Global financial regulations are tightening, making compliance more complex for asset holders. Here’s what you need to know:

- CRS 2.0 (effective January 2026): Includes crypto-assets like digital currencies and mandates faster reporting deadlines.

- FATCA: U.S. persons with foreign accounts face dual reporting to the IRS, with severe penalties for noncompliance.

- AML Updates: New rules demand full disclosure of Ultimate Beneficial Owners (UBOs), targeting hidden ownership structures.

- Jurisdictional Differences: Countries like the Cook Islands, Samoa, and Switzerland balance asset protection with compliance, but each has unique legal frameworks.

- Technology & Compliance Tools: Automated systems are essential for meeting stricter reporting standards, especially for crypto-assets.

To safeguard wealth through offshore asset protection while staying compliant, focus on transparent structures, use modern compliance tools, and work with specialists to navigate these evolving standards. The regulatory landscape is shifting, and preparation is key to avoiding penalties and securing your assets.

Key Global Regulations That Impact Asset Strategies

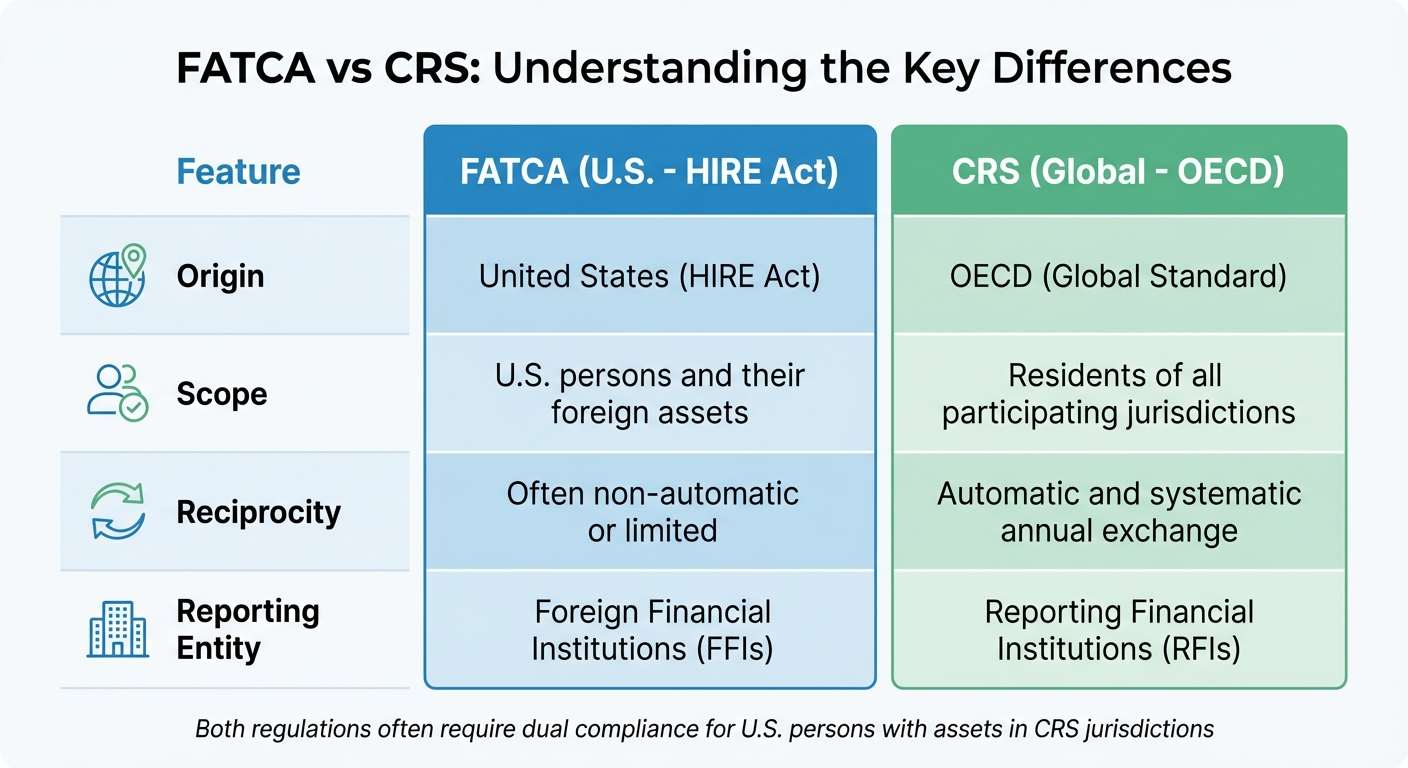

FATCA vs CRS: Key Differences in Global Financial Reporting Requirements

Three major regulatory frameworks now shape how offshore assets are reported and monitored worldwide. If you hold assets outside your home country, understanding these rules is crucial.

Common Reporting Standard (CRS) and Financial Transparency

The Common Reporting Standard (CRS), created by the OECD, has fundamentally changed how offshore assets are handled. Participating countries now require financial institutions to automatically share account information with tax authorities every year, rather than waiting for specific requests.

The shared data includes key details like the account holder’s name, address, Taxpayer Identification Number (TIN), account balance, and income (e.g., dividends and interest).

Starting January 1, 2026, the CRS will expand to include crypto-assets such as futures, forwards, options, central bank digital currencies, and certain electronic money products. Reporting deadlines are also tightening: new entities must register with tax authorities by January 31 instead of April 30, and annual returns are due by June 30 instead of July 31.

Financial institutions must collect self-certification details when accounts are opened, and errors can lead to audits. The Global Forum on Transparency and Exchange of Information for Tax Purposes highlights the importance of these measures:

"The AEOI Standard provides for the annual automatic exchange of information on Financial Accounts held by taxpayers outside their jurisdiction of tax residence… This helps ensure that tax evaders are at greater risk than ever of being caught".

