FATCA (Foreign Account Tax Compliance Act) requires U.S. taxpayers to report foreign financial assets to the IRS to combat offshore tax evasion. By 2026, over 113 countries are sharing data with the U.S., making offshore account privacy nearly obsolete. Non-compliance can result in penalties starting at $10,000 per year, escalating to $50,000, plus a 40% surcharge on underpayments.

Key points:

- Who must report: U.S. taxpayers with foreign financial assets above specific thresholds.

- What to report: Bank accounts, investments, pensions, insurance policies, and other foreign-held financial assets.

- Filing requirements: Submit Form 8938 with your annual tax return. Thresholds vary based on residency and filing status.

- Penalties: Fines for non-compliance can reach tens of thousands of dollars, with potential criminal charges for willful violations.

- New in 2026: Cryptocurrency on foreign exchanges is now reportable.

Staying compliant involves understanding reporting thresholds, keeping detailed records, and filing accurately. If you’ve missed filings, IRS programs like Streamlined Filing Compliance can help avoid penalties. FATCA compliance is critical for avoiding costly fines and ensuring transparency with the IRS.

What Assets Must Be Reported Under FATCA

Knowing what needs to be reported under FATCA is essential to avoid penalties and stay compliant in 2026. U.S. taxpayers are required to disclose Specified Foreign Financial Assets on Form 8938. These include two main categories: 1) financial accounts held at foreign institutions and 2) other foreign assets held for investment purposes. This distinction forms the basis for FATCA’s detailed reporting rules.

"Specified foreign financial assets include foreign financial accounts and foreign non-account assets held for investment (as opposed to held for use in a trade or business), such as foreign stock and securities, foreign financial instruments, contracts with non-U.S. persons, and interests in foreign entities." – Internal Revenue Service

The intent behind holding the asset matters – only assets held for investment, not those used in business operations, must be reported. Additionally, assets held by U.S. payors (like U.S. branches of foreign banks) are not subject to reporting.

Bank Accounts, Brokerage Accounts, and Investment Holdings

Foreign financial accounts that require reporting include checking, savings, brokerage, and deposit accounts. Even something as ordinary as a checking account can trigger reporting if it meets the threshold.

Investments such as foreign-issued stocks, bonds, mutual funds, hedge funds, private equity funds, and ownership stakes in foreign corporations or partnerships also fall under FATCA. Digital assets held on non-U.S. exchanges may need to be reported as well, though the rules for cryptocurrency are still under review. If you’re unsure about whether an asset qualifies, it’s usually safer to report it than risk leaving it out.

FATCA’s scope also extends to non-traditional financial assets.

Trusts, Life Insurance Policies, and Pension Plans

Non-traditional assets are often overlooked but are just as important to report. For instance, foreign-held pensions and retirement plans, such as Canadian Registered Retirement Savings Plans (RRSPs) or Swiss pensions, must be disclosed.

Life insurance or annuity contracts with a cash value issued by foreign insurers are also reportable. Similarly, any beneficial interest in foreign trusts or estates – such as distributions received – needs to be included.

However, social security or social insurance programs run by foreign governments are generally not considered specified foreign financial assets and don’t need to be reported. This exemption applies strictly to government-run programs, not private pension arrangements.

| Asset Category | Reportable Examples |

|---|---|

| Bank & Brokerage | Checking, savings, and investment accounts at foreign financial institutions |

| Securities | Foreign stocks, bonds, and mutual funds |

| Retirement | Foreign pensions, retirement plans (e.g., Swiss pensions, Canadian RRSPs) |

| Insurance | Foreign life insurance or annuity contracts with a cash value |

| Business Interests | Interests in foreign partnerships, corporations, and private equity |

| Trusts & Estates | Beneficial interests in foreign trusts or foreign estates |

| Other Instruments | Financial instruments or contracts with a non-U.S. counterparty |

sbb-itb-39d39a6

FATCA Reporting Thresholds for 2026

Whether you need to file Form 8938 depends on the total value of your specified foreign financial assets and your residency status. The thresholds for the 2025 tax year (to be filed in 2026) remain unchanged from previous years. Filing is required if your assets exceed the threshold either on the last day of the tax year or at any point during the year – whichever is higher.

