If you’re an American trying to open an offshore bank account, you’ve likely faced rejection. Why? It boils down to US indicia – specific markers like U.S. citizenship, birthplace, or a U.S. address that flag you for tax reporting under FATCA (Foreign Account Tax Compliance Act). FATCA has made it costly and risky for banks to work with U.S. clients, leading many to avoid them altogether. Here’s what you need to know:

- US Indicia: Banks look for ties to the U.S., such as citizenship, phone numbers, or instructions to transfer funds to U.S. accounts. These connections trigger reporting obligations to the IRS.

- FATCA Compliance: Banks face penalties (30% withholding tax on U.S.-sourced payments) and high compliance costs – up to $1 million or more for large institutions.

- Rejection Triggers: Missing tax forms (like W-9), unclear financial details, or refusal to waive privacy protections often lead to account denial.

- Options for Americans: Staying tax-compliant, choosing FATCA-friendly banks, and using non-U.S. entities (like offshore companies) can improve your chances. This strategy is often a core component of offshore asset protection for high-net-worth individuals.

The key takeaway: Offshore banking for Americans requires strict adherence to tax laws and thorough documentation. Banks prioritize compliance over secrecy, so transparency is essential. This article breaks down the challenges and offers strategies to navigate them effectively.

FATCA and Its Effect on Offshore Banks

What Is FATCA?

The Foreign Account Tax Compliance Act (FATCA), enacted in 2010, aims to curb tax evasion by requiring foreign financial institutions to disclose information about U.S. account holders to the U.S. Department of the Treasury. To comply, these institutions must identify accounts with U.S. connections – like a U.S. birthplace, mailing address, or phone number – and report critical details about these clients.

Participation in the U.S. financial system hinges on foreign banks registering with the IRS to obtain a Global Intermediary Identification Number (GIIN). Once registered, they appear on the IRS’s monthly "FFI List". These banks must report specific details for each U.S. account holder, including their name, address, Taxpayer Identification Number (TIN), account balance, and transaction history. If a client refuses to allow this reporting, they are classified as a "recalcitrant account holder", and the bank is required to withhold 30% of all U.S.-sourced payments. These requirements significantly increase costs and legal risks for financial institutions.

Compliance Costs and Risks for Offshore Banks

The financial burden of FATCA compliance varies widely depending on the size of the institution. For smaller banks, initial costs are estimated at $25,000, while mid-sized banks spend between $100,000 and $500,000. Large multinational financial firms often face initial expenses exceeding $1 million, with some estimates soaring as high as $850 million for major players.

Globally, the financial impact of FATCA is substantial. For example:

- The U.K. government estimated a five-year compliance cost of £1.1 billion to £2 billion.

- Germany reported an implementation cost of approximately €386 million, with €30 million in annual maintenance.

- Australia projected a 10-year cost of around A$482.68 million.

Even the IRS faced significant expenses, spending about $380 million on FATCA between 2012 and 2017. However, the Congressional Joint Committee on Taxation projected that the law would generate just $8.7 billion in additional tax revenue over 11 years. For many banks – especially smaller ones – the costs and risks of compliance far outweigh the benefits of maintaining U.S. clients.

As Executive Magazine highlighted:

"FATCA requires major initial investment within an institution, estimated at $25,000 for smaller institutions, to $100,000 to $500,000 for most institutions and $1 million for larger firms".

Faced with these financial and operational challenges, many banks choose to avoid the risks altogether by declining to serve American clients.

sbb-itb-39d39a6

Why Offshore Banks Reject American Clients

Under FATCA’s strict guidelines, offshore banks have specific triggers that influence their decision to reject U.S. clients. These triggers are designed to help banks manage regulatory risks effectively.

Common Triggers for Bank Rejection

When offshore banks detect potential U.S. ties during the account opening process, certain red flags can lead to rejection. One of the most common issues is a missing or incomplete Form W-9, which is required to verify Taxpayer Identification Numbers (TINs) and report to the IRS. Without this form, banks expose themselves to penalties for non-compliance.

Another major issue is an unclear FATCA status. If applicants provide vague or incomplete financial details – like undocumented cryptocurrency gains or unclear sources of funds – banks often reject the application to avoid regulatory complications. As OCBF Consulting aptly stated:

"The banks have not turned against Americans; they have turned against ambiguity".

A particularly severe red flag is the recalcitrant account classification. This occurs when a client refuses to provide the necessary FATCA documentation or declines to waive local privacy protections. Such accounts are subject to a 30% withholding tax on U.S.-sourced payments. For most banks, the compliance risks and administrative challenges associated with these accounts far outweigh any potential benefits, prompting them to decline such clients outright.

