Gold remains a go-to safe haven for uncertain times, offering stability when markets stumble. By January 2026, its price hit over $5,066 per ounce, underscoring its enduring appeal. While cryptocurrencies like Bitcoin and offshore asset protection strategies are gaining attention, gold’s long-standing reputation as a hedge against economic and geopolitical risks keeps it at the forefront for many investors.

Key Takeaways:

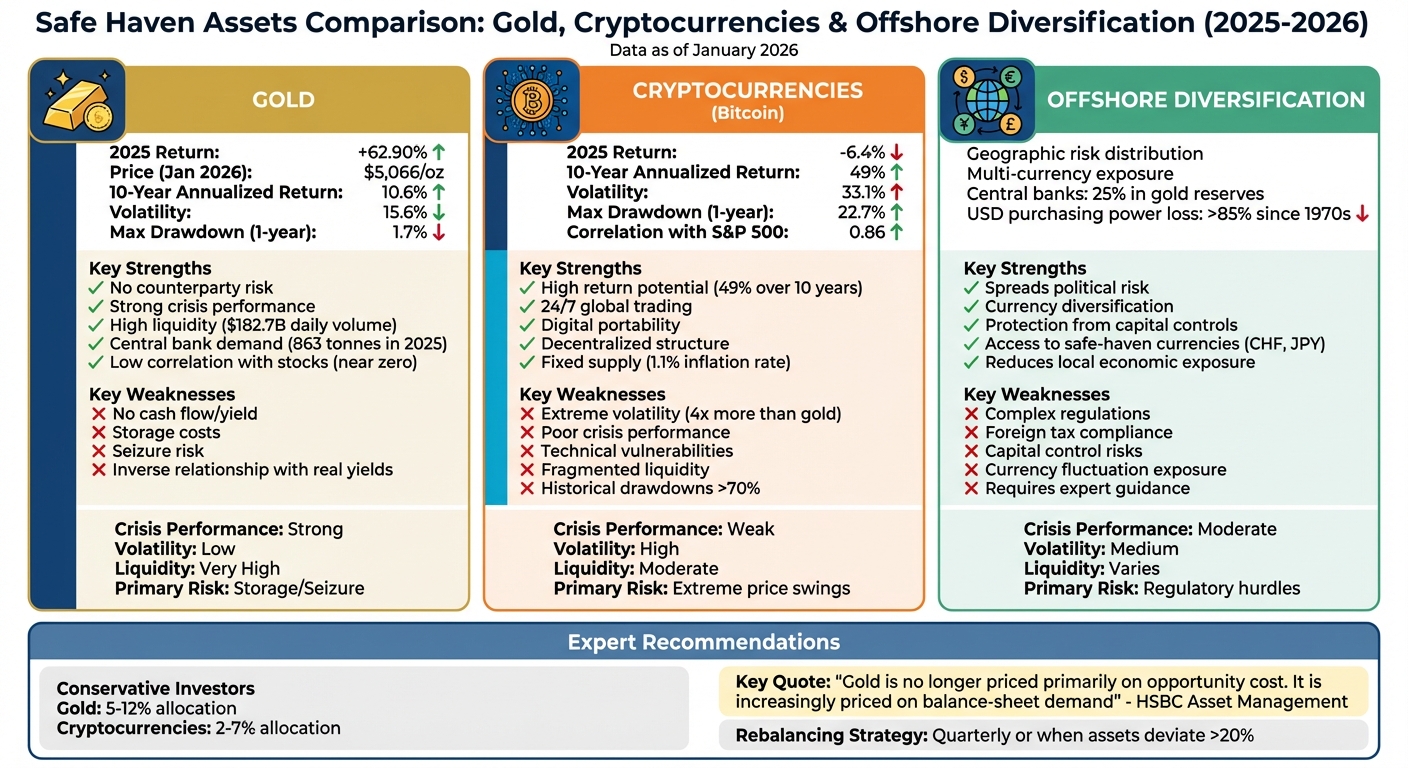

- Gold: Reliable during crises, with low correlation to stocks and consistent demand from central banks. However, no cash flow and storage costs are drawbacks.

- Cryptocurrencies: Bitcoin offers high returns (49% annualized over 10 years) but is highly volatile and less dependable in crises.

- Offshore Diversification: Reduces local political and currency risks but requires navigating complex regulations and potential capital controls.

