When you sell your startup, the sudden influx of wealth brings new challenges: taxes, lawsuits, and financial risks. Without a plan, your hard-earned gains could quickly erode. Here’s what you need to know:

- Taxes: Capital gains taxes can claim up to 20%, and estate taxes may exceed 50% if not addressed.

- Lawsuits: Wealth attracts legal risks, from frivolous claims to creditor actions.

- Economic Risks: Currency fluctuations and economic instability can impact concentrated wealth.

Key Strategies:

- Act Early: Protect assets before issues arise. Tools like structuring offshore trusts and tax exclusions have strict deadlines.

- Offshore Protection: Jurisdictions like the Anguilla offer legal barriers against U.S. judgments.

- Domestic Options: U.S.-based LLCs (e.g., in Wyoming or Nevada) provide privacy and limit creditor access.

- Diversify Globally: Invest in foreign real estate, multi-currency accounts, and alternative assets to hedge against U.S. market risks.

- Stay Compliant: File necessary tax forms (e.g., FBAR, FATCA) and adjust plans annually to align with changing laws.

The best approach combines domestic and offshore strategies, ensures compliance, and adapts to evolving financial landscapes. Early planning is the foundation for long-term financial security.

Offshore Asset Protection Strategies

After a successful business exit, protecting your wealth becomes a top priority, and offshore strategies can play a crucial role. Moving assets offshore creates a legal barrier, as foreign jurisdictions don’t automatically enforce U.S. court judgments. For instance, if a creditor wins a lawsuit in California, they can’t simply access assets held in another country. Instead, they must go through the legal system of the foreign jurisdiction, which often involves stricter standards and higher hurdles. This makes offshore asset protection a powerful tool for shielding wealth from domestic litigation.

Top Jurisdictions for Asset Protection

Certain jurisdictions have become known for offering strong asset protection laws. Among them, the Cook Islands and Nevis are often considered the top choices for entrepreneurs.

- Anguilla: Anguilla implemented its modern trust structures through the Trusts Act of 1994, which established the foundational legal framework for trusts in the jurisdiction. This legislation was later significantly updated in 2014, introducing major reforms such as the abolition of the Rule against Perpetuities and enhancing flexibility for asset protection, discretionary, and purpose trusts. The International Trust Act of 2007 further refined the legal environment, specifically governing offshore trusts and reinforcing Anguilla’s position as a leading offshore financial center for trust formation.

- Cook Islands: This jurisdiction revolutionized asset protection in 1984 with its International Trusts Act. Creditors face the daunting task of proving "beyond reasonable doubt" that assets were transferred to defraud them – a nearly impossible standard to meet.

- Nevis: Nevis requires creditors to post a $100,000 bond with the Ministry of Finance before filing claims against a trust. Additionally, creditors must hire local attorneys who work on non-contingency fees, and the statute of limitations for claims is only 1–2 years. These legal and financial barriers often discourage creditors from pursuing claims altogether.

- Belize: Belize offers strong asset protection at a lower cost compared to other premium jurisdictions. In the 1994 case SEC v. Swiss Trade and Commerce Trust Ltd., Belize’s Supreme Court upheld its trust statutes, overriding creditor claims – even those backed by Mareva injunctions. This makes Belize a cost-effective option for safeguarding assets.

By leveraging these jurisdictions, individuals can create a robust defense against potential legal threats, particularly when paired with offshore trust structures.

Using Offshore Trusts to Protect Against Lawsuits

Offshore trusts offer another layer of protection by transferring legal ownership of assets to a foreign trustee while you remain the beneficiary. This structure makes it difficult for U.S. courts to claim assets held in the trust.

For added security, many individuals pair an offshore trust with an offshore LLC. In this arrangement, the trust owns 100% of the LLC, and you manage the LLC’s daily operations. If a lawsuit arises, the trustee can activate a "duress clause", which instructs them to ignore court orders attempting to repatriate funds.

Timing is everything when setting up an offshore trust. U.S. bankruptcy law allows a lookback period of up to 10 years for transfers to self-settled trusts. However, jurisdictions like the Anguilla limit this to just 1–2 years. Establishing a trust well in advance of any legal threats ensures you’re outside this vulnerability window.

