Wealth preservation is not about luck – it’s about strategy. History shows that 70% of wealthy families lose their fortune by the second generation, and 90% by the third. The difference lies in planning. Families like the Vanderbilts lost their wealth due to poor diversification and lack of safeguards, while the Rockefellers and Mellons thrived by using tools like trusts, structured investments, and professional management.

Key takeaways:

- Diversify assets: Avoid overreliance on single industries, as seen with the Vanderbilt family.

- Use protective structures: Irrevocable trusts and LLCs shield wealth from taxes, creditors, and legal threats.

- Professional oversight: Appoint trustees or family offices for expert financial management.

- Educate heirs: Teach financial literacy to prepare future generations.

Modern strategies, such as combining domestic LLCs with structuring offshore trusts for asset protection, can further protect against lawsuits, currency risks, and political uncertainties. The key is to act early and treat wealth preservation as a disciplined, long-term endeavor.

Historical Examples: How Families Preserved Wealth During Crises

The difference between families that managed to preserve their wealth and those that lost it often boiled down to key decisions made during critical moments. Looking at three prominent American dynasties, we can see how distinct strategies – or the lack thereof – shaped their financial legacies.

The Vanderbilt Family: The Risk of Overreliance on a Single Industry

Cornelius Vanderbilt amassed a staggering fortune through shipping and railroads, making the family one of the wealthiest in the world. By 1883, William Vanderbilt, Cornelius’ son, was the richest man on the planet. However, the Vanderbilt wealth didn’t last. By 1973, when 120 family members gathered for a reunion, not one of them was a millionaire.

What went wrong? The family failed to adapt. They kept their wealth tied to railroads and shipping, even as the rise of cars, planes, and trucks revolutionized transportation. Compounding this, they divided assets among numerous heirs without using protective trusts, exposing the fortune to estate taxes and poor management. Lavish spending on extravagant estates further drained their wealth, leaving little for reinvestment.

"Any fool can make a fortune; it takes a man of brains to hold onto it." – Cornelius Vanderbilt

Despite Cornelius’ understanding of wealth preservation challenges, future generations didn’t implement the necessary safeguards. Without diversification or protective mechanisms, the Vanderbilt story became a cautionary tale of how fortunes can quickly erode.

The Rockefeller Family: Trusts as a Shield for Generational Wealth

John D. Rockefeller took a very different approach. Starting in 1934, he created the first trust, followed by a dynasty trust in 1952. These irrevocable trusts removed assets from taxable estates, allowing them to grow tax-free for future generations.

The strategy worked. The Rockefeller fortune, originally $8.4 billion, has been preserved over six generations and is now shared among more than 170 heirs. By separating assets from individual family members, these trusts provided protection against lawsuits, creditors, and divorce claims. They also enabled diversification into equities, real estate, energy, and technology. Instead of lump-sum inheritances, the trusts used discretionary terms like "suitable support and maintenance", preventing reckless spending.

Chase Bank, appointed as the institutional trustee, ensured professional management of the trusts. Even when the family faced lawsuits over environmental cleanup costs, the trust structure protected their assets from liability. This forward-thinking approach allowed the Rockefellers to survive economic downturns, including the Great Depression and shifts in the energy sector.

The Mellon Family: A Balanced Approach to Wealth and Entrepreneurship

Thomas Mellon, founder of what would become BNY Mellon, designed an estate plan that balanced wealth preservation with entrepreneurial freedom. Instead of handing out cash, he set up structured investments that gave heirs capital to start new ventures while protecting the principal.

This strategy paid off. From Thomas Mellon’s death in 1908 to today, the family has maintained an estimated $12 billion fortune. They weathered financial crises like the Panic of 1907 and the Great Depression while preparing heirs with financial education and structured succession plans. By encouraging productive enterprise while maintaining protective frameworks, the Mellons avoided the pitfalls of both over-centralization and fragmented inheritance.

These examples highlight the importance of strategic planning, diversification, and legal protections – concepts we’ll delve into further in the next section.

sbb-itb-39d39a6

Proven Strategies: How to Build Financial Resilience

Wealth preservation has always hinged on smart legal and financial planning. Just like the Rockefellers and Mellons, today’s investors can use these time-tested strategies to safeguard their assets. These tools form the backbone of financial resilience, especially in unpredictable markets.

