Looking for banking privacy in a world dominated by automatic data sharing? Here’s the deal: Most countries now follow the Common Reporting Standard (CRS), a system that automatically shares financial account details across borders. But a few jurisdictions still resist CRS, offering a layer of privacy for individuals and businesses who value discretion.

Here are 7 non-CRS countries where banking privacy remains intact:

- Cambodia: No CRS commitment, straightforward account setup, and a dollarized economy.

- Philippines: Banking secrecy laws still protect accounts, though CRS adoption is expected soon.

- North Macedonia: Non-CRS for now, but EU accession may change this in the future.

- Dominican Republic: High privacy, no CRS participation, and a simple account-opening process.

- Guatemala: Territorial tax system and non-CRS status, but residency is required for accounts.

- United States: Outside CRS, offering privacy for non-U.S. persons, but compliance hurdles are high.

- Armenia: Recently joined CRS, now sharing financial data with 47 countries.

Quick Takeaway:

- Non-CRS countries provide privacy from automatic information exchange, but tax compliance with your home country is still required.

- Consider factors like ease of account opening, tax systems, and potential regulatory changes when choosing a jurisdiction.

Pro Tip: Privacy isn’t about avoiding obligations – it’s about ensuring your financial affairs stay your business. Always consult with professionals to stay compliant with tax laws.

1. Cambodia

Banking Privacy Level

Cambodia stands apart from many jurisdictions because it is not part of the Common Reporting Standard (CRS). Its classification by the OECD as a "developing country not asked to commit" to automatic information exchange gives it a unique position. Unlike countries such as Serbia or Montenegro, which face pressure from the EU to align with CRS, Cambodia operates without such obligations. Adding to its appeal, the banking system is heavily dollarized, with most accounts and transactions conducted in USD. This eliminates the hassle of currency conversions for American clients.

"Cambodia is not part of the Common Reporting Standard – offering true financial privacy." – AsiaOffshoreBanking

Currently, Cambodia does not impose a capital gains tax on individuals, although discussions about introducing such legislation have occurred. For those seeking USD term deposits, interest rates range from 5.5% to 7% annually. The straightforward account opening process further enhances its appeal for individuals prioritizing financial privacy.

Account Opening Requirements for Non-Residents

Opening a bank account in Cambodia as a non-resident is relatively simple. You’ll need a valid passport (with at least six months of validity), a long-term or business visa, proof of address (like a rental agreement or utility bill), and an initial deposit ranging from $10 to $100. If you apply in person, the process typically takes one to two days, making it one of the quicker jurisdictions for account setup.

For those who prefer remote account opening, specialized service providers make it possible. The entire process, including KYC verification and delivery of a physical debit card via DHL or FedEx, generally takes 5 to 10 business days. Fees for remote onboarding are approximately $1,450. Additionally, Cambodian banks facilitate USDT to USD cash-outs with fees around 1.9%.

Major Banks Available

Cambodia offers several banking options for non-residents:

- ABA Bank: Supported by Japan’s SMBC and France’s BRED, this bank provides a user-friendly mobile app for quick account setup.

- ACLEDA Bank: Known as Cambodia’s first licensed commercial bank, it boasts the largest branch network – ideal for those who need in-person access.

- Canadia Bank: With over 260 branches, this bank offers a robust presence across the country.

- Prince Bank: Another accessible option for non-residents.

Most Cambodian banks are integrated with the Bakong system, which allows instant domestic transfers. Additionally, many now support cross-border QR payments through systems like Viet QR and Thai Promptpay.

Potential Risks

While Cambodia’s banking system offers privacy advantages, its regulatory framework is less transparent compared to Western standards. Although there are no immediate plans for Cambodia to adopt CRS, the National Bank of Cambodia introduced new digital asset regulations in December 2024. This suggests a gradual shift towards more comprehensive oversight.

It’s also essential to distinguish between banking privacy and tax residency. Cambodia taxes residents on their worldwide income, so extended stays in the country could lead to unexpected tax liabilities.