Authorities are also targeting loopholes. Non-reporting financial institutions, like certain retirement schemes, are under scrutiny for bypassing CRS rules. To ensure compliance, the Global Forum is conducting onsite reviews to verify that jurisdictions are enforcing these regulations effectively.

These changes pave the way for other targeted regulations, such as FATCA.

Foreign Account Tax Compliance Act (FATCA)

FATCA is a U.S. law requiring foreign financial institutions to report U.S. account holders’ assets to the IRS. Noncompliance results in a hefty 30% withholding on U.S.-sourced payments.

Unlike CRS, which applies to multiple countries, FATCA focuses solely on U.S. persons – citizens, residents, and green card holders – regardless of their location. Foreign banks must identify these individuals and report account balances, income, and transactions. To avoid penalties, institutions need a Global Intermediary Identification Number (GIIN) and must enter agreements with the IRS.

For U.S. taxpayers, FATCA creates dual reporting requirements. You must file Form 8938 (Statement of Specified Foreign Financial Assets) if your foreign assets exceed specific thresholds, and submit the Foreign Bank Account Report (FBAR) if your combined foreign account balances surpass $10,000 at any point during the year.

| Feature | FATCA | CRS |

|---|---|---|

| Origin | United States (HIRE Act) | OECD (Global Standard) |

| Scope | U.S. persons and their foreign assets | Residents of all participating jurisdictions |

| Reciprocity | Often non-automatic or limited | Automatic and systematic annual exchange |

| Reporting Entity | Foreign Financial Institutions (FFIs) | Reporting Financial Institutions (RFIs) |

While FATCA and CRS share similar goals, they operate independently. This means financial institutions often need to comply with both, creating overlapping reporting obligations for individuals with U.S. ties and assets in CRS jurisdictions.

In addition to CRS and FATCA, updated AML rules are reshaping how offshore assets are managed.

Anti-Money Laundering (AML) and Beneficial Ownership Rules

AML regulations now demand greater transparency in identifying the true owners behind legal entities. Authorities focus on revealing the ultimate beneficiaries – those who genuinely control or profit from these entities – rather than relying on incorporation documents.

The Financial Action Task Force (FATF) updated its guidelines in March 2024 to improve transparency around legal arrangements like trusts. This effort aims to prevent individuals from hiding behind shell companies or complex structures, making traditional privacy mechanisms far less effective.

