Protecting your wealth as a digital entrepreneur means safeguarding your assets from lawsuits, economic instability, and legal challenges across multiple jurisdictions. Here’s the essential takeaway:

- Asset Protection: Offshore trusts and LLCs in places like the Anguilla can shield your assets from domestic legal claims.

- Geographic Diversification: Spreading assets across countries reduces risks tied to political or economic crises.

- Tax Optimization: Operating in tax-friendly jurisdictions like Wyoming, Delaware, New Mexico or Dubai can lower your tax burden while staying compliant.

- International Banking: Secure offshore accounts in stable regions, such as Singapore or the Cayman Islands, to strengthen financial security.

- Compliance: Follow U.S. reporting laws like FBAR and FATCA to avoid penalties.

The key is to create a layered, legal strategy tailored to your global operations. Timing is critical – set up these structures before any legal issues arise to ensure maximum protection.

Legal Structures for Asset Protection

When it comes to safeguarding assets globally, digital entrepreneurs have several legal structures at their disposal. These structures are designed to provide tailored protections while accommodating the unique needs of online businesses.

Offshore Companies and Their Benefits

Offshore companies operate under foreign jurisdictions, offering a shield for your assets that domestic courts often struggle to penetrate. For instance, some jurisdictions like Nevis require creditors to post a bond before filing claims, adding an extra layer of deterrence.

Places like Anguilla and Nevis also prioritize privacy, as they don’t maintain public records of LLC owners. This makes them an attractive choice for entrepreneurs managing international clients, holding intellectual property, or running remote teams. These companies allow for smoother operations without the red tape often found in domestic systems.

The costs are fairly transparent. Setting up an offshore company typically costs between $1,000 and $5,000, with annual maintenance fees ranging from $500 to $2,000. For example, pairing an Anguilla LLC with a Belize bank account could cost around $3,350 in the first year. However, timing is critical – creating these structures before any legal claims arise is crucial, as post-claim transfers may be considered fraudulent. With approximately 5 million new lawsuits filed in the United States in 2023 alone, proactive planning is more important than ever.

For those seeking additional layers of protection, offshore trusts and foundations are worth considering.

Offshore Trusts and Private Interest Foundations

Offshore trusts and private interest foundations serve as complementary tools for wealth protection, each offering distinct advantages.

In common law jurisdictions like the Anguilla, Nevis, or Belize, a trust delegates asset management to a trustee who acts on behalf of the beneficiaries. Foundations, on the other hand, are separate legal entities originating from Civil Law jurisdictions such as Anguilla and Liechtenstein. While trusts are generally more flexible for business activities, foundations are better suited for non-commercial purposes unless paired with an offshore company.

Privacy is another major factor. Trust deeds remain private, as they don’t require government registration. In contrast, foundation charters are public, though the identities of beneficiaries are usually kept confidential. For example, in Anguilla, creditors have only two years from the settlement of a trust to challenge it for fraudulent conveyance. Additionally, jurisdictions like the Anguilla do not recognize foreign court orders, forcing creditors to start legal proceedings locally under stricter standards.

One popular strategy for digital entrepreneurs is the "Trust + LLC" setup, where the trust owns the LLC but you retain operational control. This arrangement shields assets from legal threats while maintaining day-to-day functionality. Foundations, being incorporated entities, are less likely to be dismissed as "shams", a risk sometimes associated with trusts if the grantor retains excessive control. Plus, foundations are often more easily recognized by tax authorities in Civil Law countries.

Using Multiple Structures Together

Combining different legal structures creates a robust, multi-layered defense against potential claims.

For instance, an offshore trust owning an LLC means creditors must go after a foreign-managed entity rather than targeting you directly. Entrepreneurs often use one LLC for active business operations and another, held under a trust, to protect long-term assets. Assets can also be distributed across multiple jurisdictions – such as an LLC in Nevis, a trust in Anguilla, and bank accounts in a third location – making it significantly harder for creditors to pursue claims.

This complexity acts as a powerful deterrent. While no single structure offers complete immunity, layering multiple entities and legal systems increases the cost and difficulty of enforcement, often leading to more favorable settlements. For example, adding a trust to an LLC not only enhances confidentiality but also makes it harder to trace assets through public records.

It’s crucial to maintain a clear separation between ownership and control. Structures where you retain too much control are more likely to fail under legal scrutiny. Compliance with regulations like FBAR, FATCA, and IRS Form 8938 is also essential to ensure the legitimacy of these setups. As attorney Jon Alper explains:

Offshore trusts often own offshore LLCs, which in turn hold operating businesses or investment portfolios. This layering means creditors aren’t just pursuing an individual’s asset – they’re pursuing an entity owned by a foreign trustee, dramatically increasing enforcement difficulty and cost.

