Offshore banking isn’t just for the ultra-wealthy – it can help you diversify assets, protect wealth, and access global financial tools. But U.S. citizens face unique challenges due to strict regulations like FATCA and FBAR. This guide ranks the best offshore banks based on three factors: financial stability, privacy, and ease of access for U.S. clients.

Key Highlights:

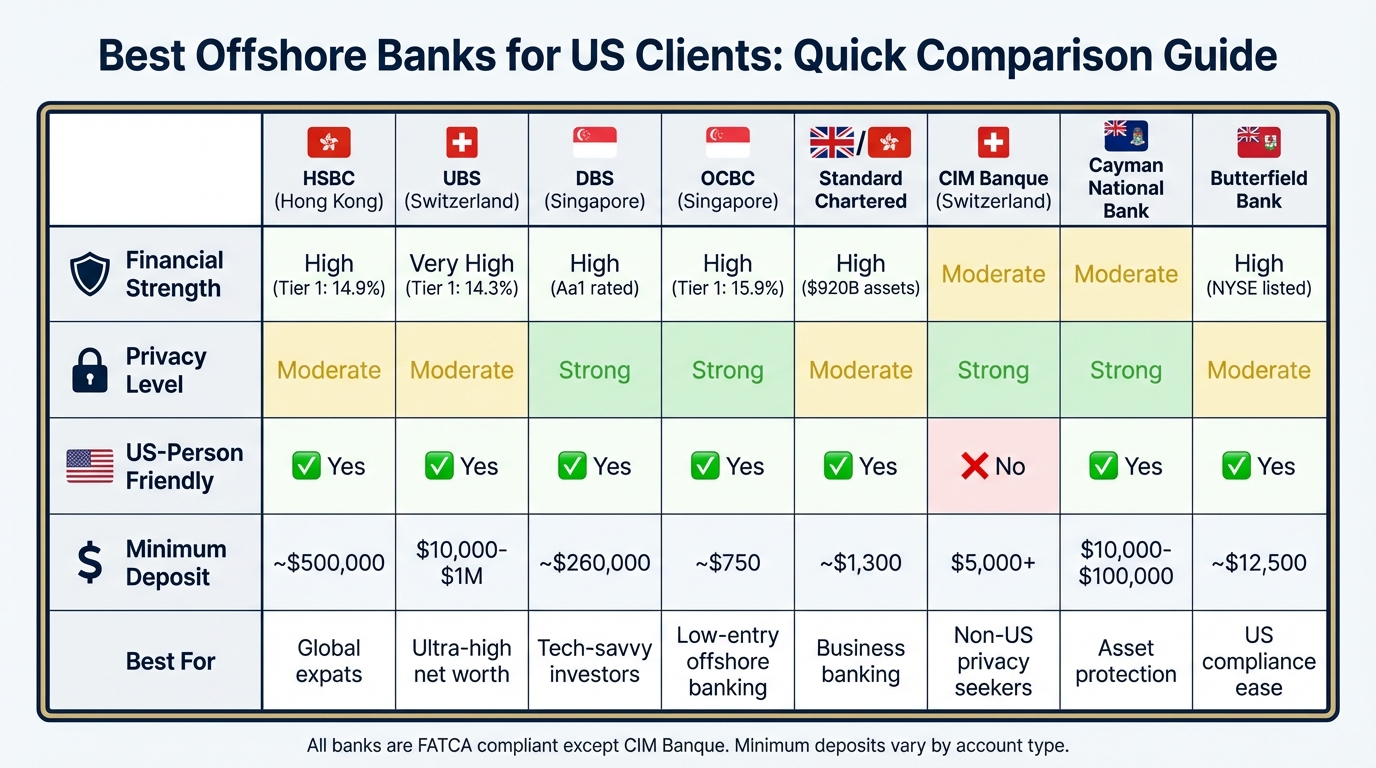

- HSBC (Hong Kong): Large global bank with strong financial stability and tailored services for U.S. clients. Minimum deposit: ~$500,000.

- UBS (Switzerland): Focuses on wealth management with high stability but requires significant assets. Minimum deposit: $10,000–$1,000,000.

