Protecting your retirement savings is a critical challenge, especially in a world of economic uncertainty. Here’s the bottom line: relying solely on U.S. systems and the dollar exposes you to risks like inflation, currency devaluation, and legal vulnerabilities. Offshore strategies can help safeguard your wealth by diversifying assets, reducing dependency on a single economy, and providing legal protections.

Key takeaways from the article:

- Why Offshore Wealth Protection Matters:

- The U.S. dollar lost over 10% of its value against global currencies in early 2025.

- Domestic systems are vulnerable, as seen with the Silicon Valley Bank collapse in 2023.

- Retirees abroad have grown from 500,000 in 2016 to 760,000 today, reflecting a shift toward international planning.

- Risks to Retirement Savings:

- Inflation: Even affordable destinations like Portugal have seen rent surges (49% from 2017–2022).

- Taxes: Investing in non-U.S. funds can trigger PFIC rules, leading to tax rates up to 70%.

- Legal threats: U.S. court cases reached 5 million in 2023, making retirees with assets prime targets.

- Currency devaluation: The dollar’s worst six-month performance since 1973 happened in 2025.

- Offshore Strategies:

- Asset Protection Trusts: Jurisdictions like Anguilla offer strong legal barriers against creditors.

- Currency Diversification: Holding assets in stable currencies (e.g., Swiss Franc, Euro) reduces exchange rate risks.

- Privacy: Offshore accounts protect personal information from public records, reducing lawsuit exposure.

- Top Jurisdictions:

