Offshore investing is often misunderstood, thanks to media portrayals and high-profile scandals like the Panama Papers. However, the truth is far less dramatic. Offshore investing is legal and widely used for asset protection, portfolio diversification, and accessing global markets. Misconceptions persist, but with proper compliance, offshore strategies can be effective and legitimate. Here’s a breakdown of the most common myths:

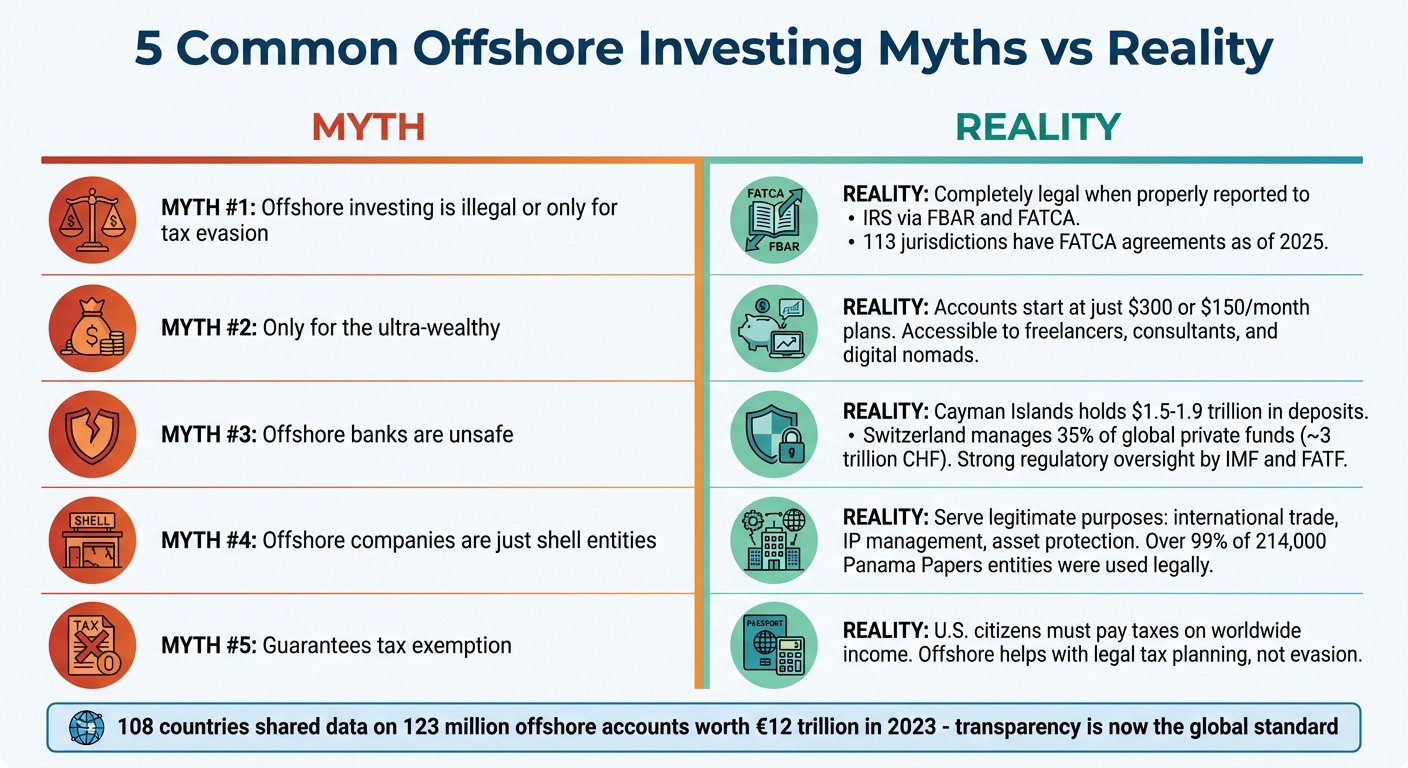

- Myth 1: Offshore investing is illegal or only for tax evasion.