If you are not required to file a U.S. income tax return, you do not need to submit Form 8938, no matter how much you hold in foreign assets. The requirement applies only to those who must file a tax return.

The thresholds vary depending on whether you are a U.S. resident or a U.S. citizen living abroad. Here’s a breakdown of the requirements.

Thresholds for U.S. Residents

For U.S. residents, the filing thresholds are as follows:

- Single or married filing separately: $50,000 at year-end or $75,000 at any point during the year.

- Married filing jointly: $100,000 at year-end or $150,000 at any time.

If you are married filing separately and jointly own assets, include half the value of the assets when determining if you meet the threshold. However, if you are required to file, report the full value of the jointly owned assets.

Thresholds for U.S. Citizens Living Abroad

For U.S. citizens living abroad, the thresholds are significantly higher:

- Single or married filing separately: $200,000 at year-end or $300,000 at any time.

- Married filing jointly: $400,000 at year-end or $600,000 at any time.

To qualify for these higher thresholds, you must meet the following conditions:

- Your tax home must be in a foreign country.

- You must satisfy either the bona fide residence test or the physical presence test. The latter requires you to spend at least 330 days in a foreign country during a consecutive 12-month period.

Summary of Thresholds

| Filing Status | Residency | Year-End Threshold | Any Time During Year Threshold |

|---|---|---|---|

| Single or Married Filing Separately | Living in the U.S. | $50,000 | $75,000 |

| Married Filing Jointly | Living in the U.S. | $100,000 | $150,000 |

| Single or Married Filing Separately | Living Abroad | $200,000 | $300,000 |

| Married Filing Jointly | Living Abroad | $400,000 | $600,000 |

When calculating these amounts, convert all foreign currency values to U.S. dollars using the Treasury Bureau’s exchange rate for the last day of the tax year. Keep detailed records of both year-end balances and the highest balances reached during the year. Exceeding either threshold triggers the requirement to file Form 8938.

With these thresholds clarified, the next sections will dive into the Form 8938 filing process and the differences between FATCA and FBAR.

How to File Form 8938 for FATCA Compliance

To comply with FATCA, you’ll need to attach Form 8938 to your annual tax return (1040, 1040-SR, or 1040-NR). For the 2025 tax year, the filing deadline is April 15, 2026. If you’re living abroad, you have until June 15, 2026, with an option to extend to October 15 by filing Form 4868. Below is a detailed guide on completing Form 8938 and keeping the necessary records.

Completing and Submitting Form 8938

Start by entering your name, Taxpayer Identification Number (TIN), and address at the top of the form. Then, follow these steps:

- Part I: Report the maximum value of your specified foreign assets. Indicate if you’ve filed other related forms, such as 3520, 5471, or 8621.

- Part II: List each foreign deposit or custodial account. Include the financial institution’s name, address, account number, the maximum value (in U.S. dollars), and any income earned.

- Part III: Use this section for other foreign assets, like directly held foreign stocks, bonds, or partnership interests. Provide details such as the issuer’s name, type of security, maximum value, and associated income.

- Part IV: Summarize all tax items (e.g., interest, dividends, capital gains) and specify which schedules (like Schedule B or D) report this income on your tax return.

- Parts V and VI: Use these sections to provide additional details about the accounts and assets listed earlier.

When reporting amounts, convert all foreign currency values to U.S. dollars using the U.S. Treasury exchange rate as of the last day of the tax year. For foreign accounts, report the highest dollar value during the year. For non-account assets, use their fair market value as of December 31.

"Report borderline assets; over-reporting incurs no penalties." – Vincenzo Villamena, CPA and Founder of Online Taxman

Ensure all the information is accurate and supported by proper documentation.

Maintaining Proper Documentation

You’ll need to keep records for at least six years. This aligns with the extended statute of limitations for foreign asset omissions – if you fail to report more than $5,000 in income tied to a specified foreign financial asset, the IRS has six years to assess additional taxes. Your records should include:

- Annual financial account statements showing year-end and maximum balances.

