Moving your assets abroad can safeguard wealth, provide diversification, and enhance estate planning. However, it requires precise timing, compliance with U.S. tax laws, and selecting the right jurisdiction. Here’s what you need to know:

- U.S. Tax Rules: Americans are taxed on worldwide income. Reporting is required for foreign accounts exceeding $10,000 (FBAR) or assets over $50,000 (Form 8938). Non-compliance can lead to severe penalties.

- Timing: Act before economic downturns or tax law changes to minimize losses from exit taxes or currency devaluation.

- Jurisdictions: Options like Nevis, Belize, and the Cook Islands offer strong asset protection. Choose based on your goals – litigation protection, estate planning, or cost-efficiency.

- Structures: Offshore trusts, LLCs, and bank accounts are common tools. Set these up before any legal challenges arise.

- Compliance: Strict adherence to regulations (FBAR and FATCA requirements) is critical. Penalties for non-compliance include fines up to 50% of account balances.

Work with professionals to ensure legal and financial compliance while protecting your assets globally.

When to Move Assets Abroad: Timing Your Decision

Deciding when to move your assets offshore depends on economic trends, tax law changes, and your personal financial situation. Timing is everything – acting before an economic downturn can protect your wealth. High-net-worth individuals who delay until a crisis unfolds often face steep losses. Exit taxes and currency devaluation alone can chip away 25% to 35% of wealth, and in extreme cases, total losses could range from 55% to 110%.

The key is to act when clear economic signals, tax policy shifts, or personal financial milestones open the door to safeguarding your assets internationally.

Economic Warning Signs That Point to Diversification

Certain economic indicators can signal the need to reduce your reliance on domestic assets. For instance, when a country’s debt-to-GDP ratio exceeds 100%, financial experts often recommend keeping no more than 40% of your portfolio in domestic liquid assets. Currency devaluation is another red flag – it erodes purchasing power globally, even if your account balances appear stable. This is especially true when local currencies weaken against stronger ones like the U.S. dollar, Swiss franc, or Singapore dollar. Political instability adds to the risk, often leading to capital controls that lock wealth within national borders.

Market performance also plays a role. Between 2014 and 2024, U.S. markets delivered annual returns of 13.1%, outpacing international markets by 7.7%. However, projections for the next decade suggest a shift: international stocks have a 70% chance of outperforming U.S. stocks, with median annual returns of 6.1% compared to 4.3% for U.S. markets.

Monetary policy changes are another clue. Rising interest rates indicate higher borrowing costs and slower business investments, while shifts in the Consumer Price Index (CPI) can reveal emerging opportunities. Additionally, new tax laws, labor regulations, or tariff adjustments can disrupt business operations and increase costs, making diversification more appealing.

These economic indicators highlight the importance of staying alert to tax law changes that could impact your asset protection strategy.

How Tax Law Changes Affect Your Decision

Changes in U.S. tax laws can significantly influence both the cost and complexity of moving assets abroad. Unlike most countries, the U.S. taxes its citizens on worldwide income, even if they live overseas. The Tax Cuts and Jobs Act (TCJA) and subsequent updates have added layers of complexity. For individuals with over $2 million in assets, exit taxes can be a major hurdle. The IRS treats all assets as if sold at fair market value the day before leaving the U.S. tax system, resulting in taxes on 15% to 30% of unrealized capital gains.

"It’s effectively the IRS’s last chance to tax accumulated appreciation before the individual leaves the U.S. tax system."

- Ada K. Colomb, International Estate Tax Attorney, Vacovec, Mayotte & Singer

Recent legal updates in 2025 and 2026 introduced Section 2801 and Form 708, which impose a 40% tax on gifts or inheritances from "covered expatriates" to U.S. heirs. Notably, U.S. expatriation rates surged by 102% in early 2025 compared to the previous quarter. These developments underscore the importance of acting before major tax reforms take effect.

Personal Life Events That Trigger Asset Protection

Certain life events can also make international asset protection more relevant and practical. For business owners and executives, growing liability risks often call for professional strategies to globalize wealth. Facing litigation? Offshore structures can offer protection. While a U.S. court might order the repatriation of funds held in your name, combining an offshore account with offshore trusts and foundations can help shield assets from such orders.

