Economic downturns can wreak havoc on your finances if you’re unprepared. From falling stock values to job instability, recessions test your financial resilience. But with the right strategies, you can safeguard your wealth and even seize opportunities when others are struggling.

Here’s how you can protect your finances during tough times:

- Diversify internationally: Spread investments across countries to reduce risks tied to domestic policies or market crashes. For example, in 2025, non-U.S. equities outperformed U.S. equities by 12.1%.

- Focus on stable jurisdictions: Countries like Switzerland and Singapore offer strong financial systems, robust legal protections, and stable currencies.

- Use offshore trusts and companies: These structures shield your assets from lawsuits, creditors, and economic instability. Jurisdictions like Anguilla and the Cook Islands are top choices for asset protection.

- Open international bank accounts: Holding funds in multiple currencies and locations ensures liquidity and hedges against currency devaluation, like the U.S. dollar’s 10% drop in early 2025.

- Plan ahead: Timing is critical. Courts often reverse last-minute transfers, so set up protective structures during stable periods.

Key takeaway: Preparation is everything. By acting early and diversifying your assets globally, you can weather economic cycles and protect your financial future.

Spreading Investments Across Multiple Countries

Relying solely on domestic investments can leave your finances vulnerable to a single point of failure. If your home country faces an economic downturn, your entire portfolio could take a hit. International diversification spreads your assets across different countries, shielding you from risks like domestic policy shifts, capital controls, or even government actions that could freeze your assets.

Take the first half of 2025, for example. During this period, the U.S. dollar dropped over 10% against a basket of major currencies – its worst six-month performance since the Bretton Woods collapse in 1973. Meanwhile, non-U.S. equities outperformed U.S. equities by 12.1%. Investors who kept their wealth tied exclusively to the dollar saw their global purchasing power shrink, whereas those with diversified, multi-currency portfolios stayed on steady ground.

"Diversifying across currencies, geographies, and jurisdictions helps US investors manage risk in uncertain times."

- Evelyn Vigistain, Senior Investment Strategist – Global Families, Bernstein

But the benefits go beyond market performance. In 2023, the U.S. saw about 5 million new court cases filed. Wealthy Americans are frequent litigation targets, but many foreign courts don’t automatically enforce U.S. judgments. This forces creditors to pursue costly legal battles across multiple jurisdictions, creating a significant layer of protection around your assets.

Selecting Financially Stable Countries

Not every country offers the same level of security for your investments. The key is to focus on countries with strong financial systems, reliable legal frameworks, and stable governments. Switzerland and Singapore, for instance, are prime choices. Their central banks (FINMA in Switzerland and MAS in Singapore) enforce strict lending practices and maintain high capital requirements, which help safeguard deposits even during global market turbulence.

You’ll also want to prioritize countries with constitutionally protected property rights and judicial systems that require strong legal justification before freezing assets or recognizing foreign claims. Jurisdictions like the Cook Islands, Nevis, and the Bahamas stand out for their robust trust laws and consistent legal rulings. Tax-neutral regions can also provide a stable environment by reducing the risk of unexpected government levies.

Currency stability is another important factor. The Swiss Franc (CHF) and Singapore Dollar (SGD), for example, have a track record of holding steady during inflationary periods or geopolitical crises. Align your currency holdings with your spending needs – if 40% of your expenses are in Euros, consider holding 40% of your assets in Euro-denominated accounts to minimize exchange rate risks.

By choosing stable jurisdictions and diversifying your portfolio, you create a more resilient financial strategy.

Advantages of International Investment Diversification

International diversification offers a direct defense against domestic economic risks. The main advantage is sovereign risk protection. While a domestic portfolio focuses on market risks – like stock fluctuations and interest rate changes – an international portfolio adds a layer of defense against government actions that could restrict, tax, or even seize your assets.

Currency diversification is another major benefit. By holding assets in multiple currencies, you protect your purchasing power globally. For example, when the U.S. dollar weakens, investments in stronger currencies retain their value. Multi-currency accounts allow you to hedge against risks tied to any single country’s monetary policies. Additionally, offshore LLCs or trusts can legally separate your assets from your personal ownership. This makes it harder – and more expensive – for creditors to seize them, as they would need to navigate foreign legal systems with unfamiliar rules and higher evidentiary standards.

