When it comes to protecting your assets offshore, offshore trusts and offshore foundations are two popular options. Both offer strong safeguards against lawsuits, creditors, and other risks, but they work differently. Here’s a quick breakdown to help you decide:

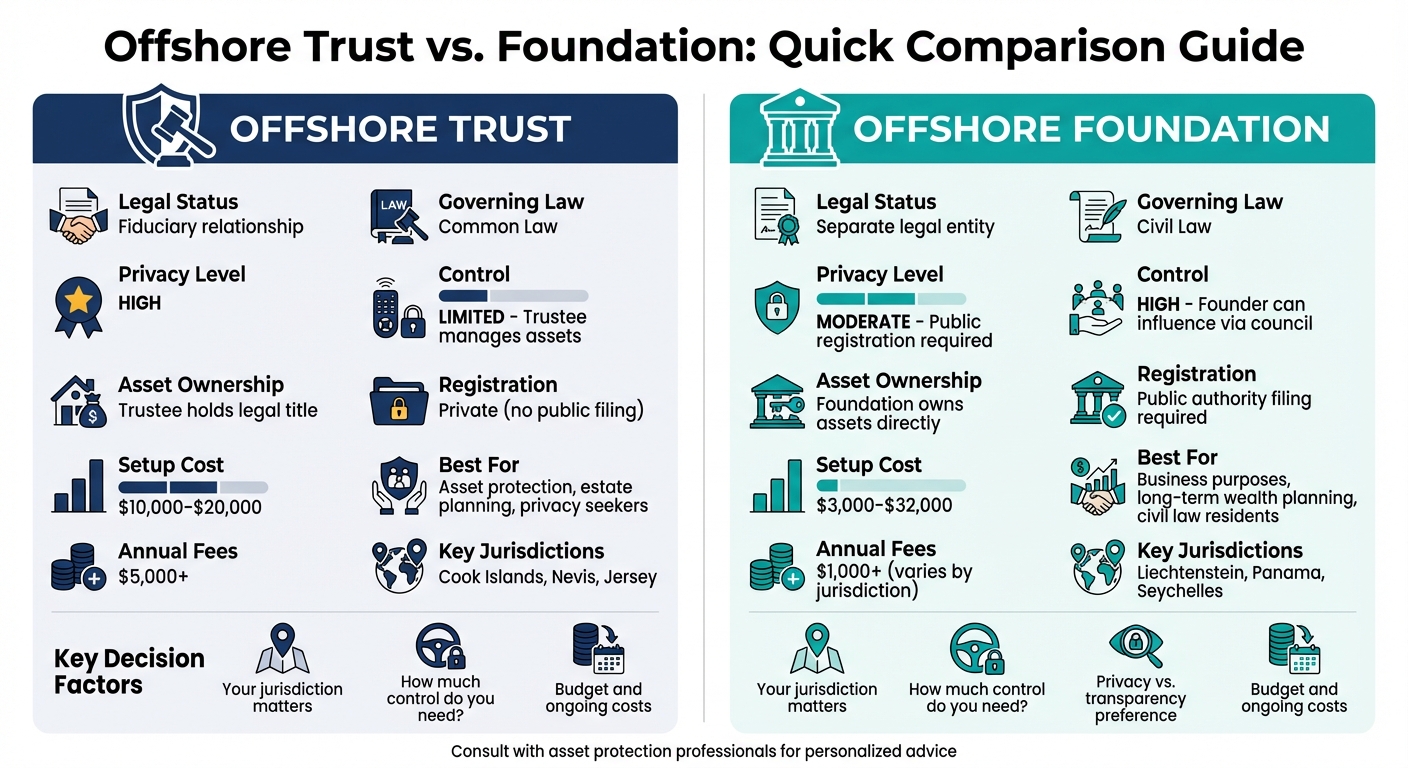

- Offshore Trusts: A legal relationship where a trustee manages assets for beneficiaries. Often used in common law jurisdictions like the Cook Islands, trusts provide strong privacy, flexible estate planning, and protection from lawsuits. However, the settlor must give up direct control of the assets.

