Offshore priority banking is designed for high-net-worth individuals managing wealth internationally. It offers exclusive services like personalized financial management, private family office services, multi-currency accounts, and custom wealth strategies. Clients benefit from financial privacy, access to global investments, and offshore asset protection structures. Popular jurisdictions include Switzerland, Singapore, and the UAE, each offering unique advantages for wealth management. However, compliance with global regulations like CRS and FATCA is essential.

Key Takeaways:

- Exclusive Services: Dedicated relationship managers, multi-currency accounts, and tailored wealth solutions.

- Financial Benefits: Privacy, global investment access, and tax optimization.

- Top Jurisdictions: Switzerland for safety, Singapore for Asian market access, UAE for tax advantages.

- Compliance: Adherence to CRS and FATCA ensures transparency and legal protection.

Offshore banking is no longer about secrecy but about structured, compliant strategies for wealth growth and protection.

Main Features of Offshore Priority Banking

Offshore priority banking stands out from standard banking by offering three key features: personalized relationship management, multi-currency accounts, and customized wealth management solutions. These services are specifically tailored to meet the needs of high-net-worth individuals with cross-border financial interests.

Dedicated Relationship Management

Clients of offshore priority banking are assigned a personal relationship manager who acts as their main point of contact, delivering tailored financial advice. These managers handle a wide range of services, including investment strategies, estate planning, specialized lending, and global mobility solutions. For instance, Barclays International provides dedicated managers to clients maintaining significant account balances, while DBS Private Bank in Singapore operates with similarly high thresholds.

Relationship managers also assist with managed portfolio services and custom portfolio construction. They play a vital role in estate and succession planning, offering services such as trust planning, will writing, and inheritance strategies – key for ultra-high-net-worth families.

As Nav Singh, Head of International Markets at Barclays, explains: "Our local expertise can help you find ways to diversify your wealth, unlock opportunity in multiple countries, and keep your assets safe and secure".

Multi-Currency Accounts

A multi-currency account allows clients to hold, send, and receive funds in various currencies from a single account. This feature works hand-in-hand with the advisory services provided by relationship managers, reducing the need for constant currency conversions, lowering associated fees, and protecting against exchange rate fluctuations. For example, the Wise platform supports over 50 currencies, making it a popular choice for such needs.

These accounts are particularly useful for individuals with international commitments, such as owning overseas properties, paying foreign school tuition, or supporting family members abroad. They also act as a safeguard against inflation and currency devaluation by enabling users to store funds in stable currencies like the Swiss franc. However, with the introduction of CRS 2.0 regulations on January 1, 2026, digital wallets and e-money accounts will also become reportable, except for low-risk accounts under $10,000 over a 90-day period. Clients must ensure compliance by declaring all offshore holdings to the appropriate tax authorities.

Customized Wealth Management Solutions

Offshore banks go beyond currency management by offering wealth management strategies tailored to individual goals. These strategies are designed to match each client’s risk tolerance and growth objectives. Offshore priority banking opens access to international markets and asset classes that may not be available domestically, such as opportunities in Asia or Europe.

Wealth managers focus on diversification, spreading assets across currencies and jurisdictions to reduce exposure to local market risks. They also provide asset protection by leveraging legal frameworks in stable locations like Switzerland or Liechtenstein, shielding wealth from political instability, economic downturns, and currency fluctuations. For clients prioritizing legacy planning, services include trust creation, will drafting, and cross-border wealth transfer strategies. Tax optimization is another critical element, as managers advise clients on leveraging favorable tax regimes.

In some cases, institutions combine liquidity with asset protection measures, ensuring both the safety and growth of deposits. This combination reflects the comprehensive approach offshore priority banking takes to secure and grow wealth.

sbb-itb-39d39a6

Benefits of Offshore Priority Banking

Offshore priority banking offers three main advantages tailored to the needs of high-net-worth individuals: enhanced financial privacy, access to global investment options, and tax efficiency paired with asset protection. These benefits work together to create a solid foundation for managing and safeguarding wealth.

Enhanced Financial Privacy

Many offshore banking jurisdictions have strict confidentiality laws that protect account holder information from public access, unwarranted scrutiny, and identity theft. For example, Swiss banks held approximately $2.4 trillion in foreign assets in 2022, showcasing the trust placed in their privacy measures.