- Documentation of the methods used to value non-account assets.

- Currency conversion data and applicable exchange rates.

Additionally, record the Global Intermediary Identification Number (GIIN) for each foreign financial institution. Keep detailed records of all income, such as interest, dividends, royalties, and capital gains, to ensure consistency between Form 8938 and Schedule B of your Form 1040.

If you realize you’ve omitted Form 8938 in a previously filed return, you can correct this by submitting Form 1040X (Amended U.S. Individual Income Tax Return) with the missing Form 8938 attached. Proper documentation and timely corrections are key to staying compliant.

FATCA vs. FBAR: Understanding the Differences

After explaining how to file Form 8938, it’s important to clarify how this requirement differs from FBAR, another critical reporting obligation for offshore assets.

If you have accounts or assets overseas, you might wonder whether to file Form 8938, FBAR, or both. These are separate filings, overseen by different agencies, and submitting one does not fulfill the requirements of the other. Knowing the distinctions between these forms is key to staying compliant and avoiding penalties.

"The Form 8938 filing requirement does not replace or otherwise affect a taxpayer’s obligation to file FinCEN Form 114 (Report of Foreign Bank and Financial Accounts)." – Internal Revenue Service

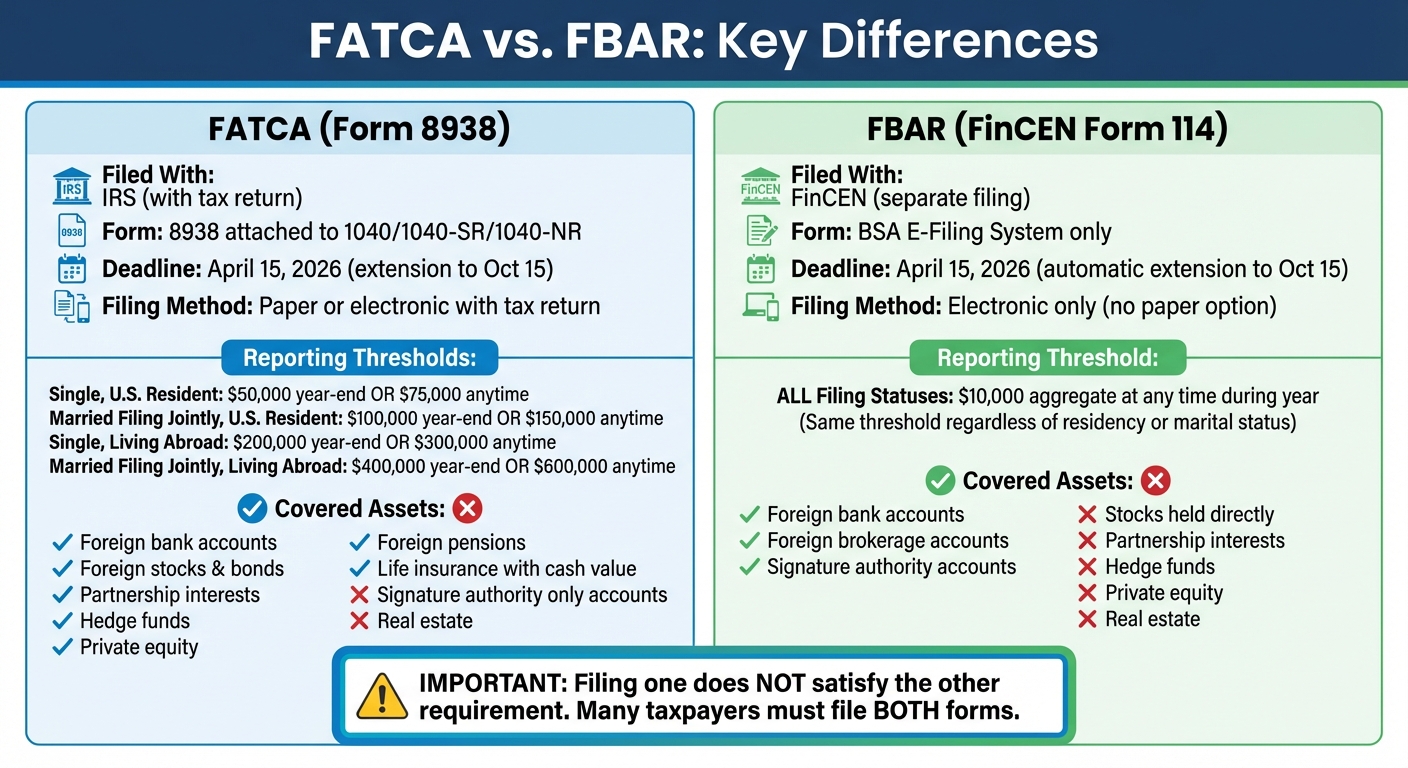

Comparing Thresholds and Covered Assets

The main difference between FATCA and FBAR lies in their reporting thresholds and the types of assets they cover. FBAR has a flat threshold of $10,000 in aggregate across all accounts at any point during the year. For instance, if you have three accounts with $4,000 each (totaling $12,000), they all must be reported. In contrast, FATCA thresholds are higher and depend on your tax filing status and whether you live in the U.S. or abroad.

| Feature | FATCA (Form 8938) | FBAR (FinCEN Form 114) |

|---|---|---|

| Reporting Threshold (Single, U.S. Resident) | $50,000 at year-end or $75,000 at any time | $10,000 aggregate at any time |

| Reporting Threshold (Single, Living Abroad) | $200,000 at year-end or $300,000 at any time | $10,000 aggregate at any time |

| Reporting Threshold (Married Filing Jointly, U.S. Resident) | $100,000 at year-end or $150,000 at any time | $10,000 aggregate at any time |

| Reporting Threshold (Married Filing Jointly, Living Abroad) | $400,000 at year-end or $600,000 at any time | $10,000 aggregate at any time |

