Here’s the bottom line: If you’re looking to protect your wealth, offshore trusts and offshore LLCs are two powerful options. But they serve different purposes:

- Offshore Trusts: Best for long-term asset protection. They transfer ownership to a foreign trustee, making it extremely hard for creditors to access your assets. Ideal for high-net-worth individuals or those in high-risk professions.

- Offshore LLCs: Great for retaining control while protecting business assets. They shield personal wealth from business liabilities and are easier to manage for active operations like real estate or e-commerce.

Quick Takeaways:

- Offshore trusts offer stronger protection but come with higher costs and less control.

- Offshore LLCs are more affordable and flexible but may not provide the same level of creditor protection.

- Combining both – a trust owning an LLC – can create a layered defense, balancing control and security.

Key Decision Factors:

- Your Assets: Trusts work best for passive investments; LLCs suit active businesses.

- Risk Level: High-liability professions benefit more from trusts.

- Control: LLCs let you manage assets directly, while trusts require handing over control to a trustee.

Timing Matters: Set up these structures before facing legal threats to avoid fraudulent transfer claims.

What Are Offshore Trusts?

To understand how offshore trusts stack up against offshore LLCs for asset protection, it’s important to first grasp what they are and how they work.

Definition and Legal Framework

An offshore trust involves transferring asset ownership from the settlor (the person creating the trust) to a licensed trustee in a foreign jurisdiction. Under the laws of that jurisdiction, the trustee gains control of the assets, making it nearly impossible for U.S. courts to enforce their orders. Creditors attempting to access these assets must navigate the foreign legal system, which can be incredibly challenging. For instance, in the Cook Islands, creditors face several hurdles: they must pay a mandatory litigation bond of about $50,000 to file a claim, adhere to a short statute of limitations (often just one to two years), and prove fraudulent transfer claims to an exceptionally high standard – "beyond a reasonable doubt". These legal structures make offshore trusts a powerful tool for asset protection.

Main Features of Offshore Trusts

Offshore trusts come with unique protections that domestic options can’t match. A key feature is the "impossibility defense", where transferring control to a foreign trustee means you can’t retrieve the assets yourself, even if ordered to do so by a U.S. court.

Other notable features include anti-duress clauses, which strip you of decision-making authority under legal pressure, such as a court order. Additionally, many offshore trusts include a flight clause, allowing the trustee or a trust protector to move the trust’s legal jurisdiction (or "situs") to a more favorable location if the current one becomes less secure.

A well-known example is the 1999 case FTC v. Affordable Media. In this case, the Ninth Circuit upheld civil contempt charges against the creators of a Cook Islands trust who refused to repatriate assets. Despite the court’s orders and the settlors being jailed, the Cook Islands trustee did not comply, leaving the trust’s assets fully protected. While these features provide strong protection, they also come with certain trade-offs.

Advantages and Disadvantages

Offshore trusts are renowned for their ability to protect assets. In fact, no creditor has successfully recovered assets from a properly structured Cook Islands trust through local litigation in over four decades. They also offer estate planning benefits, such as designating beneficiaries, customizing distribution terms, and allowing for private, probate-free wealth transfers.

However, this level of protection comes with significant costs and reduced control. Setting up a Cook Islands trust typically costs between $20,000 and $25,000, with annual trustee fees ranging from $5,000 to $8,000. Additionally, you’ll need to budget $3,000 to $5,500 annually for required IRS filings, including Forms 3520, 3520-A, and FBAR. Another important consideration is that you must relinquish day-to-day control of the assets. Even if you’re named as a discretionary beneficiary, the trustee has the final say over distributions. This loss of control is a key part of what makes the trust so secure.

As asset protection attorney Jon Alper puts it:

"The trust’s protective power comes from two features. First, the foreign country’s laws impose barriers to creditor enforcement… Second, the trust creates a defense when a U.S. court orders the settlor to bring trust assets back to the United States."

To achieve the best results, it’s essential to establish and fund the trust before any legal issues arise. This allows the foreign jurisdiction’s statute of limitations to expire, making it extremely difficult for future creditors to challenge the transfer.

sbb-itb-39d39a6

What Are Offshore LLCs?

Offshore LLCs, like offshore trusts, provide asset protection, but they stand out by allowing owners to maintain operational control.

