Did you know that 70% of family wealth disappears by the second generation, and 90% by the third? The main reason: heirs aren’t prepared to manage their inheritance. Without proper guidance, even the most carefully built fortune can vanish due to poor decisions, taxes, or financial mismanagement.

Here’s the solution: Start early. Teaching kids about money – saving, budgeting, investing, and protecting wealth – can transform them into responsible stewards of your legacy. This means:

- Start financial education early: Kids as young as 7 can learn the basics of saving and spending.

- Use age-appropriate lessons: From "spend, save, give" jars for young kids to investment accounts for teens, hands-on experience is key.

- Talk openly about money: Family discussions can demystify wealth and reinforce values.

- Introduce tools like trusts: Explain how structures like trusts safeguard assets and ensure responsible use over time.

- Involve financial professionals: Schedule a private consultation to Let children meet your advisors to build confidence and knowledge.

Developing the Right Attitude Toward Money and Wealth

Before children can effectively protect wealth, often through offshore asset protection strategies, they need to understand its purpose. Money doesn’t create character; it amplifies it. If children believe wealth guarantees happiness, they might misuse it, no matter how strong the legal protections. The real foundation for safeguarding wealth lies in the values and attitudes children develop long before they inherit anything.

By the age of 7, kids already have a basic understanding of financial habits – how to save, spend, and even their sense of entitlement. The goal is to guide them away from seeing wealth as a guarantee and instead view it as a responsibility. Teach them that money is a tool for creating purpose, building a legacy, and contributing to others, rather than just a means for personal consumption.

"Money magnifies character. If we want our children to be wise stewards, we must nurture wisdom first." – Holdun

Developing the right mindset starts with fostering emotional intelligence. Encourage gratitude, empathy, and resilience – qualities that counteract entitlement or dependency. By seeing money as a tool for both personal growth and positive impact, children can grow into responsible stewards of their family’s wealth.

Using Family Discussions to Teach Money Values

Talking openly about money helps remove the mystery around wealth. Yet, 82% of parents admit they avoid financial conversations with their kids because of fear. This silence can leave children unprepared. The solution isn’t to overwhelm them with details about your net worth but to introduce age-appropriate discussions that align with your family’s values.

A helpful starting point is creating a Family Values Charter. This document outlines your family’s mission and principles regarding wealth, emphasizing beliefs about earning, saving, and giving. It serves as a guide for future decisions, helping children connect financial choices to a broader sense of purpose.

Everyday moments can be great teaching opportunities. For example, involve your kids in discussions about paying bills, grocery shopping, or planning a major purchase. Explain why you’re saving for a family vacation instead of making an impulsive buy. Monthly family money meetings can also be a great way to review expenses, discuss charitable giving, or plan for upcoming costs. Explaining the reasoning behind financial structures – like why a property is held in a trust – helps reinforce values beyond just numbers.

One inspiring example comes from a family documented by RBC Wealth Management in 2025. They created "Grandma’s Foundation", where grandchildren joined the board starting at age seven. These kids attended meetings, reviewed investments, and presented grant proposals for how foundation funds should be used. This hands-on experience turned abstract ideas like fiduciary responsibility into real-world lessons, preparing them to manage wealth responsibly.

Building on these discussions, giving children practical financial tasks helps them apply what they’ve learned.

Giving Children Hands-On Financial Experience

To truly understand money, kids need real-life experience with it. Start by assigning small, age-appropriate financial responsibilities, allowing them to make decisions and learn from their outcomes.

For younger children (ages 3–6), the Three-Jar System works well. Label three jars as "Spend", "Save", and "Give", and help your child divide any money they receive – whether from an allowance, gifts, or small jobs – into these jars. This makes the different purposes of money more tangible.

As kids get older, introduce an effort-based allowance. Instead of paying for basic chores, reward them for tasks that add extra value, like washing the car or organizing a room. This approach connects effort with reward.

For children aged 7–12, let them take on real budgeting tasks. For instance, they could plan a budget for a family outing or manage a holiday gift exchange. By researching costs and making decisions, they’ll learn about trade-offs and the consequences of financial choices.

Teenagers (13–18) can handle more advanced responsibilities. Consider opening a youth investment account and encouraging them to track a stock or participate in family foundation discussions. These activities help them build confidence as they prepare for larger financial responsibilities.

