Life insurance is more than just income replacement – it’s a powerful way to protect and transfer wealth. For high-net-worth individuals, it helps manage estate taxes, shields assets from creditors, and ensures liquidity for heirs to avoid forced asset sales. With estate tax exemptions dropping in 2026, now is the time to act.

Key Takeaways:

- Estate Taxes: Estates over $13.99M for individuals ($27.98M for couples) in 2025 face up to 40% federal tax. Life insurance provides liquidity to cover these costs.

- Tax-Free Benefits: Death benefits are income-tax-free and, when placed in an Irrevocable Life Insurance Trust (ILIT), excluded from taxable estates.

- Asset Protection: Policies in ILITs are safeguarded against creditors, lawsuits, and divorce settlements.

- Cash Value Growth: Permanent policies build tax-deferred cash value, accessible through loans or withdrawals.

- Business Succession: Life insurance funds buy-sell agreements, ensuring smooth ownership transitions.

Life insurance isn’t just about financial security – it’s a smart, flexible tool for managing taxes, protecting assets, and ensuring smooth wealth transfer. Start planning today to stay ahead of upcoming tax changes.

Types of Life Insurance Policies for Wealth Protection

Comparison of Life Insurance Policy Types for Wealth Protection

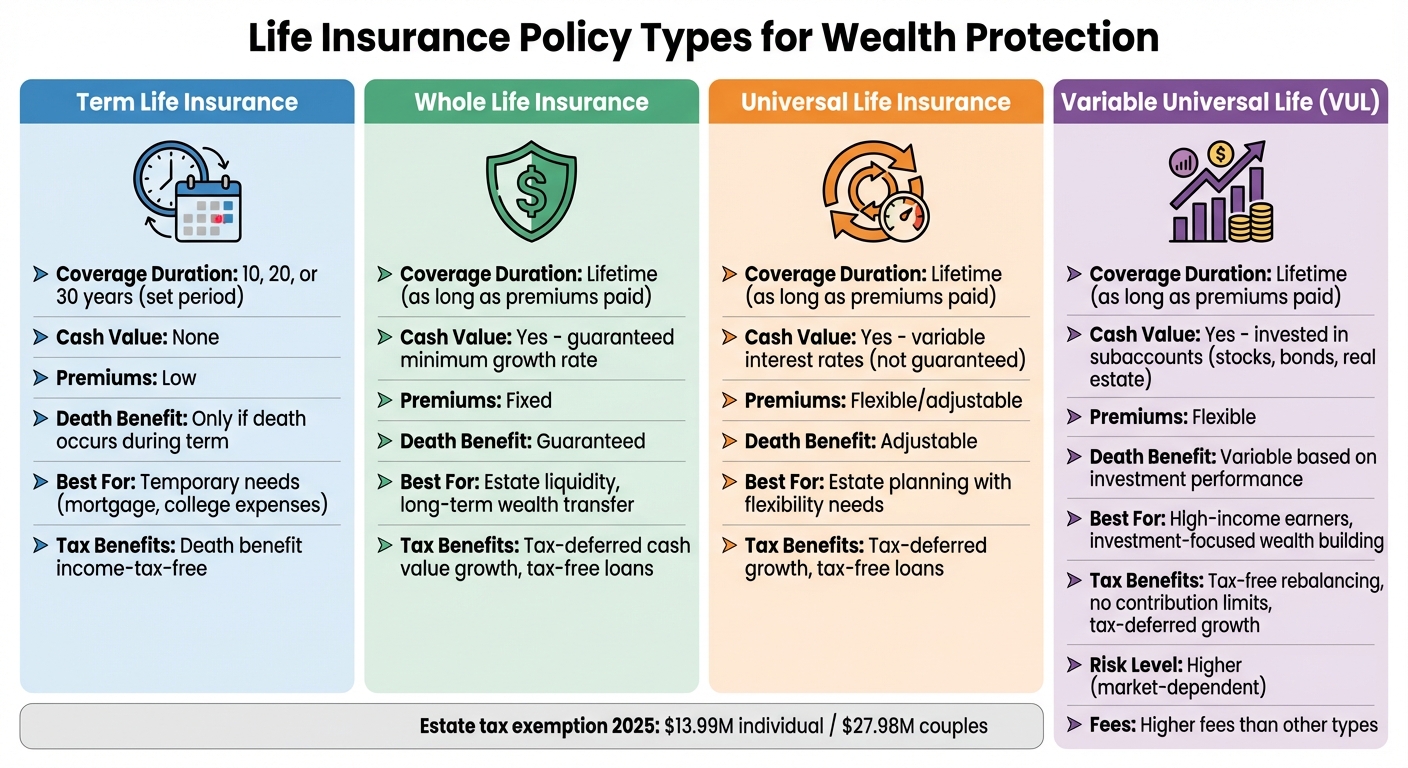

Term Life Insurance vs. Permanent Life Insurance

Term life insurance provides coverage for a set period – commonly 10, 20, or 30 years. If you pass away during the term, your beneficiaries receive the death benefit. If you outlive the policy, the coverage ends, and there’s no cash value or investment component. Because of this, premiums are relatively low, making term policies a budget-friendly option.