- Offshore Foundations: An independent legal entity that owns assets. Common in civil law jurisdictions like Liechtenstein and Panama, foundations allow founders to retain some control through a council or protector. They’re ideal for business purposes or long-term wealth planning but require public registration.

Quick Comparison

| Feature | Offshore Trust | Offshore Foundation |

|---|---|---|

| Legal Status | Fiduciary relationship | Separate legal entity |

| Governing Law | Common Law | Civil Law |

| Privacy | High | Moderate (public registration) |

| Control | Limited (trustee manages assets) | High (founder can influence) |

| Setup Cost | ~$10,000–$20,000 | ~$3,000–$32,000 |

| Best For | Asset protection, estate planning | Business, long-term wealth |

Key Takeaway

Choose a trust if you prioritize privacy and asset protection in common law jurisdictions. Opt for a foundation if you want more control and operate in civil law environments. Always consult a professional to ensure compliance with local laws and tax regulations.

Offshore Trust vs Foundation Comparison Chart

What Are Offshore Trusts?

How Offshore Trusts Are Structured

An offshore trust operates through a three-party relationship involving the settlor, trustee, and beneficiaries. As the settlor, you establish the trust by transferring your assets to a trustee, which could be an individual or a corporate entity. The trustee then manages these assets on behalf of the beneficiaries.

The key to this structure is the division of ownership. The trustee holds the legal title to the assets, while the beneficiaries have the equitable interest, meaning they benefit from the trust. The Trust Deed, a formal document, outlines the trust’s rules – how it functions, when distributions are made, and the scope of the trustee’s authority. Many offshore trusts also include a Protector, an additional party who monitors the trustee’s actions and can replace them if needed to ensure your wishes are upheld.

For an offshore trust to be legally valid, it must meet the "three certainties": certainty of intention (a clear intent to create the trust), certainty of subject matter (clearly defined assets), and certainty of objects (identifiable beneficiaries). This structured framework is the foundation of the trust’s strong asset protection, which we’ll explore in the next section.

Main Benefits of Offshore Trusts

Offshore trusts are a powerful tool for safeguarding your wealth, thanks to the legal protections offered by certain foreign jurisdictions. For example, in Nevis, creditors must post a $100,000 bond before pursuing a lawsuit against a trust. Similarly, the Cook Islands enforce strict statutes of limitations – creditors only have one to two years to claim fraudulent conveyance, making challenges to asset transfers extremely difficult.

Another major advantage is privacy. Offshore trust deeds are typically not part of the public record, allowing you to keep your financial matters confidential. They also streamline estate planning by enabling you to pass wealth to your heirs privately, avoiding the delays, costs, and public exposure that come with probate. In places like Jersey, where the rule against perpetuities has been abolished, trusts can even exist indefinitely, preserving wealth for future generations.

Additionally, many offshore jurisdictions are tax-neutral. While you must adhere to U.S. tax laws, these jurisdictions do not impose local income, capital gains, or estate taxes on trust assets. This setup can provide flexibility in distributing income, potentially helping you manage your overall tax obligations more efficiently.

sbb-itb-39d39a6

What Are Offshore Foundations?

How Offshore Foundations Are Structured

An offshore foundation is a legal entity with the ability to own assets, enter contracts, and even participate in legal proceedings. This concept stems from civil law systems in places like Liechtenstein and Panama, in contrast to trusts, which originate from English common law traditions.

The structure of an offshore foundation typically involves four key roles:

- Founder: The person or entity that establishes the foundation and sets its goals.

- Foundation Council: Similar to a board of directors, this group manages the foundation’s assets and ensures it operates according to its Charter.

- Protector: An optional role, the Protector oversees council activities and appointments.