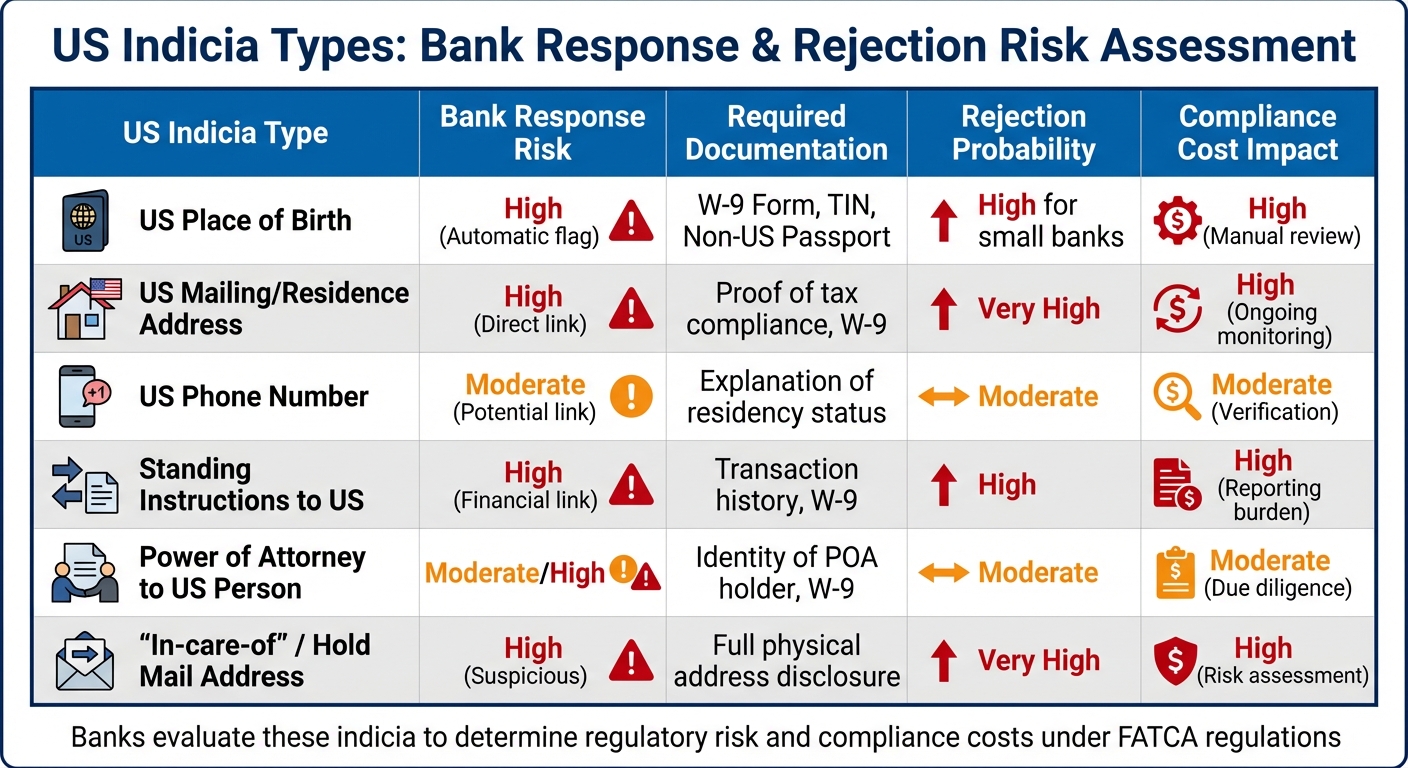

US Indicia Types and Bank Responses

In addition to these triggers, banks evaluate specific U.S. indicia – clues that suggest a connection to the United States – to determine the risk of accepting a client. Each type of indicia carries a different risk level, influencing whether a bank will proceed with or reject an application. The table below outlines how banks typically respond to various U.S. indicia:

| US Indicia Type | Bank Response Risk | Required Documentation | Rejection Probability | Compliance Cost Impact |

|---|---|---|---|---|

| US Place of Birth | High (Automatic flag) | W-9 Form, TIN, Non-US Passport | High for small banks | High (Manual review) |

| US Mailing/Residence Address | High (Direct link) | Proof of tax compliance, W-9 | Very High | High (Ongoing monitoring) |

| US Phone Number | Moderate (Potential link) | Explanation of residency status | Moderate | Moderate (Verification) |

| Standing Instructions to US | High (Financial link) | Transaction history, W-9 | High | High (Reporting burden) |

| Power of Attorney to US Person | Moderate/High | Identity of POA holder, W-9 | Moderate | Moderate (Due diligence) |

| "In-care-of" / Hold Mail Address | High (Suspicious) | Full physical address disclosure | Very High | High (Risk assessment) |

