Stress testing your wealth plan is like a financial fire drill – it helps you prepare for worst-case scenarios before they happen. Could your finances handle a 40% market crash, a 10% inflation spike, or a legal crisis? Most plans assume smooth conditions, but life rarely works that way. Here’s what you need to know:

- Find Weaknesses: Identify risks like untitled assets, outdated beneficiaries, or overexposure to U.S. laws and markets.

- Test Scenarios: Use tools like Monte Carlo simulations to evaluate how your plan performs during market crashes, inflation, or income loss.

- Protect Assets: Offshore trusts, LLCs, and diversification across countries can shield wealth from lawsuits and geopolitical risks.

- Plan for Inflation: Ensure your portfolio grows faster than rising costs, with liquidity for 1–3 years of living expenses.

- Review Regularly: Test your plan every two years or after major life changes to keep it resilient.

Step 1: Find Weaknesses in Your Wealth Plan

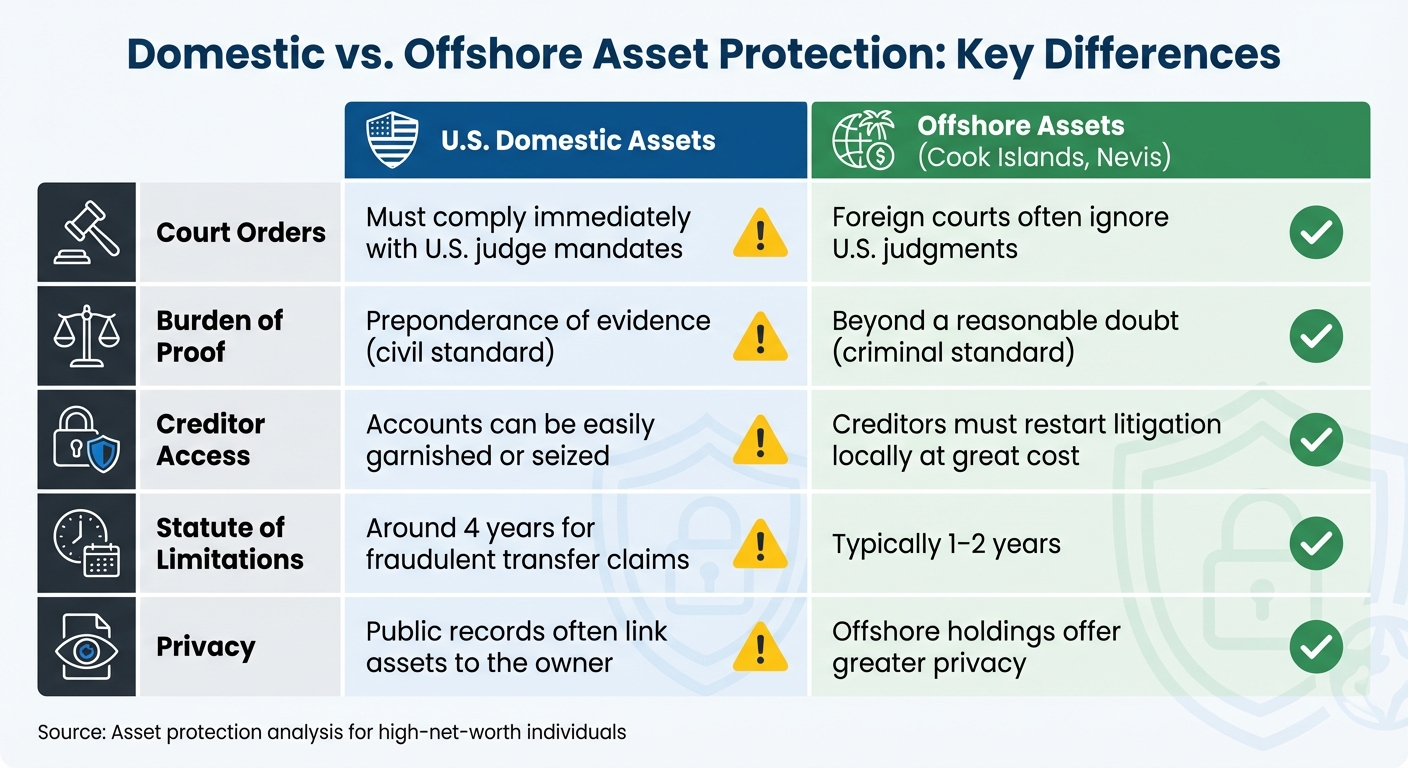

Domestic vs Offshore Asset Protection: Key Differences Comparison

The first step in evaluating your wealth plan is pinpointing its vulnerabilities. Start by listing all your assets – real estate, investments, businesses, retirement accounts, and bank accounts. Pay special attention to those held solely in your name. Why? Assets directly tied to your name are easy targets for lawsuits, creditor claims, and court orders. With around 5 million new court cases filed annually in the U.S., high-net-worth individuals often find themselves in the crosshairs.

Overlooking critical steps, like retitling assets into LLCs or structuring offshore trusts for asset protection, or failing to update beneficiaries after major life changes, can leave your wealth exposed. And don’t think you can fix this after the fact – moving assets after a lawsuit has been filed is usually a dead-end. Courts commonly nullify such actions as "fraudulent conveyances", rendering them ineffective.

You also need to consider how the location of your assets impacts their safety.

Domestic vs. Offshore Asset Risks

Where your assets are held matters just as much as how they’re titled. Domestic assets in the U.S. are bound by U.S. court orders. If a judge demands you turn over property or funds, you typically have no legal way to resist. Creditors can garnish wages, freeze accounts, or seize property with relative ease under civil litigation laws.