Costs to set up an offshore trust typically range from $10,000 to $50,000, with annual maintenance fees between $5,000 and $20,000. This makes offshore trusts a practical option for individuals with over $1 million in liquid assets.

Offshore Companies for Tax Optimization and Privacy

While offshore companies don’t reduce your U.S. tax obligations, they offer other benefits like enhanced privacy and legal protection. As a U.S. citizen, you’re required to pay taxes on worldwide income and comply with reporting requirements such as FBAR (FinCEN Form 114) and Forms 3520/3520-A for foreign trusts.

As asset protection attorney Jon Alper explains:

"Offshore asset protection is not a tax strategy. It requires full compliance with all U.S. tax and reporting obligations."

Offshore companies help protect your identity by keeping your name off public registers. For example, an offshore LLC in Nevis or Anguilla can shield your identity and limit creditor actions to liens on distributions. Additionally, these structures provide charging order protection, preventing creditors from seizing LLC assets or interfering with its management.

Offshore companies also simplify access to global markets and allow diversification across currencies and jurisdictions. With the U.S. dollar facing challenges – it experienced its worst six-month start to a year since 1973 – holding assets in multiple currencies can act as a hedge against domestic economic risks. These companies not only enhance privacy but also strengthen broader strategies for protecting wealth after a business exit.