For retirees, the focus shifts to preserving wealth for heirs, managing distributions, and minimizing tax exposure. Long-term care planning also becomes critical, as chronic illness or nursing home costs can quickly drain savings. Transferring assets at least five years before applying for Medicaid can help avoid penalties tied to look-back rules.

Offshore asset protection is generally most cost-effective when liquid assets exceed $250,000. Below this amount, annual fees for offshore accounts ($500 to $2,500) and tax compliance costs ($3,000 to $5,500) can eat into your funds disproportionately. By 2025, around 1.5 million Americans had foreign accounts for reasons like business, diversification, or asset protection.

Knowing when to move assets is just the first step – meeting the legal requirements that follow is equally important.

Meeting US and International Legal Requirements

When moving assets across borders, compliance with strict reporting rules is non-negotiable. U.S. law requires full disclosure of foreign financial accounts and assets. Failing to file the necessary forms can lead to steep penalties. The IRS has created an extensive reporting system to monitor offshore holdings, and foreign banks routinely share account details with U.S. authorities.

"The FBAR is also a tool used by the U.S. government to identify persons who may be using foreign financial accounts to circumvent U.S. law."

Knowing which forms to file and when to submit them is key to staying compliant while managing international wealth. Below, we’ll break down the requirements for FBAR and Form 8938, and explore the role of FATCA and tax treaties in global financial compliance.

FBAR and Form 8938 Filing Requirements

If you’re a U.S. taxpayer with foreign financial accounts, you must file an FBAR (FinCEN Form 114) if the total value of all accounts exceeds $10,000 at any point during the year. This $10,000 threshold applies to the combined balance of all accounts, not just individual ones. The form is due by April 15, with an automatic extension to October 15. Filing is done electronically through FinCEN‘s BSA E-Filing System, and account records must be kept for five years.

Under FATCA (Foreign Account Tax Compliance Act), you may also need to file Form 8938 with your annual tax return. The filing thresholds vary based on residency and marital status. For single U.S. residents, the thresholds are $50,000 at year-end or $75,000 at any time during the year. For U.S. citizens living abroad, the thresholds increase to $200,000 and $300,000, respectively. Unlike the FBAR, Form 8938 covers a wider range of assets, such as foreign stocks, partnership interests, and certain foreign entities.

| Feature | FBAR (FinCEN Form 114) | Form 8938 (FATCA) |

|---|---|---|

| Reporting Threshold | Over $10,000 aggregate at any time | $50,000–$600,000 depending on residency and filing status |

| Where to File | FinCEN (BSA E-Filing System) | IRS (attached to Form 1040) |

| Due Date | April 15 (automatic extension to Oct 15) | Due with your tax return |

| Assets Covered | Bank, brokerage, and mutual fund accounts | Accounts, foreign stock, partnership interests, etc. |

Failure to file an FBAR can result in fines of up to $100,000 or 50% of the account balance. For Form 8938, the penalties start at $10,000, with additional fines for prolonged non-compliance. A 40% penalty may also apply to tax understatements linked to undisclosed foreign assets. Other forms may be required depending on the type of offshore asset. For instance, Form 3520 is necessary for foreign trusts or gifts over $100,000, while Forms 5471 and 8865 are used for foreign corporations and partnerships.

FATCA Rules and Tax Treaties Explained

FATCA has reshaped how the U.S. monitors offshore wealth. It requires foreign financial institutions, such as banks and brokers, to report U.S. account holders directly to the IRS. This makes it extremely difficult to hide foreign assets.

"The Foreign Account Tax Compliance Act (FATCA) is an important development in U.S. efforts to combat tax evasion by U.S. persons holding accounts and other financial assets offshore."

- Internal Revenue Service

FATCA applies to "U.S. persons", which includes citizens, residents, and entities like corporations or trusts formed under U.S. law. If more than $5,000 in gross income tied to foreign assets is omitted, the IRS can extend the audit window from three to six years.

Tax treaties between the U.S. and other countries aim to prevent double taxation. They allow taxpayers to claim a Foreign Tax Credit (FTC) for taxes paid to foreign governments. This credit offsets U.S. tax liability dollar-for-dollar and applies to all types of income, unlike the Foreign Earned Income Exclusion (FEIE), which only covers earned income up to $130,000 for the 2025 tax year. In high-tax countries, the FTC often provides more advantages, as it applies to investment income and allows for continued retirement contributions.