"Privacy is one of the main reasons individuals choose offshore banking. Many countries have strict financial confidentiality laws that prevent public access to banking information."

– First Anguilla Trust Company

Modern privacy practices include "transparent compliance", where regulations like CRS and FATCA require banks to report to tax authorities, but not to the public. Offshore structures, such as trusts or LLCs, further enhance privacy by legally separating ownership from personal exposure. This allows individuals to retain control while appearing to own no assets on paper through nominee services. However, these privacy measures must comply with tax reporting obligations in the account holder’s home country. By balancing privacy and compliance, offshore banking aligns with broader global financial opportunities.

Access to Global Investment Options

Offshore priority banking provides access to international markets and diverse asset classes that domestic banks may not offer. Clients can directly engage with major global exchanges and invest in professionally managed offshore mutual funds based in tax-advantaged locations like Luxembourg or Ireland.

Additionally, offshore banks facilitate investments in areas such as international real estate, private equity, and fixed-income instruments. For instance, Belize offers a real interest rate of approximately 2.3%, with inflation at about 0.8%, compared to the United States, where savings account interest rates average 0.06% against an inflation rate near 2%. Similarly, Charles Schwab provides access to over 250 offshore mutual funds spanning both emerging and established markets.

Tax Efficiency and Asset Protection

Offshore banking also supports tax optimization and strengthens asset protection. Offshore structures allow for tax deferral, enabling earnings to grow tax-free until they are withdrawn. For example, a U.S. couple utilizing an offshore arrangement with the Foreign Earned Income Exclusion (FEIE) could reduce taxes on a $300,000 income from $117,391 to $32,405, saving over $85,000 annually. The FEIE threshold for 2026 is approximately $130,000 per individual (or $260,000 for a married couple).

Asset protection is bolstered by local legal frameworks. In places like the Cook Islands and Nevis, foreign court judgments are not recognized, requiring creditors to restart legal proceedings under stringent "beyond reasonable doubt" standards. For example, Nevis mandates a $25,000 bond before creditors can bring a claim against a trust.

"Offshore asset protection is the single most important thing you can do for your financial survival. If you keep all your wealth in one country – under the thumb of one government – you are a sitting target."

– Craig Whyte

Some jurisdictions, such as Bermuda and the Cayman Islands, impose no estate or inheritance taxes, simplifying wealth transfer across generations. For domestic assets like real estate that cannot be moved offshore, individuals can register a mortgage or "charge" held by an offshore entity to reduce equity and discourage creditors. It’s essential, however, to establish these structures before any legal claims to avoid allegations of "fraudulent conveyance".

These benefits collectively highlight the robust global financial framework that offshore priority banking provides for wealth management and protection.

Choosing the Right Offshore Jurisdiction

Picking the right offshore jurisdiction is a key decision in offshore priority banking. Your choice directly affects aspects like financial privacy, asset protection, tax efficiency, and long-term wealth management.

What to Consider When Selecting a Jurisdiction

Start by assessing the political and economic stability of a jurisdiction. Favor locations known for neutrality, low corruption, and stable currencies.

A strong regulatory framework is equally important. Check if the jurisdiction aligns with international standards, particularly its status with the Financial Action Task Force (FATF). Jurisdictions on the FATF greylist can face delays or rejections in wire transfers by correspondent banks.

The tax system and asset protection laws of the jurisdiction should align with your financial goals. Some countries, like the UAE and Panama, use territorial tax systems, while others provide Double Taxation Agreements (DTAs) to prevent double taxation. Obtaining a Tax Residency Certificate (TRC) and relocating tax residency to a territorial tax nation can simplify the flow of CRS data to low-tax regions.

"True privacy in 2026 is not about hiding from the government. It’s about protection from everyone else."

– Ipanema Partners

Certain jurisdictions, such as Nevis, the Cook Islands, and Jersey, have legal systems that make it challenging for foreign courts to access trust assets. For example, Jersey’s trust laws ensure foreign judgments cannot be enforced, protecting assets from private litigants while still complying with tax authorities.