sbb-itb-39d39a6

US-Based Privacy and Protection Tools

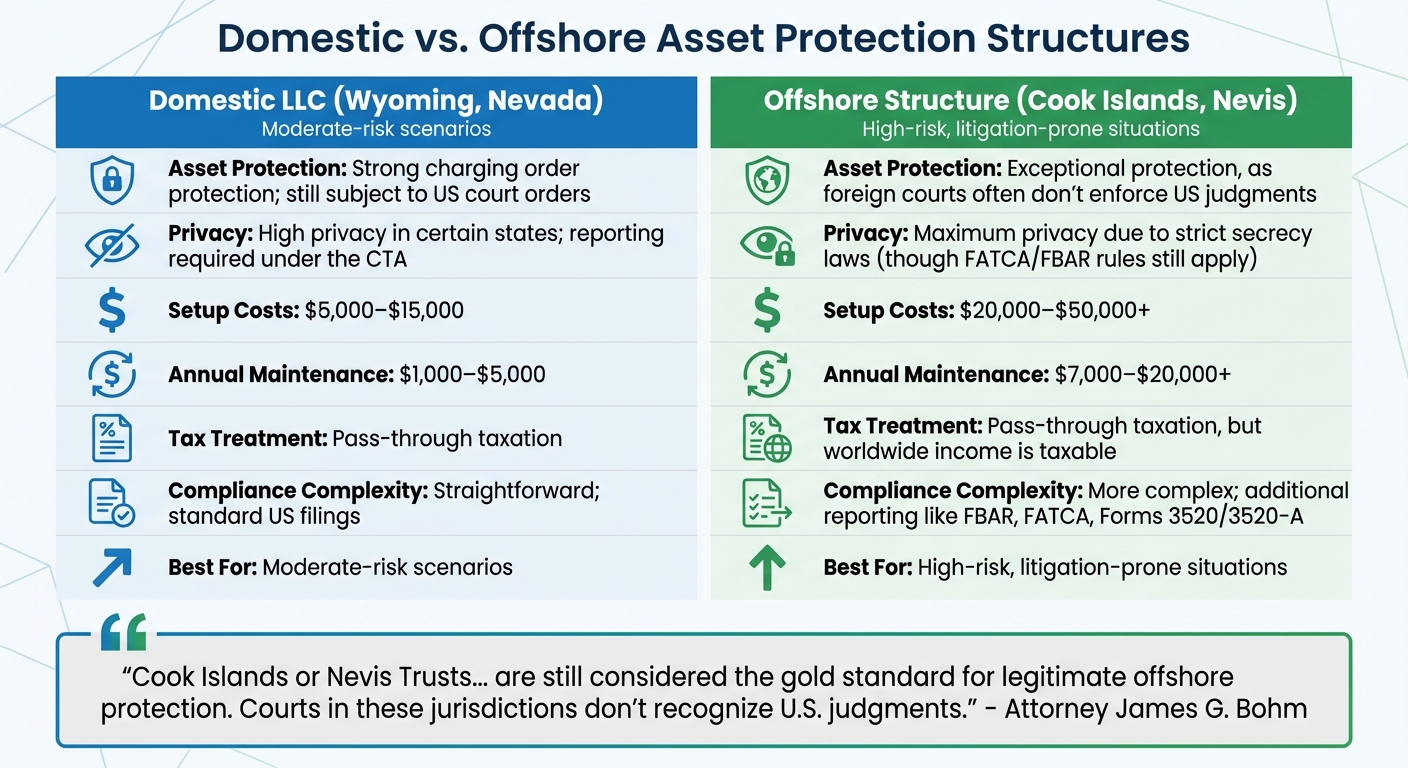

Domestic vs Offshore Asset Protection: Cost, Privacy, and Compliance Comparison

For entrepreneurs, domestic asset protection often stands out for its straightforwardness and ease of access. A private US LLC can safeguard your personal assets – like your home, personal bank accounts, and investments – from business-related debts and lawsuits.

Private US LLCs for Financial Privacy

US LLCs provide charging order protection, which restricts creditors to receiving LLC distributions without allowing them to seize assets or interfere with management.

States like Wyoming and Nevada are particularly appealing for LLC privacy since they don’t require member names to appear on public records. However, the Corporate Transparency Act (CTA) now mandates most LLCs to report Beneficial Ownership Information to FinCEN’s confidential database. This ensures some privacy at the state level but eliminates the possibility of complete anonymity.

LLC founders maintain full control over management while having the option to transfer economic interests to heirs. By gifting non-managing LLC interests at discounts (up to 40%), founders can lower the taxable value of their assets. With the federal lifetime gift and estate tax exemption set at $13.99 million per individual (or $27.98 million for married couples) in 2025, and an annual gift tax exclusion of $19,000 per recipient (or $38,000 for couples), this structure becomes a powerful tool for wealth transfer while minimizing taxes.

The cost to form a domestic LLC typically ranges from $5,000 to $15,000, with ongoing annual fees between $1,000 and $5,000. These relatively manageable costs make domestic LLCs an attractive option for entrepreneurs who want solid protection without the added complexity of offshore arrangements.

Offshore vs. Domestic Asset Protection: A Comparison

While private US LLCs offer clear advantages, it’s worth comparing them with offshore structures to understand their strengths and limitations. The choice between the two depends on your specific risk tolerance and asset protection needs. Here’s a side-by-side breakdown:

| Feature | Domestic LLC (Wyoming, Nevada) | Offshore Structure (Anguilla, Nevis, Belize) |

|---|---|---|

| Asset Protection | Strong charging order protection; still subject to US court orders | Exceptional protection, as foreign courts often don’t enforce US judgments |

| Privacy | High privacy in certain states; reporting required under the CTA | Maximum privacy due to strict secrecy laws (though FATCA/FBAR compliance requirements still apply) |

| Setup Costs | $5,000–$15,000 | $10,000–$50,000+ |

| Annual Maintenance | $1,000–$5,000 | $5,000–$20,000+ |

| Tax Treatment | Pass-through taxation | Pass-through taxation, but worldwide income is taxable |

| Compliance Complexity | Straightforward; standard US filings | More complex; additional reporting like FBAR, FATCA, Forms 3520/3520-A |

| Best For | Moderate-risk scenarios | High-risk, litigation-prone situations |

Domestic LLCs are a cost-effective and reliable choice for many, but offshore structures provide unmatched protection against foreign legal claims. For those seeking the best of both worlds, a hybrid approach can be effective. For example, you could use a Wyoming LLC to manage domestic assets while linking it to an offshore trust that activates during legal threats. This strategy combines the simplicity of domestic operations with the robust defenses of offshore jurisdictions.

As attorney James G. Bohm puts it:

"Anguilla is considered the ‘gold standard’ for legitimate offshore protection. Courts in these jurisdictions don’t recognize U.S. judgments."

It’s crucial to establish asset protection measures well in advance of any potential legal disputes. Transfers made after a lawsuit has been filed can be reversed as fraudulent conveyances. Taking action immediately after exiting a business – or as soon as possible – ensures your wealth remains secure.