As a developing nation, Cambodia’s banking infrastructure is still catching up to the sophistication of more established offshore centers. However, for those who value privacy and the convenience of a dollarized economy, Cambodia remains an attractive option.

sbb-itb-39d39a6

2. Philippines

Banking Privacy Level

The Philippines maintains a banking system that operates outside the Common Reporting Standard (CRS), meaning that major banks like Metrobank and BDO report financial data only to domestic authorities. Banking privacy is safeguarded by Republic Act No. 1405 for peso deposits and Republic Act No. 6426 for foreign currency accounts. These laws ensure strict confidentiality, with the latter requiring both a court order and proof of probable cause before authorities can access account information.

Although the Philippines has pledged to begin CRS automatic exchanges around the 2025/2026 cycle, no firm implementation date has been established. As a "developing country not asked to commit", this status may evolve in the future. Meanwhile, domestic calls to modernize what some consider outdated secrecy laws are growing louder. Cezar Consing of the Bank of the Philippine Islands has noted that "loose money laundering laws combined with strict deposit secrecy can invite illicit funds". For tax purposes, non-residents benefit from the country’s territorial tax system, which generally exempts foreign-sourced income from taxation.

These privacy laws directly impact the process of opening offshore bank accounts in the Philippines, as detailed below.

Account Opening Requirements for Non-Residents

Non-residents looking to open accounts in the Philippines must meet several requirements. These include providing a valid passport, an appropriate visa, an Alien Certificate of Registration (ACR) I-Card, proof of a local address, and a Tax Identification Number for business accounts. The process also involves strict Know Your Customer (KYC) and anti-money laundering checks, which can take up to two weeks. While some banks allow initial applications to be submitted remotely, final documentation typically requires an in-person visit.

For premium or private banking services, banks often require an initial deposit of $10,000 to $50,000. Applicants may strengthen their case by showing signs of stability, such as having a long-term lease or a local driver’s license, as tourist visa holders are often classified as "temporary visitors" and face closer scrutiny.

These requirements highlight the Philippines’ efforts to balance banking privacy with regulatory compliance.

Major Banks Available

The Philippine banking landscape offers a strong mix of local and international options. Leading local banks include BDO Unibank, Bank of the Philippine Islands (BPI), Metropolitan Bank & Trust Co. (Metrobank), and Security Bank. For those seeking high-end private banking services, Metrobank and BDO provide dedicated divisions with English-speaking relationship managers. International banks like HSBC, Citibank, and Standard Chartered also operate in the country, although they may have stricter account opening requirements or fewer branches compared to local institutions.

Additionally, the Philippines benefits from a well-connected banking infrastructure, with strong links to financial hubs such as Singapore, Hong Kong, and Tokyo, enhancing its appeal for international account holders.

Potential Risks

The regulatory environment in the Philippines is evolving, which introduces certain risks. While CRS adoption is on the horizon, the absence of a fixed timeline and potential legislative changes add uncertainty. As Jay Hilotin, Senior Assistant Editor at Gulf News, put it:

"The goal isn’t to spy on honest depositors – it’s to ensure that bank secrecy protects privacy, not plunder".

Ongoing legislative discussions include proposals for the automatic lifting of bank secrecy for public officials and steps to align with global tax transparency standards. Under the Foreign Currency Deposit Act, the Anti-Money Laundering Council (AMLC) can freeze accounts for up to 20 days, pending court approval for an extension. Similarly, the Bureau of Internal Revenue can access account details for tax fraud investigations, but only with a court order.

It’s also important to note that the Philippines’ non-CRS status does not shield account holders from reporting obligations in their home countries. For example, U.S. citizens must still comply with FBAR filings, and UK residents may need to complete self-assessments. Consulting local legal experts or corporate service providers is recommended to navigate these complex compliance and immigration requirements.

3. North Macedonia

Banking Privacy Level

North Macedonia stands out as a non-CRS jurisdiction, offering a higher degree of banking privacy and a tax-friendly environment. The country features a flat 10% income tax and no taxes on capital gains, making it attractive for those seeking discretion in financial matters as part of a broader strategy for offshore asset protection. However, as part of its EU accession process, North Macedonia will eventually need to adopt CRS, DAC8, and other transparency measures.