Reality: It’s legal when reported correctly. Compliance with reporting laws like FBAR and FATCA ensures transparency. - Myth 2: Offshore investing is only for the ultra-wealthy.

Reality: Entry barriers have dropped significantly. Offshore accounts can now start with as little as $300 or monthly contributions of $150. - Myth 3: Offshore banks and investments are unsafe.

Reality: Reputable offshore jurisdictions adhere to strict regulations and global banking standards, often offering strong depositor protections. - Myth 4: Offshore companies are just shell entities.

Reality: Offshore companies serve practical purposes, such as international trade, asset protection, and intellectual property management. - Myth 5: Offshore investing guarantees tax exemption.

Reality: U.S. citizens must pay taxes on worldwide income. Offshore strategies can help with tax planning but not tax evasion.

Offshore investing is not shady or exclusive. When done transparently, it’s a smart way to protect and grow wealth while staying compliant with international and U.S. tax laws.

5 Common Offshore Investing Myths vs Reality

Myth 1: Offshore Investing Is Illegal or Only for Tax Evasion

Why This Myth Exists

The belief that offshore investing is inherently illegal or tied to tax evasion largely stems from high-profile scandals like the 2016 Panama Papers. These events brought global attention to illicit activities, fueling public suspicion of anything labeled "offshore". Stories of money laundering and fraud have further cemented the idea that offshore accounts are shady, even though most are perfectly lawful.

To put things into perspective, the United Nations Office on Drugs and Crime estimates that illicit funds and money laundering make up 2% to 5% of global GDP – about $2 trillion. This staggering figure contributes to the stereotype of offshore accounts as secretive havens for criminals. But in reality, many investors use offshore strategies for legitimate purposes like asset protection and portfolio diversification.

Breaking down these misconceptions helps reveal the legitimate, regulated side of offshore investing.

The Truth About Offshore Investing

Offshore investing is not only legal but also a common financial strategy when done transparently. The key difference between lawful offshore activity and illegal tax evasion lies in disclosure.

For U.S. citizens, the rules are clear: all foreign accounts must be reported, and worldwide income must be included on tax returns. Thanks to international agreements like FATCA, secrecy in offshore banking is a thing of the past. As of 2025, 113 jurisdictions have FATCA agreements in place, and in 2023, 108 countries shared information on 123 million offshore accounts worth more than €12 trillion.

"Offshore banking is legal when created for legitimate reasons… The key is to ensure full compliance with all tax and reporting laws." – Investopedia

How to Do It Right

Staying compliant with offshore investing rules is straightforward if you follow the required steps. Two key reporting requirements ensure your investments remain above board:

- FBAR (FinCEN Form 114): If your foreign account balances exceed $10,000, you must file an FBAR by April 15 (with an automatic extension to October 15).

- FATCA (Form 8938): U.S. residents must file this form if their foreign assets exceed $50,000 (or $200,000 for those living abroad). Attach it to your annual tax return.

It’s essential to keep detailed records for at least five years, including account details, bank addresses, and maximum annual balances. Don’t forget to complete Part III of Schedule B on your Form 1040 to disclose foreign accounts and their locations.

If you’re considering jurisdictions, Anguilla is an example of a location with zero corporate tax that fully complies with international reporting standards through a Model 1 Intergovernmental Agreement with the U.S..

Non-compliance can lead to severe penalties. Failing to file an FBAR, even unintentionally, can result in fines of up to $10,000. Willful violations are even steeper, with penalties reaching $100,000 or 50% of the account balance – whichever is greater. In some cases, criminal violations can lead to imprisonment for up to five years. By adhering to these rules, offshore investing becomes a legitimate and effective tool for securing and growing your wealth.

sbb-itb-39d39a6

Myth 2: Offshore Investing Is Only for the Ultra-Wealthy

Where This Myth Comes From

The media often portrays offshore investing as a luxury reserved for billionaires. Headlines linking offshore accounts to celebrities, tech giants, and multinational corporations have fueled this perception. Historically, this impression wasn’t far off – traditional offshore services did cater to high-net-worth individuals, with minimum investments ranging from $100,000 to $1 million. Add to that the costs of international travel, legal fees, and ongoing account maintenance, and it’s no wonder most people assumed offshore investing was out of reach for the average investor. However, this perspective no longer reflects today’s reality.