Offshore assets, however, operate under entirely different rules. Jurisdictions like the Anguilla often ignore U.S. court judgments, forcing creditors to start fresh in local courts – an expensive and time-consuming process. In these cases, creditors must meet a much higher burden of proof, showing fraudulent intent beyond a reasonable doubt instead of the lower civil standard of a preponderance of evidence. Additionally, offshore jurisdictions often have shorter statutes of limitations for challenging asset transfers, sometimes as brief as one or two years, compared to roughly four years in the U.S..

| Feature | U.S. Domestic Assets | Offshore Assets (Anguilla) |

|---|---|---|

| Court Orders | Must comply immediately with U.S. judge mandates | Foreign courts often ignore U.S. judgments |

| Burden of Proof | Preponderance of evidence (civil standard) | Beyond a reasonable doubt (criminal standard) |

| Creditor Access | Accounts can be easily garnished or seized | Creditors must restart litigation locally at great cost |

| Statute of Limitations | Around 4 years for fraudulent transfer claims | Typically 1–2 years |

| Privacy | Public records often link assets to the owner | Offshore holdings offer greater privacy |

The 2023 collapses of Silicon Valley Bank, Signature Bank, and First Republic highlighted another domestic risk: banking system concentration. Americans who kept their liquid wealth in just one U.S. banking system faced immense uncertainty, leading to increased interest in diversifying across jurisdictions. Adding to this, the U.S. dollar experienced its steepest decline in over 50 years during early 2025, falling more than 10% against the DXY index.

Common Wealth Plan Mistakes

Beyond legal titling issues, other structural errors can undermine your wealth plan. Concentrating all your assets in one country makes them subject to that nation’s laws, economy, and political stability. With the U.S. national debt exceeding $31 trillion, relying solely on dollar-based domestic assets introduces both currency and systemic risks.

Another common misstep is relying on insufficient legal barriers. Simple LLCs or domestic trusts may not shield you from "exception creditors", such as those pursuing claims for child support, alimony, or pre-existing torts. These creditors can often bypass domestic protections. Even Domestic Asset Protection Trusts (DAPTs) in states like Delaware or Wyoming allow exception creditors access, though Nevada offers stronger protections by excluding them. Additionally, Traditional and Roth IRAs only provide $1 million in inflation-adjusted protection during bankruptcy, and this safeguard doesn’t extend to other types of court judgments.

"The best plan is to set up protection years before any trouble. This way, no one can say you were trying to dodge a specific person who’s after your money."

