Wealth preservation and wealth accumulation are two distinct financial strategies, and knowing when to focus on each is critical for long-term success. Here’s the difference:

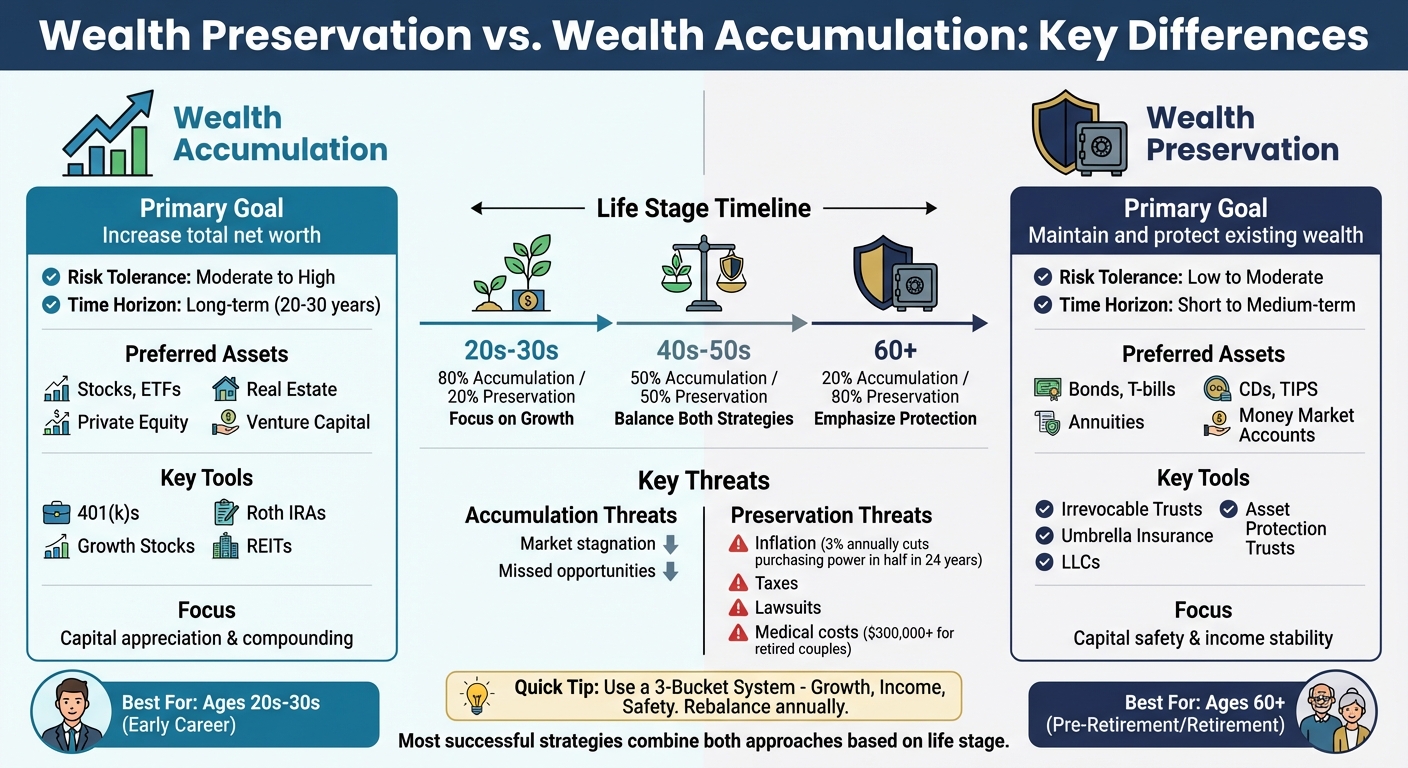

- Wealth Accumulation: Focused on growing your net worth through investments like stocks, real estate, and private equity. It involves higher risk and a long-term timeline (20–30 years).

- Wealth Preservation: Aims to protect your existing wealth from risks like inflation, taxes, market downturns, and lawsuits. It prioritizes stability, income, and lower-risk assets like bonds, T-bills, and offshore trusts for asset protection.

Key Takeaways:

- Accumulation involves growth through higher-risk investments, while preservation prioritizes safety and stability.

- Your financial strategy should align with your life stage:

- 20s–30s: Prioritize growth with stocks, ETFs, and real estate.

