Protecting your business and personal wealth requires more than just focusing on revenue. Without proper planning, entrepreneurs risk losing significant amounts annually due to poor tax strategies, weak asset protection, and missed opportunities. This guide outlines a six-step process to safeguard your assets, ensure legal compliance, and maintain financial security.

Key Takeaways:

- Set a fixed annual review date to stay consistent and proactive.

- Organize all asset records into a comprehensive inventory, covering financial accounts, real estate, business interests, and liabilities.

- Review legal structures and tools like LLCs, trusts, and compliance with tax regulations to avoid vulnerabilities.

- Evaluate insurance policies to ensure adequate coverage against lawsuits, cyber risks, and operational changes.

- Create an action plan to address gaps, prioritize risks, and assign tasks with clear deadlines.

- Refine the process yearly by analyzing what worked, improving team collaboration, and updating your checklist.

By following this structured approach, you can move from fragmented management to a well-coordinated strategy that protects your wealth and prepares for future challenges.

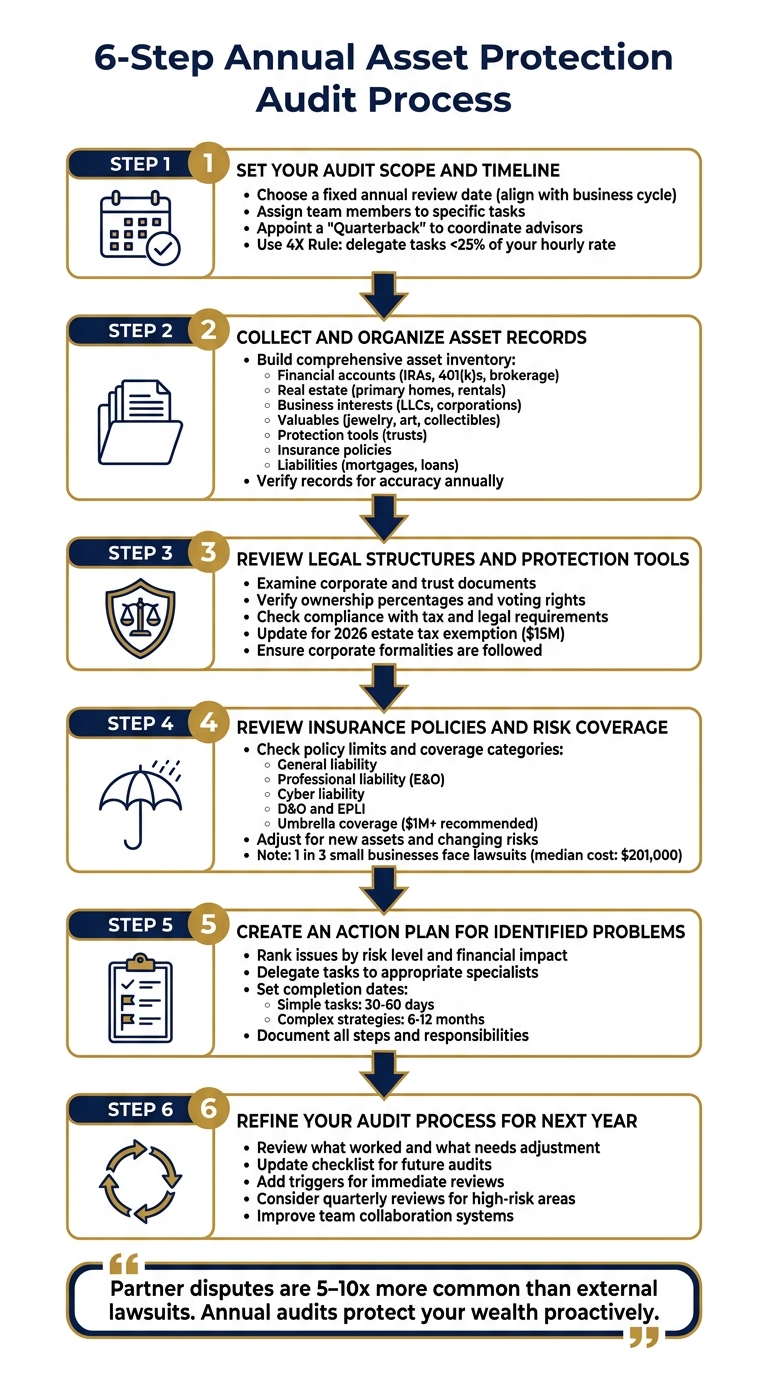

Step 1: Set Your Audit Scope and Timeline

Laying out clear boundaries and a schedule is crucial to keeping your audit on track, especially during busy times. The goal here is to shift asset protection from a reactive approach to a more structured and proactive process. Start by choosing a review date that fits seamlessly into your business cycle.

Choose a Fixed Annual Review Date

Pick a specific annual review date that aligns with your business operations and any regulatory deadlines. For example, Delaware entities should plan their audit before the March 1 annual report deadline. Many businesses opt for Q1 since it follows the year-end close and comes before tax filing season.

