Keeping all your cash in one currency is risky. Inflation, national debt, and sudden policy changes can erode your wealth over time. Diversifying across multiple currencies like the Swiss franc, U.S. dollar, Japanese yen, and euro can help protect your purchasing power and reduce exposure to economic shocks.

Key Takeaways:

- Why Diversify? Inflation and currency devaluation can harm your savings. For example, $100 in 1984 now requires over $300 to match its purchasing power.

- Safe Haven Currencies: Currencies like the Swiss franc and Japanese yen are reliable during market instability due to their economic and political stability.

- Risk Reduction: Holding multiple currencies spreads risk. For instance, in 2025, the U.S. dollar dropped 8% against the yen but remained stable overall due to its global liquidity.

- Managing Multiple Currencies: Options include multi-currency accounts or offshore banking for added jurisdictional protection.

Diversification isn’t about abandoning the U.S. dollar – it’s about safeguarding your wealth in an uncertain financial world.

What Makes a Currency a Safe Haven

Not every currency can step up as a safe haven during financial uncertainty. The ones that do share specific traits, making them dependable stores of value when markets get shaky. Let’s break down what gives these currencies their safe haven status.

Core Characteristics of Safe Haven Currencies

Certain criteria set safe haven currencies apart. Economic stability is a cornerstone – these currencies come from countries with strong economies, low debt-to-GDP ratios, and steady growth. Political stability is equally critical; nations with secure governments, a solid legal framework, and predictable policies inspire confidence in their currencies.

Market liquidity plays a big role too. In times of crisis, high liquidity allows large sums to be exchanged quickly without causing wild price swings. The U.S. dollar, for instance, dominates global foreign exchange trading, offering unmatched liquidity. On the other hand, currencies like the Swiss franc operate in smaller markets, which can sometimes lead to monthly volatility as high as 9%.

"A stable and relatively low inflation environment contributes to a currency’s purchasing power, enhancing its safe haven appeal." – Bob Iaccino, Chief Market Strategist, Path Trading Partners

Low inflation ensures a currency retains its purchasing power, while a negative correlation with stocks and bonds strengthens its appeal as a hedge. Another vital factor is trust in central banks. Investors need confidence that these institutions can handle economic crises effectively. For example, in 2022, the 120-day correlation between the USD and U.S. stocks hit its lowest level since April 2012, showcasing the dollar’s ability to safeguard wealth when equities falter.

Next, let’s look at how holding a mix of these currencies can help spread out financial risk.

How Currency Diversification Reduces Risk

Diversifying across safe haven currencies helps shield your portfolio from economic shocks in any one country. If one economy faces rising inflation, banking restrictions, or policy blunders, your holdings in other currencies remain secure. This strategy limits your reliance on a single economy’s performance.

The way safe haven currencies behave during market stress often depends on the type of crisis. Recent examples highlight the value of diversification. In 2025, the U.S. dollar acted as the "anchor of last resort" during severe systemic shocks, while the Japanese yen and Swiss franc stepped in as "first responders" during more moderate downturns. In the first half of 2025, the dollar dropped about 8% against the yen and 6% against the franc as markets anticipated Federal Reserve rate cuts. By holding all three currencies, you could benefit from their protective qualities no matter the nature of the crisis.