International Investment Strategies for Growth

Expanding your portfolio internationally isn’t just about diversifying – it’s about building resilience and tapping into global opportunities. While domestic and offshore protections safeguard your wealth, international investments can provide the growth and stability that come from spreading your assets across multiple economies. By doing so, you reduce the risk of being overly reliant on a single market and position yourself to benefit from worldwide economic trends.

International Investment Options

Foreign real estate is a solid choice for those looking to hedge against U.S. inflation and political uncertainties. Destinations like Lagos in Portugal, Panama City, Tulum, and Cabo San Lucas have become hotspots for American investors. These locations boast stable legal systems and promising growth potential, making them attractive options for long-term investment. Holding foreign real estate through an offshore entity can also reduce exposure to domestic liabilities.

Private Placement Life Insurance (PPLI) is another tool for high-net-worth individuals, offering tax-deferred growth, asset protection, and streamlined estate planning. This option typically suits investors with a minimum of $2 million to allocate. Offshore banking, particularly in financial hubs like Switzerland and Austria, provides an effective way to diversify holdings and mitigate currency risks. For instance, Swiss accounts often require a $1 million minimum deposit, while Austrian banks offer entry points between $250,000 and $300,000. With the U.S. dollar losing over 10% against the DXY index in early 2025 – marking its worst six-month performance since the Bretton Woods collapse – multi-currency accounts have become a critical diversification tool.

For added protection, consider precious metals and tokenized assets stored in secure, non-U.S. jurisdictions. With the U.S. national debt surpassing $31 trillion, allocating part of your portfolio to gold or digital assets held offshore can shield your wealth from both sovereign and systemic risks. These strategies not only diversify your holdings but also protect them from domestic legal challenges.

Adding Global Escape Hatch Plans

Wealth protection goes beyond financial instruments – it’s about ensuring mobility. Secondary residencies or citizenships are increasingly popular among high-net-worth individuals aiming to secure their assets. Between 2019 and 2024, demand for investment migration among U.S. citizens skyrocketed by over 900%, driven by concerns about political polarization and regulatory shifts. In 2024 alone, 4,820 Americans formally renounced their citizenship, a 48% jump from the previous year.

"Mobility is no longer a luxury but a necessity for HNWIs seeking to safeguard their assets and access opportunities worldwide." – Global Citizen Solutions

A second passport or residency doesn’t just provide a safety net during domestic crises – it ensures uninterrupted access to your international assets, even in scenarios involving travel restrictions or border closures. Globally, about 25% of high-net-worth individuals hold a significant portion of their assets outside their home countries. For ultra-high-net-worth individuals in the Middle East, this figure climbs to 41%. These mobility strategies complement investments like foreign real estate, offering both financial and physical security during times of uncertainty.

Maintaining and Updating Your Protection Strategy

Keeping your asset protection strategy effective requires ongoing attention. Just like the initial setup, regular updates and adjustments are necessary to safeguard your wealth after an exit.

Reviewing and Adjusting Your Asset Protection

Make it a habit to review your protection strategy every year. Tax laws and enforcement policies are always changing. For example, the "One Big Beautiful Bill Act" (P.L. 119-21) brought new challenges for 2026 tax planning that demand immediate consideration. In addition to annual reviews, reevaluate your strategy after major life events like marriage, divorce, moving to a different country, or acquiring significant new assets.

Keep a detailed inventory of international assets, including title deeds, bank statements, and registration numbers. This step streamlines your annual reviews. Also, regularly confirm your legal domicile and residency status, as these factors affect succession rules and tax obligations. If you rely on local wills for foreign assets, ensure they are carefully drafted to avoid unintentionally revoking your primary will.

"Tax laws may change over time – rates fluctuate, deductions evolve. However, your values, the pillars guiding your wealth decisions, remain steadfast." – Deloitte

One critical point to note: the federal gift and estate tax exemption is expected to drop by 2026 to nearly half the 2025 level, reducing to approximately $13.99 million per person.