Here’s a breakdown of how financial responsibilities can evolve with age:

| Age Group | Focus Area | Practical Action |

|---|---|---|

| 3–6 | Foundations | "Spend, Save, Give" jars; pretend market |

| 7–12 | Earning & Saving | Weekly allowance tied to chores; short-term saving goals |

| 13–18 | Real-World Skills | Investment accounts; digital budgets; philanthropy participation |

| 18–25 | Stewardship | Annual financial check-ins; family governance participation |

Throughout this process, aim for a balance of independence and guidance. Let children make their own financial decisions and learn from manageable mistakes. Experiencing setbacks early prepares them to handle more significant challenges later.

Lastly, introduce your kids to your "financial village" – the professionals who help manage your family’s wealth, such as financial advisors, attorneys, or CPAs. These introductions not only demystify wealth management but also ensure your children know where to turn for advice when needed. The goal isn’t to make them financial experts but to equip them with the core principles and understanding they’ll need to manage wealth responsibly. Up next, we’ll explore how to adapt money skills to different stages of development.

sbb-itb-39d39a6

Teaching Money Skills at Different Ages

Age-Appropriate Financial Education Guide for Children

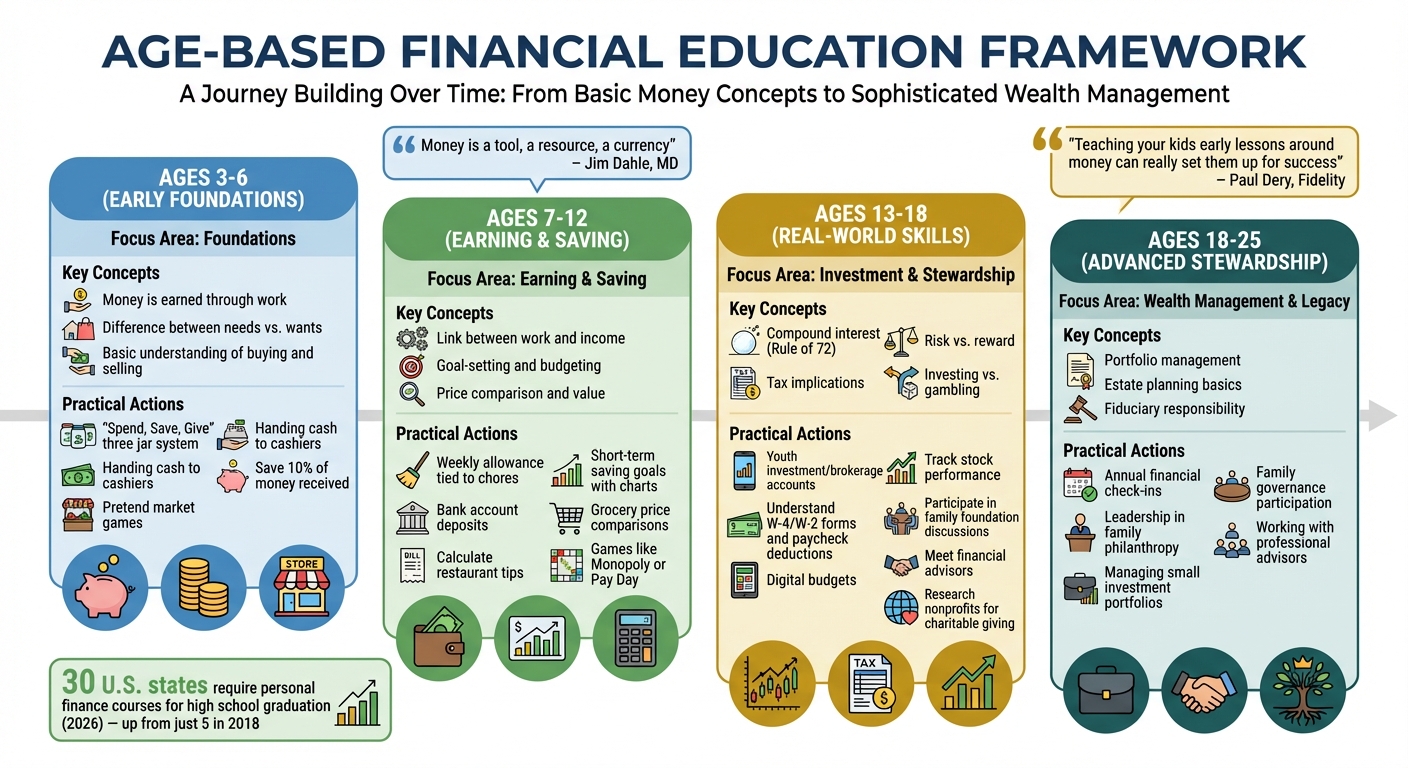

A solid financial education from a young age is key to preserving family wealth and helping heirs become responsible stewards, rather than passive recipients. Kids grasp financial concepts at their own pace, so it’s important to align lessons with their developmental stage. As of February 2026, 30 U.S. states require students to complete a personal finance course to graduate high school – up from just five in 2018. This growing emphasis highlights the importance of starting early. Here’s how to tailor financial lessons for different age groups.