Permanent life insurance, which includes whole life and universal life policies, offers lifelong coverage as long as premiums are paid. Unlike term insurance, permanent policies build tax-deferred cash value over time . This cash value can be accessed through loans or withdrawals, providing a financial resource during your lifetime.

Term insurance is ideal for covering temporary financial responsibilities – like a mortgage or college expenses. On the other hand, permanent insurance is better suited for long-term goals, such as estate liquidity, business succession, or leaving a tax-free inheritance .

"A primary purpose of life insurance is to try to help ensure that your surviving loved ones… have their needs met when you are no longer earning income."

- Adam Frank, Managing Director, J.P. Morgan Wealth Management

Permanent life insurance also provides immediate liquidity when needed. To keep the death benefit out of your taxable estate, consider having the policy owned by an Irrevocable Life Insurance Trust (ILIT) .

In addition to lifelong coverage, permanent policies also build cash value – a feature explored further below.

Cash Value Life Insurance for Long-Term Growth

Permanent life insurance policies that accumulate cash value offer more than just a death benefit – they serve as a tax-advantaged savings tool. The cash value grows tax-deferred and can be accessed through tax-free loans or withdrawals up to the amount you’ve paid in premiums .

With whole life insurance, premiums are fixed, and the cash value grows at a guaranteed minimum rate. Universal life insurance, however, provides more flexibility, allowing you to adjust premiums and death benefits, though its interest rates are not guaranteed. Both types allow borrowing against the policy without triggering income tax, as long as the policy remains active.

This cash value feature can be especially useful for estate liquidity, helping to avoid the forced sale of family assets. For the 2025 tax year, estates exceeding $13.99 million for individuals or $27.98 million for married couples will be subject to federal estate taxes.

One strategy is to first maximize contributions to traditional retirement accounts like 401(k)s and IRAs. After that, cash value life insurance can serve as a secondary option for tax-advantaged growth. If you have an older, underperforming policy, a 1035 exchange allows you to transfer its cash value to a new policy with better terms without triggering immediate taxes.

Variable Universal Life Insurance for Investment Options

Variable Universal Life (VUL) insurance combines life coverage with investment opportunities. With a VUL policy, you can allocate the cash value into subaccounts that function similarly to mutual funds, investing in stocks, bonds, or real estate . This setup offers the potential for higher returns but comes with increased risk.

One major benefit of VUL is tax-free rebalancing, which lets you move assets between subaccounts without incurring capital gains taxes. This flexibility can make managing your portfolio more efficient. Additionally, VUL policies have no contribution limits or income restrictions, making them appealing to high-income earners who have already maxed out other retirement savings options.

However, VUL policies often come with various fees. If the policy’s cash value drops due to market losses or excessive loans, there’s a risk of the policy lapsing. In such cases, you may need to pay significant additional premiums to maintain coverage.

"Variable universal life insurance is only appropriate for individuals with specific life insurance protection needs. Substantial fees, expenses, and tax implications generally make variable life insurance unsuitable as a short-term savings vehicle."

For estate planning, VUL can provide immediate liquidity to cover estate taxes, avoiding the need to sell illiquid assets. By naming an Irrevocable Life Insurance Trust (ILIT) as the owner and beneficiary, you can also exclude the death benefit from your taxable estate. However, it’s essential to evaluate your risk tolerance, as VUL policies involve investment uncertainties .

This type of policy is a useful addition to wealth protection strategies, blending life insurance with flexible investment opportunities.

sbb-itb-39d39a6

US Life Insurance Strategies for Asset Protection

Creditor Protection for Life Insurance Benefits

In the United States, life insurance policies often provide a legal shield against creditors, but the level of protection depends heavily on state laws. These laws – not federal regulations – determine whether the cash value and death benefits of your policy are safeguarded from lawsuits, judgments, or bankruptcy claims.

States like Florida, Texas, Oklahoma, Montana, Nevada, and Delaware offer some of the strongest protections, allowing unlimited exemptions for cash value with few restrictions. However, under federal bankruptcy law, cash value protection is capped at $16,850 as of April 2025.