The Truth About Accessibility

Offshore investing has become much more accessible, thanks to increased transparency and evolving financial tools. These days, freelancers, consultants, e-commerce entrepreneurs, and digital nomads are leveraging offshore accounts for smoother international transactions and multi-currency banking. You no longer need a seven-figure net worth to benefit from these opportunities.

Modern banking options have significantly lowered the entry barriers. Some offshore banks now allow account openings with as little as $300, while investment plans can start with monthly contributions of just $150. Many jurisdictions, such as Georgia (TBC Bank), Puerto Rico (Euro Pacific Bank), Antigua (Global Bank of Commerce), and Switzerland (CIM Banque), now offer online onboarding and video KYC procedures. This means you can set up accounts remotely, without the need for costly international travel.

For example, setting up an Anguilla LLC and a Belize bank account can cost around $3,350 in the first year – a far cry from the high costs associated with traditional offshore services.

How to Get Started

Starting small is the key. Many investors begin with simple structures and scale up as needed. For instance, Anguilla offers zero corporate tax and no public ownership registry, making it an attractive option for digital businesses and entrepreneurs focused on privacy. Similarly, Estonia’s E-Residency program provides a cost-effective way to access EU markets and digital infrastructure, making it a great fit for tech startups and digital nomads.

One of the most beginner-friendly options is forming an LLC. This structure offers flexibility, personal liability protection, and practical uses like international invoicing, holding multi-currency bank accounts (USD, EUR, CHF), and safeguarding intellectual property.

If you’re looking for guidance, companies like Global Wealth Protection provide services tailored to entrepreneurs. They offer offshore company formation, tax minimization strategies, and personal consultations through their GWP Insiders membership program. These resources can help you navigate the setup process without needing substantial upfront capital or existing wealth.

That said, compliance is non-negotiable. For U.S. taxpayers, offshore accounts exceeding $10,000 in total value at any point during the year must be reported via an FBAR (Foreign Bank Account Report). Working with professionals ensures you meet reporting requirements and avoid penalties that could outweigh any potential gains.

Myth 3: Offshore Banks and Investments Are Unsafe

The Fear of Weak Regulation

Offshore banks often get a bad rap for being poorly regulated, and much of this belief comes from sensationalized media stories. These reports frequently link offshore financial centers to money laundering and other financial crimes, leading many to think these jurisdictions are lawless and unsafe. However, this perception doesn’t align with the reality of the strict regulatory frameworks many offshore centers follow.

The Truth About Offshore Banking Standards

Contrary to the "Wild West" label often associated with offshore banking, these jurisdictions operate under rigorous oversight. International organizations like the International Monetary Fund (IMF) and the Financial Action Task Force (FATF) keep a close watch on these financial centers. Banks in these regions must comply with global banking standards, including maintaining adequate capital reserves and submitting regular financial reports to local regulators.

Take the Cayman Islands as an example. This jurisdiction holds deposits totaling between $1.5 trillion and $1.9 trillion and is home to 40 of the world’s top 50 banks. Nobel laureate Joseph Stiglitz explains their legitimacy:

"If you said the US, the UK, the major G7 banks will not deal with offshore bank centers that don’t comply with G7 banks regulations, these banks could not exist. They only exist because they engage in transactions with standard banks."

Switzerland is another standout, managing approximately 35% of global private and institutional funds – around 3 trillion Swiss francs. Additionally, many reputable offshore jurisdictions offer depositor protection schemes. For instance, the Isle of Man guarantees up to £50,000 of net deposits per individual. Transparency has also improved significantly, with many jurisdictions now actively sharing financial information internationally.

