Countries

Owning property abroad provides a tangible asset that often increases in value during inflationary periods. Rising prices typically boost both property values and rental incomes, while mortgage debt becomes less burdensome in real terms.

Beyond serving as an inflation hedge, foreign real estate offers protection against domestic economic and regulatory changes. Holding property in multiple jurisdictions can shield investors from local tax hikes, regulatory shifts, or economic downturns. The U.S. banking failures in 2023 underscored the importance of spreading assets across different regions.

To manage currency risks when purchasing international property, many investors use forward contracts to lock in favorable exchange rates. Properties are often held through offshore structures to enhance privacy and safeguard assets.

Country selection plays a crucial role in this strategy. Wealthy investors tend to favor locations with stable economies, strong legal systems, and attractive tax policies. For example, Switzerland is a top choice for its banking stability, typically requiring a minimum deposit of $1 million. Meanwhile, Austria offers private banking options with lower minimum deposits, ranging from $250,000 to $300,000.

sbb-itb-39d39a6

Offshore Accounts and Company Formation

Modern offshore strategies focus on creditor resistance and leveraging jurisdictional differences, especially under global transparency rules like FATCA and the Common Reporting Standard (CRS). By 2023, 108 countries had automatically exchanged data on 123 million offshore accounts, collectively valued at over €12 trillion.

"Modern offshore asset protection is about jurisdictional arbitrage: strategically placing assets in legal environments that offer superior protection compared to your home country."

A striking statistic shows that over 60% of individuals in the top 0.01% of wealth own foreign accounts. With around 5 million lawsuits filed annually in the United States as of 2023, the wealthy face mounting litigation risks. Offshore accounts not only act as a hedge against currency fluctuations but also, when combined with structured offshore companies, create robust legal barriers to protect broader asset portfolios. Offshore bank accounts, which we’ll explore next, are an essential part of this framework.

Using Offshore Bank Accounts for Inflation Protection

Offshore bank accounts are more than just a tool for currency diversification – they open doors to international investments like foreign real estate, commodities, and hedge funds. These accounts serve as a shield against domestic currency devaluation. For instance, when the U.S. dollar lost over 10% of its value against major currencies in 2025, investors with diversified currency holdings managed to preserve their purchasing power.

Some of the top jurisdictions for offshore banking include:

- Switzerland: Known for its stability, but accounts typically require $1 million minimum deposits.

- Austria: Offers entry points with deposits ranging from $250,000 to $300,000.

- Singapore: Combines strict regulatory oversight with policies favorable to investors.

For those who frequently travel or own property abroad, holding funds in local currencies can mitigate exchange rate risks. Multi-currency accounts add flexibility, allowing you to convert funds at competitive rates while protecting against inflation at home.

It’s crucial to comply with U.S. regulations by reporting offshore accounts to the IRS using FBAR (FinCEN Form 114) and Form 8938. While the days of secret accounts are over, properly structured legal protections remain highly effective.

Benefits of Forming Offshore Companies

Offshore companies take asset protection a step further by adding a layer of legal defense. Jurisdictions like the Cook Islands, Nevis, and the Cayman Islands are popular choices for forming LLCs or corporations. These entities create a legal firewall, requiring creditors to re-litigate claims in foreign courts and limiting recoveries to income flows through charging order protection.

The Cook Islands, for example, are renowned for their asset protection trusts, offering features like courts that don’t recognize foreign judgments and statutes of limitations as short as 1-2 years. Additionally, these jurisdictions require creditors to meet a high standard of proof, such as demonstrating "fraudulent transfer" beyond a reasonable doubt – a hurdle significantly harder to clear than in typical civil cases.

| Jurisdiction | Primary Strength | Key Feature |

|---|---|---|

| Cook Islands | Asset Protection Trusts | U.S. judgments not recognized; 1-2 year statute of limitations |

| Nevis | LLC Protection | Strong creditor barriers; lower fees compared to Cook Islands |

| Cayman Islands | Tax Neutrality | No income or capital gains taxes; favored by investment firms |

A common strategy involves layering entities, such as establishing a Nevis LLC owned by a Cook Islands trust. This complexity discourages legal challenges and, when paired with flight clauses, allows protections to shift jurisdictions if necessary.

Timing is everything. These structures need to be in place well before legal troubles arise. Transferring assets after a lawsuit has begun can be classified as "fraudulent conveyance", which courts can reverse. The smartest approach is to set up these protections during periods of stability, ideally years in advance.