Another upside is access to growth markets. While the U.S. economy might slow down during a recession, other regions – whether emerging markets or stable developed economies – could continue to grow. Investing internationally means you’re positioned to benefit from these opportunities, turning a domestic downturn into a manageable event rather than a financial disaster.

| Feature | Domestic Portfolio | International Portfolio |

|---|---|---|

| Primary Risk Managed | Market Risk | Sovereign Risk |

| Legal Reach | One legal system | Multiple jurisdictions |

| Currency Exposure | Single currency | Multi-currency holdings |

| Asset Access | Vulnerable to local controls | Accessible globally even under restrictions |

sbb-itb-39d39a6

Using Offshore Trusts to Protect Your Assets

Offshore Trust Jurisdictions Comparison: Anguilla vs Cook Islands vs Samoa

Offshore trusts create a legal barrier that helps shield your assets from creditors. The key idea here is separating legal ownership: your assets are placed under the control of a foreign trustee and governed by the laws of a different country. Many offshore locations, such as Anguilla and the Cook Islands, don’t recognize court orders or judgments from other countries. So, even if a U.S. creditor wins a case against you, they’d have to re-litigate in the foreign jurisdiction – often under stricter rules. For example, proving a fraudulent transfer might require evidence "beyond a reasonable doubt", which is a much higher standard than in the U.S..

"Asset protection trusts offer the strongest protection you can find from creditors, lawsuits, or any judgments against your estate."

Offshore trusts offer an additional layer of security by protecting your wealth from economic instability in your home country. Jurisdictions like Anguilla don’t impose income, capital gains, inheritance, or gift taxes on trusts, meaning your assets are also insulated from sudden government tax hikes during economic downturns. On top of that, these jurisdictions often have very short statutes of limitations for fraudulent transfer claims – sometimes as brief as one or two years – giving creditors little time to challenge the transfer of assets.

Timing is critical. It’s best to establish the trust during stable periods, long before any legal threats appear. Including features like an Anti-Duress Clause (to block distributions under legal pressure) and a Flight Clause (to move the trust to another jurisdiction if needed) can further strengthen your trust. However, it’s crucial to genuinely give up ownership – once the trust is established, the trustee legally controls the assets, not you.

This approach not only safeguards your assets from legal claims but also helps protect your wealth during economic downturns. Anguilla, in particular, demonstrates how a well-structured offshore trust can provide both legal and financial security.

Anguilla Offshore Trusts: Legal Protection and Tax Benefits

Anguilla has positioned itself as a top choice for asset protection. Its International Trust Act 2007, based on English Common Law, offers a familiar legal foundation while explicitly rejecting the enforcement of foreign judgments.

The tax advantages are equally appealing. Anguilla imposes no local taxes on income, capital gains, inheritance, or gifts for international trusts. While U.S. citizens still need to report to the IRS (via Forms 3520 and 3520-A), the trust itself remains untaxed locally. This tax neutrality ensures your wealth isn’t eroded by foreign tax obligations during tough economic times.

"Anguilla’s legal framework for trusts is characterized by a robust Common Law tradition, supplemented by modern legislative components such as the International Business Companies Act."

- Offshore Protection

Privacy is another major advantage. Anguilla enforces strict confidentiality, with no public disclosure of the trust’s beneficiaries or the person who set it up. Trust documents are kept private, and the Anguilla Financial Services Commission (AFSC) oversees compliance without compromising this confidentiality. This makes it much harder for creditors to even identify your protected assets.

Anguilla also provides flexible trust structures. You can set up discretionary trusts, fixed-interest trusts, or even combine a trust with an International Business Company (IBC) or LLC for added layers of protection. This multi-layered approach creates additional hurdles for creditors, making it both costly and time-consuming for them to pursue your assets.