Avoid scheduling audits during your peak revenue periods. For instance, if your e-commerce business sees a surge in Q4 sales, a February audit might be far more practical than one in December. Sticking to the same date every year builds consistency, making it less likely to be overlooked.

Assign Team Members to Specific Tasks

Delegating tasks ensures that the right expertise is applied where it’s needed most. Start by appointing a "Quarterback" to oversee and coordinate your advisors. Use the 4X Rule: delegate any task that costs less than 25% of your effective hourly rate (calculated as annual revenue divided by working hours).

Break down responsibilities among specialists:

- A tax strategist can review your entity structures.

- An estate planning attorney should examine trust documents.

- An insurance expert can evaluate your coverage limits.

- An investment advisor can align your personal portfolio with your business assets.

"You find yourself trapped in the center, desperately trying to manage professionals who speak different languages and often work at cross-purposes." – Dew Wealth Management

Hold a kickoff meeting to assign each professional their specific tasks and deadlines. This step ensures everyone is on the same page, preventing disjointed efforts and reducing the risk of missed opportunities.

sbb-itb-39d39a6

Step 2: Collect and Organize Asset Records

Pulling together all your asset details in one secure place is a critical step in streamlining your audit. The goal is to have everything documented before potential legal disputes or creditor issues arise. Being proactive here is key to protecting your wealth from unexpected challenges.

Build a Comprehensive Asset Inventory

Once your audit plan is ready, focus on creating an organized list of all your assets. Be thorough and include the following:

- Financial accounts: Emergency funds, IRAs, 401(k)s, and brokerage accounts.

- Real estate: Primary homes and rental properties, along with their current equity.

- Business interests: LLCs, corporations, or family partnerships.

- Valuables: Jewelry, art, and collectibles.

- Protection tools: Irrevocable trusts, family trusts.

- Insurance policies: Life, disability, professional malpractice, umbrella coverage, and cybersecurity riders.

- Liabilities: Mortgages, car loans, student loans, and credit card balances.

For each asset, note the ownership structure (e.g., individual, LLC, or trust), ownership percentages, and any liens or encumbrances. Don’t overlook digital assets or intellectual property – include registration details and any royalties. Make sure to securely store credentials for digital assets.

Verify Records for Accuracy and Completeness

Once your inventory is complete, double-check everything to ensure nothing is missing or outdated. Document recent acquisitions and transfers, and cross-check your records with bank statements, property deeds, operating agreements, or appraisals. It’s a good idea to revisit and update your asset records every year.

Make sure beneficiary designations on financial accounts and insurance policies are up to date and consistent with your legal structures. For business assets, confirm that proper formalities are followed – such as separate accounts, meeting minutes, and clear documentation – to avoid risks like piercing the corporate veil. Running a credit report is also a smart move to catch any errors or fraudulent activity that might affect your asset values or borrowing ability. Regular checks like these ensure your protection strategies remain solid and legally sound.

Step 3: Review Legal Structures and Protection Tools

Once you’ve organized your asset records, the next step is to evaluate the legal frameworks safeguarding those assets. Over time, older structures may no longer align with your evolving business needs or the latest regulations. With a clear inventory of your assets, this review ensures that your LLCs, trusts, and other legal mechanisms are still functioning as intended.

Examine Corporate and Trust Documents

Start by reviewing key documents like operating agreements, trust deeds, shareholder agreements, and bylaws. These should reflect your current business operations. Many entrepreneurs find discrepancies between formal documentation and how decisions are actually made – often through informal channels like emails or text messages. Such gaps can lead to complications during audits, transactions, or legal disputes.

Double-check ownership percentages, board structures, and voting rights to ensure they’re accurate. If you’ve brought on new partners, shifted roles, or adjusted decision-making authority, update your documents to reflect these changes. For trusts, verify that distribution strategies align with the upcoming federal estate tax exemption change, which drops to $15 million in 2026.

Also, confirm that your entities comply with local and jurisdictional rules. If you have inactive entities, consider consolidating or dissolving them to simplify audits and reduce unnecessary tax filings. For LLCs in states like Wyoming, Nevada, or Delaware, ensure they limit creditor remedies to charging orders. Offshore trusts, such as those in the Cook Islands or Nevis, must also be properly documented.

Verify Compliance with Tax and Legal Requirements

Tax laws and compliance requirements are constantly evolving. For instance, the 2025 One Big Beautiful Bill Act (OBBBA) made permanent certain provisions from the 2017 Tax Cuts and Jobs Act. This includes raising the State and Local Tax (SALT) deduction cap to $40,000 for 2025–2029, although it phases out for incomes above $500,000. Review your pass-through entity elections to ensure they align with these changes.

Although FinCEN has temporarily paused enforcement of Beneficial Ownership Information (BOI) reporting for domestic companies in 2025, keep your records up-to-date in case the requirements shift. If you hold offshore assets, ensure compliance with the Foreign Account Tax Compliance Act (FATCA) to avoid penalties. Additionally, reporting for foreign trusts (Forms 3520 and 3520-A) remains a priority for the IRS, with penalties potentially reaching 35% of the transfer value.

