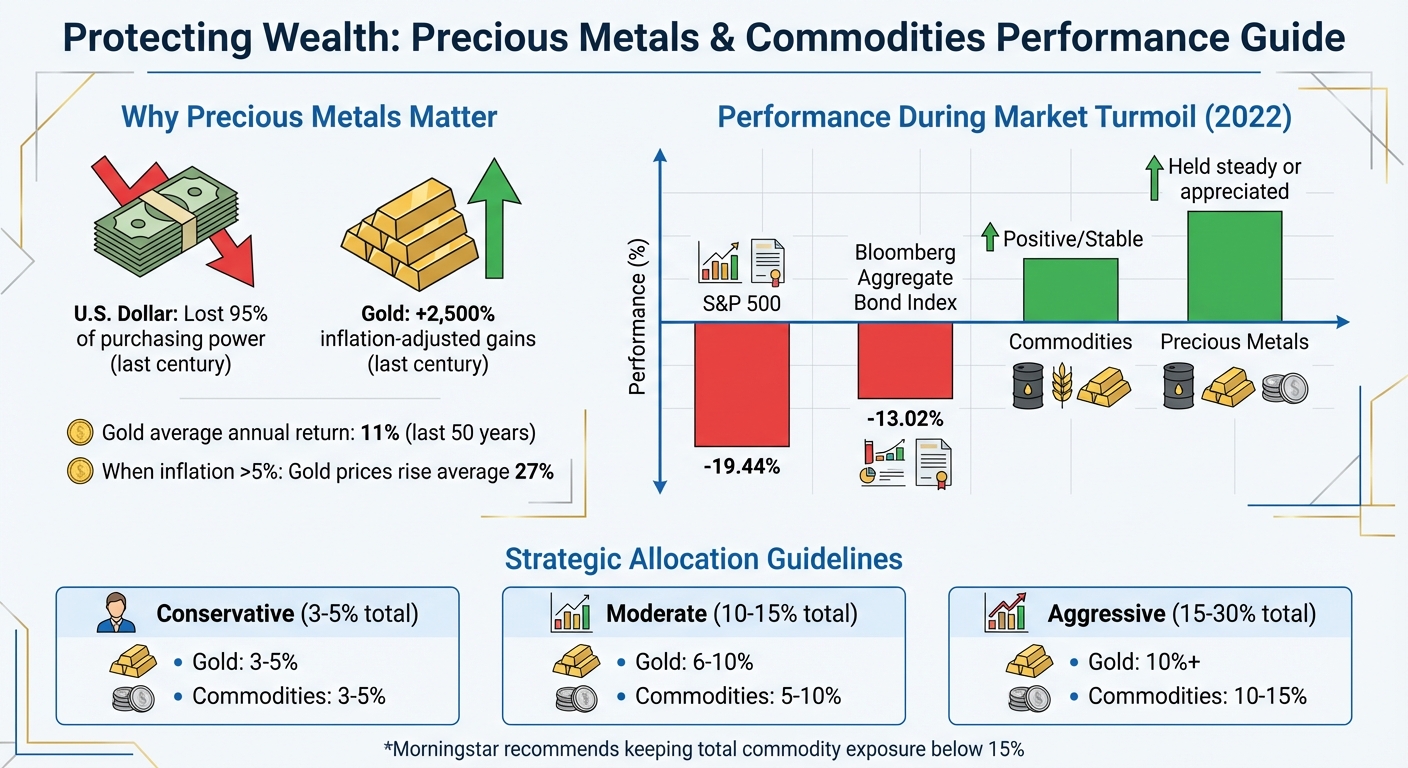

Your wealth is at constant risk from inflation, currency devaluation, and economic instability. Over the last century, the U.S. dollar has lost 95% of its purchasing power, while gold’s inflation-adjusted value has surged by over 2,500%. Traditional investments like stocks and bonds often fail to protect against such challenges, especially during periods of high inflation or market downturns.

Precious metals (like gold and silver) and commodities (such as oil, natural gas, and agricultural products) offer a reliable way to preserve and grow wealth. These assets:

- Hedge against inflation: Gold prices rise during inflationary periods, with average gains exceeding 20% when inflation hits 5% or more.