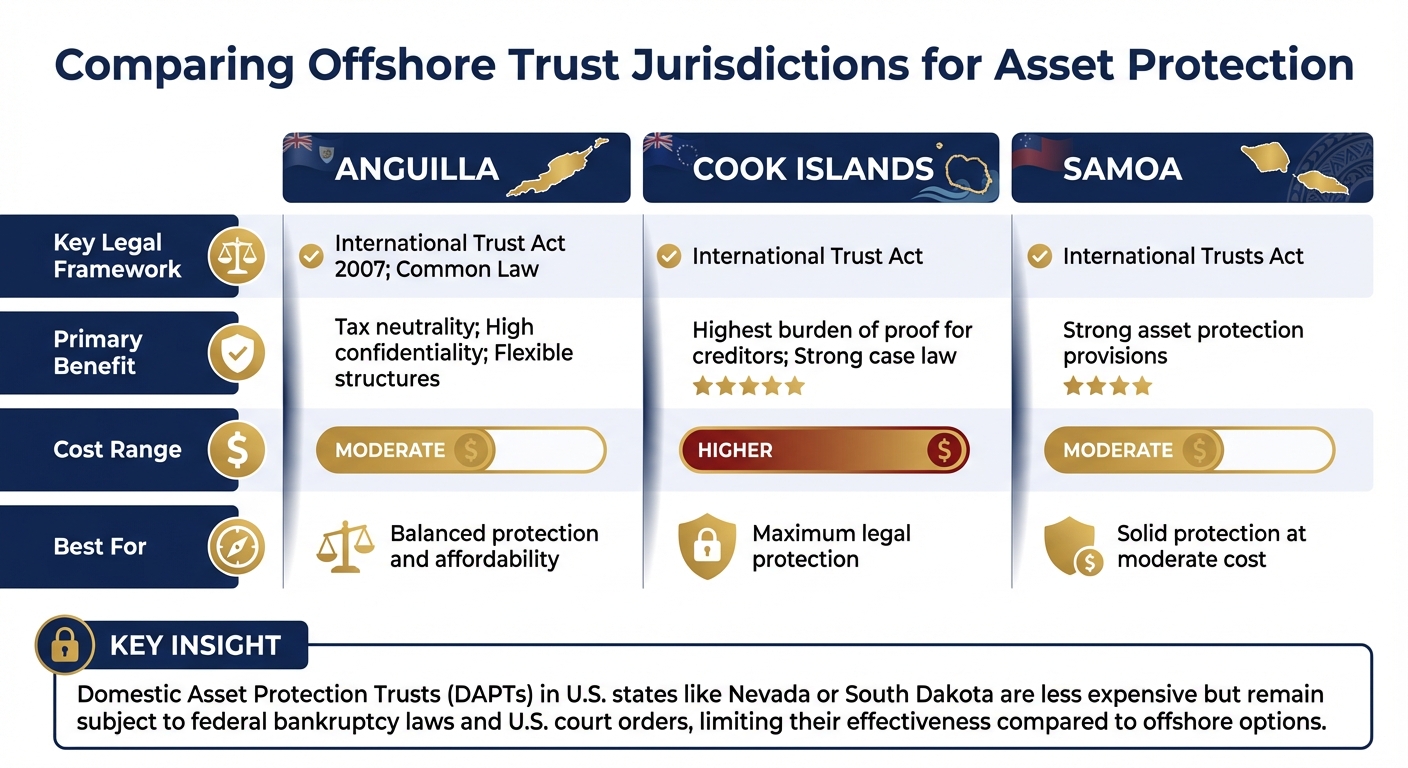

Comparing Different Trust Jurisdictions

Each jurisdiction offers its own blend of legal protections and cost structures. The Cook Islands is often regarded as having the strongest asset protection trust laws globally, with well-established case law to back it up. Creditors face a high burden of proof – similar to criminal cases – and have very limited time to file claims. However, Cook Islands trusts generally come with higher setup and maintenance costs.