Teaching Basic Money Concepts to Young Children

Even children as young as 3 can begin to understand simple financial ideas like buying and selling. At this stage, the goal isn’t to dive into complex topics like interest rates or taxes but to establish a basic understanding of money’s role in everyday life. Focus on these key points:

- Money is earned through work – it doesn’t appear magically.

- Needs (like food and clothing) are different from wants (like toys or candy), and waiting to buy something can make it feel more rewarding.

"An effective way to teach money is to start small and build over time. Early experiences, like saving part of a birthday gift or choosing between two treats, lay the foundation for more advanced concepts as they grow." – Citi

Simple activities can make these lessons stick. Let kids hand cash to a cashier to help them see money as a practical tool. Play a game where they decide if an item – like milk or a candy bar – is a need or a want. You can also introduce a habit of saving by setting aside 10% of any money they receive.

"Money is a tool, a resource, a currency. It’s not dramatically different from time, food, energy, and other resources in your life." – Jim Dahle, MD, Founder, The White Coat Investor

Experts suggest starting with physical money, like coins and bills, before moving to digital concepts. The tactile experience helps young children grasp the value of spending.

Teaching Budgeting and Saving to School-Age Children

By the time kids are 7–12 years old, they’re ready for more structured financial lessons. This is the perfect time to introduce budgeting, goal-setting, and the link between work and income. Allowances or payments for chores can help them see that money isn’t free – it’s earned.

Encourage goal-setting by having them write down what they want to save for, whether it’s a toy, bike, or game, and attach a price to it. A savings chart can help them visually track their progress. During grocery trips, challenge them to compare prices and find the best value among brands or package sizes.

"You may find that kids make different choices with their own hard-earned money than they would with someone else’s." – Chris Kawashima, Financial Planner, Charles Schwab

To introduce digital literacy, take them to a bank to deposit their allowance and explain how account balances work. Show them how ATMs operate, emphasizing that the money comes from deposits, not a magical source. Teach them about ATM fees and PIN security. You can also make math practical by having them calculate tips at restaurants, reinforcing percentage skills and the concept of service-based income.

Games like Monopoly or Pay Day can make budgeting fun while teaching real-world skills. To encourage saving, consider a matching program where you contribute an extra 50 cents for every dollar they save. As they grow, you can start introducing them to the basics of investing.

Teaching Investment Basics to Teenagers

Teenagers (13–18 years old) are ready to move beyond saving and budgeting into the world of investing. This is the time to explain concepts like compound interest, risk vs. reward, and how taxes affect investments.

Opening a teen brokerage account under parental supervision allows them to invest in U.S. stocks or ETFs, giving them hands-on experience. Tracking a single stock’s performance or managing a small portfolio can teach them about risk and reward, with small losses serving as valuable lessons.

"Teaching your kids early lessons around money, the importance of saving, and investing can really set them up for success later in life." – Paul Dery, Vice President and Financial Consultant, Fidelity Investments

Use milestones like a first job to explain tax forms (W-4/W-2), paycheck deductions, and saving strategies. Share your own investment experiences – both wins and mistakes – to make the lessons relatable. Introduce them to your financial advisors, such as planners or CPAs, to normalize seeking professional guidance.

Encourage teens to take part in your family’s charitable giving. Let them research nonprofits and present their choices to teach due diligence and responsible decision-making. A matching program for their savings or investments can also show how capital grows over time.

Be mindful that teens may turn to social platforms like TikTok for investment advice, which often promotes risky schemes like cryptocurrencies or meme stocks. Help them distinguish between investing – owning shares in businesses – and gambling, which involves high-risk bets like the lottery.

A simple way to explain compound interest is the Rule of 72: divide 72 by the interest rate to find out how many years it takes for money to double. For example, at a 4% interest rate, money doubles in 18 years.

Teaching Your Children About Trusts and Offshore Protection

Once kids grasp the essentials of money management and investing, it’s time to tackle the next step: understanding how to protect family wealth for the long haul. Trusts and offshore asset protection might sound complex, but breaking them down into simple ideas can help future heirs see their value. By connecting these concepts to everyday life, you can show how trusts play a key role in securing your family’s legacy.