How to Protect Your Assets

Choosing the right offshore jurisdiction is crucial for safeguarding your wealth. Look for locations with strong political and economic stability, such as Switzerland, the Cayman Islands, Jersey, Guernsey, or the Isle of Man. Ensure your chosen bank is regulated by a credible authority, like the Cayman Islands Monetary Authority.

Diversifying your assets is another effective strategy. Spread your funds across multiple jurisdictions and currencies to minimize risks. Multi-currency accounts in stable currencies like the U.S. dollar (USD), Euro (EUR), and Swiss Franc (CHF) can help protect against currency devaluation.

Services like Global Wealth Protection can assist with bank introductions to regulated offshore institutions, guiding you through due diligence and ensuring compliance with international standards.

Staying compliant with reporting requirements is equally important. Experienced professionals can help you navigate these obligations, ensuring your asset protection plan remains intact.

Here’s a quick comparison of reputable versus high-risk offshore jurisdictions:

| Feature | Reputable Offshore Jurisdictions | High-Risk Jurisdictions |

|---|---|---|

| Regulatory Oversight | Monitored by IMF; high FATF compliance | Often on FATF "grey" or "black" lists |

| Transparency | Participates in CRS and FATCA sharing | May resist international transparency |

| Bank Quality | Hosts branches of 40 of the world’s top 50 banks | Mostly local banks with limited global reach |

| Asset Protection | Strong legal frameworks and independent judiciaries | Higher risk of asset freezing or seizure |

Myth 4: Offshore Companies Are Just Shells with No Real Purpose

How Offshore Companies Got a Bad Reputation

High-profile scandals, like the Panama Papers, have unfairly cast offshore companies in a negative light. These stories often focus on misuse, branding such entities as tools for tax evasion or money laundering. Legally, a "shell company" refers to an entity that exists primarily on paper, without full-time employees or a physical office. While this might sound shady, the structure itself is entirely legal.

What’s often overlooked is the bigger picture. The media tends to spotlight the rare instances of abuse, overshadowing the legitimate ways most offshore companies are used. This skewed perception ignores the practical roles these entities play in global business.

Legitimate Uses for Offshore Companies

Offshore companies are far from being mere paper entities; they serve real, practical functions, especially for businesses operating internationally.

- International trade: Businesses involved in dropshipping, import/export, or cross-border invoicing use offshore companies to simplify multi-currency transactions and reduce administrative hurdles.

- Intellectual property management: Offshore entities are often used to hold trademarks, patents, or software. This setup allows businesses to centralize licensing and collect royalties efficiently.

- Asset protection: These structures provide legal safeguards, helping individuals protect their wealth from lawsuits, creditor claims, or political instability.

Privacy is another key benefit. Jurisdictions like Anguilla or Belize allow business owners to keep shareholder information private, offering protection for personal and financial security. Additionally, offshore companies can play a role in estate planning. For example, Panamanian foundations help streamline the transfer of international assets, avoiding costly probate processes. As Eli Carter from OVZA explains:

"Offshore companies are one of the most misunderstood tools in international business… most [clients] aren’t looking for loopholes. They’re looking for structure."

How to Use Offshore Companies Properly

For those considering offshore companies, proper setup and compliance are crucial. The choice of jurisdiction plays a significant role. For example, Anguilla has become a favorite for crypto and digital businesses, thanks to its zero corporate tax rate and lack of a public ownership registry. Setting up a company here typically costs around $3,350, with annual fees ranging from $500 to $2,000.

Compliance is not optional. U.S. citizens must file an FBAR if their offshore accounts exceed $10,000 in total value. Additionally, many jurisdictions now require companies to demonstrate economic substance – proof of legitimate business activities and minimal operational standards. Transparency has become the global standard, with 108 countries sharing data on 123 million offshore accounts worth over €12 trillion in 2023 alone.