Definition and Operating Structure

An offshore LLC is a legal entity formed under the laws of a foreign jurisdiction, such as Nevis or the Cook Islands. These entities combine the liability protection of a corporation with the tax flexibility of a partnership. Unlike U.S.-based LLCs, which are governed by state laws, offshore LLCs operate under foreign legal systems that often don’t recognize U.S. court rulings. This creates a legal barrier: even if a creditor wins a judgment in the U.S., they must re-litigate the case in the foreign jurisdiction. These jurisdictions usually impose stricter requirements, such as Nevis‘ $100,000 litigation bond and a two-year statute of limitations for challenging asset transfers.

The structure of an offshore LLC is simple. Instead of shareholders and directors, it has "Members" (owners) and "Managers" (responsible for daily operations). The entity is governed by an Operating Agreement, which allows for a customized management setup. Blake Harris, Managing Attorney at Blake Harris Law, explains:

"The key reason to use an LLC is to protect personal assets from business-related lawsuits or debts."

Offshore LLCs also differ from domestic ones in a critical way: U.S. courts, under the Full Faith and Credit Clause, can enforce out-of-state judgments. However, offshore LLCs operate outside this framework, offering an added layer of protection.

Main Features of Offshore LLCs

One of the most appealing aspects of offshore LLCs is the ability to retain control. Unlike trusts, which require transferring ownership to a trustee, you can serve as the LLC’s manager, maintaining direct control over accounts, investments, and transactions. This makes them an excellent choice for active business ventures like e-commerce, real estate, or intellectual property management.

Another key feature is charging order protection. In many offshore jurisdictions, if a creditor wins a judgment against you, their remedy is limited to a charging order on your LLC membership interest. This means they can only claim distributions made by the LLC, without gaining access to its assets or management.

Offshore LLCs also offer tax advantages. They are usually structured as pass-through entities, meaning profits flow directly to members and are taxed at individual rates. Steven James, Offshore Structures Researcher at OCBF Consulting, notes:

"An LLC is effectively a look-through entity and what this means in practice is that tax is normally not levied or accounted for at the LLC level but instead passes through to the members."

Privacy is another benefit. In jurisdictions like Nevis, the names of LLC members and managers are not publicly disclosed, adding a layer of financial confidentiality.

These benefits make offshore LLCs a versatile tool for asset protection and business operations.

Advantages and Disadvantages

Offshore LLCs are generally more affordable and flexible compared to offshore trusts. Formation costs range from $500 to $3,000, with annual fees between $1,000 and $5,000. For example, setting up a Nevis LLC costs around $9,000, while a Cook Islands LLC is about $10,000 – far less than the $20,000 to $25,000 required for a Cook Islands trust.

Their operational flexibility is another plus. Offshore LLCs are ideal for managing active businesses, investment accounts, or international real estate. Banks and e-commerce platforms often find LLCs easier to work with compared to trusts, which are typically viewed as passive entities.

However, offshore LLCs are not without their challenges. In high-stakes litigation, if you serve as the manager, a U.S. judge could order you to repatriate funds, threatening the LLC’s effectiveness. A foreign trustee, in contrast, would not be subject to such orders.

Additionally, there’s the risk of "piercing the corporate veil." If you fail to maintain proper formalities – like separating personal and business finances or keeping accurate records – courts may disregard the LLC’s liability shield and access your personal assets.

Brian T. Bradley, Esq., of Bradley Legal Corp, offers a sobering reminder:

"You don’t rise to the level of your income. You fall to the level of your legal structure."

For the best protection, experts recommend setting up an offshore LLC before any legal threats arise. This allows the foreign jurisdiction’s statute of limitations to take effect, making it harder for creditors to challenge asset transfers later.

