Want to protect your wealth during economic downturns? Crisis-proof investments are your solution. These assets – like gold, real estate, and commodities – retain their value even when markets crash. Here’s what you need to know:

- Gold: Historically, gold thrives during crises. For example, it surged 60% in 2025, reaching nearly $5,000/oz.

- Real Estate: Offers stability through rental income and lower volatility compared to stocks.

- Offshore Investments: Diversify globally to reduce reliance on one economy and shield assets from domestic risks.

- Alternative Assets: Art, collectibles, and commodities provide unique portfolio protection.

Economic crises hit stocks hard, but these assets can secure your financial future. By diversifying into crisis-resistant options, you can safeguard your wealth against inflation, volatility, and market downturns. Let’s explore how each investment works and how they can fit into your portfolio.

Crisis-Proof Investment Performance Comparison During Economic Downturns

Precious Metals: Gold, Silver, and Beyond

When it comes to assets that hold their ground during turbulent times, precious metals consistently prove their worth. Their physical nature means they don’t rely on anyone else’s promise to pay, which eliminates counterparty risk entirely. This makes them a go-to choice when markets are shaky.

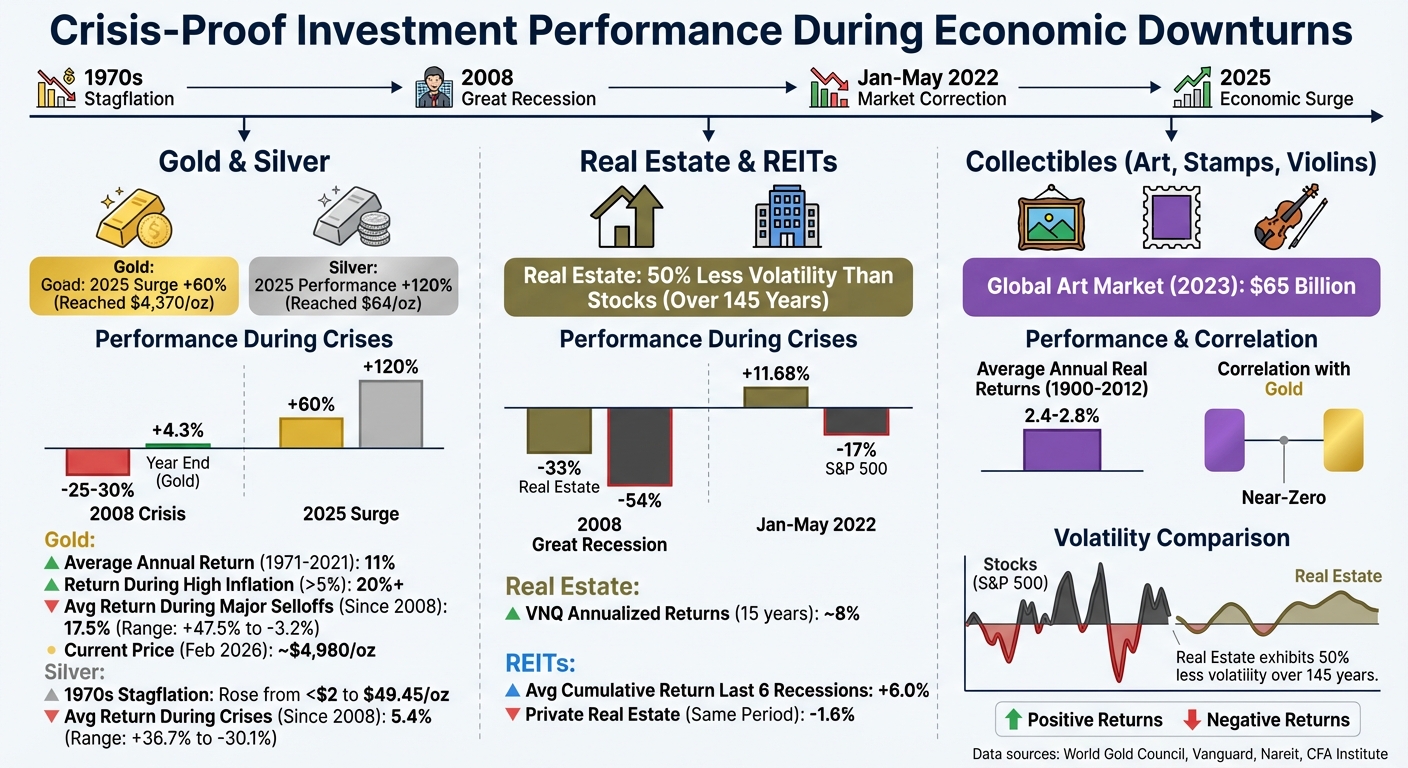

Looking at the numbers, gold’s performance over time is hard to ignore. Between 1971 and 2021, gold delivered an average annual return of nearly 11%. During periods of high inflation – when U.S. inflation exceeded 5% – those returns climbed above 20%. Meanwhile, major currencies have steadily lost value against gold. For example, in the 21st century alone, they’ve dropped over 90%, and over the last century, that figure jumps to 99%.