sbb-itb-39d39a6

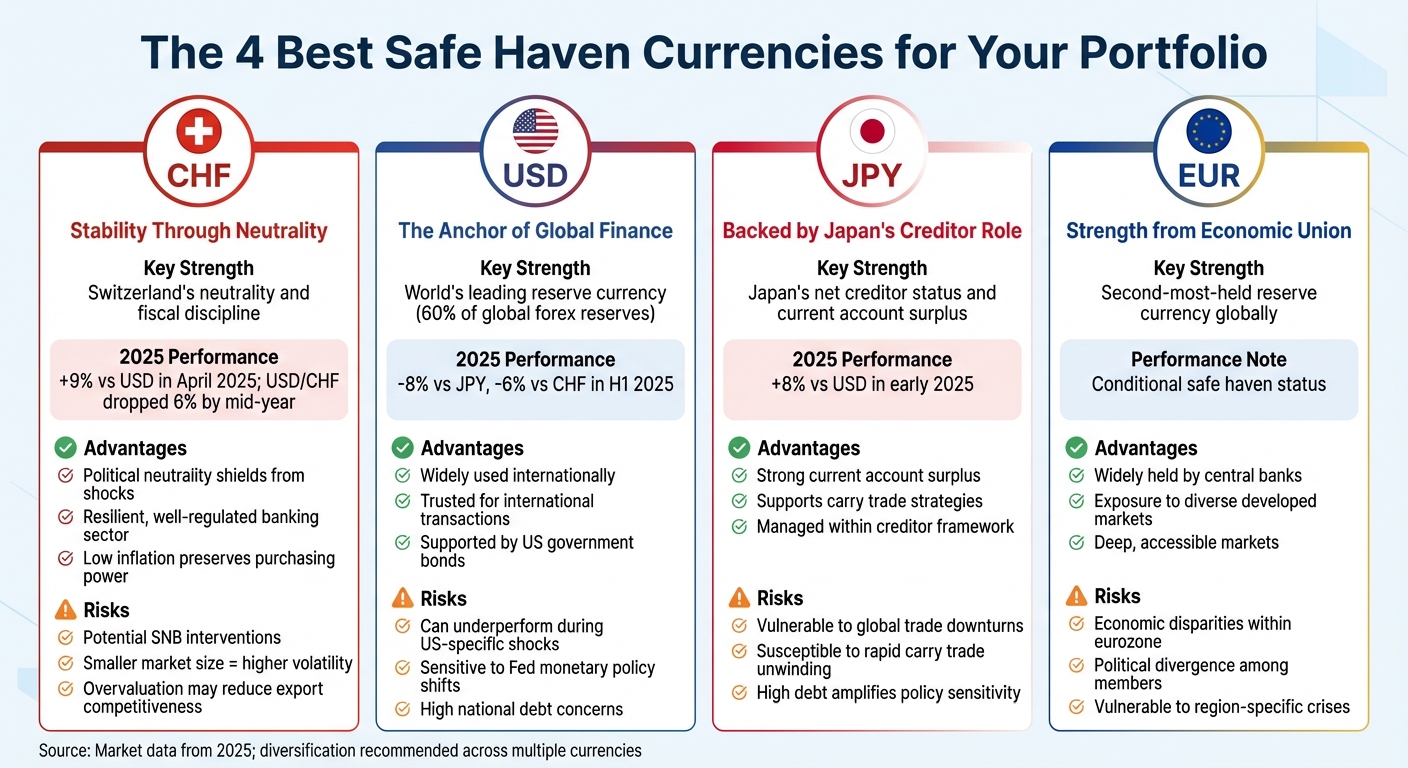

The 4 Best Safe Haven Currencies for Your Portfolio

Safe Haven Currencies Comparison: CHF, USD, JPY, and EUR

Adding safe haven currencies to your portfolio can help protect your assets during times of economic uncertainty. Among the top choices, four currencies stand out for their reliability during market turbulence. Each has its strengths, but they also come with unique risks that require careful consideration.

Swiss Franc (CHF): Stability Through Neutrality and Low Inflation

Switzerland’s long-standing neutrality and fiscal discipline make the Swiss franc a reliable safe haven. The Swiss National Bank (SNB) focuses on maintaining price stability, which enhances the franc’s appeal, especially during market volatility.

"Switzerland’s neutrality and fiscal discipline underpin its safe haven status. Moreover, the Swiss National Bank’s (SNB) commitment to maintaining currency stability attracts safe haven investments." – Bob Iaccino, Chief Market Strategist, Path Trading Partners

For example, in April 2025, trade tensions and geopolitical events drove the franc up 9% against the U.S. dollar. By mid-year, the USD/CHF pair had dropped 6%, demonstrating the franc’s role as a “first responder” during financial stress. However, the SNB sometimes intervenes to prevent overvaluation, which can hurt Swiss exporters. Additionally, the franc’s relatively small market size can lead to sharp price swings.

| Factor | Advantage | Risk |

|---|---|---|

| Political Stability | Neutrality shields the currency from shocks | Potential for SNB interventions |

| Financial System | Resilient, well-regulated banking sector | Smaller market size can lead to higher volatility |

| Inflation | Low inflation preserves purchasing power | Overvaluation may reduce export competitiveness |

These traits make the Swiss franc a strong choice for diversifying your portfolio.

Next, let’s look at the U.S. dollar, the backbone of global finance.

US Dollar (USD): The Anchor of Global Finance

The U.S. dollar is the world’s leading reserve currency, accounting for about 60% of all disclosed foreign exchange reserves held by central banks. Its strength comes from the U.S. economy, political stability, and its widespread use in global transactions. Notably, in 2022, the dollar showed a negative correlation with U.S. stocks, reaching its lowest point since 2012, which reinforced its role as a diversification tool.