"It’s not about hiding money; it’s about using internationally recognized legal and financial tools to build stronger, more resilient barriers around what you’ve worked hard to earn."

- The Nestmann Group

Work with international tax experts and asset protection attorneys to ensure compliance and maintain these structures through regular filings and legal reviews.

Assets That Hold Value During Inflation

When inflation chips away at the buying power of cash, wealthy individuals often turn to tangible assets – things like real estate, precious metals, and commodities. These physical assets tend to hold their worth because they’re both useful and scarce.

The numbers back this up. In 2021, with inflation at 7%, art delivered returns of 58.81%, and commodities saw gains of 37.95%. Over the last century, the U.S. dollar lost 95% of its purchasing power, while gold’s inflation-adjusted value climbed by over 2,500%. This stark contrast explains why savvy investors focus on assets that resist the effects of inflation.

It’s not just about growing your portfolio in dollar terms – it’s about preserving what your money can actually buy. For example, a $1 million portfolio earning 5% in a year with 7% inflation results in a 2% loss in real terms. Hard assets can help safeguard, and even grow, wealth during inflationary times. Let’s dive into how real estate, precious metals, and alternative assets perform under these conditions.

Real Estate as Protection Against Inflation

Real estate is a go-to inflation hedge because property values and rental income often rise alongside the Consumer Price Index (CPI). Historically, Real Estate Investment Trusts (REITs) have outpaced inflation about 67% of the time, delivering nearly 5% in annual real returns. Rising construction costs tend to push up the value of existing properties, and rental agreements often include clauses that adjust for inflation. Plus, if you finance property with a fixed-rate mortgage, your debt payments stay the same while inflation makes them cheaper in real terms.

For those who find direct property ownership too demanding or expensive, REITs offer a more accessible option. These investments provide exposure to a wide range of real estate portfolios without the hassle of property management. With U.S. inflation expectations hitting 4.8% by late 2025, assets like real estate that adapt to price increases become especially appealing.

Gold and Silver for Long-Term Value

Gold and silver are often seen as “alternative currencies” because they can’t be printed or devalued like paper money. Gold, for instance, has delivered an annualized real return of about 2.3% over long periods. Its inflation-adjusted value has risen more than 2,500%. This makes it a reliable choice during times of economic uncertainty or rising inflation. Silver offers similar benefits, with its industrial applications adding another layer of demand. However, during periods of sharply rising interest rates, gold can underperform since it doesn’t generate income.

Beyond these traditional hedges, alternative assets provide additional ways to protect against inflation.

Other Options: Art, Collectibles, and Commodities

Alternative investments like fine art, collectibles, and commodities can add diversity to a portfolio and reduce risk, thanks to their low correlation with traditional markets. In 2021, art delivered a 58.81% return, rare whiskey gained 20.62%, and fine wine appreciated by 19.10%. Scarcity is often the driving factor behind these impressive returns.

Commodities, in particular, stand out. These are the raw materials behind countless products, and their value often rises with inflation. Historically, a 1% unexpected increase in U.S. inflation has resulted in a 7% real return on commodities. During high-inflation periods, commodities have outperformed stocks and bonds about 74% of the time, while energy stocks have beaten inflation nearly 75% of the time with annual real returns close to 13%.

| Asset Class | 2021 Return (7% Inflation) | 5-Year Avg Annual Return (2017-2021) | Key Consideration |

|---|---|---|---|

| Art | 58.81% | 12.08% | High transaction and storage fees |

| Commodities | 37.95% | 9.03% | Geopolitical volatility |

| Rare Whiskey | 20.62% | 22.39% | Less regulatory oversight |

| Fine Wine | 19.10% | 7.45% | Illiquidity challenges |

Of course, these investments come with challenges. Physical assets often require specialized storage, insurance, and security, which can eat into returns. Markets for collectibles are less transparent than traditional exchanges, making it harder to sell quickly. Ultra-high-net-worth individuals (with $30 million or more) often hold about half their assets in alternatives, as they’re better equipped to manage these complexities.

For those who want exposure to commodities without dealing with physical storage, commodity-indexed ETFs are an option. These funds generally come with expense ratios between 0.40% and 0.75%. Some platforms even offer fractional ownership, with entry points as low as $1,000, making these strategies more accessible. Just be sure to account for all fees – like auction charges, brokerage costs, and management expenses – before jumping in. Together, these diverse assets can help build a strong defense against inflation, complementing traditional strategies and bolstering wealth protection.