- Diversify portfolios: Commodities and metals have low correlation with traditional assets, offering stability during market volatility.

- Perform well during crises: In 2022, while stocks and bonds plummeted, commodities and metals held or increased in value.

To safeguard your wealth:

- Allocate 6–10% of your portfolio to gold and 3–15% to commodities, depending on your risk tolerance.

- Consider physical ownership (like coins or bars) for stability or ETFs for liquidity.

- Use secure storage options, including professional vaults or international locations like Switzerland or Singapore, to protect your investments from geopolitical risks.

This strategy ensures your assets are shielded from inflation, market instability, and economic uncertainty.

Precious Metals vs Traditional Assets: Historical Performance and Portfolio Allocation Guide

How Precious Metals Preserve Your Wealth

Precious metals hold their value due to their scarcity, universal recognition, and low correlation with traditional financial markets. Unlike stocks or bonds, which rely on corporate success or government stability, gold and silver retain worth through their limited supply and global acceptance. Over the last century, fiat currencies have lost 99% of their purchasing power when compared to gold.

This unique characteristic helps precious metals act as a counterbalance, reducing portfolio risk and shielding against sudden market downturns. For instance, in 2022, while the S&P 500 dropped 19.44% and the Bloomberg Aggregate Bond Index fell 13.02%, precious metals often held steady or even appreciated in value. This reliability highlights their role in protecting and growing wealth, especially during turbulent times.

Gold: The Primary Safe-Haven Asset

Gold is widely regarded as the ultimate safe-haven asset during financial crises, currency devaluations, and geopolitical turmoil. From 1971 to 2021, gold consistently delivered strong average returns and remained highly liquid, even in challenging market conditions. Notably, during periods of high inflation – when consumer prices rose above 5% – gold prices jumped by an average of 27%.

The global gold market’s size and accessibility make it easy for investors to buy or sell, even during economic stress. This liquidity is further reinforced by central banks, which continue to accumulate gold as a way to diversify their reserves, driving demand even higher.

Investment experts suggest allocating 6% to 10% of a portfolio to gold to enhance performance and support long-term returns. Investors can choose to hold physical gold – such as coins or bars – to avoid counterparty risk, though this requires secure storage and insurance. Alternatively, exchange-traded funds (ETFs) like GLD provide exposure to gold without the logistical challenges of storing bullion. Gold’s historical role as a safe haven and its enduring demand make it a cornerstone of financial stability.

Silver: A Flexible and Affordable Investment

While gold offers stability, silver brings versatility and growth potential to the table. Silver functions as both a precious metal and an industrial commodity, making its price influenced by industrial demand as well as investor interest. Its extensive use in electronics and chemical applications means silver’s performance is tied to both economic trends and market sentiment. This dual role results in higher volatility compared to gold but also creates opportunities for more substantial gains during market upswings.

Silver’s lower price point makes it accessible to a broader range of investors and allows for easier liquidation. For instance, owning ten one-ounce silver bars provides more flexibility for partial sales than a single ten-ounce bar. This affordability and divisibility make silver an appealing option for those looking to build a diversified portfolio.

While gold often takes the lead in terms of stability, silver enhances a precious metals strategy by combining safe-haven appeal with the potential for industrial-driven growth.

sbb-itb-39d39a6

How Commodities Fit Into a Diversified Portfolio

Commodities bring a different type of protection to a portfolio compared to precious metals. While gold and silver are often seen as safeguards during financial uncertainty, commodities like oil, natural gas, wheat, and corn are influenced by factors such as weather, geopolitical events, and supply-demand dynamics. This independence creates a diversification effect that’s hard to replicate. For instance, between 1991 and 2025, the Bloomberg Commodity Total Return Index had rolling one-year returns that showed nearly zero correlation with global bonds. This unique behavior makes commodities an excellent complement to traditional assets and precious metals for wealth protection.