- The Nestmann Group

Timing is everything. If you wait until a lawsuit or investigation is underway, you’ve likely missed your chance. Courts can and will reverse asset transfers made when a claim is foreseeable.

sbb-itb-39d39a6

Step 2: Test Economic Downturn Scenarios

After identifying vulnerabilities in Step 1, it’s time to stress-test your wealth plan against economic downturns. These scenarios help pinpoint critical gaps in your portfolio. 78% of financial advisors note that clients proactively bring up portfolio risk. Getting a clear picture of your downside exposure before a crisis unfolds is essential.

Start by analyzing how your portfolio would have fared during historical events like the 2008 financial crisis, when the S&P 500 dropped nearly 57% from its peak, or the 2020 COVID-19 market crash. You can also create hypothetical situations, such as a 10%–15% S&P 500 decline or a sudden 3% spike in interest rates. Tools like Monte Carlo simulations can model these scenarios, giving you a probability-based view of your financial plan’s success under varying conditions. For example, a plan showing an 80% success rate using average returns may see that figure fall below 40% when factoring in real-world market volatility. This step ensures you understand how your portfolio holds up during both past and imagined economic shocks.

Portfolio Performance During Recessions and Market Drops

Diversification is key during market downturns, but not all diversification strategies offer equal protection. Government bonds, for instance, have historically fared better than corporate bonds during equity declines. When the S&P 500 posted negative returns, government bonds showed a correlation of 0.0 to the index, while corporate bonds – though offering higher returns in growth periods (7.0% vs. 6.2%) – performed worse during downturns (4.7% vs. 5.0%).

It’s also important to evaluate your portfolio’s maximum drawdown, which reflects the largest peak-to-trough drop in value. This helps set realistic expectations. Remember, recovering from a 20% loss requires a 25% gain. Between 1980 and 2023, nearly 50% of publicly traded U.S. companies experienced a "catastrophic loss" (a 70% peak-to-trough decline without recovery). To avoid selling growth assets during downturns, consider keeping a cash reserve that covers one to three years of living expenses. Once you’ve addressed market fluctuations, shift your focus to inflation’s impact on your portfolio.

Testing for High Inflation

Inflation erodes purchasing power faster than many expect. Simulating multi-year scenarios with inflation rates of 10% or higher can reveal how quickly savings might dwindle. Cash and fixed-income investments are particularly vulnerable to inflation, so focus on whether your portfolio’s growth outpaces the rising cost of living. Real returns – adjusted for inflation – matter far more than nominal account balances.

Take a close look at both essential and discretionary expenses to assess how a 10%+ cost increase would affect your financial plan. Make sure your liquidity buffer can cover at least 24 months of potential spending needs. Additionally, review your debt levels, as high debt can amplify financial stress during inflationary periods. For precise modeling, consider professional tools like Morningstar Direct, BlackRock‘s Scenario Tester, or J.P. Morgan‘s Digital Portfolio Analysis. These tools provide a detailed view of how your portfolio might perform under inflationary pressures.

Step 3: Protect Against Legal and Creditor Threats

After assessing how your portfolio holds up under economic challenges, it’s time to address legal risks that could jeopardize your wealth. Civil lawsuits, malpractice claims, divorce settlements, business failures, and tax levies are some of the most common ways individuals can lose their accumulated assets. On average, defending a lawsuit in the U.S. costs between $5,000 and $20,000. However, the bigger issue is how easily creditors can track down and seize your assets once they secure a judgment.

Testing for Creditor Claims

With market risks evaluated, the next step is to test how well your assets are protected from creditor claims. Imagine a situation where a creditor wins a judgment and forces you to disclose all your assets under oath – this includes real estate, bank accounts, investments, and even cryptocurrency. Creditors often use asset search firms and forensic accountants to dig through tax records, bank statements, and public filings to uncover everything you own.

Domestic structures like LLCs can offer some protection, but they’re not foolproof. If you mix personal and business finances, courts can "pierce the corporate veil", exposing your assets. Domestic Asset Protection Trusts (DAPTs), available in 19 states such as Nevada, Delaware, and South Dakota, provide another layer of defense. However, these trusts are still subject to federal court orders, which limits their effectiveness.