- Beneficiaries: These are the individuals or organizations that benefit from the foundation. However, unlike trusts, a foundation doesn’t always need beneficiaries – it can exist solely for a specific purpose, such as charitable work.

The foundation operates under two main governing documents. The Charter, which is public, outlines the foundation’s purpose and structure. Meanwhile, the Regulations are private and detail management processes and how benefits are distributed. For instance, in Panama, while the Charter is publicly accessible, the Regulations and the list of beneficiaries remain confidential.

This clearly defined structure is what gives offshore foundations their unique functionality and appeal.

Main Benefits of Offshore Foundations

Offshore foundations offer several advantages, thanks to their independent legal structure. By owning assets directly, the foundation creates a strong separation between personal liabilities and the foundation’s holdings. Unlike trusts, where a trustee owns the assets, the foundation itself is the legal owner. This makes it an effective tool for holding intellectual property, managing charitable projects, or creating a transparent, self-contained entity for international dealings.

These foundations can also be perpetual, making them ideal for protecting assets across multiple generations. Liechtenstein was the first to introduce this model in 1926, and today, jurisdictions like Panama offer cost-effective options. Setting up a foundation in Panama typically costs between $3,000 and $6,000, with annual maintenance fees around $1,000.

Another benefit is the balance of control and independence. Founders can influence the foundation’s operations by appointing council members or a Protector, while the foundation itself remains legally independent. Proper governance, including formal meeting records and resolutions, ensures compliance with regulatory standards. However, to maintain the foundation’s legitimacy, it’s crucial for founders to avoid acting as unofficial managers and to appoint independent council members.

This blend of asset protection, flexibility, and structured governance makes offshore foundations a practical choice for many individuals and organizations.

Offshore Trusts vs. Foundations: Main Differences

Offshore trusts and foundations handle asset protection in fundamentally different ways, thanks to their unique legal structures. Knowing these differences can help you decide which option aligns with your goals.

A trust is essentially a fiduciary arrangement involving the settlor, trustee, and beneficiaries. On the other hand, a foundation operates as an independent legal entity, much like a corporation. As John Goldsworth puts it:

"A private foundation is an independent self-governing legal entity, set up and registered or recorded by an official body… in order to hold an endowment… for a particular purpose for the benefit of beneficiaries."

This distinction affects ownership. In a trust, the trustee holds the legal title to assets, while beneficiaries have an equitable interest. Foundations, however, own assets outright as a legal entity, completely separating them from the founder’s personal ownership. In places like the Seychelles, laws explicitly confirm that a foundation is both the legal and beneficial owner of its assets.

These ownership rules also impact management and legal responsibilities. In a trust, the trustee manages assets for the benefit of the beneficiaries. Foundations, however, are governed by a foundation council, which acts to fulfill the foundation’s purpose. Beneficiaries of a foundation usually have limited or no legal rights unless the foundation’s charter explicitly grants them.

Privacy and registration requirements also differ. Trust deeds are typically private and don’t require public filing. Foundation charters, however, must be registered with a public authority in the jurisdiction where the foundation is established. While some details, like beneficiary lists, may remain private, this registration process helps establish the foundation’s legitimacy, reducing the risk of it being deemed a "sham" due to excessive control by the founder.

To make these differences clearer, here’s a comparison table:

Comparison Table: Trusts vs. Foundations

| Feature | Offshore Trust | Offshore Foundation |

|---|---|---|

| Legal Status | Fiduciary relationship (not an entity) | Separate legal entity |

| Governing Law | Common Law | Civil Law |

| Creation Document | Trust Deed | Foundation Charter |

| Management | Trustee | Foundation Council |

| Asset Ownership | Trustee holds legal title | The foundation itself owns assets |

| Registration | Typically private | Registered with a public authority |

| Fiduciary Duty | Owed to beneficiaries | Owed to the foundation and its purpose |

| Risk of Sham | Higher if settlor retains too much control | Lower; formal incorporation confirms existence |

| Beneficiaries | Required | Optional (can be purpose-driven) |

| Setup Cost | ~$10,000 (e.g., Cook Islands) | ~$32,000 (e.g., Liechtenstein) |

Pros and Cons: What Each Option Offers

Shared Benefits and Different Strengths

Offshore trusts and foundations both provide strong asset protection, shielding against lawsuits, divorce claims, and creditors. They also simplify probate and support international tax strategies. The choice between the two depends on your specific goals and circumstances.