How to Explain Trusts to Your Children

Think of a trust as a "shield" that safeguards your family’s assets from risks like lawsuits, creditors, or unexpected challenges. For younger kids, you might call it a safety net – one that ensures their basic needs, like education and healthcare, are covered if their parents aren’t around.

To make it relatable, explain the "milestone approach": funds from the trust are released at certain life stages, like graduating college, buying a home, or reaching specific ages such as 25, 30, or 35. This way, they don’t get overwhelmed with a large sum too early, helping them manage money responsibly.

Introduce the trustee as a professional who oversees the funds, ensuring they’re used as intended. For younger children, use a fun, hands-on activity – like dividing money into three piggy banks labeled charity, savings, and spending. This mirrors how a trust allocates funds for different purposes and makes the concept easier to grasp.

"A parent is the best judge on what details to disclose to children and how to frame such a conversation… the goal is to avoid surprises when that wealth is ultimately passed down." – Scott Kerr, Vice President of Advanced Planning, Fidelity Investments

Another helpful tool is a "letter of wishes", which explains the trust’s purpose in plain, heartfelt language. This adds a personal touch to the formal documents and helps heirs understand the reasoning behind the trust’s rules. For older children, invite them to sit in on meetings with financial advisors or attorneys. This demystifies the process and gives them a sense of involvement.

Now, let’s look at how offshore trusts add another layer of protection by tapping into international legal systems.

Understanding Offshore Trusts for Better Asset Protection

Offshore trusts are a powerful way to protect wealth from creditors, lawsuits, or even divorce. While local trusts offer some security, offshore options go a step further by placing assets in jurisdictions with stronger privacy laws and legal protections.

These trusts operate in countries with laws specifically designed to shield assets from domestic threats. For example, the HEMS standard (Health, Education, Maintenance, and Support) ensures trust funds are reserved for meaningful needs, not reckless spending. Framing it this way can help instill responsibility in younger generations.

Regular family discussions can normalize the idea of offshore protection. Explain that these structures aren’t about hiding money – they’re about safeguarding it for future generations in an increasingly unpredictable world. You can also tie trust distributions to achievements, like earning a degree or starting a business, to emphasize the connection between wealth and accountability.

Here’s some perspective: an estimated $84 trillion will pass to heirs by 2045. Yet, nearly 50% of inherited wealth is spent, lost, or given away. By the second generation, most family wealth is gone, and by the third, nearly all of it disappears. These numbers highlight why protection structures like trusts are essential.

Onshore vs. Offshore Trusts: Key Differences

As children grow older, it’s important to teach them how to weigh the pros and cons of different trust structures. The main differences often boil down to privacy, protection, control, and tax treatment. Understanding these factors helps them appreciate the careful planning involved in preserving family wealth.

| Feature | Onshore (Local) Trust | Offshore Trust |

|---|---|---|

| Privacy Levels | Lower; may be subject to public records or disclosure | Higher; many jurisdictions have no public filing requirements |

| Asset Protection | Exposed to local legal claims | Stronger; "Firewall" laws often block foreign court orders |

| Setup | Simpler using local legal frameworks | More complex; requires international laws and licensed foreign trustees |

| Tax Advantages | Subject to local income, capital gains, and estate taxes | Often tax-neutral (no income or capital gains tax in the jurisdiction) |

| Control | Grantor can often act as trustee | Typically requires independent trustees for legal and tax compliance |

One key lesson for heirs is understanding that offshore trusts often require independent, licensed trustees instead of family members. While this might feel like giving up control, it’s a necessary step to ensure the trust is legally valid and offers maximum protection.

"Giving up control of your trust to someone you don’t know can feel scary to many trust founders, but it’s actually a good thing. In fact, the only way you can save tax and properly establish a trust is to create independent control." – Coreen van der Merwe, Director, Sovereign Trust

Help older children evaluate trust jurisdictions by considering factors like "Firewall Legislation" (laws that limit the recognition of foreign judgments), political stability, and the availability of skilled local service providers. For example, the British Virgin Islands allows trusts to last up to 360 years, while Jersey and Guernsey permit them to exist indefinitely. If you’re using a professional trustee, introduce your children to them early so they understand the trustee’s role in managing the trust and ensuring compliance.

Keep the conversation simple and approachable. The goal is to show how these structures protect family wealth and prepare heirs to manage it wisely when the time comes.