The "Compliance Cost Impact" column highlights the operational challenges banks face when dealing with accounts tied to U.S. indicia. For example, a U.S. place of birth automatically flags the applicant as a potential U.S. citizen, requiring extensive documentation – even if citizenship has been renounced. The most problematic indicia, such as "in-care-of" or hold mail addresses, are often seen as deliberate attempts to hide a physical location, leading to a high likelihood of rejection. These factors play a critical role in shaping how banks approach accounts with U.S. connections.

How Americans Can Open Offshore Accounts

Opening an offshore bank account as an American may seem daunting, but it’s entirely possible with the right approach. The key is to prioritize transparency and follow all regulatory guidelines.

Maintain Full Tax Compliance

Staying compliant with U.S. tax laws is non-negotiable. Under FATCA, you’re required to report all offshore accounts to the IRS and the U.S. Treasury Department. If the total value of your foreign accounts exceeds $10,000 at any point during the year, you’ll need to file an FBAR (FinCEN Form 114). Missing these deadlines could lead to steep penalties – ranging from $15,611 per non-willful violation to as much as $156,107 or 50% of the account balance for willful violations.

To meet FATCA requirements, you’ll need to provide your Social Security Number and complete a W-9 form. Banks will also request proof of your "Source of Wealth" and "Source of Funds." This could include tax returns, pay stubs, or inheritance documents. Keeping a U.S.-based bank account can simplify tax payments and help manage U.S.-sourced income.

Once your tax compliance is in order, the next step is identifying a bank that aligns with FATCA standards.

Find FATCA-Compliant Banks

To ensure the bank you’re considering is FATCA-compliant, use the IRS Foreign Financial Institution (FFI) List search tool. A bank with a Global Intermediary Identification Number (GIIN) confirms compliance. Currently, over 113 jurisdictions have FATCA agreements with the U.S..

For instance, Switzerland offers financial stability but typically requires minimum deposits between $250,000 and $1 million. Singapore, known for its safety measures, has deposit requirements ranging from $200,000 to $500,000. The Cook Islands, recognized for asset protection, provides remote account opening options through institutions like Capital Security Bank. Panama is another option, offering dollar-based banking with lower deposit thresholds and potential residency benefits.

When applying, prepare a detailed "Source of Wealth" file covering 6–12 months of financial activity. This might include bank statements, wage slips, or inheritance letters, which are essential for anti-money laundering checks. You’ll also need to provide a passport, proof of address (like a utility bill), and a clear declaration of your source of funds.

Once you’ve chosen a compliant bank, the focus shifts to organizing your documentation.

Use Non-US Entities to Reduce US Indicia

Another strategy to simplify the process is using non-U.S. entities, such as offshore companies or structuring offshore trusts. These structures can reduce the visibility of U.S. ties, which banks often view as a risk. However, these entities must be legitimate and active. For example, setting up a business for e-commerce, consulting, or international trade can improve your chances of approval. Avoid offshore trusts and foundations that act as shell companies or dormant structures, as they tend to raise red flags.

Offshore banking expert Steven James explains:

"The bank is judging whether that relationship will create headaches or operate smoothly within its existing reporting systems. If you present yourself as someone who respects those systems, you immediately stand apart."

Choose jurisdictions with clear regulations to minimize perceived risks. Transparency is still critical – banks will require verifiable documentation of your entity’s ownership and the source of funds. Even with a non-U.S. entity, you’ll need to continue filing FBARs and Form 8938 if your foreign holdings exceed the required thresholds. Additional forms, like Form 5471 or Form 3520, may also be necessary, so working with an international tax attorney is highly recommended.

How Global Wealth Protection Can Help

Navigating the complexities of offshore banking as an American requires a well-thought-out approach. Global Wealth Protection (GWP) focuses on helping U.S. citizens and residents tackle the challenges posed by FATCA and U.S. indicia. Here’s how their services provide tailored solutions to make offshore banking more accessible and manageable.