It’s critical to set up asset protection measures before any legal claims arise. Transfers made after a lawsuit are considered "fraudulent conveyances" and can be reversed, often with penalties. Domestic trusts also require a "seasoning period" of 2–4 years before they offer real protection. To test your readiness, ask yourself: if a creditor filed a claim today, which of your assets would be vulnerable? For example, ERISA-qualified retirement plans like 401(k)s are fully protected under federal bankruptcy laws, while traditional and Roth IRAs have a $1 million protection cap.

Benefits of Offshore Trusts and Legal Structures

To strengthen your defenses even further, consider the advantages of offshore asset protection structures. After running simulations for creditor claims, you’ll see that offshore trusts can provide a level of security that domestic options simply can’t match. These trusts place your assets under the control of foreign trustees, who are beyond the reach of U.S. court orders. In jurisdictions like the Cook Islands and Nevis, creditors face a much higher burden of proof – requiring them to demonstrate "actual fraud" beyond a reasonable doubt, the same standard used in criminal cases.

Offshore jurisdictions also make it costly for creditors to pursue claims. For example, in Nevis, creditors must deposit around $100,000 (EC $270,000) with the court before they can even file a case against a trust settlor. In Belize, the required deposit is either BZ $50,000 (about $25,000) or 50% of the claim amount, whichever is higher. Additionally, many offshore jurisdictions operate under a "loser pays" system, meaning creditors who lose their case must cover your legal fees.

Setting up an offshore trust typically costs between $25,000 and $75,000, with annual maintenance fees ranging from $10,000 to $28,000. While these costs are higher than domestic alternatives, the protection they offer is far more robust for individuals with significant legal exposure.

| Feature | Domestic Asset Protection Trust | Offshore Asset Protection Trust |

|---|---|---|

| Statute of Limitations | 2–4 years | 1–2 years |

| Court Jurisdiction | Under U.S. court orders | Non-U.S. jurisdiction; ignores foreign judgments |

| Burden of Proof | Civil standard (preponderance of evidence) | Criminal standard (beyond reasonable doubt) |

| Setup Cost | $5,000–$15,000 | $10,000–$75,000 |

| Annual Fees | $4,000–$10,000 | $5,000–$28,000 |

Step 4: Handle Currency and Geopolitical Risks

Once you’ve safeguarded your assets from legal challenges, it’s time to assess how well they can withstand currency fluctuations and geopolitical turmoil. These external factors – like economic shifts or political instability – can undermine the value of your wealth, even if your domestic investments are diversified. For example, in 2025, the U.S. Dollar lost about 10% against the DXY index, which measures its performance against a basket of major currencies. If your portfolio is entirely tied to the dollar, you’re vulnerable to inflation and global tensions in ways that domestic diversification can’t address.

Testing for Currency Devaluation

Imagine the dollar’s value dropping by 10–40% over the next five years. Could your portfolio absorb the impact? Would you still have enough for retirement, education, or healthcare costs? Here, asset-liability matching becomes critical – your investments should align with the currency you’ll need for future expenses. A comparison of U.S.-listed and Euro-denominated Euro ETFs from 2012 to 2022 shows why this matters: the U.S.-listed ETF returned 7% annually, while the Euro-denominated version achieved 9%, demonstrating the importance of matching investments to spending currencies.

Multi-currency accounts in countries like Switzerland or Austria offer a practical way to hedge against dollar volatility. Swiss private banks typically require a minimum of $1,000,000, while Austrian banks have lower thresholds, starting around $250,000 to $300,000.

"Currency planning is about alignment, not prediction." – Skybound Wealth USA

After addressing currency risks, the next step is to consider how geopolitical diversification can protect your assets.

Reducing Geopolitical Risk with Multi-Jurisdiction Holdings

Geopolitical instability can disrupt even the most carefully planned wealth strategies. For instance, following Russia’s 2022 invasion of Ukraine, over 15,000 high-net-worth individuals moved their assets or families to neutral countries like the UAE and Armenia. Similarly, as of 2023, the European Union has frozen more than €21.5 billion in private assets tied to sanctioned individuals. Even without direct exposure to sanctions, domestic political polarization or regulatory changes could create unexpected vulnerabilities.