FATCA also influences investment strategies. U.S. expats are often advised to avoid foreign mutual funds and ETFs, as they are classified as Passive Foreign Investment Companies (PFICs). Owning PFICs triggers the complex filing of Form 8621 and may lead to high tax liabilities. Instead, U.S.-domiciled ETFs or individual stocks are generally better options to avoid these complications.

If you’ve missed required filings, the IRS offers programs to help. The Streamlined Filing Compliance Procedures (SFCP) are designed for non-willful failures, while the Voluntary Disclosure Practice (VDP) is available for cases with potential criminal exposure. Taking advantage of these programs can significantly reduce penalties. Understanding FATCA and related rules is crucial for maintaining compliance as you expand your financial portfolio internationally.

Selecting the Right Offshore Jurisdiction

When it comes to protecting your wealth offshore, choosing the right jurisdiction is a key decision. Different locations offer varying levels of legal protection, privacy, and costs. The best choice depends on your specific goals – whether that’s shielding assets from litigation, planning your estate, or diversifying your financial portfolio.

The strength of a jurisdiction’s asset protection laws often lies in how difficult they make things for creditors. For example, some top jurisdictions, like Nevis and the Cook Islands, don’t recognize U.S. court judgments. This means creditors must pursue legal action locally, often facing steep hurdles. In these jurisdictions, creditors are required to prove fraudulent transfers with a high standard of evidence, equivalent to criminal certainty. This makes claims significantly harder to win.

"Jurisdiction matters, but it matters less than timing, trust structure, and trustee quality."

- Jon Alper, Asset Protection Attorney

Procedural barriers are just as important as legal protections. Nevis, for instance, requires creditors to post a bond of around $100,000 before filing a lawsuit against a trust. Belize offers immediate protection – assets transferred into a properly structured Belize trust are shielded from fraudulent transfer claims as soon as they are funded. The Cook Islands also boasts a 40-year history without a single creditor successfully challenging a properly established trust in local courts.

Other factors to consider include political stability, banking infrastructure, and the quality of local trustees. Even with strong laws, a jurisdiction with weak trustees or unstable governance won’t provide lasting protection. Look for jurisdictions with regulated, licensed, and insured trustees, a stable legal system (often based on English Common Law), and a track record of supporting international business practices. Singapore and Hong Kong, for instance, offer excellent digital banking options.