These strategies are generally most effective for individuals with at least $1,000,000 in liquid assets. Below this threshold, the costs of setup and maintenance may outweigh the benefits.

sbb-itb-39d39a6

International Banking Solutions

When you’ve set up the proper legal structures, the next logical step is choosing secure international banking solutions to strengthen your asset protection strategy. Offshore banking plays a key role here, helping diversify counterparty risk and adding layers of legal protection against creditors.

How to Select Offshore Bank Accounts

Picking the right offshore bank involves more than just considering privacy. Several critical factors come into play.

Start by assessing the strength of the jurisdiction. Look for locations where banks and regulatory bodies enforce strong privacy and asset protection measures. For example, Singapore is an excellent choice, boasting a AAA credit rating and oversight from the Monetary Authority of Singapore. Similarly, the Cayman Islands and Jersey are popular for their advanced financial systems – Jersey alone manages over £500 billion in trust assets.

Choose banks with solid regulatory oversight and proven financial stability to reduce counterparty risk. As one advisor with extensive experience notes:

In my 15+ years advising clients on asset protection, the most durable plans combine domestic protection (insurance, estate planning, entity structure) with limited, carefully documented offshore elements only after full legal and tax review. – Author Note, finhelp.io

Currency exposure is another factor to watch. Settlement differences can affect liquidity and planning. The Singapore Dollar offers stability, and Hong Kong’s common law framework makes it a central hub for accessing Asian markets.

Cost is also worth considering. Jurisdictions like Seychelles and Belize offer lower formation and maintenance costs – about 30% to 60% less than premium centers like the Cook Islands or Cayman Islands – while still providing comparable protections. However, it’s worth noting that some banks in places like Switzerland and Singapore have raised account minimums or stopped accepting U.S. clients altogether due to FATCA compliance costs.

For U.S. citizens, compliance is crucial. Any foreign account exceeding $10,000 requires filing FinCEN Form 114 (FBAR). A thorough legal review across jurisdictions is essential before funding an account to ensure compliance with both domestic and offshore regulations.

Once you’ve secured the right bank account, the next step is to distribute your assets geographically for added security.

Spreading Assets Across Multiple Countries

A well-rounded asset protection plan doesn’t just rely on legal and banking frameworks – it also involves spreading assets across stable international markets. Dispersing assets in multiple countries creates a more resilient financial position than concentrating everything in one place. For instance, you could establish a Anguilla trust to own a Nevis LLC while keeping bank accounts in Singapore or the Cayman Islands. This multi-layered approach forces creditors to navigate several legal systems, each with its own complexities and standards.

It’s also wise to maintain domestic liquidity. Keeping some liquid funds in your home country ensures you can cover operating costs or legal expenses if access to offshore funds is delayed. This isn’t about doubting your offshore setup – it’s simply smart risk management.

When choosing where to diversify, prioritize countries with political and economic stability. Switzerland is a prime example, known for its neutrality, while Singapore offers a business-friendly environment. Opt for jurisdictions with high evidentiary standards, as these make it harder for creditors to gain access. However, keep in mind that some well-known "asset protection havens" might carry negative perceptions. Lesser-known jurisdictions like Saint Vincent and the Grenadines can provide similar protections with less stigma.

Currency diversification is another advantage of spreading assets internationally. Stable currencies like the Singapore Dollar and Swiss Franc help reduce exposure to economic fluctuations in any one region.

Jacob Stein, Partner at Aliant Law, highlights the importance of working with the right professionals:

Knowing the right trust company or the right investment manager can elevate an already great asset protection structure to an even higher level.

Finally, it’s important to note that offshore banking isn’t about secrecy or tax evasion. Modern asset protection relies on legal frameworks designed to challenge creditor access. With regulations like the Common Reporting Standard making financial secrecy nearly impossible, your focus should be on building strong legal barriers rather than relying on opacity.