Spreading your assets across multiple jurisdictions adds a layer of protection. Holding foreign real estate in countries like Portugal, Panama, or Mexico through offshore structures – rather than under your name – can enhance privacy and make it harder for creditors to seize them. There’s a financial upside, too: in the first half of 2025, non-U.S. equities outperformed U.S. equities by 12.1%, emphasizing the value of geographic diversification. Offshore banking in stable locations like the Isle of Man or Switzerland also reduces the risk of domestic bank failures – something that became all too real after the collapse of Silicon Valley Bank, Signature Bank, and First Republic in 2023.

"A domestic portfolio manages financial risk; an international portfolio manages sovereign risk. The first deals with markets. The second deals with governments." – Brandon Roe, The Nestmann Group

Step 5: Add Offshore Strategies to Your Wealth Plan

Once you’ve identified potential risks to your assets, the next step is to strengthen your wealth plan by incorporating offshore strategies. These strategies act as legal and operational safeguards, offering additional protection during lawsuits, economic downturns, or political instability. Timing is critical – you must implement these measures before any legal threats arise. Otherwise, courts could reverse your actions, labeling them as fraudulent conveyances.

Offshore Trusts and Company Formation

Offshore trusts are a powerful tool for shielding your assets. By transferring ownership to a foreign trustee, assets are placed beyond the jurisdiction of U.S. courts. Jurisdictions like the Cook Islands and Nevis are particularly effective, as they do not recognize U.S. judgments. Creditors are forced to re-litigate under stricter foreign laws, which can be both time-consuming and costly. Additionally, these jurisdictions often have short statutes of limitations – sometimes as brief as one or two years – making it harder for creditors to act.

For even greater security, consider using an offshore trust in combination with an offshore LLC. This layered approach creates multiple legal barriers, making it significantly harder for creditors to access your assets. Anguilla is a popular choice for forming LLCs due to its zero corporate tax policy, lack of public ownership registries, and straightforward reporting requirements. These features make it especially attractive for digital businesses and cryptocurrency investments. Setting up an Anguilla LLC typically costs around $3,350 for the first year.

"The best time to build your defenses is during peacetime, when you can carefully plan each wall, moat, and tower without the pressure of imminent attack." – Dominion

In addition to structural planning, operational compliance is essential. Jurisdictions like Anguilla and Nevis offer non-public registries, which help protect your identity while still meeting U.S. reporting obligations, such as filing an FBAR (Foreign Bank Account Report) for accounts exceeding $10,000. Ignoring these requirements can result in penalties that exceed the value of the accounts themselves.

Using Global Wealth Protection Services

To navigate the complexities of offshore strategies, Global Wealth Protection offers specialized services tailored to asset protection and tax planning. Their expertise spans offshore company formation – particularly in Anguilla – as well as private U.S. LLC setups designed to prioritize privacy. Their comprehensive solutions include handling all necessary filings, certifications, bank introductions, and ongoing consultations to ensure your structure aligns with your financial goals.

Setting up an offshore structure typically takes four to eight weeks, starting with selecting the right jurisdiction and entity type (such as a trust or LLC). The process includes drafting incorporation or trust documents, retitling assets, and opening bank accounts. Annual maintenance costs for these structures generally range from $500 to $2,000, covering registered agent fees, government renewals, and compliance filings. For wealthier individuals, Private Placement Life Insurance (PPLI) offers additional benefits like tax-deferred growth and estate planning, though these policies usually require a minimum investment of $2 million.

"Going offshore isn’t shady. It’s smart. It’s about control." – Global Wealth Protection

To maintain the integrity of your offshore structure, you must follow strict operational protocols. This includes keeping separate bank accounts, filing necessary documentation, and recording decisions properly. Working with advisors who understand both U.S. regulations and the laws of your chosen jurisdiction is essential to ensure your plan remains compliant and effective.

Step 6: Retest and Monitor Your Wealth Plan

A solid wealth strategy isn’t a "set it and forget it" approach – it requires consistent attention. Markets fluctuate, laws shift, and personal circumstances evolve, all of which can impact the effectiveness of your plan. Regular monitoring helps ensure your financial safeguards remain strong and adaptable to new challenges, building on the offshore and legal protections established earlier.