Modern digital banking platforms are another factor to consider. Look for jurisdictions offering high-quality digital platforms, multi-currency support, and remote account opening. Belize and the Bahamas, for instance, allow for remote account setup, eliminating the need for in-person visits.

Finally, evaluate deposit protection schemes. For example, Singapore’s SDIC insures deposits up to SGD 75,000, while Hong Kong’s scheme covers deposits up to HKD 500,000. These schemes provide an extra layer of security on top of the bank’s stability.

By choosing a jurisdiction that aligns with your needs for privacy, tax efficiency, and asset protection, you can create a solid foundation for your financial strategy. This sets the stage for reviewing popular jurisdictions favored by high-net-worth individuals.

Common Jurisdictions for Offshore Banking

Several jurisdictions stand out for their advantages in offshore priority banking.

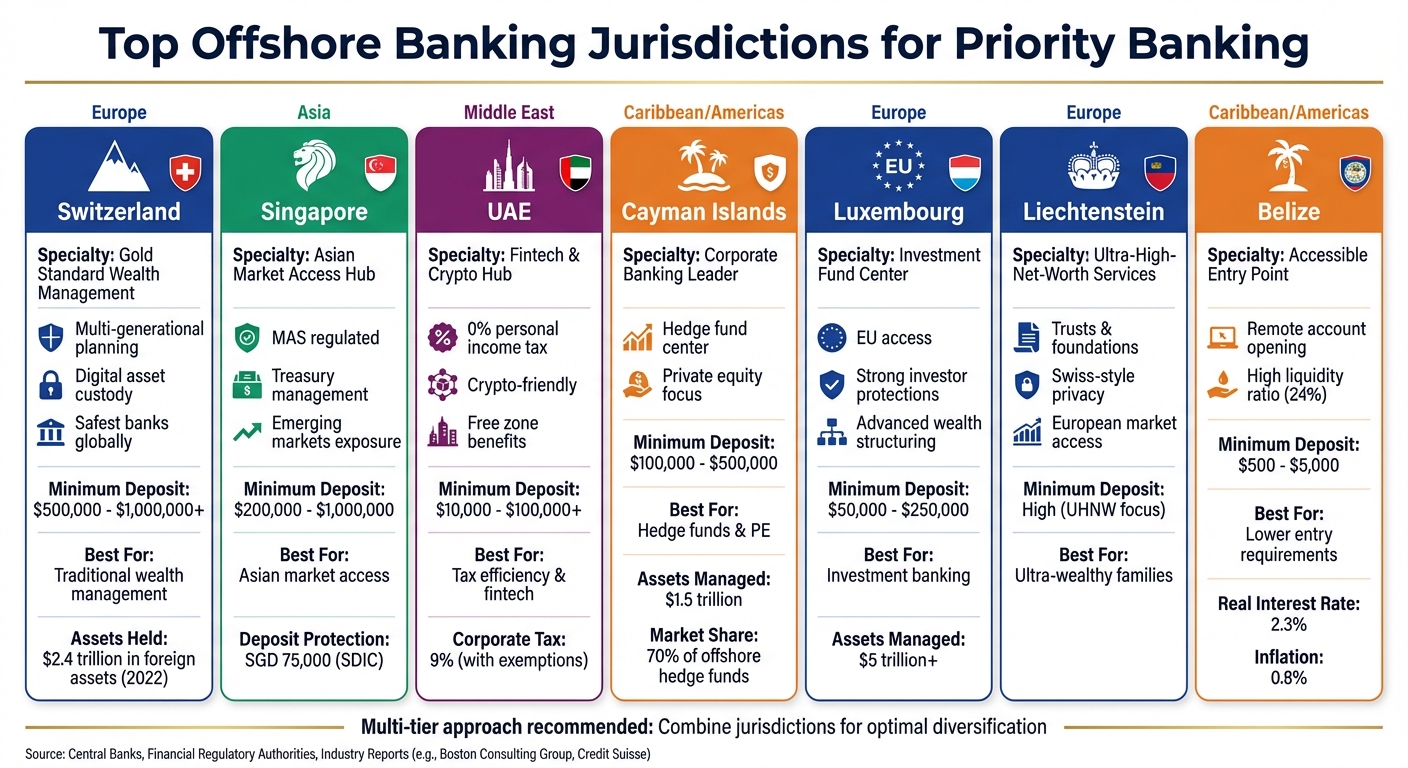

Switzerland is often seen as the "Gold Standard" for wealth management. Swiss banks, like Zürcher Kantonalbank, are among the safest globally. While secrecy is no longer the focus, Switzerland excels in multi-generational planning and digital asset custody alongside traditional wealth management. Minimum deposits typically range from $500,000 to $1,000,000+.

