High-income professionals like physicians, attorneys, and real estate developers face significant financial risks, including lawsuits, malpractice claims, and market volatility. Offshore asset protection offers a way to shield wealth legally and transparently.

Here’s how it works:

- Offshore Trusts: Assets are transferred to foreign jurisdictions like the Cook Islands or Nevis, where U.S. court judgments are not enforced. These trusts are managed by independent trustees outside U.S. jurisdiction.

- Offshore LLCs: Used to limit liability and protect personal wealth by isolating assets from lawsuits or claims.

- International Banking: Diversifies asset locations and integrates with trusts or LLCs for added protection.

Key considerations:

- Compliance: Full disclosure to the IRS is mandatory through FBAR and IRS Form 8938.

- Timing: Assets must be moved before legal disputes arise to avoid fraudulent transfer claims.

- Costs: Setting up a Cook Islands trust costs $20,000–$25,000, with annual fees of $5,000–$8,000. Nevis and Belize offer more affordable options.

Offshore strategies focus on creating legal barriers rather than secrecy, making it harder and costlier for creditors to access assets. These tools provide a proactive way to safeguard wealth while staying compliant with U.S. laws.

Why These Professions Face High Financial Risks

Grasping the financial challenges faced by certain professions sheds light on the importance of offshore asset protection strategies. Physicians, attorneys, and real estate developers often work in what’s referred to as a "litigation hotspot." With over 1.2 million attorneys practicing in the United States, these professionals frequently become targets due to their significant wealth.

Defending a lawsuit in the U.S. can be incredibly costly – ranging from $100,000 to $150,000 in legal fees – even if the case is resolved in their favor. This is largely because the U.S. does not follow a "loser pays" rule. The financial risks, however, vary depending on the profession, with physicians, attorneys, and real estate developers each facing unique challenges.

Medical Malpractice Risks for Physicians

Physicians are particularly vulnerable to malpractice claims throughout their careers. For instance, in California alone, medical malpractice payouts surpassed $260 million in a single year.

One of the biggest threats comes from excess judgments – when verdicts exceed the limits of insurance policies – potentially putting personal assets at risk. As Mikkel Thorup, Founder and CEO of Expat Money, explains, "Medical malpractice litigation is commonplace (and lucrative) and should not be underestimated". Adding to this is the unpredictability of U.S. court rulings, which means a physician’s career and achievements can be scrutinized regardless of the claim’s merit.

Professional Liability Risks for Attorneys

Attorneys face their own set of challenges, including malpractice claims, ethical complaints, and disputes with clients. Professional negligence claims can lead to personal liability, and the intricate agreements common in legal practice often surpass the protection offered by domestic LLCs or state-based trusts.

Litigation and Market Risks for Real Estate Developers

Real estate developers encounter a broader range of risks compared to attorneys. In California alone, during the 2023–2024 period, over 6,500 premises-liability lawsuits were filed. Developers frequently deal with contract disputes, construction defect claims, and on-site injury lawsuits – any of which can threaten their entire portfolio.

A particularly troubling risk for developers is tied to personally guaranteed business loans. These guarantees effectively strip away the corporate veil, exposing personal assets to business liabilities. When combined with market fluctuations and construction challenges, this creates a precarious financial situation where personal wealth is increasingly at stake.

sbb-itb-39d39a6

Offshore Asset Protection Tools

Offshore asset protection strategies often combine trusts, LLCs, and international banking to shield assets effectively. These tools cater to different types of risks, offering tailored solutions for high-net-worth individuals seeking to safeguard their wealth.

Offshore Trusts

Offshore trusts are a powerful tool for mitigating litigation risks, acting as a legal shield between your assets and U.S. court judgments. These trusts place control in the hands of a trustee operating outside U.S. jurisdiction, making them immune to U.S. court orders. Popular jurisdictions like the Cook Islands and Nevis are known for their strong legal frameworks that render U.S. judgments unenforceable.

The protections offered by these trusts are formidable. For instance, creditors face steep hurdles, such as proving fraud with substantial evidence and often needing to meet additional financial requirements. In Nevis, a creditor must post a $100,000 cash bond before filing a lawsuit. Meanwhile, the Cook Islands boasts a 40-year history during which no properly structured and funded trust has been successfully breached by U.S. creditors.

"The trustee of the trust is outside the jurisdiction of the U.S. Court system and can’t be ordered to pay a judgment from a ‘foreign’ U.S. court."