Tax Optimization Strategies

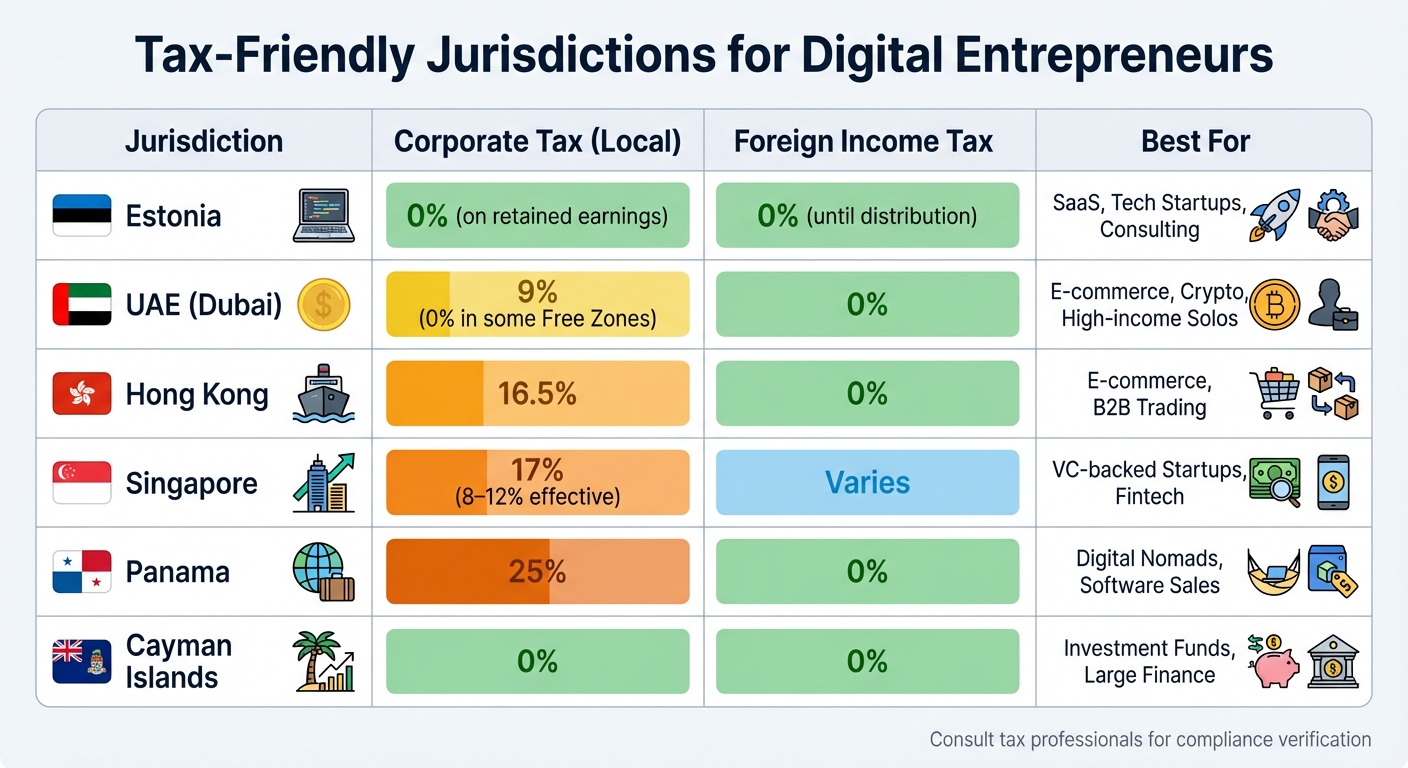

Top Tax-Friendly Jurisdictions for Digital Entrepreneurs Comparison

Once your banking and asset distribution are in place, the next step in reducing your tax burden is to operate within jurisdictions that offer favorable tax laws. This approach is a key part of a broader global wealth protection strategy. Tax optimization involves structuring your business operations in a way that aligns with both your financial goals and lifestyle, all while staying within legal boundaries.

Operating in Tax-Friendly Jurisdictions

Digital entrepreneurs have the unique flexibility to establish their operations in countries with tax systems that work to their advantage. For instance, Estonia is a standout choice for SaaS and consulting businesses, thanks to its 0% corporate tax on retained and reinvested profits. Tax is only applied at a rate of 20% when dividends are distributed. Estonia’s e-Residency program also makes it possible to incorporate and manage a company entirely online using digital signatures.

For high-income solo entrepreneurs, Dubai in the UAE offers a 0% personal tax rate and a 9% corporate tax rate, with some Free Zones providing even greater exemptions. However, while Dubai’s tax benefits are attractive, setting up a bank account often requires an in-person visit, unlike Estonia’s fully remote system.

Other attractive jurisdictions include:

- Hong Kong: Operates on a territorial tax system, taxing local income at 16.5% while exempting foreign-sourced income. This makes it an ideal hub for B2B trading and accessing markets in the Far East.

- Panama: Its strictly territorial tax system means a 0% tax on income earned outside the country, making it appealing for digital nomads and software consultants.

- Singapore: Though its corporate tax rate is 17%, various incentives can bring the effective rate down to 8–12%, making it especially appealing for startups and fintech ventures.