Trust Structures: Revocable vs. Irrevocable Trusts

Revocable trusts, often called living trusts, give you full control over your assets. You can update beneficiaries, add or remove assets, or even dissolve the trust entirely. While they help avoid probate and keep your financial matters private, they don’t protect assets from creditors or IRS claims.

On the other hand, irrevocable trusts operate differently. Once assets are transferred, you relinquish direct ownership, which might seem limiting. However, this is exactly what shields those assets. As MetLife explains: “If you file bankruptcy or default on a debt, assets in an irrevocable trust won’t be included in bankruptcy or other court proceedings”.

Modern irrevocable trusts offer more flexibility than you might think. They can include income distributions, custom rules for asset allocation, and trustee appointments – all while safeguarding wealth. A specialized version, dynasty trusts, allows families to pass down wealth across generations while minimizing estate taxes.

"The goal of an irrevocable trust isn’t to strip away control; it’s to provide protection and stability." – Cote Law Group

Family Limited Partnerships and LLCs

Family Limited Partnerships (FLPs) and Limited Liability Companies (LLCs) provide families with a way to manage assets while protecting them from creditors. These structures divide ownership into two tiers: General Partners or Managing Members, who handle decisions, and Limited Partners or non-managing members, who hold economic value but no operational control.

One of the key advantages is charging order protection. If a creditor wins a judgment against a family member, they can’t seize the underlying assets. Instead, they’re limited to potential future distributions through a charging order, leaving the assets themselves untouched.

These entities also come with tax perks. Limited partnership interests often qualify for valuation discounts due to their lack of control and marketability, reducing their taxable value by 30–40% for gift and estate tax purposes. For instance, gifting a 20% interest in a $5 million LLC with a 40% discount lowers the taxable gift value from $1 million to $600,000 – saving $160,000 in taxes at a 40% tax rate.

With the federal transfer tax exemption set at $15 million per person in 2026, a married couple can transfer up to $30 million tax-free. By leveraging valuation discounts, families can pass even more wealth to future generations. To ensure these protections hold up, maintain strict business formalities like separate bank accounts, regular meetings, and detailed records.

Insurance Policies and Gifting Strategies

Beyond structural tools, financial instruments like insurance policies and gifting strategies add liquidity and tax efficiency. Life insurance, particularly whole life policies, can provide tax-free liquidity to replenish family trusts, ensuring they remain stable even if heirs borrow against trust assets. Since payouts are typically tax-free, they’re especially useful during estate transitions.

Generation-Skipping Trusts (GSTs) streamline wealth transfer by skipping one layer of taxation. Instead of passing assets from parent to child and then to grandchild – with taxes at every step – GSTs allow direct transfers to grandchildren, avoiding double taxation.

Charitable gifting is another powerful strategy. By donating to foundations, families can reduce their taxable estates while fostering a legacy of generosity and responsibility among younger generations. Prominent families have long used this approach to align financial planning with philanthropic goals.

Combining these strategies creates a robust, layered defense. For instance, the Mellons balanced secure investments with ventures that grew their wealth. By integrating trusts, business entities, insurance, and gifting, they sustained a $12 billion fortune from 1908 to the present.

Modern Tools: Asset Protection for Today’s Investors

Modern asset protection combines tried-and-true methods with contemporary tools, integrating domestic and international solutions to address risks like lawsuits, currency instability, and political uncertainties. This evolving approach reflects the need for both flexibility and resilience in safeguarding wealth.

Offshore Trusts and Foundations

Offshore Asset Protection Trusts (OAPTs) are a powerful way to shield assets. By transferring ownership to a trustee in jurisdictions such as the Cook Islands or Nevis, these trusts make it significantly harder for creditors to access your wealth. Many of these jurisdictions don’t automatically enforce U.S. court orders, requiring creditors to re-litigate their claims locally – a process that is both expensive and time-intensive. For example, Nevis often requires creditors to post a high bond before pursuing claims, and remedies are typically limited to charging orders, which only place liens on future trust distributions rather than seizing assets outright.