Precious metals also tend to move in the opposite direction of traditional assets like stocks and bonds. A perfect example is the 2008 financial crisis. Initially, gold dropped by 25–30% as investors sold off assets to meet margin calls. But it didn’t stay down for long. By the end of the year, gold had rebounded to post a 4.3% gain and climbed to a record $1,918 by 2011. Fast forward to 2025, gold surged over 60% to break $4,370 in October, fueled by trade disruptions, a government shutdown, and central banks – especially China – stockpiling reserves for seven straight months. These examples highlight gold’s enduring role as a safe store of value.

Gold as a Store of Value

Gold’s value often reacts strongly to economic policy changes, especially quantitative easing and interest rate cuts. Take what happened after President Nixon ended the gold standard in 1971. Gold’s price skyrocketed from $35 per ounce to $850 by early 1980, a staggering 2,300% increase, as U.S. inflation peaked at 14.8%. More recently, during the COVID-19 pandemic, gold climbed from around $1,515 in early 2020 to hit $2,067 by August of that year, following aggressive Federal Reserve measures to stabilize the economy.

As Ben Bernanke, former Federal Reserve Chair, succinctly put it:

"The reason people hold gold is as a protection against what we call tail risk, really, really bad outcomes."

Gold’s resilience during market turmoil is equally impressive. According to the World Gold Council, gold has averaged a 17.5% return during major market selloffs since 2008, with gains reaching as high as 47.5% and losses capped at just 3.2% in the worst-case scenario. As of February 2026, gold was trading between $4,978.89 and $4,980.34 per ounce.

Its appeal isn’t just financial – gold also benefits from consumer demand in the jewelry and tech industries. At the same time, gold mine production has grown at a modest pace of 1.7% annually over the past two decades, reinforcing its scarcity and long-term value.

Silver, Platinum, and Palladium

While gold is the dominant player, other precious metals bring their own advantages. Silver, for instance, often tracks gold’s movements but tends to be more volatile. This is because it serves a dual purpose: as a monetary asset and as an industrial metal. During the stagflation of the 1970s, silver’s price jumped from under $2 to $49.45 per ounce. In 2025, it outpaced gold by surging over 120%, reaching new highs above $64 per ounce. However, silver’s performance is closely tied to industrial demand, which means it can experience sharper declines when manufacturing slows. Since 2008, silver has averaged a 5.4% return during market crises, with gains as high as 36.7% but losses plunging as low as 30.1% – a stark contrast to gold’s minimal 3.2% downturn. Historical data from 1688 to 2018 further shows that while gold is a reliable crisis hedge, silver doesn’t consistently offer the same stability.

Platinum and palladium, on the other hand, are heavily tied to industrial uses, particularly in automotive catalytic converters. Their value tends to follow industrial production cycles rather than responding to inflation or monetary policy, making them less effective as crisis hedges. However, they can still add diversification to a portfolio.

When it comes to reliability, gold remains the standout choice, with silver offering a higher-risk, higher-reward option. As Chris Temple, founder of National Investor, aptly notes:

"The bond market understands that Washington is so broken and the debt situation is so bad. That’s why gold all of a sudden is the safe haven now, even more than treasuries."

sbb-itb-39d39a6

Real Estate: Physical Assets That Endure

Real estate plays a key role in a well-rounded, crisis-resistant portfolio, offering a steady and tangible alternative to more unpredictable investments. Unlike paper assets, real estate fulfills a basic human need – shelter. Regardless of economic turmoil, people need homes, businesses need workspaces, and storage space remains essential. This foundational demand helps stabilize real estate values in ways that stocks and bonds cannot.

Take the 2008 Great Recession as an example. While the S&P 500 nosedived 54%, home values fell by 33% – a smaller drop, even though the crisis was housing-related. More recently, between January and May 2022, the S&P 500 declined 17%, yet residential real estate delivered an 11.68% return.

The stability of real estate comes partly from its illiquid nature and consistent rental income. Unlike stocks, which can see sharp daily swings, property transactions move slowly, reducing the likelihood of panic-driven sell-offs. Rental income also tends to hold steady – or even rise – during economic downturns as renting becomes a more attractive option.