Staying Compliant with US and International Laws

Regular reviews should go hand in hand with staying compliant with evolving regulations. Offshore structures, in particular, require consistent oversight to avoid any transactions being classified as fraudulent. U.S. persons with foreign accounts must file FinCEN Form 114 (FBAR) if the total balance exceeds $10,000 at any point during the year. This form is due April 15, with an automatic extension until October 15. Missing this filing can lead to severe civil or even criminal penalties.

Keep an eye on updates related to the Corporate Transparency Act. By early 2025, enforcement of Beneficial Ownership Information (BOI) reporting had been paused by the Fifth Circuit, with Supreme Court arguments scheduled for March 25, 2025. Additionally, monitor annual inflation adjustments to lifetime gift and estate tax exemptions, as these directly affect the amount of wealth you can transfer without incurring taxes. Be aware of how the IRS applies doctrines like "economic substance" and "step-transaction", which allow them to disregard transactions aimed solely at avoiding taxes.

Don’t forget to periodically audit beneficiary designations on your retirement accounts and life insurance policies. These "contract assets" often bypass probate and can override your will. Keeping them up to date is a key part of maintaining a strong asset protection strategy.

Conclusion: Building Long-Term Financial Security

To safeguard your wealth after an exit, it’s crucial to have a well-thought-out, adaptable protection plan in place. The key is to act before potential disputes arise. Transfers made after claims surface can often be reversed as fraudulent conveyances, so early planning is non-negotiable.

A strong asset protection strategy combines domestic and offshore measures. Domestically, tools like umbrella insurance, estate planning, and LLCs serve as your first line of defense. Offshore trusts, in jurisdictions such as the Cook Islands or Nevis, add another layer of security by creating significant legal barriers. By spreading your assets across jurisdictions, you reduce exposure to sovereign risks and economic uncertainties. In today’s climate of rising national debt and currency fluctuations, diversifying your holdings across multiple currencies is also a wise move.

Integrating tax strategies with asset protection further strengthens your financial position. Tax planning isn’t just about saving money – it’s about securing your future. For example, gifting Qualified Small Business Stock (QSBS) to irrevocable non-grantor trusts can extend the $10 million tax exclusion through a technique known as QSBS Stacking. Estate planning tools like Grantor Retained Annuity Trusts (GRATs) and Intentionally Defective Grantor Trusts (IDGTs) allow your assets to grow outside your taxable estate. This shields them from the hefty 40% federal estate tax on amounts exceeding $13.61 million per individual.

"By failing to prepare, you are preparing to fail." – Benjamin Franklin

Compliance is another critical component of asset protection. For offshore structures, adhering to IRS requirements like FBAR and FATCA filings is essential. Modern strategies focus on creating strong legal protections rather than relying on secrecy. With around 5 million new lawsuits filed in the U.S. in 2023 alone, litigation risks are ever-present. By combining domestic and offshore defenses with rigorous compliance and smart tax planning, you can shield your wealth from future threats. However, your strategy must remain flexible, evolving to meet changes in laws, personal circumstances, and economic conditions. This adaptability is the cornerstone of long-term financial security.

FAQs

When is it too late to start asset protection after an exit?

When it comes to asset protection, timing is everything. If risks like lawsuits or tax liabilities are already on the table, it’s often too late to take full advantage of protective measures. The key lies in planning ahead – putting strategies in place long before any potential threats arise. This proactive approach helps minimize exposure and shields your wealth effectively. Once risks become a reality, your options narrow significantly, and the tools available may not work as well.

Do offshore trusts protect me if I’m sued in the U.S.?

Offshore trusts might not offer complete protection in U.S. lawsuits. Courts frequently scrutinize elements such as control, intent, and timing when evaluating these trusts. In some cases, they have managed to override them, especially when the trusts are perceived as tools for hiding assets from creditors or government actions. To navigate the complexities and risks tied to offshore trusts, thorough planning and expert legal advice are crucial.

What filings are required for offshore accounts or trusts?

To stay compliant with U.S. tax laws, you’re required to file the FBAR (FinCEN Form 114) if you have offshore accounts or trusts that meet the reporting threshold. Additionally, you might need to submit IRS Form 8938, depending on your specific financial situation. Make sure all forms are filled out correctly to satisfy these reporting requirements.