Take the inflation surge during 2021–2022 as an example: while the Bloomberg Aggregate Bond Index fell 13.02% and the S&P 500 dropped 19.44%, broad commodity indexes saw notable gains. As PIMCO puts it:

"Commodities are one of the few asset classes that tend to benefit from rising inflation".

Different commodities shine during various economic phases. Energy and industrial metals thrive during periods of growth, while agricultural products often perform well when inflation expectations climb. Experts suggest moderate investors allocate 5% to 10% of their portfolios to commodities, with conservative strategies targeting 3% to 5% and aggressive ones going up to 10% to 15%. Many investors turn to broad-based ETFs like DBC or BCI for exposure across multiple commodities, while sector-specific ETFs (such as USO for oil or CORN for corn) and stocks of commodity producers (like ExxonMobil or Archer-Daniels-Midland) offer more focused options. These varied approaches ensure commodities play a key role in building a resilient portfolio.

Oil and Energy Commodities

Oil is one of the most actively traded commodities in the world, making it a cornerstone for energy-focused investments. Energy commodities are particularly effective at hedging against unexpected inflation, as they react directly to supply disruptions and demand shifts. For instance, when Russia reduced gas exports to Europe in 2022, commodities were among the few assets to deliver positive inflation-adjusted returns, while both stocks and bonds posted negative real returns.

Price swings in energy markets can be dramatic. In 2021, as global travel rebounded, WTI crude oil prices jumped from around $48 per barrel at the start of the year to $75 by year-end, delivering a 62% return for the Bloomberg Sub WTI Crude Oil Index. This followed a steep 51% loss in 2020, showcasing the volatility inherent in energy markets.

Natural gas is also gaining importance, with the U.S. expected to supply over one-third of the global liquefied natural gas (LNG) market by 2030. As Lina Thomas, an analyst at Goldman Sachs Research, explains:

"the growing use of commodities as leverage may reinforce the diversification benefits of commodities in portfolios".

Since owning physical oil or natural gas isn’t practical for most investors, futures-based ETFs or stocks of energy producers provide accessible alternatives. However, investors should be cautious of "contango", where future prices exceed current ones, potentially dragging down returns for futures-based investments.

Agricultural Commodities and Other Natural Resources

Agricultural commodities like wheat, corn, soybeans, and cattle add another layer of diversification to a portfolio. These "soft commodities" are driven by weather patterns, seasonal cycles, and food supply stability, often rising in response to energy supply shocks or increased demand.

During peak economic cycles, both agricultural and industrial commodities demonstrate strong inflation-hedging potential. Industrial metals, for example, have delivered average real returns of about 30% during high-inflation periods. Timber and other natural resources also benefit from long-term trends, such as the shift toward green energy. For instance, building an onshore wind plant requires nine times more mineral resources than a traditional gas-fired plant, fueling demand for industrial commodities. Additionally, the rise of AI is driving increased demand for energy and infrastructure, further supporting both traditional and renewable resources.

Investors can access agricultural commodities through broad-based ETFs or funds specifically focused on agriculture. Stocks of companies like Archer-Daniels-Midland offer exposure to agricultural processing and distribution without the complexities of owning physical commodities. A diversified approach is essential here – single-crop failures or regional droughts can significantly affect individual commodity prices, but a broader basket of commodities can help mitigate these risks.

| Economic Phase | Outperforming Commodities |

|---|---|

| Expansion | Industrial metals (copper, aluminum) and energy |

| Peak | Agricultural commodities (wheat, corn) |

| Contraction | Precious metals (gold, silver) for downside protection |

| Recovery | Base metals and energy |

(Source: Investopedia)

How to Add Precious Metals and Commodities to Your Portfolio

Building a portfolio that includes precious metals and commodities can help safeguard your wealth during uncertain economic times. Let’s explore how to allocate these assets effectively and choose between physical ownership and paper-based investments.

Portfolio Allocation for Better Protection

Your allocation strategy should align with your financial goals and risk tolerance. Here’s a breakdown:

- Conservative investors: Allocate 3% to 5% of your portfolio to gold ETFs or shares in established mining companies.

- Moderate investors: Increase allocation to 5% to 10%, incorporating broad-based commodity ETFs or sector-specific investments.