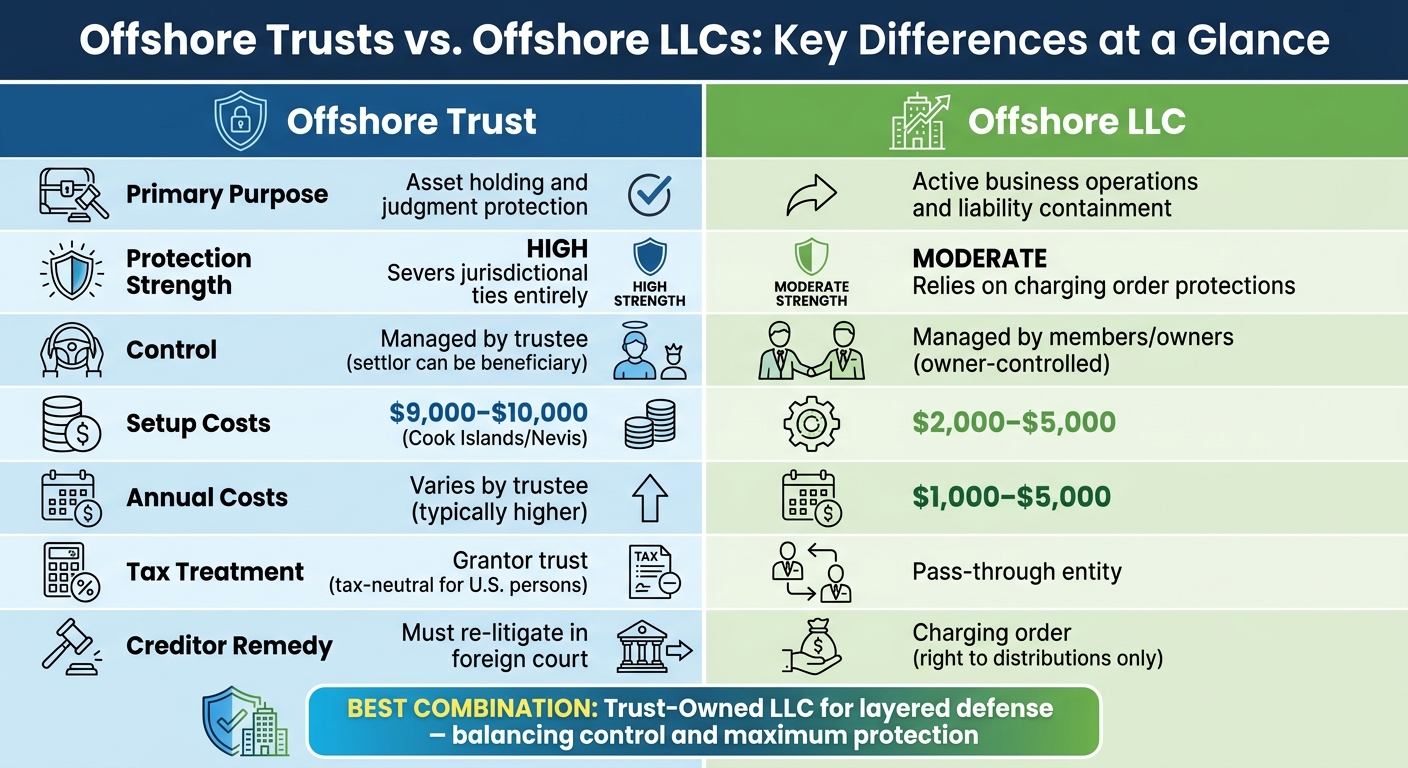

Side-by-Side Comparison: Offshore Trusts vs. Offshore LLCs

Here’s a breakdown of the key differences between offshore trusts and offshore LLCs. The main distinctions lie in how they protect assets and who holds control.

Offshore LLCs offer what’s often called "horizontal protection." This means they isolate liabilities within the entity, preventing them from spilling over to your personal assets. On the other hand, offshore trusts focus on shielding personal wealth from creditors by transferring legal ownership to a foreign trustee.

The strength of protection also varies. Offshore trusts create a legal barrier by being governed under foreign laws, which often disregard U.S. court judgments. For example, in the Cook Islands, creditors must meet the high bar of proving fraudulent intent "beyond a reasonable doubt", making claims almost impossible to win. LLCs, while protective, rely on charging orders, which don’t provide the same jurisdictional separation as trusts.

Below is a table summarizing the key differences to help you decide which structure suits your needs.

Comparison Table: Key Differences

| Factor | Trust | LLC |

|---|---|---|

| Primary Purpose | Asset holding and judgment protection | Active business operations and liability containment |

| Protection Strength | High: Severs jurisdictional ties entirely | Moderate: Relies on charging order protections |

| Control | Managed by a trustee (settlor can be beneficiary) | Managed by members/owners (owner-controlled) |

| Setup Costs | $9,000–$10,000 (Cook Islands/Nevis) | $2,000–$5,000 |

| Annual Costs | Varies by trustee (typically higher) | $1,000–$5,000 |

| Tax Treatment | Grantor trust (tax-neutral for U.S. persons) | Pass-through entity |

| Creditor Remedy | Must re-litigate in foreign court | Charging order (right to distributions only) |

When to Use Each Structure

The table above highlights when each structure works best.