While both structures share these advantages, they differ in key aspects. Trusts are known for their privacy and ability to engage in direct commercial activities. For example, a trust can buy property, sign contracts, or invest in mutual funds without needing to establish additional corporate entities. Trusts also benefit from centuries of established case law in common law jurisdictions, offering predictable legal outcomes.

On the other hand, foundations are better suited for civil law jurisdictions. Their corporate-like structure simplifies banking processes, as financial institutions often prefer dealing with a separate legal entity over a fiduciary arrangement. Foundations also allow founders to maintain more control. As Steven James puts it:

The core idea of a trust is that you give up any ownership and control of your assets so that they can be managed for your benefit without you having to retain ownership.

With foundations, founders can serve on the council or appoint protectors to retain influence.

However, there are trade-offs. Trusts carry a risk of being labeled a "sham" if the settlor retains too much control, whereas foundations avoid this issue due to their incorporated status. Foundations, however, cannot directly engage in commercial operations without creating an underlying LLC or IBC. In terms of cost, trusts are generally more affordable – about $10,000 for a Cook Islands trust compared to $32,000 for a Liechtenstein foundation. Foundations, though, offer greater statutory clarity.

To help you weigh your options, here’s a side-by-side comparison of their benefits and drawbacks.

Comparison Table: Advantages and Disadvantages

| Feature | Offshore Trust | Offshore Foundation |

|---|---|---|

| Privacy Level | High; no public registration required | Moderate; charter filed with public authority |

| Commercial Use | Permitted directly for business operations | Restricted; requires underlying company |

| Founder Control | Limited to avoid "sham" designation | High; founder can serve on council |

| Banking Ease | More difficult due to fiduciary nature | Easier with separate legal entity status |

| Legal Certainty | Extensive case law (centuries old) | Statutory certainty but less tested |

| Setup Cost | Lower (~$10,000) | Higher (~$32,000) |

| Best For | Common law residents, business operations | Civil law residents, long-term wealth planning |

| "Sham" Risk | Higher if settlor retains control | Lower due to incorporated status |

| Beneficiary Rights | Enforceable equitable rights | Limited or no legal rights |

How to Choose Between a Trust and Foundation

What to Consider Before Deciding

Start by evaluating your jurisdiction – this plays a big role in determining the better option. Civil law countries like France, Spain, or Germany typically recognize foundations more readily, especially when dealing with forced-heirship rules. On the other hand, common law jurisdictions such as the United States or United Kingdom have a long history of trust law, offering more predictable outcomes due to established case precedents.

If maintaining some level of control is important to you, a foundation allows you to be part of the council or appoint a protector. For those prioritizing protection against lawsuits, trusts in jurisdictions like the Cook Islands or Nevis are worth considering. These locations have strong asset protection laws – Nevis, for example, requires creditors to post a US$25,000 bond to challenge a trust.

Foundations also appeal to entrepreneurs and crypto investors because their corporate-style governance often aligns better with banking compliance requirements.

For U.S. individuals, tax compliance is a critical factor. Foreign trusts involve annual IRS reporting through Forms 3520 and 3520-A. Foundations, depending on their structure, may be treated as either trusts or corporations for tax purposes. Nonresident individuals should also be aware of the low US$60,000 estate tax filing threshold on U.S.-based assets, making proper structuring essential.