CitizenX highlights:

"North Macedonia’s financial institutions face no obligation to report foreign account holders to other tax authorities. This gap in automatic information exchange means that banking activities conducted with North Macedonian citizenship remain shielded from the routine financial surveillance that characterizes most developed economies".

That said, North Macedonia complies with FATCA, so U.S. citizens will have their banking data shared with the IRS. Additionally, its membership in NATO and INTERPOL facilitates information sharing in cases involving security or criminal investigations. Despite these factors, the country’s current banking setup allows for a relatively simple account opening process.

Account Opening Requirements for Non-Residents

Non-residents looking to open accounts in North Macedonia need to provide a valid passport, proof of address, and a Tax Identification Number (TIN). The process adheres to standard Know Your Customer (KYC) regulations, although specific requirements may differ slightly between banks. Multi-currency accounts are available, supporting MKD, EUR, USD, GBP, and CHF. Additionally, with North Macedonia joining the Single Euro Payments Area (SEPA) in March 2025, Euro transfers across borders are now more efficient, even though the country remains outside the automatic reporting framework.

Major Banks Available

North Macedonia’s banking sector includes 12 private banks, with foreign entities controlling 73.4% of the market. Nomad Tax comments:

"The banking system in Macedonia is stable, although relatively small. Most banks in the country are under the control of foreign institutions".

Prominent foreign-owned banks operating in the country come from Greece, Slovenia, Turkey, Austria, and Bulgaria, offering infrastructure comparable to European standards.

Potential Risks

While North Macedonia’s current privacy measures are appealing, investors should be aware of potential regulatory shifts. EU accession will eventually require the implementation of CRS and other transparency initiatives, which could reduce the level of banking privacy currently available. However, this transition is not expected to happen immediately, as financial regulatory chapters in the EU negotiations remain open.

Another factor to consider is the country’s integration into Western security frameworks and the dominance of foreign-owned banks. These elements may complicate efforts to leverage dual citizenship for maintaining privacy. As of February 2026, the EU acknowledges North Macedonia as a cooperative jurisdiction, signaling compliance with existing EU cooperation standards. This recognition suggests that the transition to full transparency may occur more smoothly here than in other non-CRS jurisdictions. For investors, it’s crucial to weigh the benefits of current privacy against the likelihood of future regulatory changes.

4. Dominican Republic

Banking Privacy Level

The Dominican Republic stands out for maintaining a high level of banking privacy. It operates outside the Common Reporting Standard (CRS) framework and is not bound by Caribbean transparency mandates. As of January 12, 2026, it remains one of the few banking systems globally that does not participate in the automatic exchange of financial data across 116 jurisdictions. The OECD categorizes the Dominican Republic as a "developing country not asked to commit" to CRS, meaning it faces less international scrutiny compared to countries aiming for EU membership.

This privacy advantage stems from the fact that account information is not automatically shared with foreign governments. Additionally, the country has not signed the multilateral agreement for the Automatic Exchange of Information. On the tax front, foreign-source income is lightly taxed, and there’s no wealth tax. While the banking system adheres to modern Anti-Money Laundering and Counter-Terrorism Financing regulations, discretion remains a hallmark of its operations. Combined with a simple account opening process, this makes the Dominican Republic an appealing option for those seeking financial privacy.

Account Opening Requirements for Non-Residents

Opening an account as a non-resident is relatively straightforward. You’ll need a valid passport, proof of a local address, and a reference letter from your bank. Once these documents are submitted, accounts are typically opened within one to two weeks. Many banks also offer USD accounts, allowing access to freely convertible currency.

Major Banks Available

The Dominican Republic’s banking sector is well-developed, featuring a mix of international and local financial institutions. Scotiabank, for instance, operates alongside prominent local banks such as Banco Popular Dominicano and Banco BHD León. The banking infrastructure is supported by excellent connectivity, with key international airports like Punta Cana International Airport and Las Américas Airport in Santo Domingo offering direct access to the Americas and Europe.