Over the past 145 years, real estate has shown half the volatility of stocks. For instance, the Vanguard Real Estate ETF (VNQ) has delivered around 8% annualized returns over the last 15 years. As Christopher Stroup, the founder of Silicon Beach Financial, puts it:

"Real estate and gold feel tangible. They’re physical, familiar, and have long histories tied to wealth preservation."

This stability varies between residential and commercial real estate, each with its own strengths.

Residential vs. Commercial Properties

Not all real estate reacts the same way during economic downturns. Residential properties, especially affordable housing supported by programs like Section 8 vouchers, tend to maintain high occupancy rates even in tough times.

Commercial real estate, on the other hand, presents a more complex picture. While office and retail spaces often struggle during recessions as businesses downsize or close, certain commercial sectors are surprisingly resilient. For example, self-storage facilities were the only commercial asset class to generate positive returns during the 2008 Great Recession. When people downsize or move in with family, they still need storage for their belongings, making this sector a safe bet.

Other durable commercial investments include healthcare facilities, data centers, and student housing. Student housing, for instance, often sees increased demand during recessions as more young adults opt to return to school instead of entering a weak job market. In 2021, commercial real estate prices climbed 11.5%, outpacing the 5.6% growth in residential property prices.

The difference often lies in necessity. Residential properties benefit from their connection to basic survival needs, while some commercial sectors depend on discretionary spending and face higher risks. As J Scott, author of Recession-Proof Real Estate Investing, notes:

"Of the other 34 recessions that we’ve seen over the past 160 years, real estate has never dropped more than one or 2%."

For investors looking to gain real estate exposure without direct property ownership, REITs offer an attractive alternative.

Real Estate Investment Trusts (REITs)

Real Estate Investment Trusts (REITs) are an excellent option for those who want the benefits of real estate without the responsibilities of property management. REITs allow investors to earn passive income through dividends while accessing a diversified portfolio of properties with far less capital than direct ownership requires.

During the last six recessions, REITs achieved an average cumulative total return of 6.0%, outperforming private real estate, which averaged -1.6%. They also continued to outperform in the year following each recession. As Edward F. Pierzak from Nareit explains:

"REITs outperformed private real estate during a recession, and REITs outperformed private real estate in the four quarters after a recession."

However, REITs come with a trade-off. While direct property ownership offers low correlation with stock markets, publicly traded REITs are more closely tied to market fluctuations, making them vulnerable to short-term volatility.

Ultimately, the choice depends on your investment goals. Direct ownership provides stability and independence from market swings but requires significant capital and hands-on management. REITs, on the other hand, offer liquidity, diversification, and ease of access but are more sensitive to stock market trends. Many investors find a balance by combining the two – using direct ownership for long-term stability and REITs for liquidity and diversification.

Offshore Diversification: International Asset Protection

Spreading your wealth across multiple countries can act as a safeguard against domestic economic or political instability. When all your assets are tied to a single government, you’re more exposed to risks like policy changes, currency devaluation, bank collapses, or legal disputes. By diversifying internationally, you distribute your assets across different legal systems, currencies, and banking networks, which strengthens your financial resilience.

The numbers highlight the urgency. Since early 2025, the US dollar has dropped over 10% against the DXY index – a basket of major global currencies – marking its worst six-month performance since 1973. With the US national debt surpassing $31 trillion, diversifying your currency exposure is becoming a key strategy for safeguarding wealth.

Legal risks also pose a significant threat. In 2023 alone, approximately 5 million new lawsuits were filed in the United States. For those with substantial assets, it’s not a matter of if legal challenges arise, but when. Offshore structures can shield your wealth by placing it under foreign legal systems, forcing creditors to relitigate claims under local laws.

Advantages of Offshore Holdings

Offshore holdings come with several strategic benefits that build on these risks. One of the most important is jurisdictional separation. Assets held in a foreign entity governed by local laws and managed by an independent trustee are far harder for domestic courts to access.

Another advantage is currency diversification. By holding assets in currencies like the Swiss Franc, Singapore Dollar, or UAE Dirham, you reduce your dependence on the performance of a single currency.

International banking systems also provide a buffer against risks like bank runs or regulatory restrictions. And while offshore holdings require full tax compliance, they often operate in jurisdictions with strict confidentiality standards, lowering exposure to predatory lawsuits.

Physical assets, such as foreign real estate, add another layer of security. Many American investors are buying properties in stable locations like Portugal (e.g., Lagos), Panama, or Mexico (e.g., Tulum and Playa del Carmen) as long-term safe havens. Similarly, obtaining a second passport can provide a tangible retreat if domestic conditions worsen.