Reducing Taxes with Offshore Trusts

Offshore trusts build upon earlier strategies like offshore accounts and corporate structures, offering another way to reduce tax burdens while protecting wealth. These trusts are particularly effective in managing tax liabilities during inflationary periods, where the nominal value of assets can rise, pushing individuals into higher tax brackets without any real increase in wealth. By placing assets under the control of a foreign trustee in jurisdictions with favorable tax laws, offshore trusts provide a legal method to separate asset ownership from domestic claims and tax obligations.

Here’s how it works: assets transferred to offshore trusts in tax-exempt jurisdictions often avoid taxation during the transfer and when distributed to beneficiaries. Trusts can also own businesses or investments in tax-free zones, allowing revenue to grow without local tax deductions. For Americans, incorporating Private Placement Life Insurance (PPLI) into a trust allows for tax-deferred or even tax-free growth, though this typically requires a minimum investment of $2,000,000.

How Offshore Trusts Protect Your Assets

Offshore trusts act as a legal shield for your wealth. By transferring asset ownership to a foreign trustee in jurisdictions like the Cook Islands or Nevis, you create a significant barrier against U.S. court actions. For instance, the Cook Islands boasts a 96% success rate in protecting trusts from legal challenges over the past 30 years. Nevis, on the other hand, requires creditors to post a $100,000 cash bond before filing claims against a trust.

"Think of an offshore asset protection trust as a legal fortress for your assets – like the moat around a castle." – The Nestmann Group

These jurisdictions also refuse to recognize U.S. court judgments, meaning domestic judges cannot force foreign trustees to relinquish assets. With around 5 million new court cases filed in the U.S. in 2023 alone, this separation has become increasingly valuable. Offshore trusts combine legal protections with strategic tax planning, helping preserve purchasing power even during inflationary cycles.

Tax Reduction Methods During Inflation

Offshore trusts minimize taxes by housing income-generating assets in tax-exempt zones. Whether it’s properties, commodities, or other inflation-resistant investments, trust-owned assets remain shielded from domestic taxes. Additionally, many offshore jurisdictions have abolished or extended the rule against perpetuities, allowing trusts to remain active indefinitely – an advantage for preserving wealth across generations during extended periods of inflation.

A growing strategy involves hybrid setups, where domestic entities (like a Nevada LLC) are paired with an offshore trust (such as one in the Cook Islands). This structure maintains compliance with U.S. regulations while optimizing tax efficiency. Transparency is key – filing FinCEN Form 114 (FBAR) and Form 8938 is crucial to avoid legal issues tied to tax evasion. Attorney James G. Bohm explains:

"Offshore asset protection is still viable, but it’s no longer a ‘hidden vault.’ Today, it’s most effective as part of a transparent, legally compliant, and professionally structured estate and asset plan."

Timing matters. These structures should be established well before any financial or legal troubles arise, as transfers made after claims emerge could be reversed as "fraudulent conveyance". With the U.S. national debt projected to exceed $31 trillion by late 2025 and ongoing inflationary concerns, offshore trusts have transitioned from being secretive tools to legitimate solutions for tax management and wealth preservation. They are now integral to broader international asset protection strategies, ensuring tax efficiency aligns with legal safeguards.

Treasury Inflation-Protected Securities (TIPS)

TIPS are a straightforward option for guarding your investments against inflation. Backed by the U.S. government, these bonds automatically adjust with inflation, making them a low-risk way to preserve purchasing power. You can buy TIPS through TreasuryDirect for as little as $100, with terms of 5, 10, or 30 years available.

How TIPS Work

TIPS operate differently than traditional bonds. Their principal value rises with inflation and falls with deflation, based on changes in the Consumer Price Index (CPI). While the interest rate is fixed, the actual dollar amount of interest payments fluctuates as it’s calculated on the inflation-adjusted principal. When inflation increases, both the principal and interest payments grow.

When the bond matures, you’re guaranteed to receive either the inflation-adjusted principal or your original investment – whichever is higher. This built-in protection ensures you won’t lose your initial capital even if deflation occurs. As TreasuryDirect puts it:

"When the TIPS matures, if the principal is higher than the original amount, you get the increased amount. If the principal is equal to or lower than the original amount, you get the original amount".