Anguilla provides a strong alternative, offering comparable protections at a more accessible price. Its legal system emphasizes confidentiality and aligns with international compliance standards like CRS and FATCA. Samoa is another solid option, with its International Trusts Act providing strong asset protection measures.

| Jurisdiction | Key Legal Framework | Primary Benefit | Typical Cost Range |

|---|---|---|---|

| Anguilla | International Trust Act 2007; Common Law | Tax neutrality; high confidentiality; flexible structures | Moderate |

| Cook Islands | International Trust Act | Highest burden of proof for creditors; strong case law | Higher |

| Samoa | International Trusts Act | Strong asset protection provisions | Moderate |

Domestic Asset Protection Trusts (DAPTs) in U.S. states like Nevada or South Dakota are less expensive and easier to set up. However, they remain subject to federal bankruptcy laws and U.S. court orders, which limits their effectiveness. As of 2024, at least 20 states allow DAPTs, but none offer the same level of security as offshore trusts.

Ultimately, the right choice depends on your goals. For those at high risk of litigation or seeking maximum protection, jurisdictions like the Cook Islands or Anguilla are top contenders. If your needs are more focused on estate planning and moderate asset protection, a domestic trust might suffice. For anyone looking to secure their wealth against both legal and economic threats, offshore trusts remain the most robust option.

Setting Up Offshore Companies for Financial Protection

Offshore companies add a critical layer of security to your financial strategy by separating personal assets from potential risks. Establishing an entity in locations like Anguilla or Nevis allows the company to legally own assets – whether it’s real estate, intellectual property, or investments – while you retain control through proper structuring. This setup makes lawsuits against you personally more complex, as plaintiffs would need to pursue separate legal action in the offshore jurisdiction. Many jurisdictions also limit creditors to a charging order, which only gives them a claim to a portion of the company’s income instead of direct access to its assets.

"Think of it like having multiple locks on your door instead of just one. By placing assets in carefully chosen foreign locations with favorable laws, you make it much harder for others to get to your money."

- The Nestmann Group

Offshore companies also protect your identity by keeping ownership details off public records, reducing the risk of opportunistic lawsuits. This is unlike many U.S. entities, where ownership records are often publicly accessible. In 2023 alone, approximately 5 million new lawsuits were filed in the United States, highlighting the importance of maintaining privacy.

Another advantage is currency diversification. For example, during the first half of 2025, the U.S. dollar experienced its steepest decline since 1973, losing over 10% against the DXY, a basket of major global currencies. By holding assets in multiple currencies – such as Swiss francs, euros, or even physical gold – through an offshore company, you can safeguard your wealth from dollar devaluation. The next sections delve into specific structures and strategies to make the most of these benefits.

Forming an Anguilla Company: Privacy and Asset Separation

Anguilla is a top choice for setting up an offshore company. Its strong privacy laws ensure that beneficial ownership details are not part of any public registry, keeping your name off searchable databases. This legal framework offers a reliable, long-term solution for maintaining confidentiality.

Setting up an Anguilla International Business Company (IBC) is straightforward and involves minimal ongoing compliance. Additionally, there is no local taxation on income, capital gains, or dividends earned outside Anguilla. However, U.S. citizens must still report these companies to the IRS via Form 5471 and file an FBAR (FinCEN Form 114) if foreign accounts exceed $10,000 during the year.

When you transfer assets – such as investments or intellectual property – into an Anguilla company, the entity becomes the legal owner. This separation shields your personal wealth from liabilities tied to your domestic business. For instance, if your U.S.-based business faces a lawsuit, assets held in the Anguilla company remain protected under foreign jurisdiction.

It’s crucial to establish offshore structures well in advance of any legal troubles to avoid accusations of "fraudulent conveyance." Courts carefully examine whether assets were transferred to hinder creditors. Setting up these entities during stable times ensures their legitimacy.

To maintain the legal integrity of your offshore company, treat it as a genuine business. Keep separate bank accounts, file annual reports, and document decisions properly. These practices strengthen the company’s legal standing, making it harder for creditors to "pierce the corporate veil" and access its assets.

Combining Private US LLCs with Offshore Companies

A layered approach – combining domestic and offshore structures – can make it significantly harder for creditors to access your assets. For example, a Wyoming LLC can serve as the first line of defense for domestic operations, while an offshore company provides an additional barrier. This forces creditors to navigate distinct legal systems in separate jurisdictions.