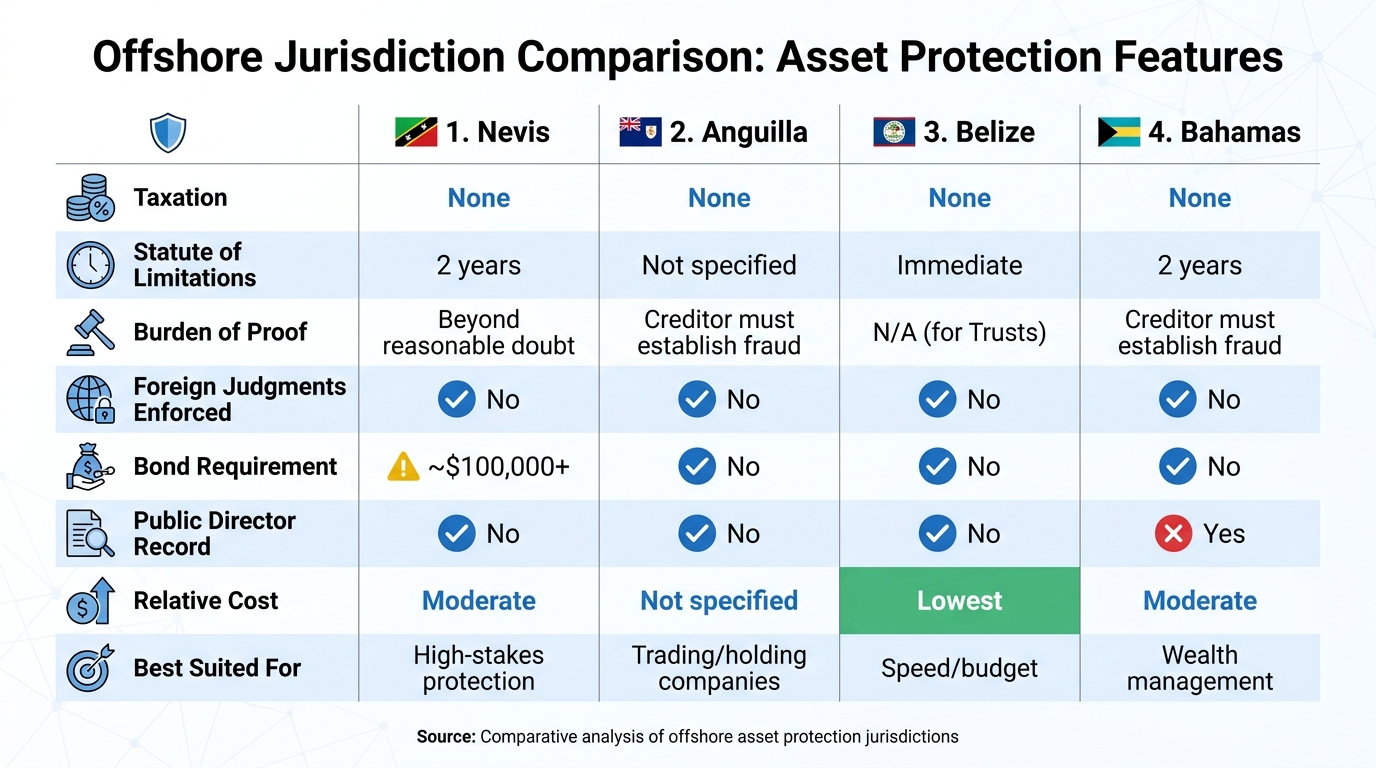

Jurisdiction Comparison: Nevis, Anguilla, Belize, and the Bahamas

Here’s a closer look at how some of the most popular offshore jurisdictions compare:

- Nevis: Known for its aggressive asset protection laws, Nevis requires a $100,000+ bond for lawsuits and has a short two-year statute of limitations. It also blocks Mareva injunctions, preventing creditors from freezing assets during litigation.

- Belize: A budget-friendly option with immediate asset protection upon funding. Belize is ideal for those needing quick solutions at a lower cost. It also provides strong banking privacy, as account details are only disclosed under court orders tied to criminal investigations.

- The Bahamas: A well-established financial hub, the Bahamas is favored for dynasty planning and life insurance. While its asset protection laws are less aggressive than Nevis, it offers stability and a 120-day limit for challenging transfers as fraudulent.

- Anguilla: A British Overseas Territory offering solid privacy protections and a neutral tax environment. While not as aggressive as Nevis, it’s a reliable choice for international trading and holding companies.

| Feature | Nevis | Anguilla | Belize | Bahamas |

|---|---|---|---|---|

| Taxation | None | None | None | None |

| Statute of Limitations | 2 years | Not specified | Immediate | 2 years |

| Burden of Proof | Beyond reasonable doubt | Creditor must establish fraud | N/A (for Trusts) | Creditor must establish fraud |

| Foreign Judgments Enforced | No | No | No | No |

| Bond Requirement | ~$100,000+ | No | No | No |

| Public Director Record | No | No | No | Yes |

| Relative Cost | Moderate | Not specified | Lowest | Moderate |

| Best Suited For | High-stakes protection | Trading/holding companies | Speed/budget | Wealth management |

What to Look for When Choosing a Jurisdiction

Start by clarifying your main objective. If you’re concerned about litigation or work in a high-risk profession, Nevis or the Cook Islands are strong choices due to their robust legal barriers. For estate planning across generations, consider the Cayman Islands or the Bahamas. The Cayman Islands, for example, removed perpetuity limits in 2024, allowing for unlimited multi-generational trusts. If cost is a priority, Belize offers the most affordable entry point with immediate asset protection.

Another key factor is whether the jurisdiction enforces U.S. court orders. The most effective jurisdictions do not, forcing creditors to litigate locally, which adds time, cost, and complexity to their efforts. Jurisdictions that have abolished tools like Mareva injunctions are also worth considering, as they prevent creditors from freezing assets during legal disputes.