Quick Comparison:

| Feature | Gold | Cryptocurrencies | Offshore Diversification |

|---|---|---|---|

| Crisis Performance | Strong | Weak | Moderate |

| Volatility | Low | High | Medium |

| Liquidity | Very High | Moderate | Varies |

| Primary Risk | Storage/Seizure | Extreme price swings | Regulatory hurdles |

Gold remains a cornerstone for stability, while Bitcoin and offshore strategies can complement portfolios for those seeking diversification. Balancing these options is key to navigating today’s complex financial landscape.

1. Gold

Economic Uncertainty

Gold has consistently delivered an annualized return of 8% since 1971, outperforming bonds and most commodities. What makes gold stand out is its nearly zero correlation with stocks. Unlike bonds, gold is free from counterparty risk, making it a unique asset in times of economic upheaval. Historically, during major geopolitical crises since 1990, gold has averaged a 4% gain in the month following such events, often outperforming other safe-haven assets. Robert S. Jeter II, Founder of Back Bay Financial Planning & Investments, sums it up well:

"It’s hard to argue that gold isn’t a great economic malaise hedge".

Financial advisors usually recommend treating gold as a form of insurance rather than a primary investment, suggesting it comprise 5% to 15% of a diversified portfolio. While stocks tend to outperform gold over the long term (20–30 years), gold can significantly outpace equities during shorter periods of economic stress, particularly over 3–5 years.

This resilience naturally fuels debates over its effectiveness as an inflation hedge.

Inflation Protection

Gold serves as a hedge over the long term, though only 16% of its price movements since 1971 have aligned with changes in the Consumer Price Index (CPI). Instead, gold’s strength lies in its ability to guard against currency debasement and money supply growth (M2), rather than directly tracking consumer prices.

When inflation has ranged between 2% and 5%, gold’s price has risen by an average of 8% annually. Its inflation-adjusted return since 1971 has ranged between 2.0% and 3.6%. Many modern investors view gold as protection against fiscal deficits and policy uncertainty, rather than a straightforward CPI tracker. David Einhorn, Founder of Greenlight Capital, encapsulates this shift:

"Deficits, not CPI, are the key driver now".

Gold’s supply grows slowly, with mining output increasing by just 1.75% in 2024. Meanwhile, central banks continue to buy gold aggressively – 166 tonnes in Q2 2025 alone – helping it maintain purchasing power over time. These factors highlight gold’s role as a safeguard in turbulent economic environments.

Beyond inflation, geopolitical factors further emphasize gold’s importance.

Geopolitical Stability

Gold has become a priority for central banks worldwide. Non-U.S. central banks now hold more gold in their reserves than U.S. Treasuries, a trend that has accelerated since 2014. By November 2025, gold accounted for 26.7% of global foreign reserves, surpassing the euro to become the second-largest reserve asset.

This shift reflects growing concerns over geopolitical tensions and the risks of sanctions. Lilia Peytavin, Global Market Strategist at J.P. Morgan Asset Management, explains:

"Gold is perceived to be a neutral asset that is not subject to freezes or blockades, as is the case with currency reserves".

Official gold purchases have surged, averaging over 1,000 tonnes annually – nearly three times the average of the previous decade. In January 2025, COMEX gold futures reached their highest levels since July 2007, driven by demand for physical assets amid trade policy uncertainty following the 2024 U.S. presidential election. Similarly, exposure to gold derivatives in the euro area hit €1 trillion in March 2025, a 58% increase from November 2024. These developments underline gold’s role as a reliable safe haven during periods of international instability.

Practical Accessibility

Gold offers unmatched liquidity compared to other hard assets. Its average daily trading volume is around $182.7 billion, far exceeding the $19.4 billion seen in inflation-linked securities. For context, selling 109 tons of gold (roughly $11.8 billion) would represent only about 5% of daily market turnover and would likely cause just a 2% price impact.

However, gold’s lack of cash flow introduces an opportunity cost when real interest rates rise, as its price tends to move inversely to real yields. This makes monitoring real yields critical for investors.