- Aggressive investors: If you’re preparing for severe economic disruptions or inflation, consider allocating 10% to 15%, or even up to 20% to 30% in extreme cases.

Morningstar advises keeping total commodity exposure below 15% to avoid over-concentration. For long-term stability, hold these investments for at least 10 years to ride out market fluctuations.

When investing in precious metals, diversification is key. Instead of focusing solely on bullion, consider splitting your holdings: allocate 10% to 20% to liquid bullion for quick access and 80% to 90% to rare coins or numismatics, which offer long-term growth potential due to their scarcity.

Once you’ve set your allocation, it’s time to weigh the benefits and drawbacks of physical assets versus paper-based investments.

Physical Ownership vs. Paper Investments

Your choice between physical and paper-based investments should depend on your investment goals.

- Physical ownership: Owning tangible assets like gold bars or American Eagle coins gives you direct control and eliminates counterparty risk. These assets remain accessible during financial crises, but they come with added costs for secure storage, insurance, and premiums over spot prices.

- Paper investments: Options like ETFs, futures contracts, and mining stocks provide high liquidity and ease of trading through brokerage accounts. They’re great for short-term strategies, but they involve counterparty risk, management fees, and potential discrepancies between share prices and the underlying metal. In some markets, paper gold claims can exceed the physical supply by 100 to 1 or more.

Here’s a quick comparison of the two approaches:

| Investment Method | Best For | Key Advantage | Main Drawback |

|---|---|---|---|

| Physical Ownership | Long-term preservation, systemic risk hedge | No counterparty risk; tangible asset | Storage costs; lower liquidity |

| ETFs/Funds | Easy trading, diversified exposure | High liquidity; no storage needed | Management fees; tracking error |

| Futures Contracts | Leveraged price exposure | Direct price access; high leverage | High volatility; margin requirements |

| Mining Stocks | Growth potential, dividend income | Operational leverage; accessible via brokerage | Company-specific risks; equity volatility |

For retirement accounts, a Gold IRA allows you to hold physical gold while enjoying tax benefits. Just ensure you work with an approved custodian and depository. If you’re buying physical gold, remember to account for costs like minting, shipping, and insurance. For example, as of February 2026, a 1oz Gold American Eagle MS70 coin is priced at $5,720.17, while smaller denominations like the 1/10oz version start at $586.36.

Once you’ve chosen your investment type, focus on secure storage solutions and consider international options for added protection.

Secure Storage and International Options

When it comes to safeguarding physical precious metals, secure storage is non-negotiable. A solid storage plan should strike a balance between security, accessibility, and protection against both physical dangers and geopolitical uncertainties. This ensures your wealth remains safe during times of market instability or political upheaval.

Safe Storage Options for Precious Metals

For those with substantial holdings, experts suggest a layered storage approach:

- Keep a small emergency stash of 1–3 ounces of coins at home for quick access. While convenient, home safes come with risks like theft, fire, or flood. High-quality burglary-rated safes (look for TL-15 or TL-30 ratings) typically cost between $1,000 and $2,500.

- Store 10–20% of your holdings in a local bank safe deposit box. These offer moderate security with annual fees ranging from $50 to $300, but they lack insurance and are only accessible during bank hours.

- Place the bulk of your assets in a professional depository. Reputable providers like Brink’s, Loomis, or Malca-Amit offer 24/7 monitoring, full insurance, and regular audits. Fees typically range from 0.4% to 1.0% of the asset’s value. For example, some charge 0.5% of the average daily value, while others may be closer to 0.7%.

For maximum security, opt for allocated, segregated storage. This means your metals are assigned to you by serial number and stored separately from other clients’ assets. This arrangement ensures your holdings remain off the custodian’s balance sheet, giving you clear legal ownership.

"For high-value holdings, use a layered storage plan combining professional vaulting with documented insurance and regular audits."

Using International Markets for Wealth Protection

To add another layer of security, consider diversifying your storage internationally. Offshore storage can shield your assets from domestic uncertainties like political instability, sudden policy changes, or even asset freezes. Historical cases, such as U.S. Executive Order 6102 in 1933, highlight the importance of having wealth stored in multiple jurisdictions.