- 40s–50s: Balance growth and protection; add tools like umbrella liability insurance. You may also consider offshore asset protection to shield high-value holdings from domestic legal threats.

- 60+: Focus on protecting assets with bonds, annuities, and estate planning.

- Combining both strategies – growth and protection – can create a balanced financial plan that adapts to changing goals.

Quick Tip: Use a three-bucket system (Growth, Income, Safety) to manage assets effectively. Rebalance annually to stay aligned with your goals.

Key Differences Between Wealth Preservation and Wealth Accumulation

Understanding the differences between wealth preservation and wealth accumulation is essential for aligning your financial strategies with your specific goals, especially when it comes to international asset protection.

Protection vs. Growth Goals

Wealth accumulation is all about growing your net worth by investing in assets that aim for long-term gains, even if it means taking calculated risks. On the other hand, wealth preservation focuses on protecting what you already have. It aims to shield your assets from threats like inflation, taxes, market downturns, and legal challenges.

While accumulation strategies prioritize growth through capital appreciation and reinvestment, preservation strategies concentrate on reducing risks, ensuring tax efficiency, and maintaining income stability. This often involves accepting lower returns in exchange for protecting your principal and maintaining liquidity. The shift here is from seeking "more" to ensuring "enough", redefining success as sustainability rather than constant growth.

This difference plays a major role in shaping both your risk tolerance and your investment timeline.

Risk Tolerance and Investment Timeline

The level of risk you’re willing to take and the time you have to invest vary significantly depending on your chosen strategy. Accumulation typically involves a long-term timeline – spanning 20 to 30 years – and a higher tolerance for risk. This approach allows you to weather short-term market fluctuations and recover from temporary losses. In contrast, preservation strategies are more focused on the short- to medium-term. They come with a lower risk appetite, which is especially crucial for individuals nearing or already in retirement.

For example, a retired couple in 2025 might need over $300,000 just to cover out-of-pocket healthcare costs during retirement, not including long-term care. Add to that the impact of inflation – at just 3% annually, inflation can slash the real purchasing power of an investment by half in 24 years. These realities highlight the importance of timing and risk management in wealth preservation.

Preferred Asset Types

The assets you choose will depend on whether your goal is growth or protection. Accumulation portfolios often focus on growth-oriented investments like stocks (particularly growth stocks and small caps), real estate, venture capital, and private equity. Historically, equities have been a reliable driver of returns.

Preservation portfolios, however, lean toward safer, low-risk options. These include U.S. Treasury bills, municipal bonds, certificates of deposit (CDs), money market accounts, and Treasury Inflation-Protected Securities (TIPS). These choices help protect your principal from market volatility and provide the liquidity you might need. Beyond investments, preservation strategies often incorporate tools like umbrella liability insurance, long-term care insurance, and legal structures (e.g., trusts and LLCs) to safeguard wealth from lawsuits, taxes, and unexpected medical costs.

Ultimately, your choice of assets should align with your financial priorities.

"Many clients don’t realize that diversification isn’t just about owning more stocks; it’s about owning the right mix of assets that respond differently to the same event."

– Melody Townsend, CFP, Founder of Townsend Financial Planning

| Aspect | Wealth Accumulation | Wealth Preservation |

|---|---|---|

| Primary Goal | Increase total net worth | Maintain and protect existing wealth |

| Risk Tolerance | Moderate to High | Low to Moderate |

| Time Horizon | Long-term (20–30 years) | Short- to Medium-term |

| Preferred Assets | Stocks, real estate, startups, private equity | Bonds, CDs, T-bills, annuities, insurance |

| Key Threats | Market stagnation, missed opportunities | Inflation, taxes, lawsuits, medical shocks |

| Focus | Capital appreciation | Capital safety and income stability |

sbb-itb-39d39a6

Tools and Methods for Each Strategy

When deciding between strategies for wealth preservation or accumulation, the tools you choose make all the difference. Each approach has its own set of financial instruments tailored to its goals, whether that’s safeguarding what you already have or growing your assets for the future.

Wealth Preservation Tools

Irrevocable trusts are a cornerstone for protecting assets. These structures legally separate ownership from your personal finances, making it harder for creditors to access your wealth. For even stronger protection, Asset Protection Trusts (APTs) – both domestic and offshore – include features like spendthrift provisions to block forced distributions and anti-duress clauses to resist foreign court orders.