Singapore has become a leading hub for accessing Asian markets and global business banking. With high regulatory standards under the Monetary Authority of Singapore (MAS) and advanced treasury management, it attracts individuals looking for exposure to both developed and emerging markets. Minimum deposits generally range from $200,000 to $1,000,000.

"The key distinction of modern offshore banking isn’t privacy – it’s financial sophistication and regulatory efficiency."

– Project Black Ledger

The United Arab Emirates (UAE) has quickly become a fintech hotspot. It offers zero personal income tax and a crypto-friendly banking environment. Although a 9% corporate tax was introduced in 2023, free zone entities and offshore structures meeting substance requirements still enjoy notable benefits. Minimum deposits range from $10,000 to $100,000+.

The Cayman Islands are a major player in corporate banking, managing over $1.5 trillion in assets and hosting 70% of the world’s offshore hedge funds. While primarily used for hedge funds and private equity, it is less suited for personal banking. Minimum deposits usually range from $100,000 to $500,000.

Luxembourg is Europe’s main investment fund center, managing over $5 trillion in assets. It specializes in investment banking and private wealth services, offering strong investor protections and advanced wealth structuring. Minimum deposits typically range from $50,000 to $250,000.

Liechtenstein caters to ultra-high-net-worth individuals with services like trusts and foundations. It blends Swiss-style privacy with access to European markets, proving that expertise often matters more than size in offshore banking.

For those seeking lower entry requirements, Belize is a good option, with minimum deposits starting as low as $500 to $5,000. Belizean banks are required to maintain a 24% liquidity ratio, far exceeding the 3–4% typical in U.S. banks, providing added financial stability.

Increasingly, individuals are using a multi-tier approach – leveraging Singapore for operations, Switzerland for investment management, and the UAE for regional business – to diversify risk while meeting various financial needs.

Managing Risks in Offshore Priority Banking

Offshore priority banking can be a powerful tool for wealth management, but it comes with risks that demand careful oversight. Staying informed about regulations and adopting effective risk management practices are key to safeguarding your assets.

Regulatory Compliance

Navigating the regulatory landscape is a critical aspect of offshore banking. U.S. citizens, for instance, must report all worldwide income, regardless of where their assets are located. This includes filing the FBAR (FinCEN Form 114) for foreign accounts and FATCA (Form 8938) for specified foreign financial assets.

Financial institutions have also tightened their compliance protocols. Enhanced Due Diligence (EDD) and Know Your Customer (KYC) processes are now mandatory, especially for high-net-worth individuals with complex financial structures or those classified as Politically Exposed Persons (PEPs). You’ll need to provide clear documentation of your Source of Wealth (SoW) and Source of Funds (SoF) to meet these requirements.

The introduction of CRS and FATCA has made automatic financial data sharing between jurisdictions the norm, effectively dismantling offshore secrecy. Regulatory bodies like Singapore’s Monetary Authority of Singapore (MAS), the UK’s Financial Conduct Authority (FCA), and the U.S.’s Financial Crimes Enforcement Network (FinCEN) have adopted stringent anti-money laundering (AML) measures. For example, in 2016, the MAS revoked BSI Bank’s license and closed Falcon Private Bank due to their involvement in the 1MDB scandal. These actions were accompanied by fines of SGD 13.3 million and SGD 4.3 million, respectively.

"Offshore asset protection is still viable, but it’s no longer a ‘hidden vault.’ Today, it’s most effective as part of a transparent, legally compliant, and professionally structured estate and asset plan."

– James G. Bohm, Attorney, Bohm Wildish & Matsen, LLP

It’s also crucial to establish offshore structures before any legal issues arise. Moving assets offshore after a claim has been filed may be considered a "fraudulent conveyance", which courts can reverse.