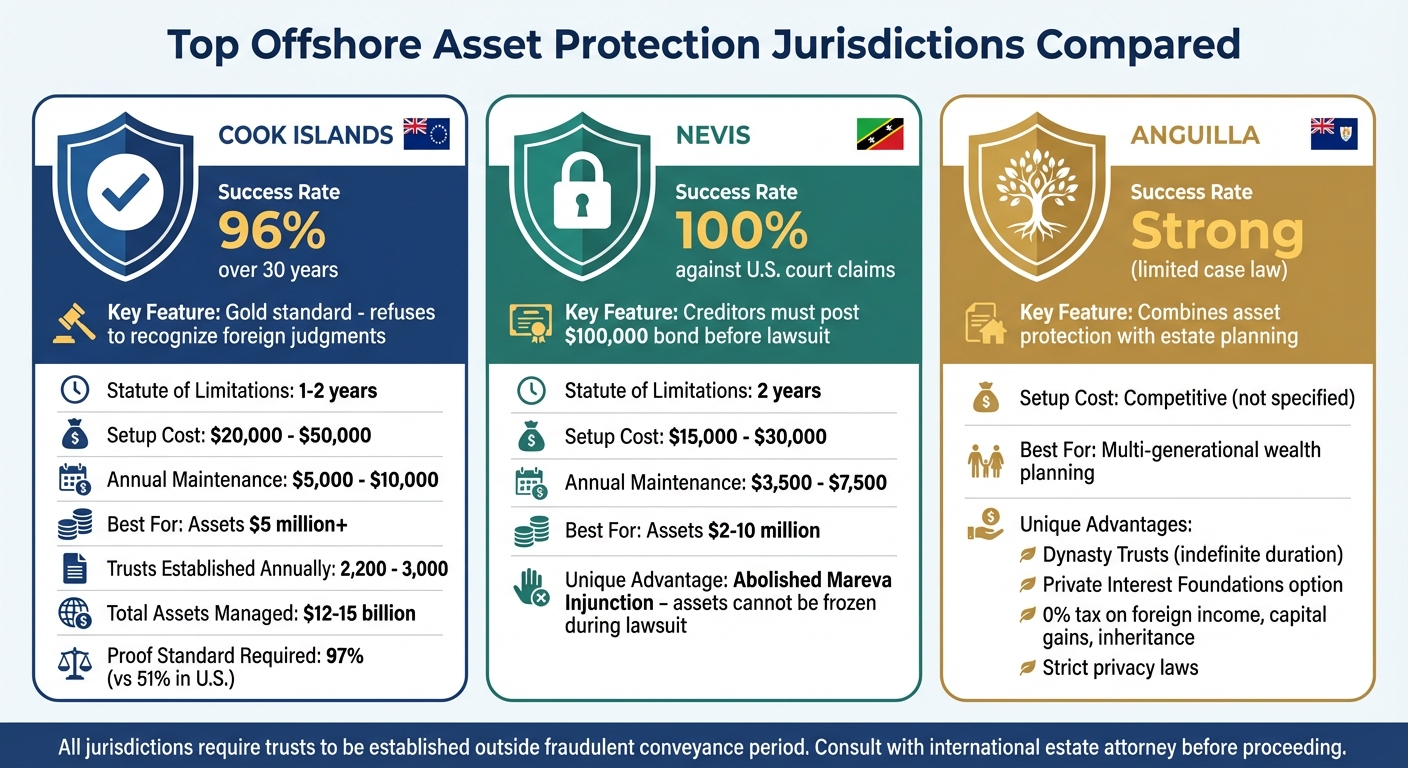

- Cook Islands: High success rate (96%), strong asset protection, but costly ($20k–$50k setup).

- Nevis: 100% success rate, requires creditors to post $100k bond before lawsuits, setup costs $15k–$30k.

- Anguilla: Combines asset protection with estate planning, offers tax-free foreign income.

- Retirement-Friendly Countries:

- Panama, Costa Rica, and Belize offer territorial tax systems, meaning no taxes on U.S. retirement income.

- Greece and Portugal provide flat tax rates on foreign income, making tax planning simpler.

- Implementation Tips:

- Start early to avoid fraudulent transfer claims.

- Work with experts like estate attorneys and international tax advisors.

- Comply with IRS reporting (e.g., FBAR, Form 3520) to avoid penalties.

- Choose jurisdictions based on legal protections, not just cost.

Offshore wealth protection is about creating a multi-layered defense for your retirement savings. By acting early and strategically, you can reduce risks and secure long-term financial stability.

Retirement Wealth Risks and Offshore Benefits

Common Threats to Retirement Savings

Retirement savings face a range of challenges that can chip away at your wealth faster than you might expect. Take inflation, for instance – it quietly reduces your buying power, even in places known for affordability. Portugal is a prime example: property rents there surged by 49% between 2017 and 2022, transforming a once-budget-friendly haven into a pricier option.

Taxes also pose a significant risk. If you invest in non-U.S. mutual funds, you might trigger PFIC (Passive Foreign Investment Company) rules, which could drive your tax rate on investment income up to an eye-watering 70%.

Legal risks are another concern. In 2023 alone, the U.S. saw about 5 million new court cases. Retirees with substantial assets often become prime targets for lawsuits. Once a judgment is issued, domestic assets can be seized under U.S. court orders. On top of that, currency devaluation can further threaten your savings. For example, the U.S. dollar had its worst six-month performance in early 2025 since 1973, dropping over 10% against the DXY index.

And then there’s the banking system. The 2023 collapses of Silicon Valley Bank and First Republic highlighted just how quickly financial institutions can fail. Keeping all your assets within one regulatory framework increases your exposure to systemic risks.

To navigate these challenges, offshore strategies provide a way to diversify geographically and implement legal protections.

How Offshore Strategies Protect Retirees

Offshore strategies can act as a strong defense against these financial vulnerabilities. By allocating your assets across multiple jurisdictions, you tap into legal and financial systems that are globally recognized for their stability. This approach ensures that you’re not overly reliant on the economic or legal conditions of a single country. If one jurisdiction becomes unfavorable, your assets in other regions remain secure.

Certain offshore jurisdictions, like the Cook Islands and Nevis, offer legal frameworks that make it extremely difficult for creditors to access your wealth. Even if a creditor wins a judgment in the U.S., they would need to re-litigate the case in the offshore jurisdiction, which is both time-consuming and costly. Additionally, these jurisdictions require creditors to meet a much higher standard of proof – 97% certainty versus the 51% standard in U.S. civil cases.

Another advantage is currency diversification. Instead of keeping all your assets in U.S. dollars, you can hold accounts in stable currencies like the Swiss Franc or Euro. For retirees living abroad, aligning your investments with the currency of your expenses can help reduce the risk of unfavorable exchange rate fluctuations.

Offshore banking also adds a layer of privacy. While you’re still required to report these accounts to the IRS, offshore structures generally keep your name out of public records. This makes you less of a target for opportunistic lawsuits. Importantly, the goal here isn’t tax evasion but rather safeguarding your wealth through legal means.

Experts often describe this approach as creating a "castle and moat". The combination of geographic diversification, legal protections, and currency hedging forms multiple layers of defense, making it significantly harder for creditors, economic downturns, or currency issues to jeopardize your retirement savings.

sbb-itb-39d39a6

Best Offshore Jurisdictions for Asset Protection

Top Offshore Asset Protection Jurisdictions Comparison for Retirees

When it comes to safeguarding assets, not all offshore jurisdictions are created equal. Each offers varying levels of protection, and the right choice depends on your specific needs, risk tolerance, and financial situation. Among the top options are the Cook Islands, Nevis, and Anguilla, each with its own strengths.