Offshore Company Formation Services

Setting up an offshore company in the right jurisdiction can significantly ease compliance challenges. GWP specializes in forming companies in Anguilla, a jurisdiction that has had a Model 1 Intergovernmental Agreement (IGA) with the U.S. since June 22, 2017. Under this agreement, the Anguillan government handles data transfers to the IRS, simplifying reporting for banks and reducing their compliance workload.

By opening accounts through an offshore entity instead of as an individual, you can better control the "indicia profile" that banks scrutinize during the application process. However, this doesn’t eliminate your reporting obligations – ownership stakes exceeding 10% still require FATCA disclosure. GWP ensures your offshore entity is not only legitimate but also fully operational, while connecting you with banks experienced in U.S. compliance requirements.

Private Consultations for Custom Strategies

Recognizing that every client’s financial situation is unique, GWP offers private consultations to create personalized plans. These sessions focus on areas like tax efficiency, asset protection, and compliant banking strategies. Consultants help identify and address your specific U.S. indicia – such as U.S. birthplaces, addresses, or instructions to transfer funds to U.S. accounts – before they become obstacles.

These consultations also cover dual reporting obligations, ensuring that your financial structures comply with both IRS and FinCEN requirements while safeguarding your privacy.

GWP Insiders Membership Program

For ongoing support, GWP offers the GWP Insiders membership, designed for high-net-worth individuals. This program provides exclusive resources, including an offshore banking report, on choosing the right jurisdictions and banking strategies for those with U.S. tax obligations. Members gain insights into "U.S.-friendly" banks in places like the Cayman Islands, Panama, and the Cook Islands – jurisdictions with strong FATCA reporting systems that continue to work with American clients.

The program also addresses the shift in offshore banking from secrecy to what experts call "transparency that banks can live with". With banks prioritizing regulatory compliance over anonymity, GWP helps members prepare thorough documentation to confirm income, tax status, and business activity – key steps to avoid rejection by banks. Given that 113 jurisdictions now participate in FATCA agreements, expert guidance is essential to navigate this intricate system effectively.

Conclusion

Navigating the world of offshore banking as an American has evolved into a process that prioritizes transparency and compliance. By 2026, opening an offshore bank account will require a clear, organized approach. The era of banking secrecy is over – success now hinges on presenting banks with well-documented proof of income sources, tax compliance, and financial activities.

As Steven James aptly puts it:

"The banks have not turned against Americans; they have turned against ambiguity".

To overcome the barriers imposed by regulations like FATCA and U.S. indicia, staying on top of your tax filings is non-negotiable. Offshore banks now expect thorough documentation to confirm tax compliance before allowing new accounts. Without this, gaining access to these financial institutions is nearly impossible.

Seeking professional guidance can simplify the process significantly. Experts can help identify banks that are open to working with U.S. clients, prepare applications tailored to meet stringent requirements, and address any red flags tied to indicia. Whether you’re forming an offshore entity in Anguilla or leveraging insider knowledge through specialized memberships, having the right support makes managing regulatory hurdles far easier.

The formula for success boils down to a few key steps: stay fully compliant with tax laws, organize your paperwork meticulously, and focus on institutions equipped to handle FATCA reporting. Offshore banking for Americans isn’t about avoiding oversight – it’s about diversifying financial options and accessing global opportunities while adhering to legal standards. By following the strategies outlined in this article, Americans can confidently navigate the offshore banking landscape and work toward their international financial goals.

FAQs

What documents do offshore banks usually require from U.S. clients?

Offshore banks typically require U.S. clients to submit personal identification, proof of address, and documents verifying the source of funds. These documents might include items like bank statements, tax returns, or records of employment income. It’s important to ensure all submitted paperwork is up-to-date and accurately represents your financial situation to comply with the bank’s regulations.

Does using an offshore company reduce my FATCA and IRS reporting duties?

Using an offshore company doesn’t eliminate your FATCA or IRS reporting obligations. If you’re a U.S. taxpayer, you’re required to report foreign financial assets, including those held through offshore entities, when they surpass specific thresholds. In fact, using offshore companies can make compliance more complex, as you’ll still need to disclose ownership and assets on forms like Form 8938 and FBAR. Failing to comply can result in hefty penalties, making it crucial to follow IRS regulations carefully.

How can I check if a foreign bank is FATCA-compliant before applying?

To determine if a foreign bank complies with FATCA, start by checking if it is registered with the IRS under FATCA regulations. Banks that meet compliance standards will have a Global Intermediary Identification Number (GIIN) and will be listed on the IRS’s official registry of foreign financial institutions. Another option is to contact the bank directly and ask them to confirm their FATCA registration and adherence to U.S. reporting obligations.