Banking access is a practical consideration as well. If a bank has U.S. branches or correspondent relationships, it could be subject to domestic garnishment orders. To avoid this, check whether the bank is FDIC-insured – if it is, it falls under U.S. jurisdiction and may not be suitable for offshore asset protection.

"A bank with no U.S. footprint has no obligation to comply with a U.S. court order."

- Gideon Alper, Attorney

Finally, align your financial capacity with the costs of the jurisdiction. Offshore trusts are typically viable for assets exceeding $1,000,000. For instance, Cook Islands trusts cost $20,000–$25,000 to establish and $5,000–$8,000 annually. Nevis offers more moderate costs, while Belize is the most budget-friendly option. Keep in mind, the quality of your trustee can often outweigh the statutory strength of the jurisdiction itself. Choose wisely to create a well-rounded asset protection plan that complements your broader financial strategy.

sbb-itb-39d39a6

How to Structure and Transfer Assets Legally

To effectively manage your wealth across borders, start by choosing a legal structure that aligns with your goals. Options like offshore trusts, private interest foundations, and offshore companies allow you to move assets abroad while staying compliant with U.S. tax laws. Each option serves specific purposes, and many opt for a mix of these structures to enhance asset protection.

Before transferring your assets, define your primary goal. For protection against lawsuits, an offshore trust in jurisdictions like the Cook Islands or Nevis is often the strongest option. If your focus is estate planning for future generations, consider a foundation, trust, or private family office in the Cayman Islands. On the other hand, an offshore company is ideal for holding business assets or managing international operations.

Timing is critical. Setting up these structures before facing legal challenges is key. Transfers made when you’re financially stable and free of creditor claims are less likely to face accusations of fraud. For instance, Belize provides immediate protection for assets transferred into a trust, provided no fraudulent intent is involved.

Creating Offshore Trusts and Foundations

Setting up an offshore trust involves a few important steps. First, you’ll need an attorney to draft a Deed of Trust, which details how the trust will operate, including the trustee’s powers, the beneficiaries, and distribution conditions. Then, appoint a non-U.S.-based trustee in your chosen jurisdiction. Many recommend corporate trustees because they provide access to professional legal and accounting services and carry liability insurance.

Once your trust is set up, you’ll transfer ownership of your assets – like property titles, LLC shares, bank accounts, or cryptocurrency holdings – into the trust. Some individuals prefer a hybrid approach, such as forming an offshore LLC and placing it within an offshore trust for added security.

Alternatively, private interest foundations are a popular choice in Panama. These structures are similar to trusts, offering confidentiality and flexibility for holding global assets. The setup process involves drafting a Foundation Charter, appointing a foundation council, and transferring assets.

The effectiveness of these tools is well-documented. For example, Cook Islands trusts boast a 96% success rate in protecting assets over three decades, while Nevis trusts have a perfect record against U.S. court challenges due to their strong legal protections. The Cayman Islands, home to over 100,000 active trusts managing more than $6 trillion in assets, is another prime location.

"Offshore does not mean tax-free."

- Blake Harris, Founding Attorney, Blake Harris Law

While there’s no legal minimum to fund an offshore trust, most experts suggest starting with at least $250,000 to justify setup and maintenance costs. In Nevis, you can establish a trust in just 24 to 48 hours, while other jurisdictions may take longer. Belize stands out for its affordability, with setup fees roughly 32% lower than those in similar jurisdictions.

U.S. taxpayers must also stay on top of required filings to avoid penalties. For instance, Form 3520 is necessary when transferring assets to a foreign trust, while Form 3520-A must be filed annually to report the trust’s income and structure. Non-compliance can lead to severe penalties, including fines of up to $60,000 for failing to file Form 8938.

Next, let’s explore how to establish an offshore company to further diversify your asset strategy.

How to Form an Offshore Company

If your goal is to manage international business operations, hold assets, or oversee investments, forming an offshore company could be the right move. Start by selecting a jurisdiction that fits your business needs. For example, Anguilla is often chosen for its strong privacy protections, while Belize offers cost-effective options. The Bahamas is another favorite due to its robust financial infrastructure.