Cook Islands: A Benchmark in Asset Protection

The Cook Islands has set the standard for asset protection trusts since 1984, boasting an impressive 96% success rate over the past three decades. One of its standout features is the refusal to recognize foreign judgments, requiring creditors to restart legal proceedings under local law. Once the statute of limitations – typically 1–2 years – expires, these trusts provide an exceptional level of security.

"The Cook Islands stand as the gold standard in asset protection trusts, with case precedent demonstrating near-impenetrable barriers against foreign judgments." – NTL Trust

Each year, between 2,200 and 3,000 trusts are established in the Cook Islands, managed by 58 licensed trustee companies overseeing $12–15 billion in assets. However, the costs reflect the high level of protection offered, with setup fees ranging from $20,000 to $50,000 and annual maintenance costing $5,000 to $10,000. These trusts are generally best suited for individuals with $5 million or more in assets.

Nevis Trusts: Strong Protections with Added Deterrents

Nevis provides a robust alternative with some unique advantages. One notable feature is the requirement for creditors to post a cash bond of approximately $100,000 before pursuing legal action against a Nevis trust. This upfront cost serves as a significant deterrent to frivolous lawsuits.

"Nevis International Trust statutes have abolished the Mareva Injunction… your opponent cannot freeze your trust assets this way. With the Mareva Injunction out of the picture, your trustee can continue to move funds within the trust during a lawsuit." – Asset Protection Planners

Nevis trusts have demonstrated a 100% success rate in protecting assets from U.S. court claims, provided they are established outside of the fraudulent conveyance period. With a two-year statute of limitations, setup costs range from $15,000 to $30,000, and annual fees fall between $3,500 and $7,500. This jurisdiction is particularly appealing to retirees with assets between $2 million and $10 million.

Anguilla Trusts and Foundations: Protection Meets Estate Planning

Anguilla offers a combination of trusts and private interest foundations, blending asset protection with estate planning benefits. While its case law isn’t as extensive as that of the Cook Islands or Nevis, Anguilla still provides strong protections, such as non-recognition of foreign judgments, short statutes of limitations, and strict privacy laws that keep trust details confidential.

For those familiar with civil-law systems, Anguilla’s private interest foundations might feel more intuitive. These foundations operate like trusts but with a corporate structure, offering more hands-on management options. The jurisdiction also allows for the creation of "Dynasty Trusts", which can last indefinitely, making them ideal for multi-generational wealth planning. Additionally, Anguilla imposes no taxes on foreign-sourced income, capital gains, or inheritance for non-residents, making it an attractive option for retirees seeking tax-efficient strategies.

Each of these jurisdictions offers unique tools and structures for asset protection, forming a solid foundation for further strategies like tax planning and residency programs to safeguard retirement wealth.

Tax-Efficient Structures and Residency Programs

Choosing the right jurisdiction is just one piece of the puzzle when it comes to safeguarding your retirement wealth. Pairing that decision with smart investment structures and residency choices can further protect your assets, reduce taxes, and optimize income streams.

Investment Vehicles That Reduce Taxes

Certain offshore investment tools can help retirees lower their tax burdens significantly. For example, Indexed Universal Life (IUL) policies allow the cash value to grow without being taxed, while annuities let you defer taxes on gains until you make withdrawals. As Steve Azoury puts it:

"Annuities allow the gains on your investment to be tax‐deferred until withdrawn… you can build up your account and delay the taxation while you’re working and in a higher tax bracket"

Unlike traditional retirement accounts, IUL policyholders can access tax-free loans at any age without worrying about early withdrawal penalties.

Tax-managed mutual funds and ETFs are another option. These funds use strategies like tax-loss harvesting and low turnover to minimize capital gains taxes. Without these strategies, investors in the highest tax brackets might lose about 13% of their returns to taxes over a decade.

However, U.S. retirees should steer clear of Passive Foreign Investment Companies (PFICs), as they come with harsh tax treatment, taxing gains at ordinary income rates instead of the more favorable capital gains rates. To avoid double taxation, retirees can use the Foreign Tax Credit (Form 1116), which provides a dollar-for-dollar credit for foreign taxes paid.

Equally crucial is selecting a retirement destination with tax policies that align with these investment strategies.