- DBS (Singapore): Stable and government-backed, offering multi-currency accounts. Minimum deposit: ~$260,000.

- OCBC (Singapore): Affordable entry point with strong stability and privacy. Minimum deposit: ~$750.

- Standard Chartered: Global presence with a balance of accessibility and compliance. Minimum deposit: ~$1,300.

- CIM Banque (Switzerland): Privacy-focused but less U.S.-friendly. Minimum deposit: $5,000.

- Cayman National Bank: Strong asset protection and privacy. Minimum deposit: $10,000–$100,000.

- Butterfield Bank: Transparent and U.S.-compliant, ideal for high-net-worth individuals. Minimum deposit: ~$12,500.

Quick Comparison:

| Bank | Financial Strength | Privacy | US-Person Friendly | Minimum Deposit |

|---|---|---|---|---|

| HSBC | High | Moderate | Yes | ~$500,000 |

| UBS | Very High | Moderate | Yes | $10,000+ |

| DBS | High | Strong | Yes | ~$260,000 |

| OCBC | High | Strong | Yes | ~$750 |

| Standard Chartered | High | Moderate | Yes | ~$1,300 |

| CIM Banque | Moderate | Strong | No | $5,000+ |

| Cayman National Bank | Moderate | Strong | Yes | $10,000+ |

| Butterfield Bank | High | Moderate | Yes | ~$12,500 |

Each bank has trade-offs, so your choice depends on your financial goals, privacy needs, and compliance requirements. Offshore banking is no longer about secrecy; it’s about diversification and accessing financial tools while staying compliant with U.S. laws.

1. HSBC (Hong Kong/Global)

HSBC is the largest bank based in Europe and ranks 7th globally by total assets, managing around $3.233 trillion as of 2025. This vast capital base offers offshore depositors a high level of security. With operations in 57 countries and a customer base of approximately 39 million, HSBC provides extensive geographic diversification, reducing exposure to risks tied to any single market. Below, we’ll explore HSBC’s financial stability, privacy measures, and services designed for U.S. clients.

Financial Stability

HSBC’s financial health is a standout feature. The bank boasts a Tier 1 capital ratio of 14.9% as of 2025, comfortably exceeding regulatory requirements. Bloomberg has referred to HSBC as "one of the world’s strongest banks by some measures". The bank’s consistent profitability is evident in its 2025 net income of $23.131 billion. For added peace of mind, eligible deposits with HSBC Expat in Jersey are insured up to £50,000 under the Jersey Bank Depositors Compensation Scheme.

Privacy Protections

HSBC places significant emphasis on safeguarding client data. Operating within modern transparency frameworks, the bank ensures that client information is protected from commercial misuse while adhering to FATCA and the Common Reporting Standard (CRS). These frameworks automatically share account details with the appropriate tax authorities. Additionally, HSBC operates under the oversight of strict regulatory bodies, including the Hong Kong Monetary Authority (HKMA) and the Jersey Financial Services Commission (JFSC), ensuring rigorous security measures.

US-Person Friendliness

HSBC has tailored its offerings to meet the needs of U.S. clients. Through its Global View portal, clients can manage both domestic and offshore accounts seamlessly, with fee-free transfers between them. The bank also provides resources like "Tax in USA" guides and access to professional tax referral services for U.S. citizens. Alvaro Teixeira, Head of Wealth and Personal Banking at HSBC Expat, highlights this convenience:

"You gain access to a one-stop solution for managing your banking, wealth, and international payments".

HSBC’s full compliance with FATCA ensures transparency and ease for U.S. clients navigating international banking.

Minimum Deposit Requirements

For non-resident private banking in Hong Kong, HSBC typically requires an initial deposit of $500,000. Meanwhile, HSBC Expat offers new customers 4.50% AER/gross on 6-month deposits within the range of £150,000 to £300,000 (or the USD equivalent). Monthly fees are often waived for Premier status holders or those meeting minimum balance thresholds. Existing HSBC Premier customers may also enjoy streamlined processes when opening offshore accounts.

sbb-itb-39d39a6

2. UBS (Switzerland)

UBS stands as the largest private bank globally, managing over $6.1 trillion in invested assets as of FY24, with projections suggesting this could rise to $6.99 trillion by 2025. The bank serves nearly half of the world’s billionaires and oversees about 25% of global cross-border private assets. Its acquisition of Credit Suisse in March 2023, brokered by the Swiss government, boosted its balance sheet to $1.6 trillion, solidifying its status as a Global Systemically Important Bank (G-SIB). This acquisition, coupled with its tailored services, underscores UBS’s strong foothold in the financial world, including its appeal to U.S. clients.