To qualify for creditor protection, most states require you to name a third-party beneficiary, such as a spouse, child, or dependent. If your estate is the beneficiary, these protections are typically voided. For even greater security, an Irrevocable Life Insurance Trust (ILIT) can be used. By placing the policy outside your personal estate, an ILIT shields it from creditors, regardless of state exemption rules.

"Life insurance isn’t just about protecting your family after you’re gone – it’s one of the most overlooked asset protection tools available today. When properly structured, it creates a financial fortress that creditors often cannot breach."

- Steven Gibbs, JD, AEP®, Estate Planning Attorney

Real-life cases highlight the power of these protections. In 2017, the Michigan case DC Mex Holdings LLC v. Affordable Land LLC saw debtor Dale Fuller successfully protect $73,078 in universal life cash value from a $2.5 million judgment. Similarly, OJ Simpson utilized Florida’s unlimited life insurance exemption to shelter millions from a $114 million civil judgment spanning from 1997 to 2024.

It’s worth noting that state exemptions don’t apply to IRS liens, child support, alimony, or fraudulent transfers. To be effective, asset protection strategies should be implemented well before any legal claims arise.

In addition to shielding assets from creditors, life insurance provides immediate liquidity, which can prevent the need for forced sales of other assets to cover taxes or debts.

Estate Liquidity and Tax Reduction

Life insurance serves another critical purpose: providing liquidity to settle estate taxes and preserve the value of your assets. Without sufficient cash on hand, heirs may be forced to sell family businesses, real estate, or other valuable but illiquid assets at a loss to pay estate taxes. For 2025, estates valued above $13.99 million for individuals or $27.98 million for married couples are subject to federal estate taxes of up to 40%. These taxes must be paid within nine months of death.

Life insurance can solve this problem by offering tax-free cash exactly when it’s needed most. Additionally, placing a policy within an ILIT removes the death benefit from the taxable estate. The trust can then use the payout to cover tax bills or purchase illiquid assets from the estate at fair market value, ensuring liquidity without triggering additional taxes. Keep in mind the three-year lookback rule: if you transfer an existing policy into an ILIT, you must live at least three years after the transfer for it to be excluded from your estate.

Survivorship (or second-to-die) policies are another effective tool. These policies cover two people, typically spouses, and pay out only after the second death – when estate taxes are due. They are often more affordable than individual policies and align perfectly with estate tax timing. For example, in 2022, an individual named Sarah used a $1 million joint-life annuity generating $43,843 annually to fund a $5.68 million second-to-die policy. This strategy turned $600,000 after-tax into a guaranteed $5.68 million tax-free inheritance.

Looking ahead, the current estate tax exemptions are set to decrease significantly after 2025 unless Congress intervenes. For high-net-worth families, acting now to secure today’s higher exemption levels and ensure future liquidity is more important than ever.

International and Offshore Life Insurance Strategies

Irrevocable Life Insurance Trusts (ILITs)

An Irrevocable Life Insurance Trust (ILIT) is a powerful tool for managing life insurance policies while keeping them outside your personal estate. By doing so, it removes the policy’s death benefit from federal estate taxes, which can climb as high as 40%. Additionally, both the cash value and the death benefit are shielded from creditors.

When you secure a policy through an ILIT from the start, you bypass the three-year lookback rule, which could otherwise pull the policy back into your taxable estate. The trust is typically funded through annual gifts that fall under the $19,000 exclusion limit (set for 2025) and require Crummey notices to qualify for the gift tax exemption.

"When a life insurance policy is held in an ILIT, ownership of the policy transfers from the insured individual to the trust. This feature enables the death benefit to move out of the estate and, eventually, to beneficiaries, tax-free."

- Trevor J. Hamilton, Director of Life Insurance Advisory, Bessemer Trust

One of the standout benefits of an ILIT is its ability to control distributions. Instead of giving beneficiaries a large lump sum, the trustee can release funds strategically – whether for education, a home purchase, or other specific needs. These distributions bypass probate, keeping the details of your estate private.

With the federal estate tax exemption set to drop from $13.99 million to around $6.4 million in 2026, establishing an ILIT now can help lock in the current, more favorable exemption levels. Once the domestic structure is in place, you can also explore offshore options for additional asset protection across borders.

Offshore Life Insurance Policies for Cross-Border Protection

For those with international ties, offshore life insurance policies offer an extra layer of protection. These policies are based in jurisdictions with tax-neutral frameworks and strong legal safeguards, such as the Cayman Islands, Bermuda, and Jersey. These locations typically impose no inheritance or estate taxes, allowing wealth to pass to heirs without local tax erosion.