Retirement-Friendly Countries Compared

Retirement residency programs have become more accessible than ever. Patricia Casaburi, CEO of Global Citizen Solutions, notes:

"Around 61% of programs offer explicit, legally defined tax benefits for retirees, including flat tax rates and exemptions for foreign-sourced pensions"

Even more encouraging, IRS Taxpayer Advocate data reveals that 62% of expats owe $0 in U.S. taxes.

Countries with territorial tax systems, like Panama, Costa Rica, Belize, and Malaysia, only tax income earned within their borders. This means U.S. Social Security benefits, pensions, and investment income remain untaxed in these countries. Panama’s Pensionado program, for example, requires just $1,000 in monthly pension income and includes perks like 50% off entertainment and 25% off utility bills.

Flat-tax systems also offer retirees predictable and straightforward tax planning. Greece, for instance, applies a 7% flat tax rate on foreign-sourced income for up to 15 years, while Italy offers the same rate for 10 years, though only in smaller southern towns with populations under 20,000.

Here’s a closer look at some top retirement destinations:

| Country | Tax Rate on Retirement Income | Residency Requirements | Monthly Cost of Living | Key Benefits |

|---|---|---|---|---|

| Panama | 0% (Territorial) | $1,000/mo pension | ~$2,400 | USD-based economy; 50% off entertainment; 25% off utilities |

| Malaysia | 0% on passive income | $10,000/mo income + $400,000 assets | ~$3,200 | Modern amenities; English widely spoken; MM2H program |

| Greece | 7% flat rate (15 years) | €3,500/mo income | ~$3,500 | EU access; stable tax system; Golden Visa option |

| Portugal | 10% (special regimes) | Passive income (D7 visa) | ~$3,500 | Path to EU citizenship after 5 years; high safety rankings |

| Costa Rica | 0% (Territorial) | $1,000/mo pension | ~$2,800 | Excellent healthcare; Blue Zone longevity; rich natural beauty |

| Belize | 0% (QRP Program) | $2,000/mo income (age 45+) | ~$2,000 | English-speaking; duty-free imports; Caribbean lifestyle |

Interestingly, 93% of countries offering retirement visa programs provide a clear path to citizenship, with dual citizenship often allowed. Additionally, 61% of these programs require monthly incomes of €2,000 or less, and 68% have application fees under €2,000. This makes international retirement an option not just for the ultra-wealthy but also for middle-class retirees seeking a financially secure and fulfilling lifestyle abroad.

How to Implement Offshore Wealth Protection

Getting Started: Action Steps

Securing your retirement wealth internationally requires careful planning and expert advice. The first step? Define your main objective. Are you aiming to shield assets from lawsuits, diversify currencies, reduce taxes, or maintain privacy? Your goal will dictate the structures and jurisdictions that best suit your needs.

Next, take stock of everything you own. Create a detailed inventory of your assets, broken down by country. Include real estate deeds, bank statements, retirement accounts, insurance policies, and investment portfolios. This will help you and your advisors pinpoint which assets need protection and identify any vulnerabilities.

Building the right team is crucial. You’ll need a U.S. estate attorney experienced in outbound wealth planning, local legal experts in the offshore jurisdictions you’re considering, and a tax advisor who understands cross-border treaties (such as a CPA or international tax attorney). The Nestmann Group underscores the importance of professional help:

"Offshore planning is complex and constantly changing. Trying to set everything up yourself based on internet research typically leads to serious problems."

Once your team is assembled, carefully choose your jurisdictions. Look at each location’s legal framework, political stability, and asset protection laws. Common law jurisdictions like the Cook Islands and Nevis often provide stronger trust protections. Then, establish the right legal structures. This could mean setting up an offshore trust, creating an LLC for business assets, or converting retirement funds into a self-directed IRA for international investments.

Opening offshore accounts comes next. Be prepared to provide extensive documentation, as international banks adhere to strict anti-money laundering regulations. Also, ensure your estate documents are aligned. For example, if you create local wills for foreign property, make sure they don’t unintentionally override your primary U.S. will. Consider setting aside cash or life insurance to cover foreign probate fees and inheritance taxes.

Timing is everything. The Nestmann Group puts it plainly:

"It’s like buying car insurance. You can’t get it after you’ve had an accident. By then, it’s just too late."

Set up your protection strategy well ahead of any potential legal threats. If a lawsuit has already begun, asset transfers can be invalidated as fraudulent. Acting early ensures your framework is both secure and legally sound.