Financial Stability

UBS demonstrates remarkable financial health with a Tier 1 capital ratio of 14.3% and $71.4 billion in CET1 capital, both comfortably exceeding regulatory requirements. Operating under Switzerland’s AAA sovereign rating, UBS enjoys strong credit ratings: A+ from Standard & Poor’s, Aa2 from Moody’s, and AA- from Fitch. For 2024, the bank reported $5.09 billion in net income. Its designation as a G-SIB by the Financial Stability Board highlights its systemic importance and the accompanying regulatory oversight. On top of traditional banking, UBS also offers secure physical gold storage in fortified facilities within the Swiss Alps.

Privacy Protections

UBS operates under the Swiss Banking Act, which prioritizes client confidentiality by safeguarding against commercial data exposure. However, the era of absolute Swiss banking secrecy has given way to greater regulatory transparency. As Project Black Ledger notes:

"The key distinction of modern offshore banking isn’t privacy – it’s financial sophistication and regulatory efficiency".

UBS adheres to both FATCA and the Common Reporting Standard (CRS), ensuring automatic reporting of account information to the IRS for U.S. clients and to over 100 other jurisdictions. This shift means UBS’s privacy protections focus more on preventing data breaches and commercial surveillance rather than concealing assets from tax authorities.

US-Person Friendliness

UBS has actively expanded its services for U.S. clients, securing a U.S. banking license in March 2026 to enhance its wealth management offerings for American customers. Features include multi-currency accounts in CHF, USD, and EUR, alongside advanced digital asset custody services. However, UBS’s extensive U.S. presence introduces potential vulnerabilities for American clients. Asset protection attorney Gideon Alper explains:

"The protection comes from jurisdictional separation, not secrecy".

This means U.S.-based creditors may be able to access foreign accounts through UBS’s U.S. operations, making it less ideal for those prioritizing asset protection from lawsuits. The onboarding process for U.S. clients is detailed and compliance-heavy, reflecting FATCA requirements. Additionally, U.S. account holders must file an FBAR (FinCEN Form 114) if their total foreign account balances exceed $10,000 at any point during the year.

Minimum Deposit Requirements

UBS offers a range of account tiers, starting with entry-level accounts at $10,000. Non-resident private banking typically requires a minimum of $500,000, while full private banking services start at $2,000,000. Management fees for global wealth management services range between 0.50% and 1.50%. Prospective clients should be ready to provide a detailed, chronological account of their wealth’s origins, as insufficient documentation remains a common hurdle during the application process.

3. DBS Bank (Singapore)

DBS Bank stands as the largest financial institution in Southeast Asia, managing an impressive SGD 739 billion in total assets as of December 31, 2023. With 29% ownership by Temasek Holdings – Singapore’s sovereign wealth fund – the bank benefits from a solid capital base. This government backing, coupled with Singapore’s net assets surpassing 100% of its GDP, creates an exceptionally stable banking environment. Remarkably, no Singaporean bank has ever failed. Adding to its reputation, DBS has been named the "Safest Bank in Asia" by Global Finance for 16 consecutive years (2009–2024). These factors underscore DBS’s financial strength and operational resilience.

Financial Stability

DBS holds stellar credit ratings: Aa1 from Moody’s, AA− from Standard & Poor’s, and AA- from Fitch – ranking among the best in the Asia-Pacific region. In 2022, the bank reported a net income of SGD 8.19 billion (approximately US$6.11 billion). Regulatory changes in 2023 required DBS to allocate S$1.6 billion in additional capital for operational risk. To address this, the bank invested S$80 million to enhance system resiliency. Furthermore, DBS’s artificial intelligence initiatives generated a record S$1 billion in economic value in 2025.