Offshore companies can deliver significant benefits, but they demand careful management and adherence to legal requirements. Global Wealth Protection offers full-service packages for offshore company formation in jurisdictions like Anguilla. These services include filing paperwork, obtaining certifications, and setting up bank accounts, ensuring compliance with international standards. As Mark Nestmann aptly puts it:

"The reality is that these financial arrangements are often practical, necessary, and above all, legal."

Myth 5: Offshore Investing Guarantees Tax Exemption

What U.S. Citizens Need to Know About Taxes

There’s a widespread belief that offshore investing magically erases U.S. tax obligations. Unfortunately, that’s far from the truth. If you’re a U.S. citizen, green card holder, or resident alien, you’re required to pay taxes on your worldwide income – no matter where you live or earn that money. The IRS spells it out clearly:

"U.S. citizens, resident aliens and certain nonresident aliens are required to report worldwide income from all sources including foreign accounts and pay taxes on income from those accounts at their individual rates."

Simply moving your money or investments offshore doesn’t change this requirement. While offshore investing can be perfectly legal and useful for diversifying assets, using it to dodge taxes is against the law. The key difference lies in tax planning versus tax evasion: one is legal, the other isn’t.

The reporting requirements for offshore accounts are strict. If the combined value of your foreign financial accounts exceeds $10,000 at any point during the year, you must file an FBAR (FinCEN Form 114). On top of that, Form 8938 comes into play if your foreign financial assets exceed certain limits – starting at $50,000 for single filers living in the U.S. and going up to $600,000 for married couples filing jointly while living abroad. Under FATCA (Foreign Account Tax Compliance Act), foreign financial institutions must also report details about accounts held by U.S. taxpayers directly to the IRS.

Legal Tax Planning Methods

Reducing tax liability is possible when done legally. Tools like foreign tax credits, the Foreign Earned Income Exclusion, and tax treaties can help prevent double taxation.

The IRS distinguishes between honest mistakes and deliberate tax avoidance. For example, failing to file an FBAR because of non-willful error can result in penalties of up to $15,611 per violation (as of 2024). However, willful violations come with much harsher penalties – up to the greater of $156,107 or 50% of the account balance. Failing to disclose assets on Form 8938 could cost you an initial $10,000 penalty, with additional fines up to $60,000 for continued non-compliance.

Some offshore investments can also trigger unexpected tax headaches. Take foreign mutual funds or ETFs, for instance. These often fall under the Passive Foreign Investment Company (PFIC) rules, which can lead to much higher tax rates compared to similar U.S.-based investments. Similarly, if you set up or transfer assets into a foreign trust, U.S. tax laws typically treat you as the trust’s owner, meaning you’re taxed on the trust’s income under grantor trust rules.

How to Plan Your Taxes Correctly

Staying compliant requires meticulous record-keeping and adherence to IRS rules. Maintain detailed records for at least five years, including account names, numbers, and maximum yearly balances. When converting foreign currencies to U.S. dollars, use the Treasury Bureau of the Fiscal Service‘s exchange rate from the last day of the calendar year.

If you’ve overlooked reporting foreign assets, don’t just start filing correctly from now on. Instead, explore options like the IRS’s Streamlined Filing Compliance Procedures, which can help reduce penalties. Keep in mind that if you fail to report over $5,000 in income from foreign assets, the IRS can extend the statute of limitations on your tax return to six years.

For personalized guidance, Global Wealth Protection offers consultations to help you navigate offshore tax obligations. These sessions provide step-by-step advice on handling FBAR, FATCA, and complex tax regimes like PFIC and CFC rules – all with the goal of maximizing tax efficiency while staying fully compliant with U.S. laws.

Myths vs. Reality: A Quick Comparison

Understanding the difference between myths and facts can clear up confusion about offshore investing. The table below highlights common misconceptions, the truth behind them, and how Global Wealth Protection offers solutions that are both practical and compliant.