A Wyoming LLC can hold U.S. real estate, benefiting from charging order protection and keeping your name off public property records. Meanwhile, an Anguilla IBC can hold liquid investments like stocks, bonds, or cash reserves. In the event of a lawsuit, a creditor would face the challenge of litigating under both Wyoming and Anguilla laws to access your assets.

"In my 15+ years advising clients on asset protection, the most durable plans combine domestic protection (insurance, estate planning, entity structure) with limited, carefully documented offshore elements only after full legal and tax review."

- Author Note, finhelp.io

This dual-structure approach spreads your assets across jurisdictions, reducing the likelihood that a single legal issue could jeopardize your entire portfolio. High-risk professionals, such as physicians – 31.2% of whom face lawsuits during their careers – may find this strategy particularly valuable.

Tax compliance is essential when using this method. U.S. citizens are taxed on worldwide income, so holding assets offshore does not eliminate tax obligations. You’ll need to file Form 5471 for the offshore company, submit FBAR for foreign accounts, and possibly address additional tax rules like Controlled Foreign Corporation (CFC) or Passive Foreign Investment Company (PFIC) regulations. Consulting with experienced legal and tax advisors ensures compliance while maximizing asset protection.

Keep your structure simple. A two-entity setup – one domestic LLC for U.S. assets and one offshore company for international holdings – offers robust protection without creating unnecessary administrative complexity.

Managing Liquidity with International Banking

Diversifying your assets across jurisdictions is a solid strategy, but managing liquidity through international banking takes it a step further. It ensures your money remains accessible, even during economic upheavals. A diversified portfolio alone won’t protect you if your funds are tied up in a single country’s banking system. Recent bank collapses have shown how depositors can face frozen accounts and delays in accessing their money. By spreading your cash across multiple countries, you minimize the risk of being caught off guard by a banking crisis in one location.

International banking also offers a hedge against currency devaluation. For instance, the U.S. Dollar has seen notable declines recently. Holding funds in stable currencies like Swiss francs or euros can help preserve your purchasing power. By maintaining accounts in multiple currencies, you’re better positioned to weather fluctuations in the value of the dollar.

Another advantage of foreign accounts is the legal protection they provide. U.S. court orders don’t automatically apply in other countries, which means creditors would need to initiate separate legal actions abroad – a costly and time-consuming process. Considering that approximately 5 million new court cases were filed in the U.S. in 2023, this added layer of protection can be a game-changer.

Timing is crucial. Establish these banking relationships during calm periods, not in the middle of financial trouble. Courts often scrutinize last-minute asset transfers, viewing them as potential attempts to defraud creditors. Setting up accounts well in advance signals legitimate financial planning rather than evasion. Next, we’ll explore the practical steps to set up these accounts.

Setting Up Bank Accounts in Multiple Countries

Opening international bank accounts isn’t as simple as walking into your neighborhood bank. Reputable foreign banks typically require thorough documentation, including apostilled passport copies, one to three years of tax returns, and detailed proof of your funds’ origin. They’ll also want to understand your tax residency, the account’s purpose, and how you intend to use it. This process aligns with international anti-money laundering regulations.

Choosing the right jurisdiction depends on your financial needs. Swiss banks, known for their stability, often require deposits ranging from $500,000 to $1 million. Singapore offers similar security with strong connections to Asian markets, usually requiring $250,000 to $500,000. For more accessible options, Portugal provides EU banking access starting at around $50,000, while Panama’s minimum deposits range from $25,000 to $100,000.

When managing multiple currencies, align your account holdings with your spending habits. For instance, if 40% of your expenses are in Europe, consider keeping 40% of your liquid reserves in euros. This strategy minimizes exchange-rate risks and avoids forced currency conversions. Many international banks now offer multi-currency accounts, allowing you to hold dollars, euros, Swiss francs, and more within a single account.

Compliance is a must. U.S. citizens are required to file an FBAR (FinCEN Form 114) if their foreign accounts exceed $10,000 at any point during the year. Additionally, IRS Form 8938 must be filed when certain thresholds are met. Partner with tax professionals who are well-versed in U.S. regulations and the laws of your chosen jurisdictions.