Private Interest Foundations provide similar protection but with additional governance benefits. These foundations, structured like corporations with a governing board, are particularly useful for preserving family wealth and ensuring smooth multi-generational wealth transfer.

Offshore structures also offer the advantage of jurisdictional and currency diversification. By moving assets offshore, investors can reduce risks tied to a single country, such as political instability, bank failures, or a weakening U.S. dollar. With the U.S. national debt exceeding $31 trillion and the dollar losing over 10% of its value since 2025, protecting against these risks has become increasingly important. Offshore solutions comply with global reporting standards like FATCA and CRS while maintaining strong legal safeguards. However, setting up these structures can take 11 to 21 months, so it’s critical to act proactively. Transfers made after legal claims arise may be voided as fraudulent.

Combining Private US LLCs with Offshore Companies

For robust protection, combining domestic and offshore entities creates layers of legal defenses. Domestic LLCs in states like Wyoming or Nevada offer strong protections, such as limiting creditors to charging orders. Wyoming Statute §17-29-503, for instance, ensures that creditors can only place liens on distributions, not seize the LLC’s assets.

"Own nothing that can hurt you. Control everything that matters."

– James Burns, Attorney

Adding an offshore LLC in jurisdictions like Nevis or Anguilla enhances this protection. These offshore entities can act as holding companies for assets like foreign real estate, creating a firewall against legal threats. Since these jurisdictions don’t recognize U.S. court judgments, creditors must re-litigate locally, further complicating their efforts.

The most advanced strategies often involve combining trusts and LLCs. For example, a trust-owned LLC merges the domestic charging order protections with the additional legal separation provided by an offshore trust. This layered approach is especially effective for shielding assets from lawsuits.

The need for such strategies is underscored by the sheer volume of legal actions in the U.S., which accounts for 80% of the world’s lawyers and 96% of global lawsuits. A new lawsuit is filed every 30 seconds, and small business owners face a 33% chance of being sued, with a median damage award of $201,000. To maintain these protections, it’s essential to follow strict formalities, such as keeping separate bank accounts, avoiding commingling funds, and documenting business decisions to prevent courts from piercing the corporate veil.

"The corporate veil is your strongest defense, but it’s only as strong as your daily financial habits."

– Commons LLC

Global Wealth Protection‘s Asset Preservation Services

Global Wealth Protection (GWP) specializes in integrating these modern strategies into customized asset protection plans. They offer services like offshore trust formation in jurisdictions such as the Cook Islands, Nevis, and Anguilla, which are known for their robust legal safeguards. For business owners, they combine domestic LLCs in states like Wyoming with offshore companies in Anguilla, providing both operational convenience and enhanced protection.

Their private interest foundations help ensure smooth wealth transfer across generations by establishing governance frameworks that preserve family assets over time. Additionally, GWP connects clients to stable banking systems in Europe and Asia, further diversifying their financial footprint.

For high-net-worth investors, GWP also advises on Private Placement Life Insurance (PPLI), which offers creditor protection, tax-deferred growth, and estate planning benefits. However, this option typically requires a minimum investment of $2,000,000.

Through private consultations and their GWP Insiders membership program, Global Wealth Protection provides step-by-step guidance tailored to individual needs. Their Global Escape Hatch action plans support strategic relocation, helping clients diversify their personal presence across multiple jurisdictions. Acting early is crucial, as setting up these structures after legal threats arise could expose transfers to fraudulent claim challenges.

Success vs. Failure: What Made the Difference

The story of the Vanderbilt family’s financial downfall compared to the enduring wealth of the Rockefellers and Mellons highlights key differences in strategy and foresight. While the Vanderbilts concentrated their wealth in railroads and shipping without protective measures, families like the Rockefellers and Mellons took a different approach. They diversified their investments – spreading wealth across industries like oil, banking, and real estate – and used legal tools like irrevocable trusts to shield assets from creditors, taxes, and spendthrift heirs. These choices helped the Rockefellers and Mellons maintain their fortunes, while the Vanderbilts saw their wealth dissipate over time.

