Currency fluctuations impact your wealth by changing the value of international investments, overseas properties, and foreign income. A strong dollar makes European assets cheaper for Americans, while a weak euro lowers the dollar value of euro-denominated holdings. Here’s what you need to know:

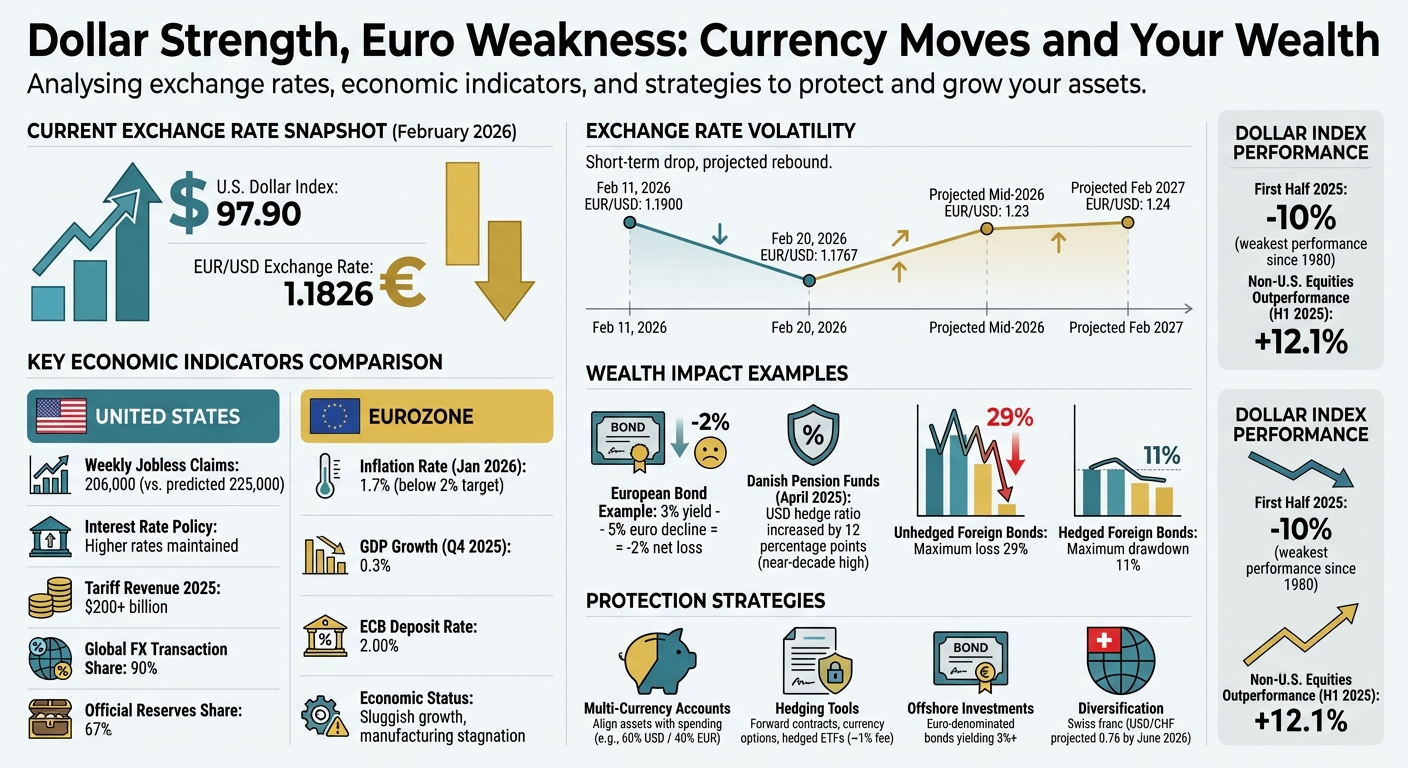

- Dollar Rebound: After a dip in 2025, the U.S. Dollar Index climbed to 97.90 by February 2026, with the EUR/USD exchange rate at 1.1826.

- Key Drivers: The dollar’s strength is fueled by a resilient U.S. economy, higher interest rates, and safe-haven demand. The euro weakens due to low inflation, slow growth, and geopolitical uncertainty.

- Impact on Investments: A strong dollar reduces the value of euro-denominated assets for Americans but makes European investments more affordable.