Privacy Protections

DBS places a premium on transparency and privacy. Singapore’s banking regulations emphasize regulatory clarity rather than absolute secrecy. DBS adheres to the Common Reporting Standard (CRS) and the Foreign Account Tax Compliance Act (FATCA), automatically sharing account information with tax authorities in over 100 jurisdictions, including the IRS for U.S. clients. The bank also has comprehensive data protection measures and explicitly states that it does not sell personal data. As Project Black Ledger aptly puts it:

"True wealth protection isn’t about hiding – it’s about structuring".

To further safeguard client accounts, DBS provides hardware tokens that generate one-time passwords every 60 seconds, protecting against phishing and unauthorized access.

US-Person Friendliness

DBS is "FATCA-friendly" and operates a branch in New York, ensuring a physical presence in the United States. U.S. persons can open accounts by submitting tax residency self-certification, including a Taxpayer Identification Number (TIN) or Social Security Number, through the bank’s digibank app. U.S. account holders must comply with FBAR requirements where applicable. Additionally, Singaporean banks, including DBS, do not automatically recognize or enforce U.S. civil judgments, adding a layer of jurisdictional protection for assets.

Minimum Deposit Requirements

DBS Treasures, the bank’s primary international wealth management platform, requires S$350,000 (around US$260,000) in investible assets. For private banking services, DBS Private Bank has a higher threshold, requiring a minimum of US$5,000,000 in investible assets. The bank also offers DBS Remit, which provides same-day, zero-fee international fund transfers via its digibank app. For foreigners living, working, or studying in Singapore, DBS My Account is available with no initial deposit or minimum balance requirement.

4. OCBC (Singapore)

OCBC, Southeast Asia’s second-largest bank, stands out as a solid choice for U.S. persons exploring offshore banking options. With assets totaling S$625.1 billion as of 2024, the bank operates under the watchful eye of the Monetary Authority of Singapore (MAS), which enforces some of the strictest capital and anti–money laundering standards globally. OCBC’s reputation is further cemented by its consistent ranking among the "World’s Safest Banks" by Global Finance, where it secured a top-three spot worldwide in 2022. Add to this Singapore’s highly stable banking environment, and OCBC emerges as a resilient institution backed by a strong government net asset ratio and flawless operational history.

Financial Stability

OCBC boasts impressive credit ratings, including Aa1 from Moody’s and A+ from S&P Global. Its Tier 1 Capital Ratio stood at 15.9% in 2023, well above regulatory requirements. The bank’s extensive presence across ASEAN and Greater China helps diversify its operations, reducing risks tied to any single market. Recognizing its financial strength, The Asian Banker named OCBC Singapore’s strongest bank in both 2018 and 2024.

Privacy Protections

OCBC is committed to safeguarding client privacy. It holds certifications such as the Singapore Data Protection Trustmark and APEC Cross Border Privacy Rules. The bank employs advanced security measures, including SSL 256-bit encryption, two-factor authentication, and automatic session timeouts. It also refrains from selling personal data, as verified by its Cyber Trust Mark and other certifications. While OCBC complies with FATCA and CRS regulations – reporting account details to tax authorities in over 100 jurisdictions – it also adheres to U.S. privacy laws like CCPA/CPRA for its American clients.

US-Person Friendliness

OCBC is a practical option for U.S. clients, offering full FATCA compliance and English-language support. Opening an account requires a Tax Identification Number, proof of wealth, and completion of comprehensive Know Your Customer (KYC) procedures. Non-residents should prepare for a processing period of two to eight weeks, which includes a video consultation as part of the due diligence process.

Minimum Deposit Requirements

OCBC’s minimum deposit requirements depend on the account type. Basic accounts require an initial deposit ranging from S$1,000 to S$5,000 (approximately US$750 to US$3,700), with a minimum balance of S$1,000 to avoid monthly fees. For non-residents without a long-term visa, the minimum deposit typically starts at S$200,000. Higher-tier services, like the Premier Private Client program, require at least S$1.5 million in qualifying assets under management and meeting Accredited Investor status under Singaporean law. Private banking services generally begin at US$1 million or more in assets under management. As an added incentive, new Premier Private Clients depositing S$1.5 million in fresh funds may qualify for cash rewards of up to S$4,000.