Costs are another important consideration. Setting up a Cook Islands trust typically costs between US$10,000 and US$20,000, with annual fees exceeding US$5,000. A Panama foundation, by comparison, costs US$3,000 to US$6,000 upfront, with annual fees around US$1,000. Liechtenstein foundations are more expensive, requiring approximately €30,000 to establish.

Given these complexities, seeking professional advice is key to making an informed choice.

Working with Experts for Custom Solutions

After identifying your priorities, consulting with experts is crucial. Factors like litigation risks, residency, tax obligations, and long-term goals all require careful consideration. As Steven James, an Offshore Structures Researcher, aptly states:

"Good governance isn’t decoration; it’s the legal oxygen that keeps the structure alive."

Professionals can help you design a structure with independent trustees or council members, ensure proper governance, and maintain clear separation between personal and entity finances. Without these safeguards, tax authorities or creditors could challenge the legal protections of your trust or foundation.

Global Wealth Protection, for instance, specializes in helping entrepreneurs and high-net-worth individuals navigate these decisions. Whether you need an offshore trust, a private interest foundation, or a combination of both, expert advice can help you stay compliant while protecting your assets effectively.

Conclusion

Main Points to Remember

Picking the right structure depends on your specific needs and circumstances. Both offshore trusts and foundations are effective tools for asset protection, but they come with different features and benefits.

Trusts are a strong choice in common law jurisdictions, offering time-tested protection through established case law. They are ideal for those who value privacy, reliable legal defenses, and a straightforward way to transfer wealth. However, using a trust means giving up direct control, as a trustee will manage the assets on behalf of your beneficiaries.

On the other hand, foundations provide an opportunity to retain some influence. As independent legal entities, they are particularly useful for individuals from civil law systems or those who need a corporate-like structure for business purposes. Foundations allow for governance through a council, but one drawback is that their charters are typically registered publicly, though the identities of beneficiaries often remain private.

Ultimately, aligning the structure with your jurisdiction, goals, tax obligations, and budget is essential. Effective governance is critical to safeguarding your assets. Whether you go with offshore trusts and foundations, or even a combination of both, proper setup and ongoing compliance are crucial to maintaining the protections these structures offer.

Collaborating with skilled professionals can help you navigate the complexities of international asset protection, meet U.S. tax reporting requirements, and avoid costly mistakes. Tailoring your approach to your unique situation ensures your asset protection strategy is both effective and compliant.

FAQs

Can I change trustees or council members later?

Yes, you can usually replace trustees or council members later on. Offshore trusts and foundations are built to offer flexibility in how they’re managed. For instance, offshore foundations allow founders to update or appoint new council members as needed. Similarly, offshore trusts often include clauses in the trust deed that outline how to replace trustees or appoint successors, depending on the specific jurisdiction and setup. This makes it easier to adjust to changing circumstances or legal requirements.

How do IRS reporting rules differ for trusts vs. foundations?

When it comes to IRS reporting rules, trusts and foundations each have their own specific guidelines to follow. For trusts, the focus is on income reporting, taxation of beneficiaries, and disclosures related to foreign ownership. This often involves filing forms like 3520-A, which ensures proper reporting of foreign trust activities.

Foundations, particularly charitable ones, face different requirements. They must adhere to rules surrounding their charitable activities, minimum distribution obligations, and taxes on any income that remains undistributed. These organizations use forms specifically designed for these purposes to ensure compliance.

While both trusts and foundations have distinct reporting obligations, their rules are crafted to align with their unique legal and tax-related goals.

What mistakes can make a trust or foundation invalid?

A trust or foundation might be declared invalid if it’s considered a sham or if it fails to meet essential elements like a clear intent to establish it, adherence to proper legal formalities, or if it includes mechanisms allowing excessive control by its creator. These shortcomings can result in legal challenges or even the trust’s invalidation. To steer clear of such risks, it’s crucial to comply with all legal requirements.