- Future Trends: Analysts predict the EUR/USD rate may rise to 1.23 by mid-2026, signaling potential dollar weakness ahead.

To protect your wealth, consider multi-currency accounts, hedging tools like forward contracts, and diversifying into stable or growth-focused currencies. Monitoring economic indicators and working with financial advisors can help you stay ahead of currency volatility.

The Strong Dollar and Weak Euro: What’s Happening

After a dip in 2025, the dollar made a solid comeback by mid-February 2026. Over four consecutive sessions, the U.S. Dollar Index climbed to around 97.90, while the EUR/USD exchange rate hovered near 1.1826. This shift marks a notable recovery, setting the stage to explore the factors behind the dollar’s strength and the euro’s decline.

What’s Driving the Dollar Higher

The U.S. economy’s resilience is a key factor. Strong economic data, like a drop in weekly jobless claims to 206,000 in February 2026 – well below the predicted 225,000 – supports the Federal Reserve‘s ability to maintain higher interest rates. A robust labor market adds to this momentum.

The dollar’s status as a safe haven also plays a role, especially with rising tensions in the Middle East. Markets are betting that the Federal Reserve won’t cut rates significantly until at least June 2026, keeping the dollar attractive due to its yield advantage.

"It doesn’t look like an economy suffering from higher rates. Even with the pressure from the White House to lower rates, that pressure doesn’t really hit until May, so there’s no real trend to this information right now."

- Joseph Trevisani, Senior Analyst, FXStreet

Trade policies have further strengthened the dollar. The U.S. collected over $200 billion in tariff revenues during 2025, and the potential for additional trade barriers has drawn investor interest. The dollar’s dominance in global finance – accounting for nearly 90% of foreign exchange transactions and two-thirds of official reserves – adds to its appeal.

Why the Euro Is Weakening

The euro, on the other hand, faces mounting challenges. Inflation in the Eurozone slipped to 1.7% in January 2026, falling below the European Central Bank‘s (ECB) 2% target. This has led to expectations of a more dovish ECB stance compared to the Fed.

Economic growth in the euro area remains sluggish, with just a 0.3% rise in GDP during the final quarter of 2025. While the services sector shows some growth, manufacturing continues to stagnate. Trade disruptions and higher tariffs are complicating supply chains and dampening export demand. Additionally, the ongoing conflict in Ukraine is eroding both consumer and business confidence, adding to economic uncertainty.

"Further frictions in international trade could disrupt supply chains, reduce exports and weaken consumption and investment."

- ECB Governing Council

Capital flows are another factor. Investors are favoring U.S. equity markets, particularly in sectors like artificial intelligence, over European markets. This shift has driven more capital into the dollar, further weakening the euro.

What This Means for Exchange Rates

The relationship between the dollar and the euro has a direct impact on cross-border trade and the value of international investments. Recent fluctuations highlight this volatility: between February 11 and February 20, 2026, the EUR/USD rate shifted from 1.1900 to 1.1767.

For Americans with euro-denominated assets, the euro’s decline means these holdings are now worth less in dollar terms. On the flip side, a stronger dollar makes European investments – like real estate or stocks – more affordable. The interest rate gap also plays a role, with the ECB’s deposit rate at 2.00% compared to higher U.S. rates, influencing exchange rate dynamics.

Looking ahead, analysts predict the EUR/USD rate could climb to 1.24 by February 2027, signaling sustained dollar strength in the near term. However, currency markets remain unpredictable, shaped by policy changes, geopolitical events, and economic data. These rapid shifts emphasize the importance of adjusting multi-currency strategies to protect offshore assets and navigate currency volatility effectively.

sbb-itb-39d39a6

How Currency Changes Affect Your Wealth

Understanding how currency fluctuations impact your wealth is a critical part of managing your financial well-being. These changes can influence your investments, spending habits, and income streams. Below, we’ll explore how currency shifts affect asset values, purchasing power, and multi-currency income.

Impact on Asset Values and Investment Returns

Currency movements can significantly influence the value of your investments. For example, when the U.S. dollar strengthens, the dollar value of assets denominated in euros – like European stocks, bonds, or real estate – decreases when converted back to dollars. In fact, currency swings often have a greater impact on international fixed-income returns than the performance of the underlying bonds themselves. A European bond offering a 3% yield might result in a 2% net loss if the euro declines by 5%.