5. Standard Chartered Bank

With a history spanning 170 years, Standard Chartered is a UK-based bank with a strong focus on Asia, Africa, and the Middle East. As of 2025, the bank reported total assets of approximately US$919.96 billion and a net income of about US$5.10 billion, with nearly 90% of its profits originating from these regions. Designated as a systemically important bank by the Financial Stability Board, it plays a key role in maintaining global financial stability. For investors seeking asset protection within a transparent and regulated framework, Standard Chartered stands out. It also offers a balanced approach for U.S. clients, ensuring compliance with FATCA while maintaining connections to major financial hubs like Singapore, Hong Kong, Dubai, and London. Below, we explore its financial stability, privacy measures, and services tailored to U.S. clients.

Financial Stability

Standard Chartered’s financial position is solid. In 2025, the bank reported total equity of about US$54.59 billion and annual revenue of approximately US$20.94 billion. It is regulated by the UK’s Prudential Regulation Authority and Financial Conduct Authority and is one of only three banks authorized to issue banknotes in Hong Kong. The bank’s stability is further bolstered by a 17% ownership stake held by Temasek Holdings, a government-owned investment company in Singapore. In March 2025, Standard Chartered introduced an exclusive investment platform for ultra-high-net-worth clients, signaling its strategic shift toward wealth management. This strong foundation underpins its privacy safeguards and U.S.-client services.

Privacy Protections

The bank provides customized wealth management services. While it ensures client privacy from public scrutiny, Standard Chartered adheres to tax transparency laws, complying with FATCA and the Common Reporting Standard. Unlike smaller boutique banks that rely on isolated jurisdictions, it operates within a well-regulated framework across more than 50 markets. Its digital platforms are equipped with secure encryption and cookies to protect online transactions. However, U.S. clients should be aware that the bank’s significant presence in New York and other U.S. locations makes it subject to U.S. court jurisdiction.

US-Person Friendliness

Standard Chartered openly accepts U.S. clients and complies with regulations by reporting customer information to the IRS and verifying tax residency. Back in April 2019, the bank paid US$1.1 billion to resolve investigations into money laundering control deficiencies and sanctions violations, demonstrating its commitment to maintaining its U.S. operational licenses.

Minimum Deposit Requirements

In Hong Kong, standard accounts require a minimum deposit of HKD 10,000 (around US$1,300), with additional fees applied for balances below this threshold. For wealth management services at its advisory centers in Singapore, Hong Kong, Dubai, and London, significantly higher minimum deposits in line with private banking standards are expected.

6. CIM Banque (Switzerland)

Founded in 1990 and based in Geneva, CIM Banque is a Swiss private bank regulated by FINMA. It serves clients across more than 80 countries, with offices in Geneva, Lugano, and Wollerau. The bank focuses on services like multi-currency accounts and wealth management. With Switzerland maintaining an inflation rate of just 0.3% in 2026, the country continues to be an economically stable choice. CIM Banque builds on Switzerland’s reputation for stability and privacy, offering distinct advantages for a select group of international clients.

Financial Stability

CIM Banque adheres to FINMA’s capital adequacy standards and provides deposit protection of up to 100,000 CHF per client. Its multi-currency accounts help reduce foreign exchange risks, and the bank offers Lombard loans with liquidity up to 70% of the portfolio’s loan-to-value ratio. While the bank has lower entry thresholds compared to larger Swiss institutions, its wealth management services are somewhat narrower in scope.

Privacy Protections

CIM Banque upholds strict confidentiality standards, guided by Article 47 of the Swiss Banking Act. Violations of banking secrecy can result in severe penalties, including fines of up to 250,000 CHF and imprisonment. Maurice Aubert explains:

"The mandate of secrecy covers all activities in the banking domain, including the relationship between client and bank, information given by the client about his financial circumstances, the client’s relationship with other banks… and the bank’s own transactions."

The Swiss Federal Constitution also guarantees individuals the right to privacy and protection against misuse of personal data. Although Switzerland participates in the Automatic Exchange of Information (AEOI) and the Common Reporting Standard (CRS), these frameworks only allow for limited data sharing, primarily for tax auditing purposes.