Insurance layering adds multiple layers of financial security. Umbrella liability insurance, for instance, extends coverage beyond standard policies and costs around $150 to $300 annually for $1 million in coverage. Long-term care (LTC) insurance is another must-have, especially since 60% to 70% of people will need long-term care at some point. For high-earning professionals, own-occupation disability insurance ensures income protection if they can no longer perform their specific job, even if they could work in another field.

Legal entity structuring is a smart way to shield risky assets. By placing these assets in LLCs or FLPs, you gain charging order protection, which limits creditor access. For added security, you can layer these entities – for example, holding individual LLCs within an irrevocable trust – to create multiple barriers against potential claims.

Treasury securities and other stable options provide a safe haven for your money. U.S. Treasury bills, Treasury Inflation-Protected Securities (TIPS), certificates of deposit (CDs), and money market accounts offer government-backed or FDIC-insured protection. High-yield savings accounts, with APYs exceeding 4% in 2025, combine safety with modest returns.

Wealth Accumulation Tools

Equities are key for long-term growth. Exchange-traded funds (ETFs) and mutual funds offer diversified market exposure, reducing the risk tied to individual stocks.

Real estate builds wealth in two ways: income and appreciation. Rental properties generate cash flow while increasing in value over time. If managing properties feels overwhelming, Real Estate Investment Trusts (REITs) offer a more liquid way to invest in real estate markets. For those with substantial capital, commercial real estate can provide larger-scale opportunities.

Tax-advantaged accounts help your money grow faster by minimizing taxes. Traditional 401(k)s and IRAs allow pre-tax contributions, offering immediate tax benefits, while Roth IRAs use after-tax dollars, enabling tax-free withdrawals in retirement. As of April 1, 2025, IRAs are protected up to $1,711,975 per person in bankruptcy cases. Converting to a Roth IRA during lower-income years can shift funds from tax-deferred to tax-free status at a reduced cost.

Alternative investments bring diversification and the potential for higher returns. Private equity, commodities, and cryptocurrency can offer significant growth, though they come with higher risks and less liquidity. Dollar-cost averaging – investing a fixed amount at regular intervals – helps smooth out market volatility and keeps emotions in check.

Side-by-Side Comparison: Preservation vs. Accumulation

| Feature | Wealth Accumulation | Wealth Preservation |

|---|---|---|

| Primary Objective | Capital Growth & Compounding | Capital Protection & Risk Mitigation |

| Risk Tolerance | High (Market & Volatility Risk) | Low (Focus on Certainty & Safety) |

| Time Horizon | Short to Medium (Active Earning Years) | Long-term (Retirement & Multi-generational) |

| Key Instruments | Stocks, Private Equity, Real Estate, 401(k)s | Trusts, Insurance, Legal Entities |

| Typical Asset Types | Growth Stocks, ETFs, Private Equity | Bonds, TIPS, Offshore Trusts, Umbrella Policies |

| Tax Focus | Tax-deferred Growth | Tax-free Transfers & Estate Tax Reduction |

| Legal Structure | Individual/Joint Ownership | Trusts, LLCs, FLPs |

| Growth Driver | Compounding & Market Expansion | Inflation Protection & Income Stability |

Next, we’ll look at how to align these tools with different life stages to maximize their impact.

Matching Your Strategy to Your Life Stage

Your financial goals and priorities shift as you move through different stages of life. What works for you in your 20s likely won’t be effective in your 60s. Trying to protect wealth too early can also cost you years of growth potential. The key is knowing when to transition from focusing on growth to safeguarding what you’ve built.

Early Career (20s–30s): Focus on Growth

In your 20s and 30s, time is on your side. With decades ahead before retirement, you can afford to take risks, ride out market fluctuations, and let compounding returns work their magic. This is the time to prioritize building wealth.

Your best tools are growth-focused investments like stocks, ETFs, and real estate. Make the most of tax-advantaged accounts such as 401(k)s and Roth IRAs, which allow your money to grow tax-free or tax-deferred for years. Don’t overlook Health Savings Accounts (HSAs); they offer triple tax benefits and can double as supplemental retirement savings if you don’t need the funds for medical expenses.