"When a foreign-currency fixed income position is unhedged, the return is to a larger extent driven by currency moves instead of the underlying asset, undermining the purpose of holding the position in the first place."

- Samuel Zief, Global Macro Strategist, J.P. Morgan Private Bank

The effect of currency changes varies across asset classes. For instance, international equities are often left unhedged because their return volatility tends to outweigh the impact of exchange rate fluctuations, making hedging less cost-effective. A notable example: in April 2025, Danish pension funds and insurers raised their U.S. dollar hedge ratio by 12 percentage points, reaching a near-decade high to mitigate the risks of a weakening dollar. These examples highlight the importance of hedging strategies, which will be covered later.

Changes to Purchasing Power and International Spending

When the dollar strengthens, your purchasing power increases when spending abroad. If you own a vacation home in France or Italy, your euro-denominated expenses – like property taxes, utilities, and maintenance – become cheaper in dollar terms. However, this advantage can be a double-edged sword. If you’re planning to retire in Europe or have children studying there, a strong dollar today might lead to unrealistic expectations about future costs should the currency relationship shift.

Managing Currency Risk for Multi-Currency Income

For those earning income in euros – whether from rental properties, business operations, or dividends – a stronger dollar reduces the value of that income when converted to U.S. dollars. The key risk arises when your income or assets are in one currency, but your expenses or liabilities are in another.

One way to manage this risk is through natural hedging – aligning your income and expenses in the same currency to avoid conversion fees and reduce exposure to exchange rate volatility. For example, if you earn in euros and also have euro-denominated expenses, you can use that income directly to cover those costs. Another strategy is to align your portfolio’s currency mix with your future spending needs. Estimating the percentage of expenses expected in each currency over the next 5 to 20 years can provide a solid framework for managing currency risk. These steps lay the groundwork for effective strategies to handle currency fluctuations.

How to Protect Your Wealth from Currency Volatility

Understanding how currency fluctuations affect your wealth is just the first step. The next move is taking action to shield your assets from these changes. Below are practical strategies to help you manage risk and prepare your portfolio for the challenges posed by a strong dollar and a weakening euro.

Holding Multi-Currency Accounts

A simple way to handle currency risk is to align your assets with your spending needs. For example, if you own property in Europe, have recurring expenses overseas, or plan to retire abroad, holding local currency can help you avoid hefty conversion fees. Multi-currency accounts make it easier to receive income and pay expenses in local currencies, sidestepping the losses that come from bank spreads on every transaction.

"Currency planning is about alignment, not optimisation." – Kumar Patel, Private Wealth Adviser, Skybound Wealth USA

Start by estimating your future spending. If 60% of your expenses are in the U.S. and 40% in Europe, try to mirror that ratio in your liquid accounts. To test your resilience, consider a 20% depreciation scenario – if your largest currency holding drops by 20% and it causes financial stress, it might be time to rebalance.

Beyond the dollar and euro, you might explore holding reserves in the Swiss franc (CHF), known for its stability. Analysts predict the USD/CHF exchange rate could hit 0.76 by June 2026, underscoring the franc’s appeal as a safe-haven currency. For those seeking growth, currencies like the Australian dollar (AUD) and Norwegian krone (NOK) may offer exposure to recovering economies.

When natural strategies aren’t enough, hedging tools can provide additional protection.

Using Forex Hedging Tools

Hedging tools are designed to lock in exchange rates or protect against unfavorable movements. Forward contracts, for instance, guarantee a specific rate for a future date. These are especially useful for predictable obligations, like paying tuition or purchasing overseas property. While forward contracts require a deposit, they lock in rates regardless of whether the market moves in your favor.

For more flexibility, currency options allow you to exchange currency at a set "strike price" without the obligation to do so. If the market shifts in your favor, you can simply let the option expire. However, options come with an upfront premium, which means the exchange rate must move significantly in your favor to cover the cost.

For investors in international bonds, currency-hedged ETFs can help reduce risk. These funds use short-term forwards to shield returns from currency fluctuations. For example, between November 2024 and November 2025, a euro-based investor holding unhedged U.S. corporate bonds saw a -3.32% return due to dollar weakness. In contrast, a EUR-hedged version of the same investment delivered a +4% return. While hedged ETFs typically charge about 1% in management fees, they ensure that currency volatility doesn’t erode bond yields.