In the first half of 2025, the dollar fell 8% against the yen and 6% against the franc as markets anticipated Federal Reserve rate cuts. Despite such fluctuations, the dollar remains a reliable anchor during global crises. As Morgan Stanley pointed out:

"The U.S. dollar played its safe-haven role as expected and helped to diversify portfolios as a result of its negative correlation with global equities." – Morgan Stanley

However, the dollar’s performance can be affected by Federal Reserve policies and the country’s high national debt. It’s also vulnerable to shocks centered on the U.S. economy. Pairing the dollar with other currencies can help create a more balanced hedge.

| Factor | Advantage | Risk |

|---|---|---|

| Global Liquidity | Widely used internationally | Can underperform during U.S.-specific economic shocks |

| Reserve Currency | Trusted for international transactions | Sensitive to shifts in U.S. monetary policy and high debt |

| Treasury Backing | Supported by U.S. government bonds | Lower yields during monetary easing can reduce returns |

The U.S. dollar remains a cornerstone of any diversified currency portfolio.

Now, let’s explore the Japanese yen, which draws strength from Japan’s creditor status.

Japanese Yen (JPY): A Safe Haven Backed by Japan’s Creditor Role

The yen’s reputation as a safe haven stems from Japan’s position as a net creditor nation and its strong current account surplus. During global financial stress, Japanese institutions often repatriate funds, boosting the yen. Additionally, the unwinding of carry trades – where investors borrow at low interest rates to invest elsewhere – further strengthens the currency.

"The yen benefits from Japan’s current account surplus, which provides support during economic downturns." – Bob Iaccino, Chief Market Strategist, Path Trading Partners

In early 2025, the yen gained 8% against the dollar as investors anticipated narrowing yield gaps. The yen often reacts more sharply than the dollar during risk-off scenarios. However, it’s highly sensitive to policy signals from the Bank of Japan, and tightening monetary policies can lead to rapid appreciation.

| Factor | Advantage | Risk |

|---|---|---|

| Creditor Position | Strong current account surplus | Vulnerable to global trade downturns |

| Low Interest Rates | Supports carry trade strategies | Susceptible to rapid unwinding and shifting yield gaps |

| Public Debt | Managed within a creditor framework | High debt levels amplify sensitivity to policy changes |

The yen’s stability makes it a valuable addition to a well-rounded currency strategy.

Euro (EUR): Strength from Europe’s Economic Union

The euro is the second-most-held reserve currency globally, supported by the European Union’s economic power and significant gold reserves. Central banks often include euros in their diversification strategies, which helps stabilize the currency during market stress. However, the euro’s safe haven status is conditional. Economic disparities among eurozone members – where stronger economies like Germany coexist with weaker ones – can undermine confidence in times of crisis.

For U.S. investors, the euro offers diversification away from dollar-centric investments, with deep liquidity and easy access through multi-currency accounts.

| Factor | Advantage | Risk |

|---|---|---|

| Reserve Status | Widely held by central banks | Economic disparities within the eurozone can cause issues |

| Economic Block | Exposure to diverse developed markets | Political and economic divergence among members |

| Liquidity | Deep, accessible markets | Vulnerable to region-specific crises |

The euro provides a solid option for diversifying your portfolio, but it’s important to weigh its regional risks.

How to Hold and Manage Multiple Currencies

Once you’ve chosen the safe haven currencies for your portfolio, the next step is determining the best way to hold and manage them. Your strategy will depend on your priorities – whether you value convenience, asset protection, or spreading your assets across different regions.

Multi-Currency Bank Accounts: Options and Features

Multi-currency accounts allow you to hold, receive, and transact in various currencies without needing to convert them every time. This can save you from paying the spread costs that banks usually charge for conversions. For example, instead of offering the market rate of 0.90 euros per dollar, banks might give you 0.87 euros, effectively charging a 3.3% fee.

If you’re in the US, institutions like Interactive Brokers, Charles Schwab (Global Account), and Citibank (Global Currency Account) provide easy-to-use multi-currency accounts. These accounts are simple to set up, integrate with US tax reporting, and offer high liquidity. However, because these accounts remain within the US financial system, they are still subject to domestic risks like regulatory changes or potential capital controls.

Alternatively, opening accounts in foreign banks located in stable regions – such as Switzerland, Austria, Canada, or Mexico – can provide geographic diversification and reduce exposure to US-specific risks. Switzerland, for example, is well-known for its financial stability and neutrality, making it a solid choice for preserving wealth over the long term. Canada offers easier access for US citizens, especially those near the border, and Mexico can be a practical option if you’re pursuing residency. That said, opening foreign accounts can sometimes be tricky, with compliance reviews causing delays or even account closures.

| Provider Type | Key Features | Jurisdictional Benefits | Accessibility for US Persons |

|---|---|---|---|

| Offshore Bank | Multi-currency support, privacy, asset protection | Separation from US system; low-tax jurisdictions | May require residency or large deposits |

| US-Based Bank | Easy access, tax reporting, regulatory compliance | Falls under US legal framework | Accessible through standard applications |

For US citizens, reporting requirements are a big deal. If your foreign accounts exceed $10,000 at any point during the year, you must file a Foreign Bank Account Report (FBAR). Additionally, Form 8938 under FATCA may apply if your accounts surpass higher thresholds. Non-compliance can lead to severe IRS penalties, so keeping accurate records is essential.