Protect your income – your most valuable asset at this stage – with disability insurance. If you have dependents, affordable term life insurance is a must.

As your career progresses, you’ll need to start balancing growth with protection.

Mid-Career (40s–50s): Balance Growth and Protection

In your 40s and 50s, you’re likely in your peak earning years. At this stage, the focus shifts to balancing growth with protecting what you’ve worked so hard to build. The question becomes less about earning more and more about ensuring your wealth lasts.

Begin incorporating defensive tools into your financial strategy alongside growth investments. For instance, umbrella liability insurance can protect your savings from lawsuits. As Charles Petitjean, CFP at Barker Wealth Management, explains:

"Umbrella liability insurance is a big one that often gets overlooked. For affluent households, a lawsuit can become a major financial threat".

This is also a good time to consider strategic Roth conversions. If you experience lower-income years during this phase, converting funds from a traditional IRA to a Roth IRA can save you money in the long run. You’ll pay taxes now at a lower rate instead of later when Required Minimum Distributions (RMDs) begin.

If you’re a business owner, start planning your exit strategy. Joshua Mangoubi, CFA and Founder of Considerate Capital, advises:

"Start planning your exit no less than five years before you think you’re ready. The most successful transitions I’ve seen… happen when there’s time to be thoughtful and strategic".

As you approach retirement, the focus will naturally shift toward protecting your nest egg.

Pre-Retirement and Retirement (60+): Emphasize Protection

By the time you’re nearing or into retirement, protecting your assets becomes the top priority. Without active income, your portfolio needs to last for decades, and avoiding major losses early in retirement is critical due to sequence-of-returns risk.

Shift your investments toward income-generating and stable assets, such as bonds, dividend-paying stocks, and annuities. It’s also wise to maintain a "safety bucket" of cash or Treasury bills that can cover two to three years of expenses, so you’re not forced to sell investments during a market downturn.

Healthcare costs take on greater importance at this stage. A retired couple can expect to spend over $300,000 on out-of-pocket medical expenses during retirement. Additionally, since 60% to 70% of people will require long-term care at some point, consider combining traditional health insurance with long-term care (LTC) coverage or hybrid life insurance policies.

Estate planning also becomes crucial. Use trusts to streamline asset transfers, take advantage of the $19,000 annual gift tax exclusion, and keep an eye on the federal estate tax exemption, which is set at $13.99 million per person in 2025 but is expected to drop to approximately $7 million in 2026.

Early retirement years can also be an ideal time for Roth conversions, as your income and tax bracket are often lower before RMDs kick in. This makes it a tax-efficient window to move funds into a Roth IRA.

Combining Both Strategies for Better Results

When it comes to managing your wealth, blending strategies for preservation and accumulation can lead to a more balanced and effective financial plan. The best plans focus on both simultaneously, structuring your portfolio so that different parts serve distinct purposes. By using the right financial tools, you can maximize efficiency and protection.

How to Allocate Your Portfolio

A three-bucket framework is a practical way to organize your assets by purpose. Here’s how it breaks down:

- Growth Bucket: This includes moderate-risk stocks and equity funds aimed at building long-term value and offsetting inflation.

- Income Bucket: Bonds, dividend-paying stocks, and annuities belong here, providing a steady stream of cash flow.

- Safety Bucket: Cash, Treasury bills, and short-term CDs are reserved for immediate liquidity and emergencies.

The idea is to let your Growth Bucket generate returns, which you can then move into the preservation-focused Income and Safety Buckets. This two-bucket transfer strategy helps lock in gains while keeping your risk exposure in check. For instance, if your tech stocks perform well over a few years, you might sell a portion and reinvest the proceeds into dividend-paying stocks or municipal bonds. This way, you’re not abandoning growth but securing what you’ve earned.

To keep this system on track, annual rebalancing is essential. Market fluctuations naturally shift the balance of your portfolio, so reviewing your buckets every year ensures your investments still align with your goals. Melody Townsend, CFP and Founder of Townsend Financial Planning, points out:

"Many clients don’t realize that diversification isn’t just about owning more stocks; it’s about owning the right mix of assets that respond differently to the same event".

Once your allocation framework is in place, you can explore more advanced strategies to further strengthen both growth and protection.