| Covered Assets | Foreign accounts, stocks, bonds, partnership interests, hedge funds, private equity | Financial accounts only (e.g., bank and brokerage accounts) |

| Signature Authority Only | Not reported | Must be reported |

| Directly Held Real Estate | Not reported | Not reported |

FATCA encompasses a wider range of foreign financial assets, such as directly held foreign stocks, partnership interests, and hedge fund investments, which FBAR does not include. On the other hand, FBAR requires reporting of accounts where you have signature authority, even if you don’t have a financial stake in them.

It’s worth noting that even if you aren’t required to file a U.S. tax return – and therefore don’t need to submit Form 8938 – you must still file FBAR if the total value of your foreign accounts exceeds $10,000.

By understanding these differences in thresholds and assets, you can better determine which forms apply to your situation.

Where and When to File Each Form

FATCA and FBAR are filed with different agencies and through distinct methods. Form 8938 is submitted to the IRS as part of your annual income tax return (Forms 1040, 1040-SR, or 1040-NR). For the 2025 tax year, the deadline is April 15, 2026, with an extension available until October 15, 2026, if you file Form 4868.

FBAR, on the other hand, is filed separately with the Financial Crimes Enforcement Network (FinCEN) using the BSA E-Filing System – there’s no paper filing option. The filing deadline aligns with the tax return deadline: April 15, 2026, with an automatic extension to October 15, 2026.

Since these forms serve different purposes and are managed by separate entities, you’ll need to assess your assets against both thresholds independently. Many Americans living overseas are required to file both forms. Interestingly, about 62% of expats owe no U.S. federal taxes after credits, yet they still must meet these reporting obligations.

Penalties for Failing to Comply with FATCA

Understanding the financial risks tied to non-compliance with FATCA is key to staying on the right side of the law. Missing deadlines or failing to disclose required assets can lead to hefty financial repercussions. The IRS takes these matters seriously – whether the failure is accidental or intentional – and knowing the penalties can help highlight the importance of accurate and timely reporting.

Civil penalties generally apply to honest mistakes, while criminal charges come into play when the IRS determines that a violation was intentional.