Intermediaries such as law firms, accountants, and tax advisors are also under the microscope. Mandatory Disclosure Rules (MDR) now require them to report schemes designed to bypass CRS reporting or obscure beneficial ownership. This means your advisors may be legally obligated to inform authorities about certain asset protection strategies. For personalized guidance on navigating these disclosures, consider private consultations with a specialist.

The results are clear: voluntary disclosure programs tied to these initiatives have recovered over EUR 130 billion globally in taxes, interest, and penalties.

By late 2024, 95% of the 114 jurisdictions assessed had legal frameworks for information exchange that were fully or substantially in place. The focus has shifted from creating laws to ensuring their practical enforcement, with onsite visits verifying compliance.

For asset holders, this means maintaining accurate, up-to-date records of beneficial ownership that can be provided immediately upon request. Static, annual reporting is no longer enough. The era of relying on complex structures for confidentiality is over – full transparency is now the standard for offshore asset management.

sbb-itb-39d39a6

How Different Jurisdictions Are Responding to Compliance Requirements

As global regulations evolve, jurisdictions are adapting their frameworks to balance the need for asset protection with stricter compliance standards. These adjustments vary widely – some focus on preserving robust asset protection, while others prioritize transparency to meet upcoming deadlines. For anyone managing offshore structures in 2026, understanding these differences is essential.

The regulatory environment is changing fast. For example, several jurisdictions are implementing CRS 2.0 amendments starting January 1, 2026. These updates broaden reporting requirements to include crypto-assets, electronic money, and central bank digital currencies. Additionally, many jurisdictions now mandate the appointment of a Principal Point of Contact (PPoC), who must be a local resident, to improve accountability. These global trends are shaping how individual jurisdictions respond.

The stakes for non-compliance are also rising. Some regions, like the Cayman Islands, have capped penalties – such as a CI$50,000 maximum for ongoing violations – but are issuing immediate fines for missed filings.

Let’s take a closer look at how specific jurisdictions are addressing these changes.

Anguilla, Samoa, Cook Islands, and Switzerland: A Comparison

Here’s a breakdown of how these jurisdictions handle asset protection and compliance:

Cook Islands is renowned for its strong asset protection, scoring 94/100. Its International Trusts Act of 1984 provides a shield against foreign judgments, requiring creditors to file lawsuits locally. The statute of limitations for challenging transfers is only 1–2 years, and creditors must meet a high burden of proof, demonstrating "actual fraud" to a "beyond a reasonable doubt" standard – about 90% certainty compared to the U.S. civil standard. However, trusts in the Cook Islands must still comply with FATCA and CRS requirements. For instance, U.S. persons with Cook Islands trusts must file FinCEN Form 114 (FBAR) if their foreign accounts exceed $10,000.

Samoa offers flexibility under its Samoa Trust Law 2014 and Samoa International Special Trust Arrangement (SISTA). These laws allow for complete foreign control and tax exemptions for non-residents. The jurisdiction is known for its quick setup process, making it attractive for estate planning. Like the Cook Islands, Samoa combines strong asset protection with adherence to global reporting standards.

Anguilla is an early adopter of CRS 2.0, enforcing stricter data quality and expanded crypto-asset reporting starting in 2026. The jurisdiction also requires a local PPoC by January 2027 to ensure compliance. Anguilla strikes a balance between offering offshore benefits and aligning with international regulatory expectations.

Switzerland, historically associated with banking privacy, now fully participates in CRS and complies with FATCA through bilateral agreements. U.S. investors should be cautious of Passive Foreign Investment Company (PFIC) rules, which could result in punitive taxation. While its asset protection measures are moderate, Switzerland’s political stability and advanced financial infrastructure make it appealing.