Potential Risks

While the Dominican Republic is expected to remain outside the CRS framework until at least 2031, this status is not set in stone. International pressures could eventually lead to CRS adoption. However, unlike EU accession candidates such as Montenegro, North Macedonia, or Serbia, the Dominican Republic does not currently face a clear mandate or timeline for compliance. Investors should stay informed about regulatory changes and seek professional advice to navigate potential shifts.

5. Guatemala

Banking Privacy Level

Guatemala stands out for its banking privacy, as it operates outside the Common Reporting Standard (CRS) framework and has not signed a FATCA Intergovernmental Agreement with the United States. This non-participation strengthens its reputation for confidentiality in banking.

On top of this, Guatemala follows a territorial tax system, meaning residents are not taxed on foreign-sourced income – it remains entirely tax-free. The country also lacks General Anti-Avoidance Rules (GAAR), Controlled Foreign Corporation (CFC) rules, and taxes on wealth, gifts, or inheritances.

Although Guatemala is a member of the Global Forum on Transparency and Exchange of Information for Tax Purposes, it only exchanges information when specifically requested.

Account Opening Requirements for Non-Residents

To open a bank account in Guatemala, residency is a must. Non-residents can secure residency through two main options:

- Investor Visa: Requires a US$60,000 investment in government bonds for a five-year term.

- Pensionado Visa: Requires proof of passive income of at least US$1,000 per month.

Once residency is obtained, the following documents are typically required to open an account:

- A valid passport

- Proof of a local address

- A bank reference letter

Major Banks Available

While specific bank names are not mentioned, Guatemalan banks provide essential multi-currency account services, making them appealing for asset protection. Both international and local institutions operate in the banking sector, offering a range of financial services.

Potential Risks

One potential concern is Guatemala’s membership in the Global Forum on Transparency and Exchange of Information for Tax Purposes. While the country does not currently participate in CRS, its membership could lead to pressure for future adoption. However, there is no clear timeline for this, and Guatemala is not among the jurisdictions expected to adopt CRS by 2031.

For individuals and businesses, it’s important to note that local income is subject to taxation: 5%-7% for individuals, 25% for corporations, and 10% on capital gains. Proper financial structuring is necessary to ensure foreign-sourced income remains untaxed.

6. United States

Banking Privacy Level

The United States stands out as a unique privacy option for non-U.S. persons, thanks to its position outside the OECD’s Common Reporting Standard (CRS) framework. As the world’s largest non-CRS banking system, the U.S. gathers extensive financial data on its citizens through FATCA but shares information with foreign governments only on a limited basis. For non-U.S. individuals, this creates a privacy advantage, as account details at major banks like JPMorgan or Bank of America are not automatically shared with other countries.

"This asymmetry has made the United States a functional financial privacy jurisdiction for non-US persons, which is precisely why wealth from traditional offshore centers has migrated toward Delaware LLCs, Nevada trusts, and Florida accounts." – Alex Recouso, CitizenX

Tools like Delaware LLCs and Nevada trusts further enhance privacy protections. Unlike CRS jurisdictions, which share account holder details such as names, addresses, tax identification numbers, and balances annually, the U.S. maintains a more selective approach to information sharing.

Account Opening Requirements for Non-Residents

Since 2020, non-residents have faced stricter hurdles when attempting to open U.S. bank accounts. Many major banks have scaled back private banking services for non-resident clients, and remote account openings without a Social Security Number (SSN) are largely unavailable due to stringent KYC (Know Your Customer) requirements under the U.S. Patriot Act.

To open an account, non-residents typically need to visit the U.S. in person with a visa or ESTA and provide:

- Two forms of identification (e.g., passport and driver’s license)

- Proof of address

- A U.S. phone number

Banks such as Bank of America, Citibank, Chase, and TD Bank – especially branches in Florida – are known to be more accommodating to non-residents without an SSN. For business checking accounts, U.S.-based entities like LLCs or C-Corps can often open accounts remotely through platforms like Mercury or Relay. However, foreign-owned LLCs must file Form 5472 with the IRS to avoid penalties, with professional services typically charging around $325 for this filing.