The Rockefellers, for instance, excelled at both diversification and protection. John D. Rockefeller Jr. created the 1934 Family Trust and the 1952 Dynasty Trust, which were managed by professional trustees at Chase Bank rather than by individual family members. This centralized management helped preserve an estimated $8.4 billion across more than 70 heirs today. Similarly, the Mellon family has maintained their wealth – around $12 billion – through strategic business succession and safeguarded investments since 1908.

Another factor was fiscal discipline. The Vanderbilts poured money into lavish estates, turning their assets into costly liabilities. In contrast, the Rockefellers and Mellons focused on controlled distributions, philanthropy, and reinvestment. For example, Anderson Cooper, a Vanderbilt descendant, inherited just $1.5 million from his mother, Gloria Vanderbilt, who famously remarked there "was no trust fund".

These historical examples provide valuable lessons for modern wealth preservation. Below is a comparison of these historical strategies and their modern counterparts:

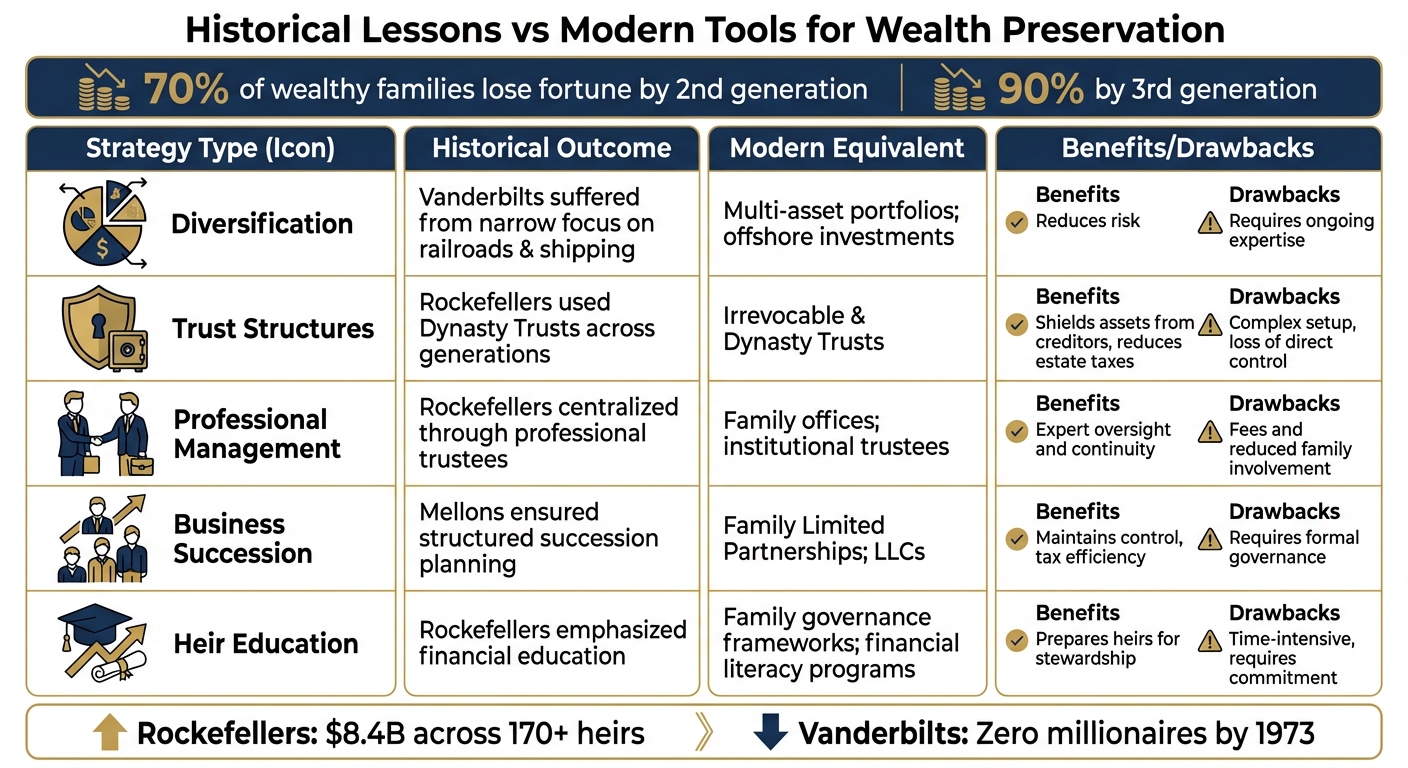

Comparison Table: Historical Lessons and Modern Tools

| Strategy Type | Historical Outcome | Modern Equivalent | Benefits/Drawbacks |

|---|---|---|---|

| Diversification | The Vanderbilts suffered due to a narrow focus on railroads and shipping. | Multi-asset portfolios; offshore investments | Benefits: Reduces risk. Drawbacks: Requires ongoing expertise and management. |