Steps to Prepare Your Children to Manage Family Wealth

Teaching children to manage family wealth effectively requires a mix of practical lessons and real-world experiences. Here’s how you can guide them through this journey.

Running Regular Family Money Meetings

Set up monthly or quarterly family meetings to discuss topics like financial goals, investments, and charitable plans. These gatherings make money conversations feel normal and help avoid surprises when wealth is eventually passed down. Start by having younger children sit in as observers, and as they grow, encourage them to actively participate. Over time, they might even share their thoughts on investments or succession planning.

During these meetings, work on creating a "Family Constitution" – a document that outlines what your family’s wealth represents and how it should serve future generations. Consider inviting professionals, such as a financial planner or estate attorney, to explain more complex topics like taxes or estate planning. This not only simplifies these subjects but also introduces your children to key advisors they may rely on later.

"Your legacy is not a spreadsheet. It’s a story – and your children are the next authors." – Holdun

These discussions also lay the groundwork for gradually assigning your children real financial responsibilities.

Giving Children Small Financial Responsibilities

Experience is often the best teacher. For children aged 11–15, open a youth bank account and introduce them to basic investment concepts, like tracking the performance of a stock. As they enter their late teens and early twenties, consider giving them more responsibility, such as managing a small investment portfolio or budgeting for a family trip.

Another hands-on approach is to involve them in philanthropy. Have them research charities, evaluate their impact, and recommend donations through a youth philanthropy fund. This not only teaches financial diligence but also instills a sense of responsibility for using resources wisely. Encouraging part-time jobs during their teenage years can also help them connect effort with income, a valuable life lesson.

Working with Professionals for Complex Topics

As your children take on more financial responsibilities, they’ll need expert guidance for more advanced topics. Introduce them to your financial planner, attorney, and accountant so they know where to turn for advice. Involve them in meetings with wealth advisors to learn about critical areas like tax planning, insurance, and estate strategies.

For particularly sensitive or complicated issues, a neutral third party can help mediate discussions and provide clarity. You might also explore internships within your family office or with professional advisors to immerse them further in wealth management. These experiences help reinforce the lessons learned at home while giving them a deeper understanding of wealth protection strategies.

Organizations like Global Wealth Protection offer private consultations to help families navigate advanced topics, including offshore trusts, private interest foundations, and tax strategies.

| Age Group | Financial Responsibility | Key Value Taught |

|---|---|---|

| 5–10 | Allowance with Save/Spend/Give jars | Money is earned and limited |

| 11–15 | Youth checking account; tracking stocks | Budgeting and market basics |

| 16–22 | Managing a small investment portfolio; filing taxes | Financial independence and risk |

| 23+ | Leadership in family philanthropy or governance | Stewardship and legacy |

Conclusion: Protecting Your Family’s Financial Future

Family wealth often diminishes over generations, largely because heirs are unprepared to manage their inheritance. The solution? Early, hands-on financial education.

Start by teaching your children basic financial concepts and gradually increase their responsibilities over time. Regular family discussions about money can also help instill a sense of accountability. Introducing them to tools like trusts and offshore protections can provide an additional safety net, shielding assets from potential risks like lawsuits or poor financial choices.

Another key step is building a reliable financial team. Bring your children into the conversation with your trusted financial advisors, so they know who to turn to when managing the family’s wealth. Organizations like Global Wealth Protection can assist with private consultations, offering expertise on complex areas such as offshore trusts and tax strategies to help secure your legacy for future generations.

FAQs

How do I talk about family wealth without creating entitlement?

Discussing family wealth in a way that avoids creating entitlement requires an emphasis on responsibility, values, and purpose. Approach these conversations by framing wealth as a matter of stewardship. Highlight the importance of hard work, making thoughtful financial decisions, and staying true to the family’s core principles.

Engaging children in discussions about financial goals and the broader family legacy can help them develop a deeper understanding and respect for what wealth represents. Regular, open conversations can shift their perspective, encouraging them to see wealth as a tool to create positive change rather than something to take for granted. This approach nurtures a sense of shared responsibility and purpose.

When should I start teaching my child about trusts?

Introducing your child to the concept of trusts during their elementary school years can lay the groundwork for financial literacy and responsibility. Early exposure helps them understand the basics of managing wealth, setting them up for better financial decision-making as they grow.

Do offshore trusts change my U.S. taxes?

Offshore trusts can influence your U.S. tax responsibilities based on their structure and how they’re reported. To stay on the right side of IRS regulations and steer clear of potential complications, consulting a tax professional is a must. Accurate reporting and strict compliance with the rules are essential for handling any related tax matters properly.