US-Person Friendliness

CIM Banque does not accept U.S. clients subject to FATCA regulations. As noted by Goldblum & Partners:

"CIM Bank does not accept applications from U.S. persons subject to FATCA, offshore companies without substantive business operations, [or] entities from sanctioned jurisdictions."

U.S. citizens looking for offshore banking options may find more suitable solutions with larger international banks that have comprehensive FATCA compliance systems.

Minimum Deposit Requirements

The bank requires a minimum deposit of $5,000 for personal accounts and $10,000 for corporate accounts, with a non-reducible balance of $1,000. Quarterly maintenance fees are 90 CHF (around $103) for personal accounts and 120 CHF (around $138) for corporate accounts. Account opening fees start at 600 EUR (about $650) for proprietary companies and 900 EUR (about $975) for third-party entities. Processing time is typically 10–15 business days for Swiss companies and up to 30 days for more complex non-EU entities.

While CIM Banque offers competitive services, U.S. clients might find better options with larger international banks that cater specifically to FATCA compliance, as outlined in earlier sections.

7. Cayman National Bank (Cayman Islands)

Founded in 1974, Cayman National Bank is part of the Republic Group (Republic Financial Holdings Limited) and stands out as the bank with the largest physical footprint in the Cayman Islands. It operates under the oversight of the Cayman Islands Monetary Authority (CIMA) and holds a Category A license, allowing it to provide comprehensive banking services to both local and international clients. The Cayman Islands Dollar (KYD) maintains a fixed exchange rate with the U.S. Dollar at 1 KYD = 1.20 USD. Let’s take a closer look at its financial stability, privacy policies, and services tailored for U.S. clients.

Financial Stability

The Cayman Islands doesn’t have a depositor insurance system. Instead, asset protection relies on conservative lending practices and maintaining high capital ratios. Mark Nestmann, Founder of The Nestmann Group, highlights this approach:

"Your funds are protected by working with good banks that maintain high capital buffers and keep risky commercial lending to a minimum."

CIMA mandates that banks maintain sufficient capital to absorb economic shocks. Cayman National Bank bolsters this with robust security measures, including 24/7 online monitoring, two-factor authentication, encryption, and fraud prevention training.

Privacy Protections

Cayman National complies with the Cayman Islands Data Protection Act (DPA) and adheres to global transparency standards. It participates in frameworks like the Common Reporting Standard (CRS) and FATCA. In line with these efforts, the Cayman Islands introduced a beneficial ownership registry on February 28, 2025, which increases transparency and modernizes traditional banking secrecy laws. Brandon Roe, Author at The Nestmann Group, notes:

"The Cayman Islands have a solid regulatory system. It aims to keep financial stability, protect clients, and meet global financial standards."

While client data is protected under the DPA, complete anonymity is limited due to the beneficial ownership registry and international reporting obligations.

US-Person Friendliness

Cayman National Bank is fully compliant with FATCA requirements and caters to U.S. clients, requiring W-9 forms for account holders. Accounts are offered in both CI$ and U.S. dollars, making international transactions more convenient. However, non-residents face stricter due diligence compared to locals. U.S. clients opening accounts remotely often need to work through intermediaries or professionals with established ties to the bank. Initial deposits for such accounts may reach up to $1,000,000. Applicants must provide a bank reference letter confirming a relationship of at least three years, proof of funds, and a professional reference from an attorney or accountant. Additionally, U.S. citizens must report their Cayman accounts to the Department of Treasury via FBAR and disclose any income to the IRS.

Minimum Deposit Requirements

| Account Type | Resident Minimum Deposit | Non-Resident Minimum Deposit |

|---|---|---|

| Personal Chequing/EZ Banking | $100 | $1,000 |

| Corporate Account | N/A | $2,500 KYD (~$3,000) |

| Fixed Deposit (USD) | N/A | $5,000 |

| Legacy Builder Savings | $500 | $500 |

Cayman National also offers a Visa Infinite Debit Card with no annual fee. Account opening procedures and processing times vary based on residency and the complexity of the application.