Timing is critical when setting up offshore structures. These measures must be in place well before a crisis or legal dispute arises. Transfers made after issues emerge could be reversed as fraudulent. As The Nestmann Group advises:

"The best plan is to set up protection years before any trouble. This way, no one can say you were trying to dodge a specific person who’s after your money".

Selecting Offshore Jurisdictions

Choosing the right jurisdiction is essential for maximizing protection. Not all offshore locations offer the same level of security. The most effective jurisdictions combine strong legal protections, political stability, and respect for property rights.

Cook Islands

Known for robust asset protection trusts, the Cook Islands require creditors to relitigate claims under local laws. They also impose a high burden of proof and enforce short statutes of limitations for challenging transfers. Setting up a trust here typically costs around $29,000.

Nevis

Nevis offers strong privacy protections and limits creditors to charging orders, which only grant access to distributions, not the underlying assets. It’s a cost-effective alternative to the Cook Islands for LLCs and trusts.

Switzerland

Renowned for banking stability, Switzerland requires a minimum of $1 million for asset management accounts. Its strict custody laws ensure client holdings are separate from the bank’s own balance sheets. The Swiss Franc’s reputation as a safe-haven currency further enhances its appeal.

Singapore

With its conservative financial regulations and strong data confidentiality laws, Singapore provides a secure gateway to Asian markets. It balances international reporting compliance with stringent national data protection standards.

Panama

Panama’s use of the US dollar and its stable legal infrastructure make it a popular choice for real estate investments and residency options.

Here’s a quick comparison of some top jurisdictions:

| Jurisdiction | Primary Benefit | Minimum Investment | Best For |

|---|---|---|---|

| Cook Islands | Strong asset protection laws | ~$29,000 setup | Asset protection trusts |

| Switzerland | Banking stability & currency | $1,000,000 | High-net-worth liquid assets |

| Nevis | Privacy & creditor barriers | Lower than Cook Islands | Offshore LLCs and trusts |

| Singapore | Financial regulation & access | Varies | Asian market access |

| Panama | USD convenience | Varies | Real estate & residency |

Austrian private banking offers another option, with minimum deposits typically ranging from $250,000 to $300,000. For ultra-high-net-worth individuals, Private Placement Life Insurance (PPLI) structures provide creditor protection and tax-deferred growth, though these often require investments starting at $2 million.

Compliance is non-negotiable. US citizens must file an FBAR (FinCEN Form 114) if the total value of their foreign accounts exceeds $10,000 during the year. Additional IRS reporting – such as Form 8938 (FATCA), Forms 3520/3520-A (Foreign Trusts), and Form 5471 (Foreign Corporations) – may also be required. The penalties for non-compliance can be severe.

To build a strong defense, combine offshore strategies with domestic tools like umbrella insurance and retirement accounts. Keep enough assets onshore to cover immediate needs or potential settlements, and always work with reputable banks and trustees in stable jurisdictions.

Alternative Investments: Art, Collectibles, and Commodities

Beyond tangible assets and offshore strategies, alternative investments can further diversify and protect your portfolio. When traditional markets falter, some investors explore non-traditional options like art, rare collectibles, and commodities. Each offers a unique form of protection but comes with its own set of challenges. Between 1900 and 2012, collectibles such as art, stamps, and rare violins achieved average annual real returns of 2.4% to 2.8%, outperforming government bonds, Treasury bills, and even gold during that time. On top of financial returns, these assets often bring personal enjoyment.

Art and Collectibles as Wealth Stores

Fine art and collectibles are often seen as both passion investments and financial hedges. In 2023, the global art market saw sales of around $65 billion, and studies reveal that art indices have a near-zero correlation with gold, offering diversification that precious metals alone cannot. However, not all art performs equally well during economic downturns. For example, nineteenth-century paintings and sculptures are considered among the most stable, retaining their value even when contemporary art becomes more vulnerable to market fluctuations. During times of war and political uncertainty, smaller, portable paintings have historically delivered better returns than larger works, making portability an essential factor for collectors focused on crisis preparedness.

Other collectibles, such as stamps and rare musical instruments – especially violins – have shown appreciation rates comparable to fine art. Neeti Goyal of the CFA Institute emphasizes their value as long-term assets:

"Smart investors should consider emotional assets to be safe havens and a long-term store of value".

However, investing in these items demands expertise. Buyers must confirm provenance (the documented history of ownership), check for inclusion in a catalog raisonné (a comprehensive listing of an artist’s works), and obtain independent condition reports from conservation experts. High transaction costs, including commissions, specialized shipping, storage, and insurance, add to the complexity. As such, collectibles are best suited for long-term holding rather than quick liquidation.