Physical gold also comes with regulatory risks, as seen when private ownership was outlawed in the U.S. from 1933 to 1974. Additionally, storage and insurance costs are ongoing concerns, and mining expenses set a rough floor for its price. Between 2006 and 2022, gold exhibited annual volatility of 17.2%, slightly higher than the S&P 500’s 15.6%, challenging perceptions of its stability. These practical considerations highlight the need to weigh gold’s safe-haven benefits against its operational challenges.

sbb-itb-39d39a6

2. Cryptocurrencies

Economic Uncertainty

When it comes to economic stress, cryptocurrencies like Bitcoin have struggled to live up to their reputation as safe havens. Take 2025, for example: while gold surged by an impressive 62.90%, Bitcoin actually dropped 6.4%. Its correlation with the S&P 500 hit 0.86, showing that it moved more like a risky asset than a defensive one. A clear instance of this was in October 2025 during tariff tensions – gold climbed 2.3% in just seven days, but Bitcoin tumbled 7.6%. Campbell Harvey, a finance professor at Duke University, summed it up well:

"Labeling bitcoin ‘digital gold’ is an oversimplification. Given its singular characteristics, bitcoin is unlikely to replace gold as the preferred safe-haven asset of investors".

Bitcoin’s volatility paints an even clearer picture. In 2025, its annualized volatility hit 33.1%, more than double gold’s 15.6%. Its maximum drawdown within a one-year period ending in early 2026 reached 22.7%, compared to gold’s much smaller 1.7%. Historically, Bitcoin has seen several drawdowns exceeding 70%. This level of unpredictability underscores the stark difference between Bitcoin and gold, especially in terms of stability during uncertain times.

Inflation Protection

Bitcoin’s fixed supply and low inflation rate – just 1.1% in 2024 compared to gold’s 1.75% – theoretically make it a hedge against currency debasement. But theory doesn’t always translate to reality.

Bitcoin’s returns tend to rise with U.S. inflation expectations, but only when inflation stays under 2%. Once inflation surpasses 3%, this relationship fades. Gold, on the other hand, holds its ground even under high inflation. Cryptocurrencies, by contrast, have shown a tendency to react negatively to surprises in the Consumer Price Index (CPI). As L.A. Smales from UWA Business School puts it:

"Cryptocurrencies do not currently offer investors a viable alternative to gold for hedging inflation".

Instead, Bitcoin’s price movements are largely driven by liquidity and adoption cycles.

Geopolitical Stability

Bitcoin’s decentralized structure gives it a theoretical edge against capital controls and government interference – something physical gold can’t claim, as it’s subject to seizure. However, Bitcoin’s real-world performance during geopolitical crises has been inconsistent.

For instance, between late January and early February 2026, gold surged 7.3% in just one week, briefly exceeding $5,500 per ounce, buoyed by geopolitical tensions. During the same period, Bitcoin fell 4.63%. While some studies suggest cryptocurrencies might hedge against fiat currency risks, data from 2025–2026 shows Bitcoin behaving more like a high-risk, high-beta asset during moments of market stress.

Additionally, central banks continue to favor gold over Bitcoin. In 2025, central banks purchased an estimated 863 tonnes of gold, creating a structural demand that Bitcoin lacks. Bitcoin also faces unique technical vulnerabilities, such as the risk of 51% attacks and potential threats from quantum computing.

Practical Accessibility

Bitcoin’s 24/7 global trading and digital portability make it undeniably convenient. The approval of spot Bitcoin ETFs in January 2024 and regulatory clarity from initiatives like the EU’s MiCA (December 2024) and the U.S. GENIUS Act (July 2025) have also made it easier for institutional investors to participate.

However, liquidity remains a significant challenge. For example, selling $11.8 billion worth of Bitcoin could trigger a 25% price drop, whereas the same transaction in gold would only cause a 2% impact. By February 10, 2026, Bitcoin’s price had fallen to about $68,854, down from $87,508 on January 1, 2026.

Self-custody offers control but comes with risks like losing access to private keys. High volatility further complicates portfolio management. As Campbell Harvey advises:

"Bitcoin is hardly a safe-haven asset. Still, both bitcoin and gold can play important roles in diversified portfolios. But since they face different risks, betting exclusively on one or the other is unwise".

These challenges highlight why many investors continue to see gold as the go-to safe-haven asset.

3. Offshore Diversification

Economic Uncertainty

Offshore diversification involves spreading assets across different countries and currencies to reduce exposure to political risks like sanctions or asset freezes. This approach gained prominence when Western nations froze Russian central bank assets following the Ukraine invasion. This event spurred central banks globally to accelerate moves toward gold and non-dollar assets.

Daniela Hathorn, Senior Market Analyst at Capital.com, highlights the appeal of gold in uncertain times:

"Gold has offered something increasingly scarce in modern portfolios: an asset that is no one else’s liability, immune to default risk, sanctions, capital controls and political interference".