8. Butterfield Bank (Cayman Islands/Bermuda)

Butterfield Bank is another strong offshore banking choice for U.S. clients, following Cayman National Bank in offering a blend of stability, privacy, and accessibility. Established in 1858, it holds the distinction of being one of the oldest financial institutions in the Atlantic region. Butterfield is publicly traded on the NYSE and BSX, which ensures transparency and adherence to regulatory standards. The bank operates in several jurisdictions, including Bermuda, the Cayman Islands, The Bahamas, Guernsey, Jersey, and the U.K. In 2015, it expanded its Cayman Islands operations by acquiring HSBC’s personal and corporate banking business in the region.

Financial Stability

Butterfield Bank’s financial strength is bolstered by its wide geographical reach and prudent risk management practices. After facing challenges in 2010, the bank secured a $550 million capital investment from major players like the Carlyle Group and CIBC, stabilizing its operations. By 2011, it returned to profitability, reporting a net income of $40.5 million. In 2016, the bank went public with a $287.5 million IPO on the NYSE.

The bank consistently earns high credit ratings from Moody’s and S&P, reflecting its conservative approach to credit risk and solid capital reserves. Michael Collins, the bank’s Chairman and CEO, highlighted this focus:

"Our commitment has always been to blend traditional offshore privacy with 21st-century accessibility and accountability."

International Offshore also recognizes Butterfield’s careful management:

"Butterfield has evolved into a publicly listed powerhouse; its disciplined credit exposure has consistently earned strong ratings from Moody’s and S&P."

This disciplined approach underpins its financial resilience and sets the stage for its privacy offerings.

Privacy Protections

Operating in jurisdictions like Bermuda, the Cayman Islands, Guernsey, and Jersey, Butterfield benefits from independent legal systems that do not automatically enforce U.S. civil judgments. This legal separation adds a layer of asset protection not typically available at banks with stronger U.S. ties.

As a publicly traded institution, Butterfield balances client privacy with its obligations for transparency and regulatory compliance. The bank meets all tax reporting requirements while leveraging its jurisdictional setup to enhance privacy. Unlike traditional banking secrecy, Butterfield’s approach focuses on regulatory efficiency and legal safeguards to protect client assets.

US-Person Friendliness

Butterfield Bank is particularly accommodating for U.S. clients. Its NYSE listing provides a strong connection to the U.S., making account opening and compliance processes smoother for American citizens. The bank has invested heavily in compliance systems, including automated FATCA reporting, and employs dedicated teams to handle U.S. tax obligations.

While U.S. clients must still meet FBAR and IRS reporting requirements, Butterfield’s expertise in these areas simplifies the process, making it a practical choice for Americans seeking offshore banking services.

Minimum Deposit Requirements

The Island Saver Instant Access account requires a minimum deposit of £10,000 (approximately $12,500). For non-residents, deposits for Channel Islands accounts range between $100,000 and $250,000. The bank’s updated Schedule of Charges, effective January 2, 2026, may impact fees and other pricing for personal and corporate accounts.

Pros and Cons

Choosing an offshore bank often requires balancing priorities like stability, privacy, and compliance. These priorities can sometimes compete with one another – for instance, greater stability might come at the expense of privacy, while banks that are more accommodating to U.S. clients often involve stricter compliance requirements.

Here’s a breakdown of how some popular offshore banks compare across key factors that matter to American clients:

| Bank | Financial Strength | Privacy Measures | US-Person Compliance | Minimum Deposit | Main Trade-Off |

|---|---|---|---|---|---|

| HSBC (Hong Kong) | Strong global network; premier tier | Limited due to U.S. connections | Excellent (FATCA compliant) | ~$1,300 | Ease of access vs. asset protection |

| UBS (Switzerland) | Top-rated wealth management leader | Moderate; potential U.S. nexus risks | High (Automatic reporting) | $10,000–$1,000,000 | Stability vs. high minimum deposits |

| DBS (Singapore) | Backed by government; AAA-rated | Strong jurisdictional isolation | High (FATCA/CRS compliant) | $750–$3,700 | Low entry barriers vs. strict KYC requirements |