Offshore policies also sidestep foreign forced heirship laws, giving you more control over how your assets are distributed, regardless of local legal mandates. Many of these jurisdictions do not recognize foreign court judgments, providing an additional shield against creditor claims or litigation.

For individuals with cross-border lives – like non-domiciled residents in the UK – offshore "excluded property trusts" can help protect foreign assets from local inheritance taxes, even if tax residency changes in the future. However, modern offshore planning must comply with global transparency standards. Regulations like the Common Reporting Standard (CRS) and the Foreign Account Tax Compliance Act (FATCA), along with economic substance laws in places like the British Virgin Islands and Cayman Islands, require entities to demonstrate genuine local activity.

Domestic vs. Offshore Life Insurance Structures

The decision between domestic and offshore life insurance structures depends on your specific goals, where you reside, and how much complexity you’re willing to manage.

| Feature | Domestic ILIT (U.S.) | Offshore Life Insurance Trust |

|---|---|---|

| Tax Efficiency | Removes federal and state estate taxes on death benefits; earnings subject to U.S. tax | Often tax-neutral; avoids local inheritance/estate taxes |

| Creditor Protection | Varies by state and subject to U.S. court orders | Generally stronger, with protection against foreign claims |

| Setup Complexity | Moderate – involves legal drafting and Crummey notices | High – requires compliance with international regulations (FATCA, CRS, etc.) |

| Privacy | Limited by domestic discovery and probate records (if not in trust) | Higher confidentiality, though subject to international transparency laws |

Domestic ILITs work well for U.S.-based families aiming to reduce estate taxes and protect assets from domestic creditors. They are relatively straightforward to set up and maintain with the guidance of an experienced attorney.

Offshore structures, however, are better suited for multinational families or high-net-worth individuals who need to navigate foreign legal systems, address forced heirship concerns, or counter aggressive creditor actions. While these structures offer enhanced protection, they come with higher costs, stricter compliance requirements, and the need for independent trustees to ensure the trust isn’t viewed as an extension of the grantor.

Advanced Life Insurance Tactics for Business and Tax Optimization

Building on earlier strategies for protecting assets, these advanced approaches focus on streamlining business transitions and improving tax efficiency.

Funding Buy-Sell Agreements with Life Insurance

When a business partner or co-owner passes away, life insurance can provide the immediate funds needed to buy out the deceased partner’s share. This ensures the business continues operating smoothly while also fairly compensating the late partner’s family.

Two common structures are used to fund these agreements. The entity redemption structure involves the business owning life insurance policies on each partner. When a partner passes away, the business uses the death benefit to purchase and retire the deceased partner’s shares. However, after a 2024 Supreme Court ruling that impacted this approach, many business owners have shifted to cross-purchase agreements. In this setup, individual partners take out policies on each other, and the surviving partners use the proceeds to buy out the deceased partner’s shares. This method often provides a tax step-up in basis, reducing potential capital gains taxes. However, it does require multiple policies to cover all ownership combinations.

"The life insurance that funds your buy-sell agreement will create a sum of money at your death that will be used to pay your family or your estate the full value of your ownership interest."

For business owners with buy-sell agreements established before 2024, it’s crucial to review these arrangements with legal counsel to avoid unexpected estate tax consequences. Including a clear valuation method or scheduling regular appraisals can also help prevent disputes with the IRS. Additionally, businesses applying for SBA loans should note that life insurance is commonly required to cover outstanding debts in the event of an owner’s death.

These strategies often serve as a foundation for more advanced solutions, such as Corporate-Owned Life Insurance (COLI), which can offer additional tax benefits.

Corporate-Owned Life Insurance (COLI) for Tax Savings

Corporate-Owned Life Insurance (COLI) is a tool businesses use to build tax-advantaged reserves while safeguarding against the financial risks of losing a key individual. The cash value within a COLI policy grows tax-deferred, and the death benefit is paid out income-tax-free upon the insured’s passing. Businesses can also borrow against the policy’s cash value to fund operations, provide executive benefits, or facilitate buyouts.

A key benefit of COLI is that the policy’s value is typically excluded from the insured individual’s personal estate, helping to reduce estate tax liabilities. Businesses often use COLI to fund buy-sell agreements or as key person insurance, which can cover the costs of recruiting and training a replacement.

"Life insurance owned by a business on an individual owner or key person generally isn’t includible in the insured’s estate."

- Vernon W. Holleman, President, The Holleman Companies

While premiums are generally not deductible when the business is the beneficiary, some exceptions exist if the insurance is part of a formal employee benefit plan.