"Unhedged bonds can fail you when you need them most – amid market tumult when bonds are normally prized for their stability." – Amy C. Arnott, Portfolio Strategist, Morningstar

One thing to keep in mind is the cost of carry, which depends on interest rate differences between currencies. Hedging from a lower-yielding currency like the euro to a higher-yielding one like the dollar can reduce returns, but the stability gained often outweighs this cost. Historically, unhedged global bonds have been nearly three times as volatile as hedged ones.

Investing Offshore in Stable Currencies

If multi-currency accounts and hedging tools address immediate needs, offshore investments offer a broader layer of protection. Investing in stable jurisdictions like Switzerland or Singapore can help diversify currency risk. Swiss custodian accounts, for example, hold assets in segregated accounts, meaning your wealth is protected even if the bank encounters financial trouble. Thanks to advanced digital onboarding, you can now set up and manage these accounts remotely.

"Currency exposure is no longer a passive consequence of investing – it is an active strategic choice." – Alpen Partners International AG

With EUR/USD projected to reach 1.23 by June 2026, shifting part of your USD-denominated bond holdings into euro-denominated investment-grade bonds can reduce overexposure to the dollar while still offering yields above 3%. This approach is gaining traction, as assets in hedged European ETF share classes grew to $283.8 billion in 2025, compared to $56.8 billion in 2017.

The real strength lies in jurisdictional diversification – spreading assets across different legal systems can protect against domestic policy changes, fiscal pressures, and regulatory risks. As non-U.S. equities outperformed U.S. equities by 12.1% in the first half of 2025, international diversification isn’t just a defensive move anymore – it’s a key part of building a resilient financial plan.

Tracking and Adjusting Your Currency Strategy

After securing your assets, it’s essential to keep an eye on economic changes that could impact your wealth. Building on earlier protective measures, staying vigilant and refining your currency exposure is key to maintaining long-term stability. Currency markets are highly responsive to economic trends, policy updates, and global events. By monitoring the right signals, you can decide whether to stay the course or make adjustments.

Economic Indicators to Watch

Certain metrics act as crucial signals for currency movements: interest rate differences, inflation trends, fiscal health (like deficit and debt-to-GDP ratios), trade balances, and volatility indices such as the VIX.

For instance, the U.S. dollar index (DXY) dropped by 10% in the first half of 2025, marking its weakest first-half performance since at least 1980. During the 2008–09 Global Financial Crisis, the U.S. Treasury basis widened by 60 basis points, while the dollar strengthened by 14.3% against G10 currencies as investors sought safety. More recently, in October 2025, the British pound faced significant pressure due to concerns over the UK’s economic growth and fiscal outlook. These examples highlight how quickly market sentiment can shift in uncertain times.

"We look for more USD weakness this year, predicated on the same combination of cyclical and structural factors that we have been discussing for several months now." – Meera Chandan, Co-head of Global FX Strategy, J.P. Morgan

Keeping an eye on these indicators can provide the early signals needed to adjust your portfolio effectively.

When to Adjust Your Portfolio

Timing your adjustments isn’t about reacting to dramatic headlines. Instead, it’s about responding to changes in your personal circumstances. For example, if you’re planning to retire abroad, supporting family members overseas, or purchasing property internationally, your currency needs will shift, and your portfolio should reflect those changes. If a significant drop – say 20% – in your primary currency holding threatens your financial stability, it’s time to rebalance.

Policy changes are another key trigger. When central banks alter their strategies – like the Federal Reserve cutting rates while the European Central Bank tightens – it often signals a period of currency realignment. Early 2026, for instance, finds the U.S. dollar in a phase of cyclical weakness, with analysts predicting continued depreciation due to slowing growth and narrowing interest rate spreads.

Valuation extremes also offer opportunities. If a currency becomes significantly overvalued or undervalued compared to historical levels, rebalancing can help manage risks or seize potential gains. For example, G10 foreign investors currently hold around $14 trillion in unhedged dollar positions, which could lead to substantial selling pressure if the downward trend continues. To reduce dollar exposure, you might consider shifting from USD-denominated bonds to euro-denominated investment-grade bonds, which are currently yielding over 3%.