| OCBC (Singapore) | Excellent stability; multi-currency options | Strong jurisdictional separation | High (FATCA compliant) | ~$750 | Affordability vs. monthly fees |

| Standard Chartered | Global reach; corporate banking focus | Moderate; impacted by regulatory changes | High (Premier services) | ~$1,300 | Business tools vs. lengthy due diligence |

| CIM Banque (Switzerland) | Strong private banking services | Strong privacy; remote account setup | High (FATCA compliant) | $10,000+ | Privacy focus vs. higher entry costs |

| Cayman National | Tax-neutral; English common law system | Excellent privacy; no U.S. nexus | High (USD-focused) | $10,000–$100,000 | Asset protection vs. intermediary requirements |

| Butterfield Bank | NYSE-listed; multi-jurisdiction transparency | Good privacy; legal separation | High (Mandatory FATCA compliance) | $10,000+ | Trust benefits vs. higher fees |

This table highlights the trade-offs that U.S. persons often face when exploring where offshore business is heading. For example, while some banks prioritize privacy, they may require higher minimum deposits or more stringent compliance measures.

Jon Alper, an asset protection attorney, puts it succinctly:

"The best offshore bank for asset protection is one that has no branches, subsidiaries, or correspondent relationships in the United States."

The key takeaway? While FATCA compliance is unavoidable for U.S. clients, the true advantage of offshore banking lies in leveraging jurisdictional isolation and accessing financial tools that aren’t readily available within the United States.

Conclusion

Picking the right offshore bank comes down to understanding your financial priorities. If your focus is on wealth management, UBS in Switzerland is a solid choice, thanks to its long-standing reputation. For those seeking financial stability and multi-currency options, DBS and OCBC in Singapore are excellent options, supported by a strong track record and the nation’s robust financial assets.

When it comes to asset protection, look for banks that offer true jurisdictional separation. As offshore consultant Steven James explains:

"Offshore banking for Americans in 2026 is not about escaping oversight. It is about diversifying risk, accessing better tools, and aligning banking infrastructure with a global life."

Banks without U.S. branches or subsidiaries – like smaller Swiss private banks or institutions in the Cook Islands – can provide stronger protection, as U.S. courts generally cannot enforce garnishment orders on them.

Accessibility is another key factor. For those who value ease of access, HSBC offers a convenient option for expats, with minimum deposits starting around $1,300. Meanwhile, CIM Banque allows clients to complete the entire onboarding process remotely via video call.

For U.S. citizens, compliance with FATCA regulations is non-negotiable.

Ultimately, the best offshore bank is one that aligns with your financial goals – whether that means safeguarding assets, exploring international investment opportunities, or managing a global lifestyle with greater financial flexibility. The right choice will balance stability, privacy, and compliance to support your unique financial strategy.

FAQs

What offshore bank is easiest for U.S. citizens to open remotely?

Singapore is widely seen as one of the simplest places for U.S. citizens to open an offshore bank account remotely. The process is generally smooth and often doesn’t require traveling to Singapore, making it a practical option for anyone exploring international banking opportunities.

Will an offshore account be reported to the IRS under FATCA and FBAR?

Offshore accounts typically need to be reported to the IRS under FATCA (Foreign Account Tax Compliance Act) and FBAR (Foreign Bank Account Report) requirements if they surpass specific thresholds. For example, accounts holding over $50,000 in assets often trigger reporting obligations.

To comply with U.S. tax laws, individuals must file Form 8938 (for FATCA) and FinCEN Form 114 (FBAR). These forms help ensure transparency regarding foreign financial assets.

How do I choose between stability, privacy, and asset protection?

When deciding on offshore banking, think about what matters most to you: stability, privacy, or asset protection.

- Stability means choosing a banking environment backed by a strong economy. Countries with solid financial systems often provide a safer place for your money.

- Privacy focuses on keeping your financial information confidential. Some jurisdictions enforce strict laws to protect client data.

- Asset protection is about shielding your assets from legal claims, often by banking in places beyond the reach of U.S. courts.

The key is to weigh these factors based on your financial priorities – whether it’s ensuring security, maintaining confidentiality, or safeguarding your wealth.