Major Banks Available

Non-residents can access banking services from major institutions like Bank of America, JPMorgan, Citibank, and Chase. These accounts come with FDIC deposit insurance, covering up to $250,000 per qualified account. However, private banking often requires significant minimum deposits, which have become increasingly demanding in recent years.

Potential Risks

The U.S. is unlikely to adopt CRS anytime soon, with no plans to join the framework before 2031 due to limited political incentives for full reciprocity. While this approach has been effective, it also highlights certain contradictions in the system.

The bigger challenge lies in meeting compliance requirements, which have become more difficult for non-residents, especially without a local presence. Non-residents should ensure they use Form W-8BEN (instead of W-9) to reduce tax liability on U.S.-source passive income. Additionally, U.S. persons with foreign accounts exceeding $10,000 at any point in the year must file FBAR reports under the Bank Secrecy Act.

7. Armenia

Banking Privacy Level

As of January 2024, Armenia became a participant in the Common Reporting Standard (CRS). By signing the CRS multilateral agreement, the country began its first automatic exchanges of financial information in September 2025, initially covering 47 countries. Unlike other jurisdictions on this list that remain outside the CRS framework, Armenia now operates with the same level of transparency as EU member states, automatically sharing financial data with foreign tax authorities. While this article primarily highlights jurisdictions that resist automatic reporting, Armenia stands out as an example of a nation that has embraced CRS compliance – something to consider for investors who prioritize financial privacy and asset protection.

"Armenian banks now require CRS self-certifications. Refusal results in account denial." – CitizenX

Notably, Armenia and Russia began exchanging financial data on December 31, 2024. This is particularly significant for Russian nationals who moved to Armenia after 2022. Armenia’s shift toward transparency sets it apart from the other jurisdictions in this list, which continue to resist CRS obligations.

Account Opening Requirements for Non-Residents

Even with its CRS obligations, Armenia allows non-residents to open bank accounts, though full financial disclosure is now mandatory. Non-residents do not need a residence permit to open an account, but they must demonstrate a "proven economic connection" to the country. The account opening process usually takes 1 to 5 working days. Additionally, all applicants must complete a CRS self-certification form that outlines their tax residency information; refusal to comply results in immediate denial.

Potential Risks

The main risk of banking in Armenia is the complete lack of financial privacy. Unlike jurisdictions such as the United States or the Philippines, which remain outside the CRS framework as of 2026, Armenia has shifted from being a "privacy haven" to a fully compliant CRS participant. Holding an Armenian account now entails full financial disclosure to tax authorities in any of the 47 partner jurisdictions. Current account holders should ensure their local tax filings are accurate and up to date to avoid penalties. Armenia’s inclusion in this list serves more as a cautionary tale than as a viable option for those seeking financial privacy. Unlike other jurisdictions listed, Armenia no longer offers the banking confidentiality sought by non-CRS clients.