Using International Structures for Protection and Growth

For high-net-worth individuals, multi-layered international structures can support both wealth preservation and accumulation. Different jurisdictions can serve specialized purposes: Singapore for active business holdings, New Zealand for passive investments, and Liechtenstein for multi-generational wealth.

One example of this dual-purpose approach is Private Placement Life Insurance (PPLI). It offers strong creditor protection under local laws while allowing investments within the policy to grow tax-deferred. However, this option typically requires a minimum investment of $2,000,000, making it suitable for those with larger portfolios.

Additionally, asset titling strategies can separate business risks from personal holdings. When combined with international structures, these strategies create layers of protection. Initial setup costs for such sophisticated structures can range from $100,000 to $500,000, with annual maintenance fees between $30,000 and $150,000.

Regular Reviews and Expert Advice

As your strategy evolves, regular reviews are critical to ensure every element – from asset allocation to legal structures – remains aligned with your goals. Your financial situation changes over time due to shifts in income, tax laws, family needs, and market conditions. What worked five years ago might not be effective today. Take the time to review not just your investments, but also your legal structures, insurance coverage, tax strategies, and estate plans.

When dealing with complex strategies, professional guidance is essential. Your financial advisor, tax attorney, and estate planner should work together to ensure all the pieces fit seamlessly. If you’re setting up international structures, the process can take 8 to 24 months to complete due diligence and documentation. Starting early is key to avoiding legal complications, such as challenges under fraudulent transfer laws.

Conclusion

Understanding the distinction between accumulation and preservation is crucial for achieving long-term financial success. Accumulation focuses on growing your wealth through higher-risk investments like stocks and real estate, typically over a 20- to 30-year period. On the other hand, preservation emphasizes safeguarding what you’ve already built, using tools such as trusts, insurance, and low-volatility portfolios.

The most successful investors find a way to balance both strategies, adjusting their approach as life circumstances evolve. For example, younger investors in their 20s and 30s often prioritize growth, while those in their 40s and 50s begin to strike a balance between growth and protection. As retirement approaches, the focus naturally shifts toward preserving assets. As Charles Petitjean, CFP at Barker Wealth Management, explains:

"A good plan does more than distribute assets – it ensures your wishes are honored, taxes are minimized, and your legacy is protected".

By carefully managing the balance between risk and reward, you can create a strong financial foundation. Tailor your strategy to fit your risk tolerance, time horizon, and personal financial goals. With legal and economic risks constantly evolving, it’s essential to establish protection measures early. Doing so helps avoid potential fraudulent transfer claims and ensures your assets remain secure.

Regularly reviewing your plan with a professional ensures it stays aligned with your goals and changing circumstances. Combining growth and protection creates a flexible, resilient strategy that serves you well at every stage of life.

FAQs

When should I shift from wealth accumulation to wealth preservation?

When your focus transitions from building wealth to maintaining it, it’s time to think about wealth preservation. This shift often comes into play as retirement nears, after a substantial increase in assets, or during periods of economic uncertainty.

To protect your wealth and ensure long-term security, consider strategies like diversifying your portfolio, investing in tax-efficient options, and exploring offshore asset protection. These approaches can help shield your assets from risks like market fluctuations and inflation while also supporting stability and legacy planning.

How do I set up a three-bucket strategy for my portfolio?

To implement a three-bucket strategy, start by dividing your assets into three time-based categories:

- Short-term (0-2 years): This bucket is for immediate needs. Focus on liquid, low-risk investments like cash, money market funds, or short-term bonds. These provide quick access to funds while minimizing risk.

- Medium-term (3-7 years): This is for goals a few years down the road. Allocate to intermediate-risk assets, such as balanced mutual funds or bond funds, which offer a mix of stability and moderate growth.

- Long-term (8+ years): Designed for long-term growth, this bucket can include higher-risk investments like stocks or real estate, aiming for higher returns over time.

Make it a habit to regularly review and rebalance your buckets. This ensures you maintain the right mix of liquidity for upcoming expenses and adjust to any shifts in the market or your financial goals.

What offshore asset protection tools fit high-net-worth families?

Offshore asset protection strategies for high-net-worth families often involve using offshore trusts, international business companies (IBCs), offshore LLCs, and foreign bank accounts. These tools are designed to safeguard assets against legal claims, creditors, and potential political risks. Additionally, they offer advantages such as enhanced privacy and effective estate planning options.