The registration process typically involves picking a company name, appointing directors (some jurisdictions may require local directors), and filing articles of incorporation. In many cases, this can all be completed remotely through a registered agent or service provider.

Opening a bank account for your offshore company requires meeting strict KYC (Know Your Customer) and AML (Anti-Money Laundering) standards. Expect to provide documents like proof of identity, proof of address, business plans, and evidence of the source of funds. Partnering with firms that have established relationships with banks in your chosen jurisdiction can speed up this process.

It’s wise to prepare asset documentation – such as brokerage statements and cryptocurrency wallet details – early. This preparation can significantly reduce delays during the transfer process.

Many offshore jurisdictions offer zero local taxation for companies that don’t conduct business within their borders. However, as a U.S. citizen, you’re still required to report worldwide income and pay taxes at individual rates. Offshore companies are tools for structuring assets, not for avoiding taxes.

Once your company is established, managing currency exchanges and international transfers becomes an important next step.

Handling Currency Exchange and International Transfers

When moving assets internationally, you’ll need to navigate exchange risks, fees, and regulations carefully. The goal is to minimize losses while ensuring compliance with U.S. and international laws.

Choosing jurisdictions with stable political and economic environments – like Singapore or the Cook Islands – helps reduce risks like sudden currency controls or asset seizures. Singapore, for example, manages over $4 trillion in assets and holds a AAA credit rating, making it a top choice for wealth management.

It’s also critical to ensure that transfers happen while you’re solvent. Transfers made under financial duress could be deemed fraudulent by courts.

"A U.S. court may demand the return of assets in your trust if it determines that the transfer of assets was fraudulent."

- Blake Harris Law

If your foreign accounts exceed $10,000 in aggregate value at any point during the year, you must file an FBAR (Report of Foreign Bank and Financial Accounts) by June 30. Failing to do so can result in penalties of up to 50% of the account balance or $100,000 – whichever is greater – for willful violations. Non-willful violations can still incur penalties of up to $10,000.

Additionally, you’ll need to file Form 8938 (FATCA) if your foreign financial assets exceed certain thresholds, which vary depending on your filing status. Penalties for non-compliance can reach $10,000, with additional fines of $10,000 for every 30 days of non-filing after an IRS notice, up to a maximum of $60,000.

| Requirement | Threshold for Filing | Potential Penalty (Non-Willful) | Potential Penalty (Willful) |

|---|---|---|---|

| FBAR (FinCEN 114) | > $10,000 aggregate value | Up to $10,000 | Greater of $100,000 or 50% of account balance |

| Form 8938 (FATCA) | Varies by filing status | $10,000 (plus $10,000 per 30 days late) | Criminal penalties may apply |

| Form 3520 | Any transfer to a foreign trust | Steep penalties for failure to file | N/A |

To streamline the process, work with attorneys who have direct relationships with foreign trustees and financial institutions. This can help avoid delays and ensure compliance with all regulatory requirements, making your transfers quicker and more efficient. For personalized guidance on your specific situation, you can schedule private consultations with our experts.

Working with Professionals for Asset Globalization

Protecting an international portfolio requires more than just understanding regulations – it demands the expertise of seasoned professionals. Without proper guidance, navigating the maze of legal requirements can lead to costly penalties.

How Global Wealth Protection Services Can Help

Specialized firms take on the heavy lifting of creating offshore structures, ensuring they comply with both U.S. and international laws. These experts craft strategies tailored to your financial goals, whether you’re focused on shielding assets from lawsuits, planning your estate, or managing international business operations. With experience in jurisdictions like the Cook Islands, Belize, and Nevis, these professionals help protect your wealth from creditors, lawsuits, and other risks.

Dual-jurisdiction professionals play a critical role by aligning U.S. and international legal efforts to ensure compliance. They work closely with regulated trustees and financial institutions, simplifying the process of setting up accounts and transferring assets. For example, in Nevis, creditors are required to post a bond of $100,000 or more before they can file a lawsuit against a trust.

Their services don’t stop at the setup phase. These firms also handle ongoing compliance, ensuring that all necessary forms are filed correctly to avoid penalties. Additionally, they provide guidance on avoiding complex investment vehicles like Passive Foreign Investment Companies (PFICs), which can lead to burdensome annual filings and high tax obligations.