| Jurisdiction | Asset Protection Strength | Statute of Limitations | Creditor Burden of Proof | CRS 2.0 Compliance | Key Consideration |

|---|---|---|---|---|---|

| Cook Islands | Very High (94/100) | 1–2 years | Beyond reasonable doubt (~90%) | Full compliance required | Does not recognize foreign judgments |

| Samoa | High | Varies | High standard | Full compliance required | Rapid setup; complete foreign control |

| Anguilla | Moderate to High | Varies | Varies | Early adopter of CRS 2.0 | Local PPoC required by Jan 2027 |

| Switzerland | Moderate | Varies | Civil standard | Full compliance | PFIC concerns for U.S. investors |

Your choice of jurisdiction should align with your priorities. If maximum asset protection is key and you can meet U.S. reporting obligations, the Cook Islands or Samoa might be ideal. For those seeking a well-established financial system and full transparency, Switzerland is a solid option. Anguilla offers a middle path, combining offshore advantages with proactive regulatory measures.

Timing is crucial. Blake Harris, Founding Principal of Blake Harris Law, highlights this point:

The key to a successful asset protection strategy is to set everything up before any threat of litigation.

Setting up structures after legal threats arise can lead to accusations of fraudulent transfers, jeopardizing the entire strategy.

Asset Protection Strategies for 2026 and Beyond

As global regulations tighten, asset protection strategies need to evolve. The goal isn’t to abandon protection but to adapt by creating frameworks that comply with new rules while keeping wealth secure. With CRS 2.0 and CARF officially in effect as of January 1, 2026, successful strategies now blend transparency with robust safeguards.

To achieve this, it’s essential to use structures that fulfill both protection and reporting requirements. Some jurisdictions have updated their legal systems to strike this balance, offering options that provide creditor protection while meeting international compliance standards.

Using Offshore Trusts and Hybrid Structures

Offshore trusts remain a powerful way to protect assets – when structured properly. For instance, the Cook Islands boasts a 96% success rate in shielding trusts from creditors over the past 30 years. Nevis, on the other hand, requires creditors to post a $100,000 bond before filing claims, effectively discouraging frivolous lawsuits. For business owners, British Virgin Islands’ VISTA Trusts allow trustees to hold company shares without interfering in management decisions, while Cayman Islands’ STAR Trusts cater to more complex investment strategies without needing traditional beneficiaries.

Hybrid structures offer another layer of flexibility. By combining an offshore trust with a Nevis or Cook Islands LLC, you can retain operational control of your assets through the LLC while the trust provides additional protection in case of legal challenges. This approach balances day-to-day control with the trust’s legal safeguards.

However, avoid setups that give you too much control. U.S. courts are increasingly scrutinizing these arrangements, focusing on the substance rather than labels. If you maintain hidden control or reversionary interests, courts may deem the trust "illusory" and strip away its protections. As one U.S. Bankruptcy Court pointed out:

Belize is a popular trust jurisdiction precisely because it allows the types of fraudulent transfers that are unenforceable in America.

Here’s a quick comparison of trust and company structures under current regulations:

| Feature | Irrevocable Trust | International Company (IBC/LLC) |

|---|---|---|

| Primary Purpose | Long-term wealth preservation and succession | Active trading, investment, or business operations |

| Economic Substance | Exempt unless conducting "relevant activities" as a business | Subject to strict substance rules if performing relevant activities |

| Reporting Regime | CRS 2.0 (focus on beneficiaries/settlors) | CARF (if crypto-related) and CRS 2.0 |

| Asset Protection | High; firewalls against forced heirship and foreign judgments | Moderate; assets may be reached via "piercing the corporate veil" |

| Control | Managed by a third-party trustee; settlor intent is key | Managed by directors/managers; higher risk of being deemed "illusory" if settlor retains total control |

For U.S. individuals, remember that offshore trusts don’t exempt you from tax obligations. If foreign accounts exceed $10,000, you must file FinCEN Form 114 (FBAR), and all trust income must be reported on your tax return.

Compliance Tools and Technologies

Beyond choosing the right structures, modern compliance tools are crucial for navigating CRS 2.0, CARF, and updated AML requirements. The complexity of these regulations – covering traditional accounts, crypto-assets, e-money, and Central Bank Digital Currencies – demands more than manual tracking.