Fines for Unintentional Errors

If you fail to file Form 8938 due to an oversight or mistake, the IRS imposes a $10,000 penalty for each year the form is missing. This penalty increases by $10,000 every 30 days, capping at $50,000 if the issue isn’t resolved within 90 days of receiving an IRS notice. Importantly, this fine applies even if no additional taxes are owed. Beyond the filing penalties, a 40% penalty can also be applied to any tax underpayment linked to undisclosed assets.

The statute of limitations for these cases extends to three years after you eventually submit the required information – or six years if you failed to report more than $5,000 in gross income from a foreign asset. However, penalties may be waived if you can prove a reasonable cause for the error.

"FATCA is primarily about transparency, not additional taxation, but ignoring it can still become costly." – Online Taxman

On the other hand, willful violations lead to far more severe consequences.

Criminal Penalties for Deliberate Violations

While civil fines address accidental errors, deliberate non-compliance carries much harsher outcomes. The IRS defines willfulness as knowingly violating a legal requirement. Even "willful blindness", where someone avoids learning about their obligations, is treated as intentional non-compliance.

For willful violations, criminal penalties can include fines up to $500,000 and imprisonment for up to 10 years. Although criminal prosecution for FATCA violations is relatively rare, it typically targets cases involving intentional tax evasion. Examples of deliberate non-disclosure include falsely denying foreign account interest on Schedule B, using nominee names to hide assets, or providing false information to the IRS about account ownership.

A notable case illustrating the consequences of willful non-compliance is United States v. Zwerner (2014). Carl Zwerner was found to have willfully failed to report Swiss bank accounts worth about $1.69 million. Despite Zwerner’s claim that the omission was unintentional, the court imposed penalties exceeding the total value of the accounts. For those facing willful violations, the IRS Voluntary Disclosure Program offers a potential route to avoid criminal charges, though legal assistance from a tax attorney is often necessary.

"Willful blindness can be treated as willful conduct. If you deliberately avoided learning about requirements when you should have known to ask, the IRS may treat this as willful." – sdocpa.com

How to Stay Compliant with FATCA Requirements

Staying on top of FATCA compliance can feel overwhelming, but having the right systems in place makes it much easier to manage and helps you avoid penalties.

Setting Up a System to Track Your Assets

Start by creating a detailed log for all your foreign accounts. Include essential information such as account numbers, the names and addresses of financial institutions, and the highest balance each account reached during the year. Keeping this log updated regularly will save you from scrambling to reconstruct records at tax time.

For valuation, rely on annual financial statements from your foreign banks. These typically include the year-end balance and the highest balance during the reporting period. If you own assets outside of accounts – like foreign stocks or interests in partnerships – use their year-end value if it closely reflects the maximum value during the year.

When converting foreign currency to U.S. dollars, always use the U.S. Treasury Bureau of the Fiscal Service exchange rate as of December 31 of the relevant tax year (e.g., December 31, 2025, for a 2026 filing). Only the official Treasury rate is acceptable for these conversions.

If you’ve already reported certain assets on other IRS forms, such as Form 3520 (for trusts) or Form 5471 (for foreign corporations), you don’t need to duplicate those details on Form 8938. However, you must reference those forms and include the asset values when determining whether you meet the reporting threshold.

"When in doubt, report. It’s better to include a borderline asset than risk a penalty for omission. Over-reporting does not trigger penalties, under-reporting does." – Online Taxman

Once your asset log is in order, make sure to coordinate with your foreign financial institutions to meet their reporting requirements.

Working with Foreign Financial Institutions

Foreign banks have their own responsibilities under FATCA. To avoid a 30% withholding tax on certain U.S.-source payments, they are required to report information about their U.S. account holders directly to the IRS.

Your foreign bank will likely ask for proof of your U.S. citizenship or your TIN (Taxpayer Identification Number) for FATCA reporting. Providing this information promptly can help you avoid potential account restrictions or even closures.

When choosing a foreign bank, look for institutions that are FATCA-registered and have experience working with U.S. expats. These banks are more likely to have established systems in place to handle the complexities of FATCA reporting.