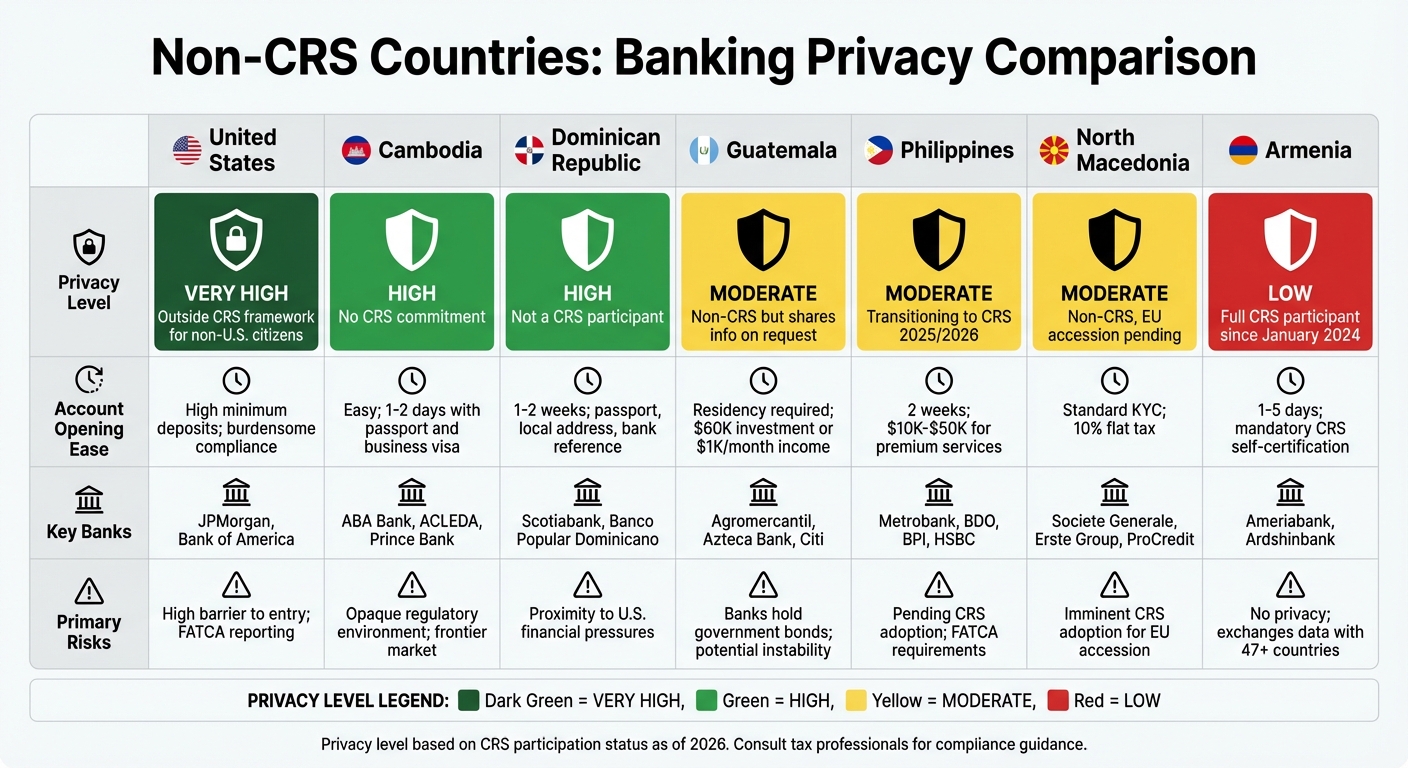

Privacy Features Comparison

The table below highlights the privacy features of various jurisdictions, offering a side-by-side comparison of privacy levels, account opening requirements, major banks, and associated risks. This breakdown aims to help you make informed decisions about privacy-focused banking.

| Country | Privacy Level | Account Opening Requirements | Key Banks | Primary Risks |

|---|---|---|---|---|

| United States | Very high for non-U.S. citizens; outside CRS framework. | High minimum deposits; burdensome compliance for non-residents. | JPMorgan, Bank of America. | High barrier to entry; FATCA reporting for U.S. persons. |

| Cambodia | High; no CRS commitment or imminent plans. | Easy; 1–2 days with passport and business visa. | ABA Bank, ACLEDA, Prince Bank. | Opaque regulatory environment; frontier market status. |

| Dominican Republic | High; not a CRS participant. | Passport, local address, and bank reference letter. | Scotiabank, Banco Popular Dominicano, Banco BHD León. | Proximity to U.S. financial pressures. |

| Guatemala | Moderate; non-CRS but shares info on request. | Standard KYC; often requires local presence. | Agromercantil, Azteca Bank, Citi. | Banks hold significant government bonds; potential instability. |

| Philippines | Moderate; transitioning to CRS exchanges in 2025/2026. | Passport and proof of address; $10,000–$50,000 for premium services. | Metrobank, BDO, BPI, HSBC. | Pending CRS adoption and FATCA requirements. |

| North Macedonia | Moderate; non-CRS, EU accession pending. | Standard KYC; 10% flat tax environment. | Societe Generale, Erste Group, ProCredit Bank. | Imminent CRS adoption required for EU accession. |

| Armenia | Low; now a full CRS participant. | Strict CRS self-certification; high documentation. | Ameriabank, Ardshinbank. | No longer offers non-CRS privacy; exchanges data with 47+ countries. |

The United States stands out for its high level of privacy for non-U.S. citizens, though it comes with steep financial and compliance hurdles. Cambodia, on the other hand, offers a quick and straightforward account setup process, making it appealing for those seeking immediate privacy.