Here’s a quick comparison of top jurisdictions:

| Jurisdiction | Corporate Tax (Local) | Foreign Income Tax | Best For |

|---|---|---|---|

| Estonia | 0% (on retained earnings) | 0% (until distribution) | SaaS, Tech Startups, Consulting |

| UAE (Dubai) | 9% (0% in some Free Zones) | 0% | E-commerce, Crypto, High-income Solos |

| Hong Kong | 16.5% | 0% | E-commerce, B2B Trading |

| Singapore | 17% (8–12% effective) | Varies | VC-backed Startups, Fintech |

| Panama | 25% | 0% | Digital Nomads, Software Sales |

| Cayman Islands | 0% | 0% | Investment Funds, Large Finance |

Before committing to any jurisdiction, it’s crucial to verify residency requirements. For example, while Dubai Free Zones offer excellent tax incentives, physical visits may be necessary for banking. In contrast, Estonia allows for complete remote management. Always consult with tax professionals familiar with both your home country’s regulations and the rules of your chosen jurisdiction to ensure compliance.

While corporate tax strategies are essential, don’t overlook the importance of optimizing your personal tax status.

Residency and Citizenship Planning

Your personal residency can play a significant role in minimizing tax obligations. Establishing tax residency in a favorable jurisdiction requires detailed planning and proper documentation. Tax residency determines which country has the primary right to tax your worldwide income and is separate from legal residency, which is simply your permission to live in a country.

Most countries apply the 183-day rule, meaning spending more than 183 days in a country typically makes you a tax resident there. Authorities may also consider factors like where your family resides, where you own property, and where your economic ties are strongest. Countries like Panama, Costa Rica, Hong Kong, and Singapore use territorial tax systems, taxing only income earned within their borders.

U.S. citizens face unique challenges due to the United States’ citizenship-based taxation system. This means U.S. citizens are taxed on their worldwide income, regardless of where they live. However, the Foreign Earned Income Exclusion (FEIE) allows qualifying citizens working abroad to exclude up to $126,500 of foreign-earned income in 2024. Beyond this threshold, U.S. taxes may still apply unless one renounces citizenship – a decision with serious legal and financial implications.

"The world’s most successful wealth strategists understand that it’s not about how much you make – it’s about how much you keep."

– Project Black Ledger

Leaving your home country’s tax system isn’t as simple as relocating – it requires formally establishing non-residency. Some countries demand deregistration from civil records, while the UK uses a Statutory Residence Test to determine overseas status. Timing your departure with the start of your home country’s tax year (such as April 6 in the UK) can help streamline the process.

To demonstrate a genuine change of residence, keep thorough records of travel, housing contracts, and utility bills in your new jurisdiction. Tax authorities are increasingly scrutinizing claims of non-residency, so establishing a clear "receiving country" for tax purposes is essential.

Be aware of potential exit taxes on unrealized capital gains when ceasing residency. For example, non-domiciled residents in the UK may face annual charges of £30,000 or £60,000 (after seven years of residence) if they wish to exclude foreign income from taxation.

"Going offshore isn’t about hiding – it’s about building a smarter system in a more favorable legal environment."

– OCBF Consulting

Modern tax strategies require transparency and compliance, focusing on creating legitimate structures that minimize tax burdens while adhering to legal standards.

Compliance and Implementation

When implementing offshore structures, it’s essential to approach the process methodically, ensuring each step aligns with the legal frameworks and strategies discussed earlier.

Steps to Start Your Asset Protection Plan

Start by identifying your goals. Are you aiming for tax efficiency, safeguarding assets from lawsuits, or diversifying investments? Your objectives will guide the choice of jurisdiction and structure. For instance, if protecting cryptocurrency holdings from creditors is your priority, a Nevis LLC could be a strong option. On the other hand, a Cook Islands trust might be better suited if you have over $1,000,000 in liquid assets and need robust protection.

"Bank first, company second." – Steven James, Offshore Structures Researcher

Before setting up any entity, confirm that you can open a bank account in the chosen jurisdiction for your specific needs. Many individuals waste resources on structures that banks later reject.

Next, assemble a team of professionals. Consult a tax advisor well-versed in both U.S. and international tax laws, an asset protection attorney familiar with offshore jurisdictions, and, if necessary, a trustee. These experts will help ensure your plan adheres to regulations and achieves the desired level of protection.

Expect the implementation process to take 3–7 weeks: 1–3 weeks for consultations and planning, another 1–3 weeks to draft documents (like trust deeds or LLC agreements), and 1–2 weeks to finalize paperwork and transfer assets. Be prepared to provide Know Your Customer (KYC) documentation and pass Anti-Money Laundering (AML) checks during the setup phase.