– Ike Devji, JD

Setting up a Cook Islands trust typically costs between $20,000 and $25,000, with annual maintenance fees ranging from $5,000 to $8,000. Nevis trusts are generally more affordable, while Belize offers the most cost-effective options. Additionally, the Cook Islands enforces a short statute of limitations – just 1 to 2 years – after which assets are protected from fraudulent transfer claims.

Offshore LLCs and Company Structures

Offshore LLCs are ideal for isolating operational liabilities. For example, if someone files a claim due to an accident at a rental property owned by an offshore LLC, the claim is limited to the LLC’s assets, leaving personal wealth untouched.

Jurisdictions like Anguilla, Nevis, and Belize have strong LLC laws. In Nevis, for example, creditors are limited to obtaining a charging order against an LLC interest. This order expires after three years and cannot be renewed. Such protections often surpass those of domestic LLCs.

A common strategy involves combining an offshore LLC with a Bridge Trust. This approach balances operational ease with robust asset protection that U.S. courts cannot override. In these setups, the LLC handles daily transactions, while the trust acts as the ultimate safeguard, shielding assets from professional liabilities and market volatility.

International Banking Options

International banking provides financial privacy and diversifies asset locations, though it is the weakest standalone form of protection. If funds are held in a foreign account under your name, U.S. courts can still order their repatriation.

To enhance security, avoid banks with U.S. branches, such as UBS or Credit Suisse, as they fall under U.S. jurisdiction. Instead, work with banks operating solely outside the U.S. and integrate these accounts into a trust or LLC structure to add a legal layer of protection.

Modern regulations require global data sharing between financial institutions and the IRS. Asset protection today focuses on creating legal barriers rather than concealing assets. Compliance with U.S. reporting laws is critical, including filing FBAR and IRS Form 8938 for all offshore accounts.

How to Set Up Offshore Asset Protection

Setting up offshore asset protection involves choosing the right jurisdiction and transferring assets well before any legal disputes arise.

Moving Assets into Offshore Structures

To safeguard assets, transferring them into offshore trusts or LLCs must follow strict legal guidelines. If done improperly or after legal claims have surfaced, courts may reverse these transfers as fraudulent. Timing is everything – assets should be moved before any lawsuits or potential litigation emerge.

The process starts with changing legal ownership. For cash and securities, this involves transferring titles to a foreign trustee operating outside the U.S. jurisdiction. Real estate, however, is trickier. U.S. courts apply the laws of the state where the property is located. For example, in United States v. Huckaby (2026), defendants used a Nevada trust to protect property in California, but the court invalidated the trust’s provisions because California law applied.

To avoid such pitfalls, professionals often transfer the membership interest of an LLC holding the property to an offshore trust instead of transferring the property itself. This strategy creates a legal barrier while ensuring the owner remains solvent and meets financial obligations.

IRS compliance is non-negotiable. Offshore trusts and accounts must be reported, and U.S. taxes on any income generated must be paid. Regulations like FATCA and CRS require global banks to report holdings to the IRS, so transparency is essential.

Once assets are securely transferred, the next step is selecting a jurisdiction that offers the strongest legal protections.