If you’ve missed filings in the past but did so unintentionally, you may qualify for the Streamlined Filing Compliance Procedures to get back on track without penalties. However, avoid "quiet disclosure" – submitting late forms without formally entering a compliance program. The IRS uses advanced data analytics to flag these cases for investigation.

What’s New for FATCA in 2026

Several updates are reshaping FATCA compliance in 2026, particularly around reporting requirements and digital assets. While the reporting thresholds for Form 8938 remain the same for the 2025 tax year (filed in 2026), the focus has shifted toward stricter oversight, especially for foreign institutions and cryptocurrency.

The IRS has extended compliance relief for Foreign Financial Institutions (FFIs) through 2027. This extension applies to institutions actively working toward meeting FATCA requirements. However, it comes with heightened scrutiny. Foreign banks that fail to register for FATCA may face serious consequences, including service disruptions or account closures. Some institutions are even withdrawing from the U.S. market altogether to avoid the compliance challenges.

Digital Assets Under the Spotlight

Offshore digital assets now fall under FATCA’s reporting scope. If you hold cryptocurrency – like Bitcoin, Ethereum, stablecoins (e.g., USDT, USDC), NFTs, or DeFi tokens – on foreign platforms, these are classified as "Specified Foreign Financial Assets" and must be reported on Form 8938 if they meet the value thresholds. While self-custody wallets remain a gray area, assets stored with foreign financial institutions clearly require disclosure.

"Report crypto on foreign exchanges if thresholds are met; maintain records of your compliance efforts." – Chip Moreno, Tax Expert

Enhanced IRS Enforcement

The IRS is stepping up enforcement using advanced data analytics. By cross-referencing foreign bank reports with individual taxpayer filings, the agency is making it riskier to delay or skip filing required forms. Starting in 2026, cryptocurrency exchanges and brokers will also issue Form 1099-DA (Digital Asset), creating a direct record for tracking and enforcing compliance.

To stay compliant, track the maximum value of your digital assets throughout the year. When filing, use the U.S. Treasury Bureau exchange rate as of December 31, 2025, to convert foreign currency values. These changes highlight the growing importance of meticulous FATCA reporting and record-keeping.

Conclusion

FATCA compliance isn’t optional when tax season rolls around. The IRS now employs advanced data analytics to cross-check information from foreign financial institutions with individual tax filings. This makes it extremely difficult to avoid detection. Even a minor discrepancy can result in an automatic compliance letter, and the situation can escalate quickly from there.

Failing to comply can be costly. Penalties start at $10,000, with additional fines every 30 days, a 40% surcharge on underpayments, and an extended six-year statute of limitations. These harsh penalties highlight the importance of keeping accurate records and addressing issues promptly.

That said, staying compliant is entirely possible with diligent recordkeeping and regular monitoring. If you’ve fallen behind on filings, the IRS Streamlined Filing Compliance Procedures provide a way to catch up without penalties – as long as your non-compliance was unintentional.

FAQs

Do I have to file Form 8938 if my foreign accounts dropped below the threshold by year-end?

If the total value of your foreign accounts stays below the reporting threshold at the end of the year, you generally don’t need to file Form 8938 for that year. This form is only necessary if your accounts surpass the specified thresholds either on the last day of the year or at any point during the year.

How do I calculate the “maximum value” for foreign accounts and crypto during the year?

To figure out the maximum value of your foreign accounts and cryptocurrency, add up the fair market value of all your foreign financial accounts and crypto assets at their peak value during the year. If the combined total goes beyond the FATCA reporting thresholds – like $200,000 for U.S. expats at year-end or $50,000 for U.S. residents – you’re required to report them using Form 8938.

What should I do if I forgot to file Form 8938 in past tax years?

If you missed filing Form 8938, it’s important to address the issue quickly to meet FATCA requirements. Start by reviewing your previous tax returns to pinpoint any years where the form was omitted. Then, amend your tax returns to include the missing form. It’s a good idea to work with a tax professional to ensure everything is accurate and to fully understand any penalties, which can begin at $10,000 per violation. Be sure to keep detailed records of your amended filings and any communication with the IRS to stay on top of your compliance.