| Trust Structures | The Rockefellers used Dynasty Trusts to protect and grow their wealth across generations. | Irrevocable & Dynasty Trusts | Benefits: Shields assets from creditors and reduces estate taxes. Drawbacks: Complex setup and loss of direct control. |

| Professional Management | The Rockefellers centralized wealth management through professional trustees. | Family offices; institutional trustees | Benefits: Provides expert oversight and continuity. Drawbacks: Fees and reduced family involvement. |

| Business Succession | The Mellons ensured wealth transfer through structured succession planning. | Family Limited Partnerships; LLCs | Benefits: Maintains control and tax efficiency. Drawbacks: Requires formal governance and documentation. |

| Heir Education | The Rockefellers emphasized financial education, unlike the Vanderbilts. | Family governance frameworks; financial literacy programs | Benefits: Prepares heirs for wealth stewardship. Drawbacks: Time-intensive and requires family commitment. |

Preserving wealth isn’t just about accumulation – it’s about building a solid foundation with legal protections, diversification, professional management, and preparing future generations. These tools are just as relevant today, helping investors navigate challenges like lawsuits, market volatility, and the intricacies of passing wealth across generations.

Conclusion: Applying Historical Lessons to Protect Your Wealth

Safeguarding wealth requires careful planning, diversification, and professional oversight. Take the Rockefellers, for example. They managed to grow and protect a fortune of $8.4 billion across more than 70 heirs by leveraging tools like irrevocable trusts and professional trustees through Chase Bank. On the flip side, the Vanderbilts lost their massive fortune within just three generations, largely due to extravagant spending and a lack of structured planning.

These contrasting stories highlight a simple but powerful takeaway: families that succeed in preserving wealth treat it like a business. They use tools such as dynasty trusts, family constitutions, and controlled distributions to ensure longevity and stability.

"The family is both a potential threat and the greatest asset to its legacy." – Octavian Pilati

Modern investors can apply these same principles, along with updated legal strategies, to protect their assets. Combining irrevocable trusts with LLCs or incorporating offshore structures in jurisdictions like Nevis can provide robust defense against creditors, lawsuits, and high tax burdens. The key is to act now and establish multiple layers of protection.

Today’s experts offer customized solutions to fit a variety of asset types. Firms like Global Wealth Protection specialize in helping families implement these strategies, whether through private U.S. LLCs, offshore trusts, or comprehensive asset protection plans. Whether your focus is on safeguarding a family business, real estate, or investment portfolios, the lessons of the past remain a valuable guide for creating strong, modern wealth protection systems.

FAQs

When should I set up asset protection structures?

Asset protection structures are best set up during estate planning or when forming trusts. These structures help secure wealth for future generations by offering legal safeguards, tax advantages, and maintaining control over your assets. Starting this process early is essential to fully benefit from these protections and ensure financial stability, even in unpredictable circumstances.

Which is better for protection: an LLC or a trust?

Both LLCs and trusts offer distinct advantages when it comes to protecting assets, and the best choice depends on what you’re trying to achieve. A trust works well for long-term goals like preserving wealth, planning your estate, and bypassing probate. On the other hand, an LLC is highly effective for protecting specific assets – like a business or investment property – from lawsuits and creditors. In fact, many families use a combination of both strategies, such as transferring LLC ownership into a trust, to create a more complete and flexible protection plan.

Are offshore trusts legal for U.S. citizens?

Yes, offshore trusts are legal for U.S. citizens, provided they are set up and reported in full compliance with U.S. tax laws and regulations. It’s crucial to meet all reporting obligations and follow legal guidelines to avoid any penalties or legal issues.