Central banks have taken the lead in this shift. In 2022, they purchased 1,037 tonnes of gold – the largest amount in 50 years – to shield reserves from geopolitical pressures. Foreign investment in U.S. debt has steadily declined since the 2008 financial crisis, while gold’s share in official reserves has increased. Emerging economies like China, Turkey, and Poland have been particularly active in reducing their reliance on the dollar.

Some countries, such as Switzerland, are also innovating in their financial strategies. On December 31, 2024, a Swiss initiative proposed amending the Constitution to require the Swiss National Bank to hold part of its reserves in Bitcoin alongside gold. This move aimed to strengthen financial independence.

These geopolitical and financial shifts also impact inflation trends, as discussed below.

Inflation Protection

Offshore diversification can help safeguard purchasing power, especially during periods of local currency devaluation. Investing in assets like gold or international property is one way to achieve this. For context, the U.S. dollar has lost over 85% of its purchasing power since the early 1970s.

Today, central banks hold roughly 25% of global gold reserves as they move away from dollar-denominated assets. HSBC Asset Management notes:

"Gold is no longer priced primarily on opportunity cost. It is increasingly priced on balance-sheet demand".

By holding assets in foreign jurisdictions or outside traditional fiat systems, investors can reduce risks tied to sanctions or custody limitations. Geographic diversification also helps smooth exposure to local economic cycles.

However, managing currency risk is crucial. Exchange rate fluctuations can undermine the benefits of offshore investments if not carefully addressed. Tools like forward contracts allow investors to lock in exchange rates for future transactions without upfront costs, offering predictability. Currency options, on the other hand, provide the flexibility to benefit from favorable rate changes while requiring an upfront premium.

Geopolitical Stability

Offshore strategies also provide a buffer against political instability. The modern global landscape, shaped by strategic rivalries and fragmented supply chains, has upended the notion that globalization reduces political risk. Nigel Green, CEO of deVere Group, captures this reality:

"Investors used to analysing fundamentals alone are being forced to price in a new global economic order, which is fast beginning to assert itself in their asset allocation decisions".

Neutral jurisdictions remain key. Switzerland’s long-standing stability and low yields make the Swiss franc a trusted safe haven. Similarly, the Japanese yen often emerges as a strong safe-haven currency in various economic models. Gold also provides a more effective hedge against U.S. dollar exchange rate risks for emerging market currencies like the Brazilian real and Russian ruble compared to developed market currencies.

However, capital controls can pose challenges. Governments may restrict capital movement during economic stress, as seen with China’s ban on Bitcoin and India’s partial restrictions. Evaluating the political risks of a primary jurisdiction – such as regime changes or capital controls – becomes an essential part of wealth protection.

Practical Accessibility

Offshore diversification requires expert legal and financial guidance. For example, investing in offshore property involves navigating local laws, tax obligations, and stricter lending criteria for non-residents. Engaging local legal experts is essential to avoid costly mistakes.

Using multi-currency accounts can help investors delay currency conversions and time exchanges more favorably. Additionally, a dollar-cost averaging strategy – spreading currency purchases over time – can reduce the impact of short-term market volatility.

This approach works best as part of a larger portfolio strategy. Daniela Hathorn emphasizes:

"In a world where uncertainty is structural, not cyclical, precious metals remain one of the few assets designed not to predict the future, but to survive it".

While physical gold has its advantages, it is not immune to risks like seizure. Digital alternatives also come with technical vulnerabilities. Ultimately, offshore diversification isn’t a one-size-fits-all solution – it’s a framework for spreading risk across jurisdictions, currencies, and asset types. It complements broader portfolio diversification strategies discussed earlier.

Strengths and Weaknesses

This section dives into the strengths and weaknesses of various asset protection strategies, building on the performance profiles discussed earlier.

Each strategy comes with its own trade-offs. Gold serves as a reliable anchor during market downturns, maintaining value when traditional markets falter. It offers high liquidity and avoids counterparty risk, meaning it doesn’t depend on any institution’s solvency. That said, gold doesn’t generate cash flow or dividends, and storing it physically adds costs and risks, including the potential for seizure.

Cryptocurrencies, such as Bitcoin, stand out for their potential to deliver significant returns. For instance, Bitcoin achieved an annualized return of 49% over a 10-year period through 2025, far surpassing gold’s 10.6% return. However, its extreme volatility and susceptibility to technical issues make it less dependable as a safe haven. Bitcoin is at least four times more volatile than gold and has endured losses exceeding 70% multiple times. During liquidity crises, it often declines alongside other risk assets. As Campbell Harvey, a Finance Professor at Duke University, points out:

"Labeling bitcoin ‘digital gold’ is an oversimplification. Given its singular characteristics, bitcoin is unlikely to replace gold as the preferred safe-haven asset of investors".