Selecting the Right Jurisdiction

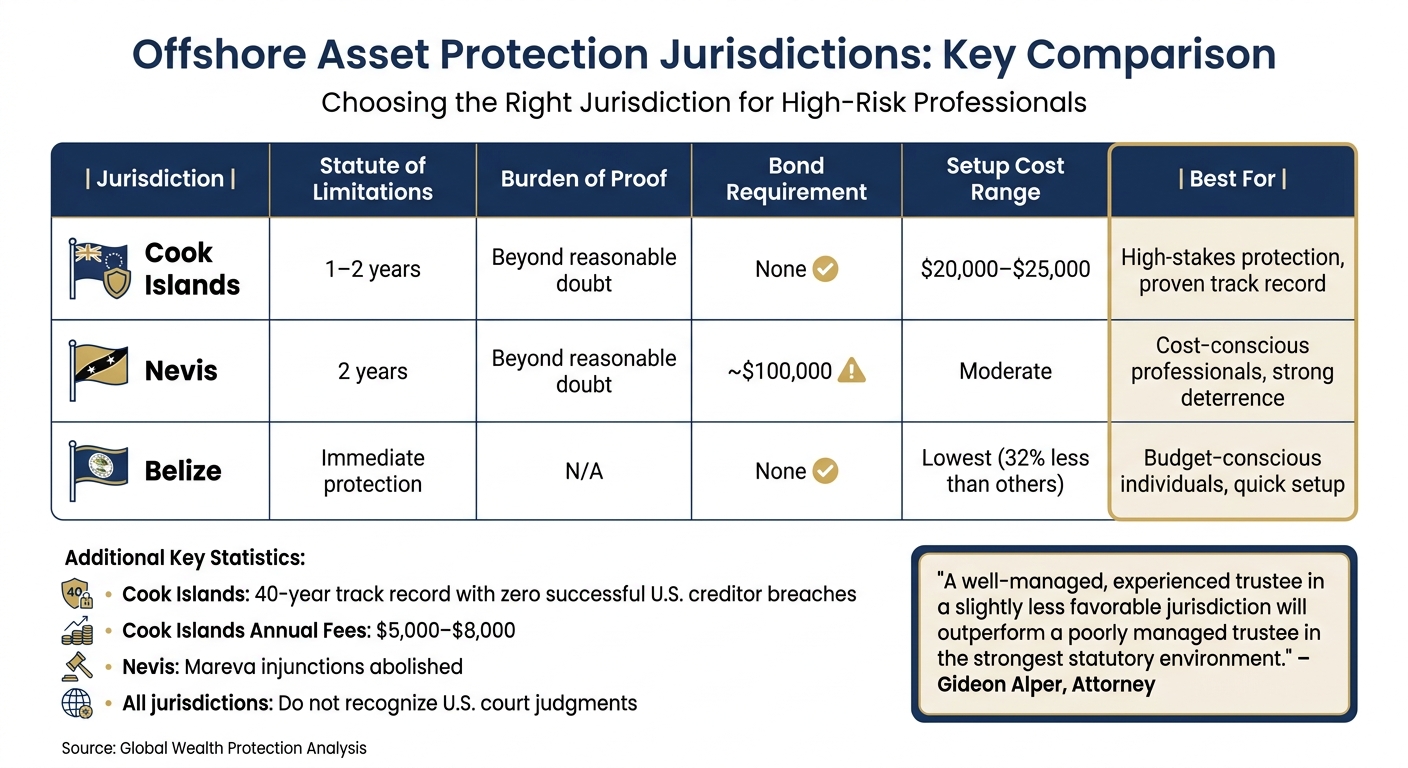

After transferring assets, choosing the right jurisdiction is key to ensuring protection. The best jurisdictions share three traits: they don’t recognize foreign judgments, impose a high burden of proof on creditors, and have short statutes of limitations for fraudulent transfer claims.

The Cook Islands is a standout choice, with a 40-year record of no U.S. creditor successfully penetrating a properly structured trust. The setup costs range from $20,000 to $25,000, with annual fees between $5,000 and $8,000. Creditors face a 1–2 year statute of limitations and must prove intent to defraud at a criminal-level standard of "beyond a reasonable doubt".

Nevis offers strong deterrents at moderate costs. Creditors must post a $100,000 cash bond to initiate legal proceedings. Nevis has also abolished Mareva injunctions, allowing trustees to manage funds even during litigation. Costs are typically lower than in the Cook Islands, making Nevis appealing to those seeking cost-effective solutions.

Belize is the most budget-friendly option, with fees about 32% lower than other jurisdictions. It provides immediate asset protection and does not follow traditional fraudulent transfer statutes. However, its track record in litigation is less extensive compared to the Cook Islands or Nevis.

| Jurisdiction | Statute of Limitations | Burden of Proof | Bond Requirement | Setup Cost Range | Best For |

|---|---|---|---|---|---|

| Cook Islands | 1–2 years | Beyond reasonable doubt | None | $20,000–$25,000 | High-stakes protection, proven track record |

| Nevis | 2 years | Beyond reasonable doubt | ~$100,000 | Moderate | Cost-conscious professionals, strong deterrence |

| Belize | Immediate protection | N/A | None | Lowest | Budget-conscious individuals, quick setup |

| Cayman Islands | 6 years | Creditor must prove fraud | None | High | Estate planning, dynasty trusts |

"A well-managed, experienced trustee in a slightly less favorable jurisdiction will outperform a poorly managed trustee in the strongest statutory environment."