Timing is key. Implement your strategy during "peacetime" to avoid accusations of fraudulent conveyance. Once your plan is in place, ensure it complies with all international legal standards.

Meeting International Legal Requirements

Once your offshore structure is established, strict adherence to U.S. and international reporting requirements is non-negotiable. U.S. citizens are taxed on their worldwide income, regardless of where they live or hold assets.

"Offshore asset protection is not a tax strategy. It requires full compliance with all U.S. tax and reporting obligations." – Jon Alper, Asset Protection Attorney

For foreign accounts exceeding $10,000 in total value at any point during the year, file FinCEN Form 114 (FBAR) by April 15 (with an automatic extension to October 15). You may also need to file IRS Form 8938 (Statement of Specified Foreign Financial Assets) with your tax return if you meet the thresholds.

If you create a foreign trust, additional forms are required: IRS Form 3520 for trust transactions and Form 3520-A for annual reporting. Failing to file these forms can lead to severe penalties or even criminal charges.

Keep detailed records for at least five years from the FBAR due date. Include information like account names, numbers, bank details, account types, and the highest value reached during the year. These records are crucial during audits, especially as tax authorities intensify their scrutiny of offshore structures.

With many jurisdictions participating in automatic information exchange under the OECD Common Reporting Standard (CRS) and maintaining beneficial ownership registries, financial privacy has diminished. The focus now is on optimizing taxes legally within transparent systems. Your offshore structure should reflect this shift, ensuring compliance while achieving your financial goals.

Lastly, document the legitimate purpose behind every asset transfer. Courts can reverse transfers deemed to "hinder, delay, or defraud creditors" under fraudulent-transfer laws. Clearly outline your business rationale – whether it’s diversifying banking relationships, entering international markets, or safeguarding intellectual property – to strengthen your position against potential legal challenges.

Conclusion: Protecting Your Wealth Internationally

For digital entrepreneurs, safeguarding wealth requires a mix of domestic protections and carefully chosen international strategies. Combining these approaches – like offshore trusts, international LLCs, and diversified banking – can offer a more secure financial foundation. Start by establishing strong protections at home, then layer in offshore elements thoughtfully.

"The most durable plans combine domestic protection (insurance, estate planning, entity structure) with limited, carefully documented offshore elements only after full legal and tax review." – Author, finhelp.io

Transparency and compliance are non-negotiable. With regulations like the OECD Common Reporting Standard and FATCA enabling automatic information exchange across borders, offshore strategies must align with legal requirements. For U.S. citizens, worldwide taxation rules mean meticulous record-keeping is essential. Filing forms like FBAR and Form 8938 on time can help avoid hefty penalties.

Timing matters. Implement your strategy well before any legal issues arise – courts can reverse asset transfers if they appear designed to block creditors. Ensure every move serves a clear, legitimate purpose, whether it’s entering new markets, diversifying banking, or safeguarding intellectual property. At the same time, keep enough liquidity in the U.S. to cover expenses or legal costs.

To execute this effectively, build a team of professionals familiar with both domestic and international regulations. They can help you meet reporting obligations, select reputable institutions, and ensure compliance. A well-structured, transparent plan offers the security and flexibility digital entrepreneurs need to succeed on a global scale.

FAQs

Do offshore trusts and LLCs protect my crypto and IP?

Yes, offshore trusts and LLCs can play a key role in protecting your cryptocurrency and intellectual property. By transferring ownership to jurisdictions with strong asset protection laws, these structures place your assets beyond the reach of local courts. Essentially, they create a legal shield, making it significantly harder for creditors or other parties to access your digital assets. This setup provides an added layer of security against potential legal or financial risks.

How do I stay FBAR/FATCA compliant with offshore accounts?

U.S. persons need to stay on top of their reporting obligations to remain compliant with FBAR and FATCA regulations. If the total value of foreign financial accounts exceeds $10,000, they must file the FBAR (FinCEN Form 114). Additionally, foreign assets worth more than $200,000 must be reported using IRS Form 8938. These filings are essential for maintaining transparency and adhering to U.S. financial regulations.

What’s the simplest trust + LLC setup for U.S. entrepreneurs?

When setting up a straightforward business structure, many choose to establish a U.S.-based LLC in states like Wyoming or Delaware. These states are popular for their focus on privacy and relatively low fees. To enhance asset protection and streamline estate planning, this LLC can be paired with a domestic or offshore trust. Just make sure the entire structure adheres to U.S. legal requirements to ensure smooth operations and protection.