Working with Financial Advisors

Once you’ve adjusted your portfolio based on market signals, professional advice can help fine-tune your strategy. Currency management isn’t a one-and-done decision – it’s an ongoing process that benefits from expert guidance. Advisors can help align your portfolio’s currency mix with your expected future spending and financial obligations. They use structured frameworks to evaluate current needs, project long-term currency requirements (spanning 5–20 years), and even plan for legacy goals involving beneficiaries in different countries.

Advisors also navigate the complex U.S. tax and reporting requirements tied to offshore holdings, such as Passive Foreign Investment Company (PFIC) rules and Treasury Department filings, helping you avoid penalties. For qualified investors, they can employ advanced tools like currency forwards, options, and structured solutions – though these carry risks like leverage and margin calls.

"Before moving assets abroad, partner with professional advisors who are familiar with various financial, legal, and tax issues in order to execute a sound investment strategy." – Bernstein

Beyond technical expertise, advisors can test your portfolio’s resilience through scenario planning. They simulate potential currency depreciation scenarios to ensure your strategy holds up during volatile periods. This combination of quantitative analysis and emotional preparedness helps you stay balanced even when markets are unpredictable. By blending expert advice with ongoing market tracking, you can keep your currency strategy aligned with your long-term financial goals.

Conclusion: Managing Wealth in a Changing Currency Environment

Currency markets are always in motion, and your wealth strategy should be just as agile. With the dollar’s recent 10% decline and shifting global trends, it’s clear that active management beats staying passive. Diversifying your holdings – whether through multi-currency accounts, euro-denominated bonds offering yields above 3%, or strategic investments in currencies like the Australian dollar – can help reduce over-reliance on a single currency.

Hedging isn’t about predicting future currency movements; it’s about protecting what you already have. For example, fixed income investments often benefit from hedging. Historically, unhedged foreign bonds have seen losses exceeding 29%, while hedged versions limited drawdowns to just 11%. At the same time, international equities are often left unhedged to capture potential currency gains without incurring annual hedging costs, which can climb to 4%.

"Managing currency exposures is a dynamic, multi-step process blending quantitative analysis with qualitative judgment. A structured framework can potentially reduce risk, preserve purchasing power, and provide greater peace of mind." – UBS

This insight highlights the importance of regularly adjusting your strategy to keep pace with changing conditions.

Professional advice simplifies this complexity. Skilled advisors align your portfolio’s currency mix with your specific financial goals – whether that’s retiring abroad, supporting family overseas, or preparing for cross-border legacy plans. They also address U.S. tax considerations, utilize advanced hedging tools when necessary, and test your strategy against potential currency swings of up to 20%.

Success in this area isn’t about perfect timing. It’s about creating a flexible framework that evolves with your life and the global economy. Combining strategic diversification, targeted hedging, and expert guidance can help your portfolio withstand currency fluctuations and aim for long-term growth – no matter what happens with the dollar next quarter.

FAQs

Should I hedge my euro investments or leave them unhedged?

Hedging your euro investments is a decision that boils down to your comfort with risk and your view of future currency movements. By hedging, you can shield your portfolio from euro depreciation and reduce exposure to currency fluctuations, particularly in uncertain markets. On the other hand, leaving investments unhedged could offer diversification and potential upside if the euro strengthens. The right choice depends on how it fits into your broader financial strategy, your tolerance for risk, and your expectations for the euro’s performance in the years ahead.

How can I match my currencies to my future spending needs?

To keep your finances in sync with upcoming expenses, start by estimating what percentage of your spending will occur in each currency over the next five years. Think about where you live, how often you travel, or any international financial commitments you might have.

Once you’ve identified these factors, adjust your currency holdings to align with your expected liabilities. It’s also wise to diversify into more stable currencies as a safeguard against potential risks.

Make it a habit to review your currency allocations regularly. This ensures your strategy stays aligned with your financial goals and helps protect you from unexpected currency fluctuations.

What are the tax and reporting risks of offshore accounts for U.S. investors?

U.S. investors holding offshore accounts must navigate serious risks, including potential civil penalties or even criminal charges for failing to comply with U.S. tax laws. Key reporting requirements, such as the Foreign Bank Account Report (FBAR) and the Foreign Account Tax Compliance Act (FATCA), mandate the disclosure of foreign bank accounts and assets. Ignoring these obligations can lead to hefty fines, legal troubles, and other severe financial repercussions.