Annual Reviews and Adjustments

Make it a habit to review your wealth plan at least annually. This involves checking key elements like insurance coverage, beneficiary designations for IRAs and 401(k)s, and ensuring your emergency fund still covers three to six months of expenses. Every two years, go a step further and run a comprehensive stress test, such as a Monte Carlo simulation, to measure how your plan holds up against market volatility, inflation, and unexpected spending needs. Ideally, a robust plan should achieve a success rate between 75% and 95%.

Life events can also disrupt your strategy. Marriage, divorce, the birth of a child, the loss of a loved one, career shifts, or significant property purchases all warrant immediate retesting of your plan. Similarly, external factors like sudden market crashes, inflation surges, or changes in tax laws should trigger a reassessment.

"Major life changes, even ones for the better, represent significant stress points when it comes to the longevity of your savings." – Scott Sommers, Principal at First Financial Consulting

Tools and Expert Assistance

Leverage tools like Monte Carlo simulations to test thousands of potential scenarios, factoring in variations in market returns, inflation, and spending patterns. Sensitivity testing is another useful method, helping you understand the impact of specific changes, such as a 1% rise in interest rates or a 30% drop in equity markets. For a deeper dive, reverse stress testing can pinpoint conditions that might cause your plan to fail – like a 20% portfolio loss. These tools, combined with regular reviews, help ensure your plan evolves with changing risks.

Partnering with a financial professional can add another layer of security. Schedule quarterly or semi-annual meetings with a fiduciary advisor who can fine-tune your assumptions, rebalance your portfolio, and adjust offshore structures to align with shifting regulations. This ensures your plan stays compliant with both U.S. reporting requirements and the laws of any offshore jurisdictions you’re utilizing. Firms like Global Wealth Protection offer ongoing consultations to help you navigate these complexities and keep your strategy effective and legally sound.

Conclusion

After examining both domestic and offshore strategies and putting your assets through rigorous stress tests, one thing stands out: flexibility is crucial. A wealth plan is only as effective as its ability to endure under real-world challenges. Stress testing acts like a safety drill, pinpointing weak spots before they escalate into full-blown crises. With economic conditions, legal landscapes, and personal circumstances constantly shifting, a plan that feels secure today might struggle during a market downturn, legal dispute, or currency fluctuation.

Using the vulnerabilities uncovered during stress testing, a strong wealth plan should incorporate specific strategies to mitigate risks. Three pillars support lasting financial security: regular stress testing to identify and address weaknesses, diversification across assets and jurisdictions to limit risk concentration, and offshore strategies that create legal protections against creditors and geopolitical uncertainty. Together, these elements establish a solid framework capable of withstanding financial shocks.

"A strong plan doesn’t avoid pressure but instead absorbs it." – Guild Capital

Maintaining these safeguards requires ongoing vigilance. Conduct thorough stress tests every two years, or immediately following major life changes like marriage, divorce, or significant asset acquisitions. Tools like Monte Carlo simulations and guidance from financial experts can help refine your strategy as new risks emerge. This proactive, integrated approach ensures your wealth plan remains resilient and ready to adapt to whatever challenges come your way.

FAQs

What’s the easiest way to stress test my current wealth plan?

Creating simple scenarios is a straightforward way to test your financial plan against potential challenges. Consider situations like a market downturn, a sudden income loss, or unexpected expenses. For instance, you could model a 25-30% drop in your portfolio or plan for a 3-6 month income gap. Running these scenarios allows you to identify weaknesses in your strategy and prepare for tough situations – no need for complicated tools or software.

When does an offshore trust make sense for me?

An offshore trust can be a powerful tool for those looking to secure strong asset protection, maintain privacy, and explore potential tax advantages. It’s especially useful if you’re dealing with risks like creditors, lawsuits, or other legal claims. High-net-worth individuals often turn to offshore trusts to protect their wealth, streamline estate planning, and ensure they stay compliant with U.S. tax regulations. Popular jurisdictions, such as the Cook Islands and Belize, are well-known for their legal safeguards tailored to these needs.

How much cash should I keep to avoid selling during a crash?

It’s a good idea to keep $500 to $1,000 in cash on hand for emergencies, such as power outages or natural disasters. Having this readily available means you won’t have to rely on selling investments, especially during times when the market is down.