Choose an offshore trust if you’re a high-net-worth individual or work in a high-liability profession – like medicine, law, or real estate development – and need maximum protection from creditor claims. Trusts are especially effective for safeguarding passive wealth when you’re ready to hand over control to an independent foreign trustee.

On the other hand, offshore LLCs are ideal for entrepreneurs managing active businesses or owning risk-laden assets like rental properties. LLCs offer direct control, making them suitable for those who want to stay hands-on while containing operational risks. They are usually more affordable and easier to work with when dealing with banks or online platforms.

One important caveat: offshore trusts may not protect real estate located in the U.S. A notable example is the March 2026 United States v. Huckaby case, where a Nevada trust failed to shield California real estate from an IRS lien. The court applied California law, overriding the Nevada trust’s protections because the property was physically in California. To maximize protection, it’s crucial to set up these structures well before any potential legal issues arise.

Using Offshore Trusts and LLCs Together

High-net-worth individuals often pair offshore trusts with LLCs to achieve strong asset protection while retaining hands-on control over their operations.

How a Trust-Owned LLC Works

Here’s how it works: an offshore trust owns 100% of the membership interest in an offshore LLC. You, as the LLC manager, maintain full control over daily operations, including managing bank accounts and making business decisions. The trustee, meanwhile, holds legal ownership at the trust level.

"An International LLC acts as the operating company for your business and is wholly owned by the Offshore Trust. This means that all profits filter back to the trust, and eventually the beneficiaries." – Steven James, Offshore Consultant

This structure creates what experts call a layered defense. The LLC acts as the operating entity, containing liabilities from business activities – such as lawsuits from tenants or business partners. Meanwhile, the trust serves as a protective shield, safeguarding the LLC’s membership interest from personal judgment creditors.

Some advanced setups use a "Bridge Trust" model. In this arrangement, domestic control is maintained until an "Event of Duress" (like litigation) occurs. At that point, a foreign successor trustee steps in, securing your assets behind an additional layer of jurisdictional protection.

This dual arrangement not only manages operational risks but also establishes a highly effective layer of asset protection.

Benefits of This Combined Approach

The layered defense provided by this structure offers practical, real-world advantages. Asset protection attorney Brian T. Bradley explains:

"LLCs contain operational liability. Partnership charging-order rules limit creditor remedies. The offshore trust layer addresses judgment collection risk. The layers are not redundant. They solve different legal problems." – Brian T. Bradley, Esq.

Here’s how it plays out: if your rental property LLC faces a lawsuit, liability is confined to that entity, leaving the trust-held assets untouched. On the other hand, if you’re hit with a personal judgment – say, from a car accident – creditors can’t easily access the LLC. Why? Because the trust owns the LLC, and the trust operates under foreign laws that don’t recognize U.S. court orders.

Another advantage is enhanced privacy. In jurisdictions like Nevis, offshore LLCs don’t require ownership details to appear in public records. When a trust owns the LLC, your name is completely absent from the registry. You retain control as the manager, but the legal ownership trail ends with the foreign trustee.

Experts emphasize the importance of professional drafting and choosing reputable jurisdictions. Setting up such a structure typically costs around $10,000 for a Cook Islands trust, plus additional fees for forming the LLC.

How to Choose the Right Structure

Deciding between an offshore trust and an LLC plays a pivotal role in shaping your asset protection strategy. After comparing offshore options, the next step is selecting the structure that aligns with your assets and risk tolerance.

Key Decision Factors

This decision isn’t about flashy legal documents – it’s about ensuring your structure holds up under scrutiny, whether from a creditor’s attorney or a bankruptcy trustee. Asset protection attorney Brian T. Bradley emphasizes:

"You don’t rise to the level of your income. You fall to the level of your legal structure." – Brian T. Bradley, Esq.

The best time to establish your legal structure is before any legal threats emerge.

Start by evaluating your asset types. Offshore trusts are particularly effective for passive investments like securities or collectibles. For real estate, jurisdictional rules come into play – property laws are governed by the state where the property is located. In these cases, an LLC can help isolate operational risks, while a trust can protect your ownership interest in the LLC.

Your risk profile also matters. For instance, 59% of U.S. physicians have been sued at least once, and by age 55, 82% of specialists have faced litigation. In California alone, nearly 470,000 civil lawsuits were filed in 2023–2024, equating to about 1,190 cases per 100,000 residents. High-risk professionals often benefit from the extra protection provided by offshore trusts, which create a strong "jurisdictional firewall."