Offshore investing isn’t about tax evasion or exclusive privileges for the wealthy. When approached correctly, it’s a legitimate strategy for protecting assets, diversifying investments, and managing international business interests.

Comparison Table

| Myth | Reality | Our Approach |

|---|---|---|

| Offshore investing is illegal. | Offshore investing is completely legal when properly reported to the IRS. | We ensure full transparency by adhering to FBAR and FATCA reporting requirements. |

| It is only for the ultra-wealthy. | Offshore accounts can start with deposits as low as $300 or plans beginning at $150/month. | We offer entry-level savings and investment platforms to help clients grow wealth globally. |

| Offshore banks are unsafe. | Many offshore banks are more stable and better rated than domestic ones. | We select jurisdictions with strong legal systems and highly rated financial institutions. |

| It is a way to avoid all taxes. | U.S. citizens must pay taxes on their worldwide income, no matter where it’s earned. | We focus on legal tax planning, using foreign tax credits and compliant structures to reduce double taxation. |

| Offshore companies are just shells. | Offshore entities serve legitimate purposes like international trading, asset holding, and privacy. | We help clients establish offshore structures (e.g., LLCs, Trusts) for asset protection and business continuity. |

This comparison shows how offshore investing, when done responsibly, can be a smart financial strategy, not a risky or unethical venture.

Conclusion: Moving Past the Myths

Offshore investing often gets a bad rap, painted as risky or even illegal. But the truth is far from the myths surrounding it. Claims that it’s only for tax evasion, reserved for the ultra-wealthy, unsafe, or a guaranteed tax loophole are largely based on dramatized media stories and misconceptions. In fact, an analysis of the Panama Papers showed that over 99% of the 214,000 offshore entities were used for legal purposes.

"Offshore isn’t shady. It’s smart." – Global Wealth Protection

This quote perfectly sums up the reality of offshore investing. When done with accurate information and full compliance, it can be a legitimate and strategic financial tool. Staying in line with U.S. reporting requirements is non-negotiable, but within those boundaries, offshore structures can offer real advantages – like asset protection, currency diversification, access to global markets, and legal privacy. Recent regulations have also made the process more transparent and compliant than ever.

For investors looking to unlock these benefits, working with the right professionals is critical. Certified tax specialists and experienced offshore attorneys can help navigate the complex reporting requirements and ensure every step aligns with the law. Global Wealth Protection specializes in creating offshore strategies that focus on transparency, legal tax efficiency, and safeguarding assets – steering clear of anything unethical or illegal.

Whether you’re aiming to protect your wealth, diversify internationally, or manage a global business, success comes down to setting clear goals, seeking expert guidance, and strictly adhering to U.S. tax laws. Offshore investing, when done right, is not just smart – it’s entirely above board.

FAQs

Which offshore jurisdictions are considered reputable for U.S. investors?

Reputable offshore locations for U.S. investors often combine strong legal frameworks, privacy protections, and tax advantages. Some well-known jurisdictions include the Cayman Islands, Belize, Singapore, Hong Kong, Switzerland, Nevis, and the Isle of Man. These destinations are recognized for their reliable asset protection, commitment to confidentiality, and adherence to international compliance standards, making them appealing for those looking to diversify and secure their wealth.

What documents do I need before opening an offshore bank or brokerage account?

To set up an offshore bank or brokerage account, you’ll typically need a valid passport and proof of address. In some cases, additional paperwork – like bank statements or proof of funds – may also be required. These documents are essential for meeting regulatory requirements and maintaining transparency.

How do I avoid PFIC taxes when investing offshore?

To steer clear of PFIC taxes, U.S. taxpayers should consider investing in alternatives like specific domestic funds or offshore structures that fall outside the PFIC classification. It’s crucial to work with a tax professional to ensure you’re meeting compliance requirements and planning appropriately. PFICs are tied to strict taxation rules under U.S. law, and expert advice can help you manage these intricate regulations with confidence.