While art and collectibles offer both tangible and emotional value, commodities provide a more direct hedge against economic volatility.

Commodities: Oil, Agriculture, and Industrial Metals

Unlike art and collectibles, commodities derive their value from real-world demand. When inflation rises or currencies weaken, prices for oil, agricultural goods, and industrial metals often climb, helping to preserve purchasing power. Commodities are fungible, meaning they have standardized pricing and liquid markets, making them easier to trade compared to unique collectibles.

However, investing in commodities comes with its own risks. Prices can be highly volatile, influenced by supply chain disruptions, political instability in producing regions, and changes in global demand. Unlike collectibles, commodities don’t offer sentimental or aesthetic value – you can’t admire a barrel of oil or a bushel of wheat. Their worth is purely financial, requiring a solid understanding of market trends.

For investors seeking a diversified, crisis-resistant portfolio, commodities work best as part of a broader strategy. This might include tangible assets like precious metals and real estate, as well as offshore holdings to spread risk across jurisdictions. Together with traditional investments, these alternatives can create a well-rounded approach to weathering economic challenges.

Conclusion: Building Your Crisis-Resistant Portfolio

Key Takeaways

A crisis-resistant portfolio is your financial safety net during uncertain times. The cornerstone of this approach is diversification across uncorrelated assets – investments that don’t all move together. Ray Dalio, the founder of Bridgewater Associates, sums it up perfectly:

"My mantra of investing is 15 good uncorrelated return streams, risk-balanced. This allows investors to maintain the same return as any one of those investments with an 80% reduction in risk".

Tangible assets, like precious metals or real estate, hold their value even when paper currencies lose purchasing power. Historically, fiat currencies tend to decline, while tangible assets often gain value. Real estate provides additional protection, especially during inflation, as landlords can adjust rents to match rising costs. Offshore diversification adds another layer of security by spreading investments across different jurisdictions, shielding you from country-specific risks. Alternative investments – such as art, collectibles, and commodities – further strengthen your portfolio by reacting differently to economic pressures.

Since 1926, diversified portfolios have consistently outperformed concentrated ones by an average of 0.55% annually, with compounding benefits over time. To prepare for any economic environment – whether it’s rising or falling growth, or rising or falling inflation – your portfolio should be structured to thrive in all four scenarios. By combining domestic stability with offshore strategies, you create a solid defense against unpredictable economic shifts.

Steps to Protect Your Wealth

Start by drafting an Investment Policy Statement (IPS). This document outlines your risk tolerance and pre-planned strategies for managing volatility, helping you avoid emotional decisions during market swings. Additionally, maintain cash reserves to cover three to six months of expenses, ensuring you won’t need to sell investments at a loss during downturns.

Make it a habit to review your portfolio annually. If your investments stray from their target allocations, rebalance by selling assets that have overperformed and reinvesting in those that have underperformed. This keeps your risk profile aligned with your goals .

"Anytime we see red in our portfolios, we ask ourselves, have the fundamentals changed? Has the underlying thesis changed? If not, then the wings still hold and we stay buckled in".

Given the complexities of regulations, tax considerations, and international investment strategies, professional guidance can be invaluable. Global Wealth Protection specializes in creating tailored solutions to help individuals build and maintain portfolios designed for long-term stability and security.

FAQs

How much gold should I own?

It’s often suggested to dedicate 5% to 20% of your investment portfolio to gold. The specific percentage hinges on a few key factors, such as your risk tolerance, financial objectives, and age. Including gold in your portfolio can act as a safety net, protecting your wealth during periods of economic instability while complementing your broader investment strategy.

Should I buy rental property or REITs?

Choosing between rental properties and REITs comes down to your personal goals and how involved you want to be. Rental properties are physical assets that can appreciate over time and provide a steady stream of income, but they demand active management – think tenant issues, maintenance, and other responsibilities.

On the flip side, REITs (Real Estate Investment Trusts) offer benefits like diversification, liquidity, and minimal effort. They generate income through dividends and allow you to invest in real estate without the headaches of property management.

Both options can strengthen your portfolio against economic uncertainty. Rental properties are ideal for hands-on investors, while REITs are perfect for those who value convenience and flexibility.

What offshore accounts must I report to the IRS?

U.S. citizens and residents are required to report foreign bank accounts, securities accounts, and trusts if their combined value exceeds $10,000 at any time during the year. This involves filing the FBAR (FinCEN Form 114) and, for certain cases, Form 8938 when foreign financial assets surpass specific thresholds. Non-compliance can lead to steep penalties, making it crucial to carefully report all qualifying accounts.