Custom Consultations for High-Net-Worth Individuals

Professionals in this field also offer personalized strategies to meet the specific needs of high-net-worth individuals. Through one-on-one consultations, they evaluate your financial situation, identify vulnerabilities, and recommend the most suitable offshore jurisdictions. For instance, they might suggest a Cook Islands trust, which has a one-year statute of limitations, or a Belize foundation, which offers immediate asset protection.

These consultations also help you weigh the pros and cons of different jurisdictions. The Cook Islands, for example, is prized for its strong privacy laws and refusal to recognize foreign court judgments, while Singapore is valued for its stability as a global financial hub. A skilled advisor can guide you toward the jurisdiction that aligns with your long-term goals.

Offshore structures are not a "set it and forget it" solution. They require consistent maintenance, annual filings, and adjustments to keep pace with evolving laws and personal circumstances. Ongoing professional support ensures that your asset protection strategies remain effective, safeguarding your wealth for the future.

Conclusion: Your Next Steps for Moving Assets Abroad

Moving assets abroad requires careful planning, precise timing, and strict adherence to legal requirements. The success of your wealth protection strategy often hinges on understanding the right time to act, selecting the most suitable jurisdiction, and staying compliant with both U.S. and international laws.

Start by identifying your primary goal – whether it’s shielding assets from lawsuits, optimizing taxes, or diversifying investments. This clarity will shape every step, from deciding between an offshore trust, LLC, or foreign bank account to pinpointing the best jurisdiction. While the typical minimum asset threshold for making such moves financially viable is $250,000, the more pressing question is whether your wealth is at enough risk to justify offshore protection. Once your objectives are clear, a strong compliance plan becomes essential for navigating the complexities of asset globalization.

Staying compliant with FBAR and FATCA rules is non-negotiable to avoid steep penalties. For perspective, about 9 million Americans lived abroad in 2020, yet only 1.4 million taxpayers filed FBARs to report foreign assets. Don’t risk falling into the non-compliant majority.

Given the challenges of dual-jurisdiction compliance, risks tied to fraudulent transfers, and ongoing reporting requirements, expert guidance is invaluable. Global Wealth Protection offers tailored consultations to assess your financial situation, pinpoint vulnerabilities, and recommend offshore structures that align with your goals.

To tackle these complexities effectively, work with specialists experienced in both U.S. and international asset protection. Establish a compliance calendar, audit your assets to determine which are suitable for transfer, and maintain detailed records of every transaction. With the right strategy, executed and monitored properly, you can secure your wealth for generations to come.

FAQs

What’s the safest first step to move assets offshore legally?

Opening and funding an offshore bank account in a well-regarded jurisdiction is often the safest initial step. Locations like the Cayman Islands or Switzerland are popular due to their strong asset protection laws. To stay on the right side of the law, it’s essential to consult a qualified legal advisor. They can guide you through U.S. tax reporting requirements, such as FBAR (Foreign Bank Account Report) and FATCA (Foreign Account Tax Compliance Act).

Make sure to provide all necessary documentation, verify your identity, and meet every reporting obligation. Following these steps ensures compliance and keeps everything above board.

Which offshore structure fits me best: trust, LLC, or bank account?

The best offshore structure varies based on your specific objectives:

- Trusts: Great for asset protection and estate planning, as they offer strong legal protections and adaptable management options.

- LLCs: Useful for protecting against liability while providing flexibility for managing businesses or investments.

- Bank accounts: Helpful for handling international transactions, though they don’t automatically safeguard assets.

It’s important to stay compliant with U.S. tax laws when selecting any offshore structure.

How do I stay compliant with FBAR and FATCA every year?

To ensure compliance, it’s crucial to report foreign accounts and assets both accurately and on time. The FBAR (FinCEN Form 114) must be filed electronically if the combined value of your foreign accounts exceeded $10,000 at any point during the year. Meanwhile, the FATCA (Form 8938) applies to foreign assets that surpass specific thresholds, which vary depending on your filing status.

Both forms need to be submitted annually, and FATCA is filed alongside your tax return. Make sure to maintain detailed records as proof for your reports. If you require additional time, extensions are available to help meet these obligations.