Don’t move all your capital offshore in one go. Keep enough liquid assets in domestic accounts for immediate needs and potential legal costs. Think of international accounts as your financial safety net – funds you can access if domestic banking becomes unstable or if you need to relocate quickly during an economic downturn. Specialized resources can simplify this process and help you implement a well-rounded strategy.

GWP Insiders Membership: Tools and Resources for Economic Downturns

Navigating the complexities of international banking and asset protection requires expertise that many financial advisors don’t offer. The GWP Insiders Membership provides a wealth of resources and guidance to help you protect your assets during uncertain times.

Members gain access to detailed information on selecting the best banking jurisdictions based on their financial goals and risk tolerance. This includes insights on minimum deposit requirements, account setup procedures, and compliance rules across various countries. Instead of piecing together information from multiple sources, you’ll have a centralized framework for building a resilient financial strategy.

The membership also offers personal consultations, allowing you to explore options tailored to your situation. Whether you’re deciding between Swiss banking stability or Singapore’s market connections, or determining the right mix of domestic and offshore assets, you’ll receive advice from specialists in international asset protection. This guidance helps you avoid costly errors and ensures your financial structures remain legally sound.

Beyond banking, GWP Insiders provides strategies for legally minimizing taxes, selecting offshore companies and trusts, and creating actionable plans for relocation if economic conditions worsen. These resources integrate with offshore structures discussed earlier, offering a comprehensive approach to asset security and liquidity management during economic cycles.

Step-by-Step Guide to Recession-Proof Wealth Protection

Protecting your wealth during a recession requires careful, long-term planning. Strategies like international diversification, offshore trusts, and international banking work best when they’re part of a well-thought-out plan established well in advance. Courts often scrutinize last-minute asset transfers, so it’s crucial to build your financial safety net during stable times – long before any economic or legal challenges arise. These steps align closely with principles of international diversification and offshore protections.

Moving Assets Before a Recession Starts

Timing is everything when it comes to safeguarding your assets. To ensure success, you need to transfer assets into protective structures years ahead of potential economic instability or legal threats. Courts can reverse last-minute transfers designed to dodge creditors, labeling them as "fraudulent conveyance".

"Timing really matters when protecting your money. You need to set things up before any problems start. If you wait until someone sues you, it’s too late."

– The Nestmann Group

Start by identifying risks such as currency devaluation, bank failures, or legal liabilities. In 2023 alone, about 5 million new court cases were filed in the U.S.. If you’re a high-net-worth individual or a business owner, these risks highlight the importance of acting proactively.

Focus on jurisdictions with strong asset protection laws, stable banking systems, and reliable governance. For instance, opening a Swiss bank account often requires a minimum of $1,000,000, while Austrian banks typically require $250,000 to $300,000.

Diversify your holdings by spreading assets across currencies like Swiss francs, euros, and other stable options. This can act as a hedge against fluctuations in the U.S. dollar, which saw a 10% drop in the Dollar Index as of August 29, 2025 – its worst six-month start since 1973.

At the same time, ensure you have sufficient liquidity domestically to cover immediate needs while reserving international assets as a backup during economic upheavals.

Following International Tax and Reporting Rules

Once your assets are repositioned offshore, compliance becomes the cornerstone of legitimate protection. For U.S. citizens, worldwide income is taxable, regardless of where the assets are located. Moving money offshore doesn’t reduce tax obligations but instead provides legal shielding from private creditors.

"Proper offshore protection is never about hiding assets from Uncle Sam – it’s about legally structuring them to be protected from private creditors."

– The Nestmann Group

The IRS mandates specific reporting for foreign accounts and structures. For instance, you must file FinCEN Form 114 (FBAR) if your foreign accounts exceed $10,000 at any point during the year. Additionally, IRS Form 8938 is required when foreign financial assets cross certain thresholds. More complex setups, like foreign trusts or corporations, may involve filing Forms 3520, 3520-A, 5471, or 8621.