One of the standout features of TIPS is their ability to provide a real rate of return, meaning the return after accounting for inflation, unlike the nominal return offered by traditional bonds. However, there’s a catch: the IRS taxes the annual increase in principal as income in the year it occurs, even though you won’t receive that cash until the bond matures. This "phantom income" makes TIPS more suitable for tax-deferred accounts like IRAs or 401(k)s.

Advantages and Disadvantages of TIPS

TIPS come with clear benefits but also some trade-offs that investors should weigh carefully.

| Advantages | Disadvantages |

|---|---|

| Inflation Protection: Principal and interest adjust with the CPI. | Lower Yields: TIPS generally offer lower interest rates compared to traditional bonds. |

| Safety: Backed by the U.S. government’s "full faith and credit". | Phantom Income Tax: Annual principal increases are taxable, even if unpaid until maturity. |

| Maturity Floor: You’re guaranteed to receive at least the original principal at maturity. | Interest Rate Risk: Rising interest rates can lower the market value of TIPS significantly. |

| Tax Benefits: Exempt from state and local income taxes. | Deflation Impact: Principal and interest payments shrink during deflation. |

The events of 2022 highlighted a key limitation of TIPS. Despite high inflation, TIPS fell by an average of 14.2% because the Federal Reserve’s aggressive interest rate hikes reduced their market value. Eric Jacobson, a Senior Analyst at Morningstar, explains:

"The inflation protection is really a long‑term feature that works properly if you hold a TIPS until maturity. You should pretty much expect that changing market yields will drive TIPS market prices all over the map in the meantime, though".

For this reason, holding TIPS until maturity is the best way to avoid market volatility and lock in your inflation-adjusted returns. By offering real returns that account for inflation, TIPS play a valuable role in a well-rounded strategy to counteract inflation’s impact on your portfolio.

Emerging Market Bonds for Higher Returns

Emerging market bonds offer an opportunity to earn higher yields, helping to counter the effects of inflation. These bonds generally pay more interest than U.S. Treasuries or bonds from developed nations, providing a yield advantage that can help maintain purchasing power. However, they come with greater risks, making diversification essential. This approach can complement other strategies aimed at protecting against inflation by leveraging the potential for higher returns while managing added uncertainties.

Why Emerging Market Bonds Pay More

The higher yields of emerging market bonds reflect the additional risks investors take on due to political and economic uncertainties in developing countries. For example, as of March 2025, hard-currency emerging market sovereign bonds offered yields of about 7.8%, compared to approximately 4.0% for 10-year U.S. Treasuries – a spread of 3.8% that can help offset inflation.

In 2023, investment-grade government bonds from emerging markets delivered returns of 7.1%, outperforming similar bonds from advanced economies by nearly 2%. By 2025, local-currency emerging market government bonds surged by roughly 16%, while global fixed income as a whole only gained 3%. Over the long term, from 2003 to 2024, emerging market corporate bonds achieved a Sharpe ratio of 1.13, outpacing both U.S. Treasuries (0.60) and the S&P 500 (0.70) on a risk-adjusted basis.

Several factors contribute to the ability of these bonds to combat inflation:

- Commodity Exports: Many emerging economies rely on exporting commodities such as oil, metals, and agricultural goods. When inflation drives up commodity prices, these countries see increased revenues, enhancing their capacity to repay debt.

- Aggressive Central Banks: Central banks in emerging markets often respond more forcefully to inflation. As of late 2025, the weighted-average policy rate in these markets was 6.3%, with real interest rates exceeding 3% in many cases.

- Currency Positioning: Emerging market currencies were undervalued by an estimated 8% to 11% against the U.S. dollar as of October 2025. Local-currency bonds not only offer higher interest rates but also the potential for gains if these currencies appreciate.

Kenneth Orchard, Portfolio Manager at T. Rowe Price, highlights another advantage, noting:

"Struggling growth coupled with persistent inflation demands a creative approach to bond portfolio management… resource-exporting EM currencies can improve bond portfolio returns during inflationary periods".

Understanding the Risks of Emerging Market Bonds

While the yields are appealing, the risks tied to emerging market bonds cannot be ignored. These risks can erode returns if not carefully managed. Key concerns include:

- Political Instability: Developing nations are often vulnerable to governance issues, sudden policy changes, and civil unrest, all of which can impact bond values.