Offshore diversification spreads risks across different nations and currencies, protecting investors from local political instability and currency devaluation. Safe-haven currencies like the Swiss franc and Japanese yen often provide stability during uncertain times. This approach works best when paired with assets such as gold or international real estate. However, it comes with its own challenges, including navigating foreign tax laws, regulatory hurdles, capital controls, and currency fluctuations. Managing these risks often requires tools like forward contracts or options, and governments may restrict capital movement during economic crises.

Here’s a quick comparison of the key features:

| Feature | Gold | Cryptocurrencies | Offshore Diversification |

|---|---|---|---|

| Primary Strength | No counterparty risk; stable in crises | High mobility; 49% 10-year return | Distributes risks across nations and currencies |

| Primary Weakness | No yield; storage and seizure risks | Extreme volatility; technical risks | Regulatory hurdles and capital controls |

| Crisis Performance | High; rose 64% in 2025 | Low; fell 6.4% in 2025 | Moderate; varies by jurisdiction |

| Liquidity | Very high; minimal market impact | Fragmented; large sales affect price | Depends on asset class |

Ultimately, choosing the right mix of these strategies depends on an investor’s risk tolerance and long-term goals. Gold offers stability and protection during downturns, cryptocurrencies provide growth opportunities with higher risk, and offshore diversification adds a layer of geographic risk management. Rather than viewing these strategies as standalone solutions, experts recommend integrating them into a broader, diversified portfolio. Each plays a complementary role in balancing risk and reward.

Conclusion

Gold continues to stand out as a reliable safe haven in 2026, reaching an all-time high of over $5,066 per ounce by January 21, 2026. Over the past two decades, it has delivered an impressive annualized return of 11.3%, solidifying its role as "crisis insurance". On the other hand, Bitcoin, despite achieving a 49% annualized return over the past 10 years, remains highly volatile. Its tendency to decline during market downturns makes it less dependable when stability is most needed.

When crafting investment strategies, aligning allocations with personal risk tolerance and financial goals is essential. Conservative investors are often advised to allocate 5–12% of their portfolios to gold, while those seeking higher returns might consider a smaller 2–7% allocation to cryptocurrencies. However, with gold’s current inflation-adjusted prices sitting at nearly three times the long-term average, some experts suggest capping gold exposure at 5% of a portfolio to manage risk. To maintain balance, regular quarterly rebalancing or adjustments when asset values deviate by more than 20% can help strengthen portfolio stability. This approach underscores gold’s steadiness compared to the unpredictable nature of cryptocurrencies.

Beyond these tailored allocations, combining a mix of assets can further enhance portfolio strength. A diversified strategy that includes gold, offshore investments, and selective cryptocurrency exposure provides a robust defense against market fluctuations. Gold remains a cornerstone for stability and liquidity during economic crises, while cryptocurrencies offer potential for significant growth. Offshore diversification spreads risk across different jurisdictions and currencies, adding another layer of security. Keeping an eye on central bank activity is equally important. In 2025, central banks purchased an estimated 863 tonnes of gold – about 20–30% of annual mine supply – fueling the current bull market and reinforcing gold’s reputation as a safe haven. However, any decline in central bank purchases could remove a key support for gold prices.

FAQs

Should I own physical gold or a gold ETF?

The decision to invest in physical gold or gold ETFs comes down to your priorities – whether that’s long-term stability, ease of trading, or convenience. Physical gold is a tangible asset that stands out for preserving wealth over time, but you’ll need to account for storage and insurance costs. On the other hand, gold ETFs are much simpler to trade and offer greater liquidity, making them a better fit for short-term strategies. Think about your investment timeline, comfort with risk, and whether you prefer holding gold in your hands or managing it through a digital platform when making your choice.

How much gold is too much in a portfolio?

Allocating 10%-15% of your diversified portfolio to gold is a common suggestion. This usually breaks down to about 10% in physical gold and up to 5% in gold-related equities, depending on your financial goals and how much risk you’re comfortable taking. These percentages aren’t set in stone – adjust them to fit your personal investment strategy and circumstances.

What’s the biggest risk to gold prices in 2026?

The biggest challenge for gold prices in 2026 could stem from a reduction in risk premia and market volatility. If economic conditions stabilize and geopolitical tensions subside, gold’s allure as a safe-haven asset might diminish, potentially driving prices down.