Once you’ve set up multi-currency accounts, consider diversifying across multiple countries to further protect your assets.

Spreading Holdings Across Different Countries

Beyond choosing the right type of account, spreading your assets across different countries adds another layer of security. Keeping all your foreign currencies in a single US-based account leaves you vulnerable to domestic risks like banking failures, capital controls, or regulatory actions. True diversification means holding assets in multiple jurisdictions.

For example, you could keep Swiss francs in a Swiss bank, euros in an Austrian institution, and Canadian dollars in a Canadian account. This approach reduces counterparty risk – the possibility that one institution’s failure could impact all your holdings – and shields you from geopolitical risks like trade restrictions or government actions that could freeze domestic assets.

You might also consider natural hedging. If you have rental property in Europe, you could use euro-denominated rental income to pay for local expenses like maintenance or property taxes.

Finally, align your holdings with your future spending plans. If you’re planning to retire in Switzerland, for instance, holding part of your portfolio in Swiss francs can help protect your purchasing power from currency fluctuations when you need it most.

Conclusion: Building Your Currency Diversification Plan

Managing currency diversification is a practical way to reduce risks during uncertain times. By distributing your cash across reliable currencies like the Swiss franc, US dollar, Japanese yen, and euro, you create a safety net against domestic challenges such as inflation, capital controls, or banking instability. This approach helps maintain your purchasing power across different economies.

Start by evaluating your current and future financial needs. Think about your residency, retirement plans, or even potential international education expenses. These factors will help you decide which currencies should be part of your portfolio. Next, conduct a stress test: imagine your largest currency allocation losing 20% of its value overnight. If this scenario feels alarming, it might be time to adjust that allocation. This test ensures your portfolio can withstand unexpected market shifts.

After fine-tuning your allocations, focus on geographically diversifying your holdings. True diversification isn’t just about owning multiple currencies – it also means keeping your assets in different jurisdictions. For example, holding Swiss francs in a US-based account still exposes you to domestic regulatory risks. To gain real protection, consider opening accounts in countries like Switzerland, Austria, or Canada.

"Managing currency exposures is a dynamic, multi-step process blending quantitative analysis with qualitative judgment." – UBS

FAQs

What factors should I consider when choosing safe haven currencies for my portfolio?

When choosing safe haven currencies, look for those tied to countries known for political stability, strong economic systems, and well-established financial markets. These currencies often maintain or even grow in value during periods of economic or geopolitical turbulence, offering a dependable way to protect your investments.

Some popular examples include:

- U.S. Dollar (USD): Backed by the economic strength of the United States and its role as the world’s primary reserve currency.

- Swiss Franc (CHF): Appreciated for Switzerland’s neutrality, stable governance, and historically low inflation rates.

- Japanese Yen (JPY): Supported by Japan’s durable economy and a strong financial infrastructure.

Spreading your investments across these currencies helps mitigate risks like currency devaluation and brings greater balance to your global cash portfolio.

What are the potential risks of holding multiple currencies?

Holding multiple currencies can add variety to your portfolio, but it’s not without its challenges. One of the biggest concerns is currency volatility. Exchange rates can shift suddenly due to economic changes or global events. Even currencies considered stable, like the Swiss Franc, US Dollar, or Japanese Yen, can see their value fluctuate during uncertain times.

Another issue to consider is the financial health of institutions where you store your foreign currency. If a bank or broker encounters financial trouble, your holdings might be at risk. On top of that, shifts in economic policies or political events in the countries tied to your currencies can directly influence their value. Staying updated on global news is crucial to navigating these risks.

Finally, poor management of your currency exposure can lead to increased portfolio instability. Without a solid plan or hedging strategies, over-reliance on a few currencies or failure to adjust to market conditions can magnify risks. While diversifying across currencies can be a smart move, it demands careful oversight to avoid unexpected losses.

What’s the best way to diversify my cash holdings across different currencies?

Diversifying your cash holdings into multiple currencies is a smart way to guard against risks like currency devaluation or geopolitical instability. Start by assessing your specific currency needs – whether for everyday use, travel, investments, or supporting family members abroad.

Consider focusing on stable "safe haven currencies" such as the US Dollar (USD), Swiss Franc (CHF), and Japanese Yen (JPY). These currencies often maintain their value during periods of economic or political turmoil. Tools like multi-currency accounts or hedging strategies can also help you manage your exposure and reduce potential risks.

Make it a habit to review your currency portfolio regularly and stay updated on global events that could affect exchange rates. This proactive approach can help safeguard your wealth and provide a stronger sense of financial security, even in unpredictable times.