Countries like North Macedonia and the Philippines are in transitional phases. While they currently operate outside the CRS framework, both are under growing pressure to adopt automatic data exchange standards. These shifts could significantly alter their appeal for privacy-conscious individuals in the near future.

Armenia illustrates how quickly privacy protections can erode. Once seen as a reliable option, it now complies with CRS regulations, sharing financial data with over 47 countries. This serves as a reminder that jurisdictions can change their policies rapidly, often in response to international pressures.

When choosing a jurisdiction, it’s crucial to weigh both the current privacy landscape and potential future changes. Countries under scrutiny for EU accession or international compliance are likely to adopt CRS requirements sooner than expected, which could impact their suitability for privacy-focused banking. Carefully assess these factors to find the best fit for your financial privacy needs.

Conclusion

Non-CRS jurisdictions offer a level of financial privacy that stands in contrast to the automated reporting systems of CRS countries. The seven nations discussed here – Cambodia, the Philippines, North Macedonia, the Dominican Republic, Guatemala, the United States, and Armenia – each bring their own mix of benefits and challenges for those prioritizing privacy.

The main advantage is straightforward: no automatic exchange of financial information. Unlike CRS jurisdictions, these countries only share data when specific legal requests are made.

"The value of non-CRS banking is privacy from automatic information sharing, not exemption from your own legal obligations." – CitizenX

That said, privacy isn’t the only factor to weigh. When choosing a jurisdiction, consider practical elements like currency compatibility, ease of travel, and political or economic stability. For instance, dollarized economies such as Cambodia and the Dominican Republic make USD transactions seamless, while the United States remains a strong privacy option for non-U.S. citizens – albeit with significant entry barriers. However, keep in mind that countries like North Macedonia, which are under pressure to join the EU, may transition to CRS compliance sooner than expected, limiting their current non-CRS advantages.

Finally, it’s crucial to understand that non-CRS banking protects against automatic data sharing but does not exempt you from tax obligations. For example, U.S. citizens must still file an FBAR for foreign accounts exceeding $10,000. Always consult with qualified professionals to ensure compliance with your home country’s tax laws. Your choice of jurisdiction should balance privacy with practical factors like currency use, accessibility, and regulatory stability to achieve effective asset protection. This often involves structuring offshore trusts to further insulate wealth from legal risks.

FAQs

Is non-CRS banking still legal if I report everything at home?

Yes, banking in non-CRS jurisdictions is perfectly legal – as long as you fully report your accounts to your home country. The Common Reporting Standard (CRS) is simply a framework for sharing financial information between participating countries. It doesn’t impose any legal or tax obligations. If you meet your country’s reporting requirements, you can legally maintain financial privacy while using banks in non-CRS jurisdictions.

How can I tell if a non-CRS country might adopt CRS soon?

Countries not currently participating in the Common Reporting Standard (CRS) may choose to adopt it by signing international agreements such as the Multilateral Competent Authority Agreement on Automatic Exchange of Financial Account Information. For instance, places like the Cayman Islands and Guernsey committed to CRS after entering into these agreements. Keeping an eye on these developments is crucial for understanding potential shifts in a country’s CRS status.

What’s the safest way to open a non-resident account without getting rejected?

To open a non-resident account, make sure all your paperwork is in order. This typically includes a valid passport, proof of address, and documentation verifying your source of funds. Double-check that everything is accurate, complete, and aligns with the local banking requirements.

When selecting where to open the account, pick a jurisdiction that aligns with your privacy preferences and compliance obligations. It’s often helpful to consult professionals who are well-versed in the specific banking laws of that region.

If the bank requests additional information or schedules an interview, respond quickly and thoroughly. This shows your willingness to cooperate and can help smooth the process, reducing the chances of your application being denied.