Automated compliance software has become indispensable. These systems help institutions and asset holders distinguish between "due diligence data" (for internal use) and "reportable data" (shared with tax authorities). Tools incorporating OECD XML Schema v4.0 can efficiently handle expanded data fields, ensuring accurate reporting without overdisclosure. This precision protects privacy while meeting regulatory demands.

For crypto-assets, specialized CARF tools can track on-chain transactions and identify reportable crypto-assets versus Specified Electronic Money Products (SEMPs). These platforms also run automated checks to verify self-certifications against AML/KYC data, catching issues early and reducing the risk of audits.

However, technology alone isn’t enough. As Stanley Foodman, CEO of Foodman CPAs & Advisors, puts it:

Reporting software is not a compliance strategy. Too many teams rely on tech solutions that don’t reconcile risk.

To ensure compliance, professional oversight is necessary. Advisors can review older structures to confirm they align with updated "economic substance" and "control" requirements. Proper placement of Principal Place of Control (PPoC) remains critical.

The UK government estimates adapting IT systems for new reporting agreements will cost £24.9 million between 2025 and 2032, with businesses facing one-time administrative costs of £107 million. While these figures focus on financial institutions, they highlight the scale of technological adjustments required.

Practical steps to improve compliance include upgrading onboarding systems, implementing real-time verification, and conducting a gap analysis to address mandatory fields before the 2027 reporting cycle.

Regulators are shifting from leniency to enforcement. Structural weaknesses are now seen as red flags, and data must be "adequate, accurate, and current" from the start. Strengthening compliance not only protects your assets but also ensures adherence to evolving standards.

Preparing Your Portfolio for Future Regulatory Changes

Global regulations are evolving at a rapid pace. For instance, the EU’s Anti-Money Laundering Regulation (AMLR) will take effect on July 10, 2027, and the FinCEN AML Rule for Investment Advisers will follow on January 1, 2028. These deadlines leave little room for last-minute compliance. The EU has already tightened its rules, lowering the threshold for identifying Ultimate Beneficial Owners (UBOs) to "25% or more" of shares or voting rights. Penalties for serious breaches have also doubled – from €5 million or 5% of turnover to €10 million or 10% of total annual turnover.

To stay ahead, focus on monitoring legislative developments rather than waiting for enforcement. Keep an eye on frameworks like the GENIUS Act and the CLARITY Act, which could reshape digital asset strategies before becoming law. Investors should also ensure they maintain accurate, up-to-date records for express trusts and similar arrangements to comply with FATF Recommendation 25 standards. Meanwhile, the IRS is intensifying scrutiny on foreign trusts, targeting "dual-resident" taxpayers and reclassifying certain foreign loans as gifts to prevent tax avoidance.

To avoid falling afoul of IRS anti-avoidance rules, any transfer labeled as a loan must be backed by a formal loan agreement, promissory note, and documented interest payments. For more intricate structures, verify individuals with 25% or more ownership early to align with the stricter EU AMLR definition. Additionally, update customer information every five years – or annually for high-risk cases – under the new EU guidelines.

While technology can streamline compliance processes, it cannot replace a well-thought-out strategy. Automated Customer Due Diligence (CDD) systems, for example, can be triggered at €3,000 for identity checks and €10,000 for in-depth reviews, aligning with EU thresholds. Looking ahead, prepare for the 2029 launch of the Bank Account Registers Interconnection System (BARIS), which will enable authorities to identify securities and crypto-asset account holders across the EU. As Christopher Woolard CBE, EY UK LLP Board Member, explains:

Success will depend on… maintaining keen awareness of the higher costs of doing business in certain jurisdictions as rules diverge.

While technology is a helpful tool, expert guidance remains vital for refining your strategy.

Working with Asset Protection Specialists

Shifting from reactive compliance to proactive planning can unlock opportunities while reducing risks. Asset protection specialists can guide you through three key phases of "regulation readiness": identifying and influencing upcoming changes, planning and prioritizing your response, and implementing compliant systems. With higher thresholds and penalties, their expertise is increasingly essential.