Once your offshore strategy is in place, stay vigilant to avoid common mistakes that could weaken your plan.

Mistakes to Avoid

One major misstep is choosing a jurisdiction based solely on cost rather than its legal protections. A low-cost trust in a jurisdiction with weak asset protection laws is essentially useless. Instead, opt for trusted common law jurisdictions like the Cook Islands or Nevis, which don’t recognize foreign court judgments and have short creditor challenge periods.

Another error is appointing friends or family as trustees to save money or retain control. Courts can easily invalidate such arrangements if the trustee lacks independence or proper fiduciary qualifications. Work with professional corporate trustees in the offshore jurisdiction instead. Also, avoid retaining too much personal control over the trust, as this could lead courts to classify the assets as personally owned. To balance protection with oversight, appoint a "protector" who can monitor the trustee’s actions.

Compliance mistakes can be costly. Offshore accounts and trusts don’t mean invisibility to the IRS. U.S. persons must file specific forms, including FBAR (FinCEN Form 114) for foreign accounts exceeding $10,000, Form 3520 for foreign trusts, and Form 8938 for foreign financial assets. Missing Form 3520 alone can result in penalties equal to 35% of the trust’s value or distributions received. Suzanne L. Shier, Partner at Levenfeld Pearlstein, LLC, emphasizes:

"The complexity and penalties for non-compliance are substantial."

Don’t overlook estate planning updates. Create separate wills (known as "situs" wills) for property in different countries to navigate local probate rules and forced heirship laws that could conflict with your wishes. Review your entire strategy annually or after major life events like moving, marriage, or acquiring new assets.

Finally, confirm that your chosen jurisdiction recognizes U.S. powers of attorney. Many don’t, which could leave your assets inaccessible if you become incapacitated. Address this by setting up specific titling arrangements or trusts that allow for asset access during periods of incapacity.

Conclusion: Planning for Long-Term Financial Security

Securing retirement wealth on an international scale calls for a well-rounded approach that addresses multiple risks. With around 760,000 Americans now receiving Social Security benefits while living abroad – an increase from 500,000 in 2016 – more retirees are realizing that careful global planning can greatly enhance their financial stability.

The most effective strategy often combines offshore asset protection trusts, tax-efficient residency options, and coordinated estate planning across borders. For example, trusts in jurisdictions like the Cook Islands or Nevis create strong legal barriers against creditors. The Cook Islands, in particular, requires a 97% proof standard to challenge trusts, compared to the 51% standard in U.S. civil courts.

Tax planning is another critical piece of the puzzle. By leveraging bilateral tax treaties and understanding how different countries – such as France, Italy, and Greece – treat foreign pension income, retirees can reduce tax burdens while remaining fully compliant. Crystal Stranger, Senior Tax Director and CEO of OpticTax.com, highlights a key consideration:

"If you’re a U.S. citizen retiring abroad, you’ll be taxed by the U.S. government on your worldwide income".

This underscores the necessity of thorough preparation and expert advice.

To navigate these complexities, it’s essential to assemble a cross-border team well before retiring. This team might include a U.S. estate attorney, local legal counsel in your chosen retirement country, and an international tax advisor. Together, they can help you maintain liquidity for probate fees, ensure compliance with FBAR and FATCA rules, and align estate documents across jurisdictions.

FAQs

Do I need an offshore trust if I’m not being sued?

An offshore trust isn’t just for people worried about lawsuits. It offers benefits like protecting your assets, maintaining privacy, and streamlining estate planning, even if legal troubles aren’t on your radar. These trusts can shield your wealth while giving you more control over how your financial legacy is managed, making them a smart option for long-term financial planning that goes beyond just legal protection.

How can I diversify currencies without creating a tax mess?

To manage currency exposure without running into tax issues, consider aligning your investments with the currency you’ll need for future expenses, like retirement or housing. This approach helps reduce the risk of currency fluctuations impacting your plans.

Another option is building a multi-currency portfolio, which can spread risk across different regions. However, you’ll need to stay compliant with tax regulations, such as FATCA, and it’s a good idea to consult a financial advisor. They can help you balance diversification with your tax responsibilities and long-term financial goals.

What IRS forms do I need for offshore accounts or trusts?

When dealing with offshore accounts or trusts, you might need to file IRS Form 8938 (Statement of Specified Foreign Financial Assets) and FinCEN Form 114 (FBAR). The forms you must submit depend on the reporting thresholds and the value of the accounts. It’s crucial to check the most up-to-date IRS guidelines to make sure you’re meeting all compliance requirements.