Risk Management Methods

A strong risk management plan ensures compliance while protecting your wealth. One effective approach is jurisdictional diversification. By distributing assets across stable jurisdictions like Singapore, Switzerland, or the Cook Islands, you can reduce exposure to risks like political instability or banking failures.

Partnering with reputable institutions – regulated banks, independent trustees, and established law firms – helps minimize counterparty risk. The Danske Bank scandal, where €200 billion in suspicious funds flowed through its Estonian branch, highlights the importance of thorough due diligence.

Before setting up any offshore structure, seek legal advice from both your home country and the offshore jurisdiction. This dual-layered review ensures your setup aligns with cross-border legal requirements. Regular compliance reviews, including updates to KYC information and assessments of high-risk accounts, are also essential.

A layered strategy offers robust protection. Combine domestic measures, like umbrella insurance and estate planning, with offshore structures. For assets that can’t be moved – such as real estate – consider the "charge strategy." This involves registering a mortgage or charge against the property through an offshore entity, effectively shielding equity from creditors.

Finally, maintain an offshore account with at least one year’s living expenses, while keeping sufficient domestic funds for any immediate legal needs or settlements. By integrating these strategies, you can build a resilient financial plan that adapts to both regulatory demands and unforeseen risks.

Conclusion

Offshore priority banking has evolved into a powerful tool for safeguarding wealth and achieving global financial diversification. The shift from secrecy to a focus on compliance and transparency has reshaped the field, making success in 2026 reliant on professional planning and selecting jurisdictions that align with specific financial goals. This transformation underscores the insights explored throughout this guide.

Effective strategies often involve a multi-layered approach to protection. For instance, combining offshore trusts as a legal shield, an offshore company to hold assets, and banking relationships in stable locations like Singapore or Switzerland creates a robust defense. This setup not only complicates asset recovery for creditors by introducing cross-border legal hurdles but also highlights the importance of establishing these structures proactively – before any legal challenges arise.

Choosing the right jurisdiction remains a critical decision in any offshore strategy. The focus can vary: asset protection in places like the Cook Islands and Nevis, advanced wealth management in Singapore or Switzerland, or fund structuring in the Cayman Islands. For example, the Cook Islands imposes high barriers to asset recovery, requiring creditors to prove fraud "beyond a reasonable doubt" and post a $50,000 bond to file a claim. These jurisdiction-specific advantages emphasize the need for careful planning and professional guidance to align strategies with individual objectives.

"Offshore strategies for high-net-worth individuals in 2026 are no longer defined by secrecy or tax avoidance – they are defined by compliance, structure, and long-term planning." – OVZA Legal Affairs

Expert advice plays a pivotal role in navigating these complexities. Collaborating with legal, tax, and financial professionals ensures adherence to regulations like CRS and FATCA while optimizing asset protection and growth. With the right planning, individuals can achieve meaningful savings and long-term financial security, avoiding the pitfalls of insufficient protection.

FAQs

Is offshore priority banking legal for U.S. citizens?

Yes, offshore priority banking is legal for U.S. citizens, provided it is done transparently and in full compliance with U.S. laws, including all tax and reporting requirements. Proper disclosure and strict adherence to these regulations are crucial to avoid any legal or financial complications.

What documents do I need to open an offshore priority bank account?

To set up an offshore priority bank account, you’ll generally need a few key documents. These include a valid passport, proof of address, and, if relevant, contact details for directors or shareholders. Some banks might also ask for financial documents or proof of the source of funds, depending on their internal policies. Since requirements can differ between banks, it’s a good idea to check directly with the institution you’re dealing with to ensure you have everything they need.

How do I choose the best offshore jurisdiction for my goals?

To find the right offshore jurisdiction, focus on key factors like stability, regulatory framework, and privacy protections. Look for locations that offer solid legal safeguards, a stable political environment, and clear, transparent banking regulations. It’s also important to examine compliance requirements and practical details, such as how straightforward the account opening process is, available currency options, and specialized services like wealth management. Matching these elements to your financial objectives can help secure your assets and support sustained financial growth.