Beyond corporate strategies, high-net-worth individuals can also use permanent life insurance for personal tax planning.

Tax-Exempt Life Insurance Policies for Investment Optimization

For individuals who have already maximized their 401(k) or IRA contributions, permanent life insurance policies, such as Variable Universal Life (VUL), offer an additional way to achieve tax-advantaged growth. These policies allow for tax-deferred investment growth across a range of options, and policyholders can access the cash value through non-taxable loans, creating a supplemental income stream for retirement.

For those with older policies, a 1035 exchange provides a tax-free way to transfer cash value into a new policy, potentially unlocking improved benefits or more attractive investment options. When these policies are structured within an Irrevocable Life Insurance Trust (ILIT), the death benefit is excluded from the taxable estate. This can provide tax-free liquidity to cover estate taxes, which can reach as high as 40%, without forcing heirs to sell off illiquid assets.

"Permanent life insurance is one of the most powerful tax planning tools you can find. It offers several unique ways to address your estate tax and income tax liabilities both while you’re alive and for your heirs after you pass away."

Conclusion

The strategies discussed emphasize the critical role life insurance plays in protecting wealth. It serves as a key financial safeguard, offering tax-free liquidity to cover hefty estate taxes. This prevents heirs from having to sell off family businesses, real estate, or other valuable but illiquid assets at less-than-ideal prices.

Additionally, Irrevocable Life Insurance Trusts (ILITs) can exclude death benefits from taxable estates, while the cash value growth within permanent policies allows for tax-deferred savings. This growth can be used to supplement retirement income or address business needs. For business owners, life insurance also facilitates smoother transitions when passing down or selling a company.

"Life insurance is an incredibly powerful tool for wealth transfer. It is tax efficient, can be guaranteed, and helps clients create certainty that their goals for their estate are realized."

- John A. O’Brien, Vice President, Senior High Net Worth Insurance Specialist, Fifth Third Bank

To make life insurance a part of your wealth protection plan, start by assessing your estate’s tax exposure and liquidity requirements. Work with an estate attorney and tax advisor to determine the right coverage and establish an ILIT if necessary. Keep in mind the three-year lookback rule for policy transfers. A proactive approach ensures your plan stays aligned with changing tax laws and personal circumstances.

Starting early can secure lower premiums and allow time for cash value to build. Regularly review your strategy, especially after significant life events, to keep it on track.

FAQs

How can life insurance help with estate taxes?

Life insurance plays a key role in addressing estate taxes, offering a way to cover tax liabilities and other costs that arise after passing. This ensures your loved ones won’t need to sell off assets or face financial pressure, helping to maintain the overall value of your estate.

For individuals with significant wealth, life insurance policies – often placed in irrevocable trusts – can provide a death benefit that is typically exempt from both income and estate taxes. This allows your beneficiaries to receive the full payout, making the process of transferring wealth much smoother and more efficient.

Including life insurance in your estate plan can help reduce tax burdens, safeguard your legacy, and provide lasting financial stability for your family.

What are the advantages of using an Irrevocable Life Insurance Trust (ILIT) for wealth protection?

An Irrevocable Life Insurance Trust (ILIT) can play a crucial role in protecting wealth and planning your estate. By placing a life insurance policy within an ILIT, the death benefit is kept out of the insured’s estate. This can significantly reduce or even eliminate federal and state estate taxes, ensuring more of your wealth reaches your beneficiaries.

ILITs also offer asset protection by transferring control of the funds to a trustee. This setup shields the assets from creditors and helps prevent potential mismanagement by beneficiaries. Plus, you can establish clear terms for how and when distributions are made, giving you peace of mind that your legacy will be managed exactly as you intend.

Another major benefit is the liquidity ILITs provide. They can help cover estate taxes or other expenses, sparing heirs from the burden of selling valuable assets to cover those costs. For individuals with substantial wealth, ILITs are a strategic way to transfer assets efficiently, minimize tax burdens, and safeguard wealth for future generations.

How does life insurance support business succession planning?

Life insurance plays a key role in making business succession planning smoother and less stressful. It ensures there’s money available to handle critical expenses like estate taxes, outstanding debts, or even buying out heirs. This can prevent the need to sell off business assets or disrupt daily operations.

When the policy is set up through a trust or owned by the business itself, it can also shield the payout from estate taxes or creditors. This not only safeguards the value of the business for future generations but also provides financial stability for surviving partners or heirs. In essence, life insurance serves as a practical way to protect your business and legacy while reducing potential financial challenges.