These specialists can secure no-action letters or staff guidance that allow previously restricted activities. For U.S. individuals with foreign holdings, they can also help navigate "dual-resident" status, which may exempt some taxpayers from international reporting under certain treaty provisions (e.g., Forms 3520/3520-A). Additionally, they bring technical expertise to balance privacy and transparency, using advanced techniques like zero-knowledge proofs (ZKP) and multi-party computation (MPC) to meet compliance requirements without compromising proprietary strategies.

Recent developments highlight the importance of staying ahead. In 2025, the SEC withdrew 17 rule proposals, and the Deloitte Center for Financial Services regulatory index hit its lowest point in nearly 15 years, signaling a slowdown in new regulations. However, as Deloitte cautions:

A more permissive SEC does not equate to a regulation-free environment, and investment managers with positive regulatory relationships and innovative leadership should be well positioned to better capitalize on new market opportunities.

Specialists from firms like Global Wealth Protection can audit compliance platforms, assess risks, and establish policies that meet regulator expectations. This is particularly critical for those entering the digital asset space, especially after the removal of restrictive accounting rules like SAB 121. As Rita M. Ryan, CFO and Head of Planning at Madan+Associates, advises:

Practitioners should continue to monitor these regs for updates and changes as they progress to finalization, as well as continue to ask and educate clients about their foreign holdings.

Conclusion

Global regulatory shifts are reshaping the financial landscape. Tax authorities across 111 jurisdictions now share data on over 134 million financial accounts, covering nearly €12 trillion in assets. The days of relying on traditional offshore privacy are over. In this new era, staying compliant is the key to safeguarding wealth without drawing unwanted attention.

Compliance isn’t just about avoiding penalties – it can be a strategic tool. For example, during periods of reduced regulatory activity, like the record low in the Deloitte regulatory index projected for 2025, firms have an opportunity to strengthen their compliance systems before the next wave of changes arrives. With anti-money laundering (AML) frameworks evolving and transparency standards tightening, the window to prepare is shrinking.

Regulations are increasingly focused on localization, digital tools, and stricter oversight. Systems like the Bank Account Registers Interconnection System (BARIS) are being introduced to help EU authorities track securities and crypto-asset accounts across borders. Elsewhere, jurisdictions like the Cayman Islands are accelerating compliance deadlines – shifting their CRS reporting from July 31 to June 30 – and imposing fines of $5,000 to $10,000 for missed filings. These developments highlight the urgency of adapting compliance strategies to meet these rising benchmarks.

As this guide has shown, managing offshore trusts, digital assets, and traditional portfolios requires alignment with today’s regulatory demands. As KPMG emphasizes:

Resilience is not just a compliance issue, but a source of competitive advantage.

The firms that succeed in the coming years won’t wait until regulations are enforced. Instead, they’ll anticipate changes, assess third-party risks, and integrate compliance into their operations from the start. The real question isn’t whether these shifts will affect your strategy – it’s whether you’ll act quickly enough to protect your wealth and stay ahead of the curve.

FAQs

Will CRS 2.0 report my crypto holdings?

CRS 2.0 could require reporting of your crypto holdings. The updated Common Reporting Standard broadens its reach to include digital currencies and crypto assets. This move aligns with international efforts to improve tax transparency and ensure compliance with evolving regulations.

Do I need both FATCA and FBAR filings?

Yes, U.S. persons typically need to file both FATCA Form 8938 and FBAR FinCEN Form 114 if their foreign assets surpass the respective thresholds.

- FATCA Form 8938 applies to foreign assets exceeding $50,000.

- FBAR is required for foreign financial accounts totaling more than $10,000 at any time during the year.

Each form serves a different purpose and comes with its own reporting requirements.

How do UBO rules affect my trust or LLC?

UBO (Ultimate Beneficial Owner) rules aim to improve transparency by requiring trusts and LLCs to reveal details about ownership and control. For example, under regulations like the Corporate Transparency Act, entities must report personal information about beneficial owners, such as their name, address, and date of birth.

These rules have a notable effect on estate planning. Any changes in ownership could trigger reporting requirements, which reduces privacy and increases oversight. Compliance with these regulations is critical – not just to avoid penalties, but also to navigate the delicate balance between legal obligations and privacy concerns.