Balancing control and protection is another critical factor. LLCs allow you to maintain direct management control, but this can also make them more vulnerable to court orders. Trusts, on the other hand, require you to transfer legal ownership to an independent trustee. While this can feel like a loss of control, it’s essential for strong creditor protection. Courts may use "alter ego" arguments to access assets if you retain too much direct control.

And remember – timing is key. Setting up your structure after legal threats arise can lead to accusations of fraudulent transfers. These factors are central to the recommendations provided by Global Wealth Protection.

Custom Solutions from Global Wealth Protection

With these considerations in mind, Global Wealth Protection offers tailored strategies to meet your specific needs. Whether you’re looking for a Cook Islands trust for maximum creditor protection, a Nevis LLC for operational flexibility, or a trust-owned LLC for layered defense, their team manages the entire process.

Their services include full offshore company formation, covering filings, certifications, and bank introductions. For high-net-worth clients, they also provide offshore trusts and private interest foundations, primarily in Anguilla, with options for other jurisdictions depending on your requirements. Setting up a Cook Islands trust typically starts at $10,000, with additional fees for LLC formation.

Through personalized consultations, Global Wealth Protection helps you navigate jurisdiction selection, tax strategies, and compliance. Their GWP Insiders membership program offers ongoing access to internationalization strategies and exclusive resources for managing your offshore structures over time.

The bottom line: asset protection isn’t a one-size-fits-all approach. Your structure should reflect your asset types, risk exposure, and operational goals – and it must be established well before any legal challenges arise.

Conclusion

Deciding between an offshore trust and an offshore LLC comes down to understanding your unique needs and goals. Offshore trusts are ideal for creating a strong legal barrier, effectively distancing your assets from personal creditors and offering powerful protection. On the other hand, offshore LLCs are better suited for those seeking operational flexibility and limited liability, particularly for active business ventures where you want to maintain direct control.

For many, the best approach is to combine these tools. A trust-owned LLC brings together the operational benefits of an LLC with the creditor protection of an offshore trust. This hybrid structure addresses both day-to-day risks and potential legal threats, making it a comprehensive solution.

Your choice should depend on factors like the type of assets you own, your exposure to risks, and how much control you want to retain. For instance, real estate investors managing rental properties often lean toward LLCs, while professionals in high-risk fields may opt for the stronger safeguards offered by offshore trusts. The Cook Islands, in particular, has an impressive 40-year history of protecting properly structured trusts from U.S. creditors when the trust was created before any claims arose.

Timing is everything. Setting up these structures after legal threats become apparent can backfire, as courts may view such actions as fraudulent transfers. U.S. bankruptcy courts, for example, have look-back periods of up to 10 years. To avoid this, planning ahead – before any claims arise – is essential.

Whether you aim to protect passive investments or manage active business operations, the right combination of an offshore trust and LLC can provide a strong defense. Tailoring your strategy to match your asset profile and risk exposure ensures that your protection plan is both effective and reliable. Global Wealth Protection specializes in creating customized strategies, from Cook Islands trusts to hybrid structures, designed to stand firm when it matters most.

FAQs

Can an offshore trust protect U.S. real estate?

Offshore trusts can be a useful tool for safeguarding movable assets such as cash or securities. However, when it comes to real estate, things get trickier. Since real estate is immovable and remains under U.S. jurisdiction, courts can still enforce liens or orders on the property, even if it’s owned by a foreign trust.

That said, there are some workarounds. Methods like equity stripping or holding the property through LLCs owned by the trust might provide a layer of indirect protection. Still, it’s important to note that these strategies come with their own limitations and may not fully shield the property from legal actions.

Can a U.S. judge force me to return LLC funds?

A U.S. judge can mandate the return of LLC funds through legal avenues like a court judgment or the enforcement of an order. However, whether this can happen depends heavily on factors such as the jurisdiction and how the LLC is structured.

What IRS filings do offshore trusts and LLCs require?

Offshore trusts often come with specific reporting requirements. For instance, individuals involved with these trusts – whether as grantors, beneficiaries, or recipients of distributions – typically need to file Form 3520. Additionally, Form 3520-A is required to disclose details about the trust’s income and structure.

If you hold foreign accounts with a balance exceeding $10,000, you’ll also need to submit the FBAR (Foreign Bank Account Report).

For offshore LLCs, the paperwork varies. You might need to file Form 8832 to determine the entity’s tax classification. If the LLC holds foreign accounts, the FBAR applies here as well. Other potential forms, such as Schedule C or Form 5471, may be necessary depending on the LLC’s ownership structure and income sources.