– Gideon Alper, Attorney

The quality of the trustee plays a critical role. For instance, the Cook Islands has nine licensed trustee companies, fostering competition and reliability. When choosing a jurisdiction, verify the trustee’s licensing, track record, and ability to defend assets under legal pressure.

It’s also important to avoid retaining direct control over the trust. In FTC v. Affordable Media (Anderson), settlors who retained backdoor control over their trust were jailed for contempt. Independent, institutional trustees operating outside U.S. jurisdiction are essential for maintaining the structure’s integrity.

Protecting Real Estate with HELOCs and Liens

Real estate equity can be protected through financial strategies, even though the property itself cannot be moved offshore. Home equity lines of credit (HELOCs) and liens are effective tools for reducing visible equity and discouraging creditor claims.

A HELOC creates secured debt against the property, reducing its equity on paper. The withdrawn funds can then be transferred to an offshore trust or LLC, converting the equity into protected liquid assets.

Another option is filing liens through friendly entities or offshore LLCs. These liens create the appearance of encumbrance, making the property less appealing to creditors. The lienholder maintains priority over future claims, effectively safeguarding the equity.

For investment properties, holding real estate in an offshore LLC provides liability protection. If an incident occurs on the property, liability is generally limited to the LLC’s assets. Combining this with a Bridge Trust – where a Cook Islands or Nevis trust owns the LLC – adds another layer of protection that U.S. courts cannot penetrate.

Global Wealth Protection offers tailored solutions for these strategies, including offshore trust and company formation. Their services emphasize compliance while building robust defenses against potential creditors.

Conclusion

With 59% of U.S. physicians experiencing at least one lawsuit during their careers and 82% of specialists facing legal action by age 55, the financial risks are stark. Personal losses from excess judgments can range from $750,000 to $2 million, underscoring the importance of advanced asset protection strategies. For many in high-risk professions, offshore asset protection creates a jurisdictional barrier that surpasses the protections of domestic structures.

The key to effective asset protection lies in proactive planning and full transparency. Assets must be transferred well before any legal disputes arise to avoid accusations of fraudulent conveyance. Modern offshore planning focuses on creating clear legal barriers and leveraging jurisdictional advantages, rather than relying on secrecy. As attorney James G. Bohm explains, "Offshore asset protection is still viable, but it’s no longer a ‘hidden vault.’ Today, it’s most effective as part of a transparent, legally compliant, and professionally structured estate and asset plan".

"You don’t rise to the level of your income – you fall to the level of your legal structure."

– Brian T. Bradley, Esq., Bradley Legal Corp

Choosing the right jurisdiction, such as the Cook Islands or Nevis, significantly enhances protection against creditor claims. Combining offshore trusts, LLCs, and strategic planning creates a robust defense, safeguarding assets while maintaining compliance with legal standards. This approach not only shields wealth but also provides peace of mind.

Global Wealth Protection employs these time-tested strategies to help high-risk professionals secure their assets. Through offshore trusts and company formation, they ensure both compliance and strong defenses. Acting before litigation strikes is essential to preserving your financial future.

FAQs

Is offshore asset protection legal for U.S. citizens?

Yes, offshore asset protection is allowed for U.S. citizens, provided it follows U.S. tax laws and reporting rules. For instance, if you hold foreign accounts with a balance exceeding $10,000, you must file the FBAR (Foreign Bank Account Report). Ensuring the structure is set up correctly and all regulations are followed is crucial to staying compliant and avoiding potential legal troubles.

When is it too late to move assets offshore?

If you’re already dealing with lawsuits, creditors, or legal claims, moving assets offshore is usually no longer an option. Courts might see these transfers as fraudulent and could work to undo them. The key is timing – acting early and meeting all legal requirements is crucial to ensure the process holds up. The best approach? Plan ahead and take action well before any legal or financial troubles come your way.

Which offshore jurisdiction is best for my situation?

The ideal offshore jurisdiction varies based on individual needs, but a few options consistently rank highly due to their strong legal systems. The Cook Islands is a standout for offshore trusts and LLCs, providing excellent asset protection and privacy – making it particularly appealing to professionals such as physicians, attorneys, and real estate developers. Another favorite is Belize, recognized for its affordable and straightforward solutions. To choose the right jurisdiction for your specific goals, it’s crucial to work with experienced legal and financial advisors.