Switzerland is a top choice, refining about 70% of the world’s gold and offering unmatched security through its banking system. Singapore has also gained traction, thanks to its strong privacy laws, no import duties on investment-grade metals, and no reporting requirements for gold and silver holdings.

When choosing an offshore location, focus on countries known for strong property rights, political neutrality, and stable governments. Switzerland, Singapore, and the Cayman Islands are consistently ranked as reliable options. Ensure any offshore storage uses allocated, segregated arrangements to maintain clear ownership, and make sure your insurance coverage explicitly outlines conditions for physical loss.

For U.S. citizens, it’s crucial to stay compliant with foreign account reporting requirements. For example, if the total value of foreign accounts exceeds $10,000 in a year, you may need to file forms like FBAR. Always consult a CPA with expertise in cross-border regulations to ensure you’re meeting obligations under FBAR and FATCA before moving assets internationally.

Conclusion: Building Financial Resilience Through Precious Metals and Commodities

Strengthen your financial foundation by looking beyond traditional stocks and bonds. Precious metals and commodities provide an alternative with lower correlation to conventional assets, offering a much-needed safeguard during market downturns. For instance, gold has delivered an impressive average annual return of nearly 11% over the last 50 years. Even more striking, when inflation (CPI) surpasses 5%, gold prices have historically risen by over 20% on average.

Consider this: since the Federal Reserve‘s inception, the dollar has lost nearly 95% of its value. Meanwhile, gold’s inflation-adjusted gains have exceeded 2,500%. This stark contrast is a key reason financial experts often recommend allocating 6% to 10% of your portfolio to gold. Additionally, commodities exposure – ranging from 3% to 15% depending on your risk tolerance – can further strengthen your portfolio.

Market analysts emphasize gold’s role as a safe haven, particularly during times when investors seek stability outside traditional financial systems. These trends underline the importance of taking proactive steps to protect your wealth.

Now is the time to evaluate your portfolio. Are you prepared for inflation, currency devaluation, or geopolitical instability? Decide whether physical assets, with reduced counterparty risk, or paper investments like ETFs and futures, offering greater liquidity, align better with your goals. Diversify not just within precious metals but across other commodities. Hard commodities like oil and industrial metals can counter inflation, while agricultural commodities can shield against supply disruptions.

At Global Wealth Protection, we make these decisions easier. From setting up Gold IRAs with IRS-approved custodians to arranging secure international storage, our expertise ensures a smoother process. Whether your approach is cautious or bold, professional guidance helps navigate the complexities of physical ownership and the risks tied to paper investments. Reassess your strategy today to safeguard your wealth against future uncertainties. A well-rounded plan now can provide lasting peace of mind.

FAQs

How do I choose between physical metals and ETFs?

When deciding between physical metals and ETFs, your choice will depend on what matters most to you and your investment approach.

Owning physical metals, such as coins or bars, gives you direct control and ownership. However, you’ll need to think about secure storage and insurance, which can add to your costs and responsibilities.

On the other hand, ETFs make investing in metals much simpler. They’re easier to buy and sell, often come with lower costs, and you won’t have to worry about physical storage. The trade-off? You won’t actually own the metal itself.

To make the best choice, weigh factors like storage needs, liquidity, and how actively or passively you want your investment to be managed. Your decision should align with your overall investment strategy.

What’s a simple way to add commodities without futures?

Investing in commodities doesn’t have to involve the complexities of futures trading. You can take a simpler route with commodity ETFs, stocks of companies involved in commodity production, or even by purchasing physical assets like gold and silver. These approaches provide exposure to commodities while keeping things straightforward and offering a way to diversify your portfolio.

How should I store precious metals safely?

To keep your precious metals secure, you have a few solid options: a sturdy home safe, professional storage facilities, or bank depositories. If you opt for home storage, invest in a durable safe that’s properly anchored to deter theft. For those with larger collections or high-value items like gold and silver, professional storage services or bank depositories provide added layers of protection, including surveillance and insurance coverage.