Most jurisdictions now participate in information-sharing agreements under FATCA or the Common Reporting Standard, with over 80 countries maintaining beneficial ownership registries.

To navigate these complexities, work with legal experts familiar with both U.S. laws and the regulations in your chosen jurisdiction. Keep detailed records of all transactions, trustee decisions, and compliance filings to demonstrate that your intent is protection – not evasion.

Building Your Global Escape Hatch Plan

Once your assets are secure and compliant, it’s time to consider a global contingency plan. This includes having a physical "Plan B" – a viable option if domestic conditions worsen. Securing foreign residency is a good first step, offering the legal right to live in another country if needed. Many residency programs require investments ranging from $100,000 to $200,000.

Purchasing foreign real estate can also serve as a practical safety net. Properties in countries like Portugal, Panama, or Mexico can double as vacation homes, rental properties, or emergency relocation options. Structuring these purchases through offshore entities can enhance privacy and protection.

Tailor your contingency plan based on your financial situation:

- Under $500,000: Focus on opening foreign bank accounts, maintaining 10–20% currency diversification, and exploring modest real estate investments.

- $500,000 to $3 million: Add asset protection trusts and foreign residency permits for additional security.

- Over $3 million: Consider advanced options like dynasty trusts, family foundations, or shared family office platforms.

Striking a balance between control and protection is essential. While maintaining personal oversight is tempting, too much control can weaken legal defenses. Independent trustees or trust protectors can provide a middle ground, offering oversight without compromising protection.

Although only 8,000 to 10,000 U.S. citizens expatriate annually, having a global escape plan doesn’t necessarily mean leaving permanently. It’s about having options – whether for temporary relocation during economic downturns or a permanent move if circumstances demand it.

Conclusion: Maintaining Financial Security Through Economic Cycles

Economic downturns are unavoidable, but taking proactive steps can shield you from financial ruin. The strategies discussed here – international diversification, offshore trusts, multi-jurisdictional banking, and thorough advance planning – work together to build a financial safety net capable of withstanding even the toughest economic challenges. The key takeaway? Preparation must come before the storm. Courts often view last-minute asset transfers as fraudulent, so timing is everything.

"The best plan is to set up protection years before any trouble… It’s like buying car insurance. You can’t get it after you’ve had an accident." – The Nestmann Group

Start with the basics: maintain six to twelve months of expenses in liquid cash, diversify your investments across different asset classes and currencies, and establish offshore structures during calm, stable periods.

Equally important is staying compliant with legal requirements. Compliance is essential. Offshore protection isn’t about hiding money; it’s about creating lawful barriers against potential claims. This means filing FBARs, keeping meticulous records, and consulting professionals well-versed in both U.S. and international regulations. With over 5 million court cases filed annually in the U.S., it’s not a question of "if" you’ll face financial risks – it’s "when."

The wealthiest individuals don’t just survive economic downturns; they thrive by seizing opportunities when others are forced to sell. By adopting strategies like international diversification, offshore structures, and global banking solutions ahead of time, you can safeguard your financial future through every economic cycle. Build your safety net now, while markets are steady and legal protections are at their strongest. Take action today to secure tomorrow.

FAQs

How much money should I keep offshore?

The amount of money to keep in offshore accounts varies based on your total assets, financial objectives, and risk tolerance. Many high-net-worth individuals choose to maintain several million dollars offshore to bolster asset protection and ensure greater privacy. It’s crucial to work with a financial professional to tailor a strategy that aligns with your unique circumstances.

Are offshore trusts legal for U.S. citizens?

Yes, offshore trusts are legal for U.S. citizens, but they come with strict tax and reporting requirements. Mismanagement or misuse can lead to serious legal or tax problems. To avoid any issues, it’s crucial to structure them correctly and follow all applicable regulations.

What IRS forms do I need for foreign accounts?

To disclose foreign accounts, you’ll need to file IRS Form 8938 (Statement of Specified Foreign Financial Assets). On top of that, if the total value of your foreign accounts exceeds $10,000 at any point during the year, you may also be required to file FinCEN Form 114 (FBAR). Staying on top of these filings is crucial to avoid potential penalties.