- Currency Risk: Local-currency bonds are especially susceptible to currency fluctuations. While appreciation can enhance returns, devaluation can sharply reduce them.

- Liquidity Risk: Selling these bonds quickly during times of market stress can be challenging and may require accepting a lower price.

- Credit and Default Risk: The likelihood of default is higher compared to U.S. government debt. Although the recovery rate for emerging market sovereign defaults since 2008 has been 56%, better than the 34% for corporate defaults, it still represents a potential loss of nearly half your investment.

Despite these challenges, there are ways to mitigate risks:

- Opt for Hard-Currency Bonds: Bonds denominated in U.S. dollars eliminate exchange rate volatility, though they typically offer lower yields.

- Invest Through Funds: Mutual funds or ETFs provide professional management and diversification across regions and issuers.

- Focus on Investment-Grade Ratings: Bonds rated ‘BBB’ (Standard & Poor’s) or ‘Baa3’ (Moody’s) or higher tend to be more stable.

- Consider Credit Default Swaps (CDS): While more complex and costly, CDS can offer protection against default risk.

Emerging market bonds can play an important role in a diversified portfolio, complementing other inflation-resistant investments like TIPS or physical assets. Their higher yields can balance the additional risks, making them a valuable tool for investors seeking to protect and grow their wealth in inflationary environments.

Conclusion: Your Action Plan for Fighting Inflation

Building Your Wealth Protection Plan

Guarding your wealth against inflation requires more than just a savings account – it calls for a well-rounded approach. Combining international diversification, inflation-resistant investments, and tax-efficient strategies can help you stay ahead of rising costs.

Start by limiting your cash reserves to cover 3–6 months of essential expenses. Beyond that, direct your surplus funds into growth-focused assets. Historically, equities have delivered an average annual return of 11.7% since 1980 – well above inflation rates. Other options, like commodities and REITs, also offer strong inflation protection, with REITs outperforming inflation about 66% of the time.

Taxes can quietly erode your returns, especially during inflationary periods. This happens because taxes are often calculated on nominal gains, not inflation-adjusted ones. To counteract this, use strategies like tax-loss harvesting and consider placing tax-inefficient investments in tax-deferred accounts. For those with significant wealth, tools like offshore trusts and strategic estate planning can provide additional layers of protection while reducing tax burdens.

The key focus here isn’t just growing your account balances – it’s safeguarding your purchasing power. Since every financial situation is unique, working with an expert can help you fine-tune these strategies to fit your needs.

Getting Expert Help

Even with a solid wealth protection plan, expert guidance ensures everything runs smoothly. Complex areas like offshore company formation, international tax planning, and advanced financial tools such as private equity or floating-rate loans often require specialized expertise.

That’s where professional advice comes into play. For example, Global Wealth Protection offers tailored strategies to align with your risk tolerance, financial goals, and liquidity needs. Whether you’re considering a private US LLC for asset protection or exploring offshore trust structures, consulting with a professional can save you from costly errors. As David Peterson, Head of Wealth Planning at Fidelity Investments, puts it:

"The best course of action is going to depend on your level of wealth and your stage of life. But having a good, robust financial plan can provide some comfort when the markets seem uncertain".

FAQs

How much should I keep in cash during inflation?

During times of inflation, it’s smart to keep enough cash on hand to cover immediate needs and emergencies. A good rule of thumb is to allocate around 10–30% of your portfolio to cash, though the exact amount will depend on your personal risk tolerance and financial objectives. However, holding too much cash can work against you, as it might hinder your ability to achieve long-term growth.

Are offshore accounts legal for U.S. citizens?

Yes, U.S. citizens can legally hold offshore accounts, provided they follow all applicable tax laws and reporting requirements. This means filing essential forms, like the FBAR (Report of Foreign Bank and Financial Accounts), and complying with FATCA (Foreign Account Tax Compliance Act) regulations. By accurately reporting these accounts and adhering to the rules, they remain both lawful and transparent.

Should I buy TIPS in a taxable account or an IRA?

It’s usually a smart move to keep TIPS (Treasury Inflation-Protected Securities) in a tax-advantaged account like an IRA. Why? It shields you from having to pay taxes each year on the inflation-adjusted interest and any principal gains. In a taxable account, these gains are treated as ordinary income, which can increase your tax burden.