Audit rates for high earners are climbing. Individuals earning over $10 million now face a 50% higher audit frequency, and complex structures like Family Limited Partnerships could see a tenfold increase in audits by 2026. The IRS is leveraging AI analytics to flag noncompliance, so maintaining strict corporate formalities is more critical than ever. Keep personal and business assets separate, maintain distinct accounts, document meeting minutes, and ensure all transfers serve legitimate business purposes – not just tax avoidance. Courts are increasingly focusing on whether legal formalities are genuinely followed, applying a "substance over form" standard.

"You don’t rise to the level of your income – you fall to the level of your legal structure." – Brian T. Bradley, Esq.

Conducting these legal and tax compliance checks annually ensures that no vulnerabilities are left unchecked.

Step 4: Review Insurance Policies and Risk Coverage

Once your legal structures are solid, it’s time to focus on insurance. Think of insurance as your first line of defense against lawsuits – it’s what stands between your assets and potential legal claims. In the U.S., lawsuits are incredibly common, with one being filed approximately every 30 seconds. For small business owners, there’s a one-in-three chance of facing a lawsuit, and the median cost of damages hovers around $201,000. Clearly, having the right coverage isn’t optional – it’s essential.

Check Policy Limits and Coverage Categories

Start by reviewing your primary insurance policies. These might include general liability, professional liability (E&O), cyber liability, Directors and Officers (D&O), Employment Practices Liability Insurance (EPLI), property, and auto insurance. If you rely on standard homeowner’s or auto policies, be aware that their limits may not be enough. This is where umbrella insurance comes in – it can add over $1 million in extra liability coverage.

Pay close attention to cyber liability insurance. Many standard business policies don’t cover data breaches, and with 61% of senior legal decision-makers identifying AI and data management as rising areas of legal risk, this type of coverage is increasingly important. If your business collects or stores customer data, dedicated cyber insurance is a must. Also, check that your D&O and EPLI policies reflect any recent changes, like new board members, ownership adjustments, or headcount increases.

Take a moment to review any “near miss” incidents your business experienced in the past year. These can reveal gaps in your current coverage. Additionally, compare the liability clauses in your vendor and customer contracts with your existing insurance policies. If there’s a mismatch, you could be exposed to unnecessary risks. Once you’ve identified any shortcomings, update your policies to address the latest threats.

Adjust Policies for New Assets and Changing Risks

After reviewing your policies, make adjustments to align with your business’s growth and evolution. Changes in size, revenue, or headcount could mean your current insurance limits, deductibles, or retentions no longer fit your needs. If you’ve introduced new products, expanded to new locations, or entered different markets, be sure to update your coverage to avoid any gaps.

"Individually, these feel like small, manageable gaps. Together, they can create outsized exposure – especially in a legal and regulatory environment that is more complex, more transparent, and more interconnected." – Adelman Firm

Double-check that every entity under your business – active, acquired, or even dormant – is listed on your master insurance policy. Make sure your internal team knows how to report incidents to your insurance carriers correctly. Proper reporting procedures not only strengthen your defense but also reduce the risk of having a claim denied. Finally, evaluate whether your premiums and deductibles are balanced with your company’s financial ability to handle potential risks as you look ahead to 2026.

Keep in mind, insurance and other asset protection measures need to be in place before a legal issue arises. Trying to adjust coverage after a claim is on the horizon could be considered a fraudulent transfer. In short, preparation is key.

Step 5: Create an Action Plan for Identified Problems

Once you’ve reviewed your legal structures and insurance policies, the next step is to tackle any gaps with a focused action plan. By addressing these issues systematically, you not only fix immediate vulnerabilities but also build a stronger foundation for protecting your assets.

Rank Issues by Risk Level and Financial Impact

Start by organizing the identified issues based on their risk level and potential financial consequences. For instance, internal risks – like tenant liability at a rental property – should be addressed quickly, as they can pose a direct and immediate threat. On the other hand, external risks, such as personal auto accidents, may affect your business assets differently and could require a separate approach.

From there, evaluate your protective measures in layers. Begin with basic safeguards, such as homestead exemptions and retirement accounts that are already shielded by law. Then, review your insurance coverage and entity structures, moving on to advanced tools like asset protection trusts if necessary. It’s worth noting that disputes between business partners are significantly more common than external lawsuits, occurring five to ten times more often. Outdated or incomplete partnership agreements can make these disputes even riskier. If your operating agreements lack essential provisions, like buy-sell clauses, updating them should be a priority.

Once you’ve ranked the issues, assign responsibilities and set clear deadlines to ensure progress.

Delegate Tasks and Establish Completion Dates

With priorities in place, delegate tasks to the right individuals. Use the 4X Rule to decide what to handle yourself versus what to delegate based on your effective hourly rate.

Establish realistic deadlines depending on the complexity of each task. Simpler tasks – like updating insurance policies or ensuring entity compliance – should be completed within 30 to 60 days. More intricate strategies, such as forming trusts or restructuring business entities, may take 6 to 12 months. Make sure your advisors – whether they’re accountants, attorneys, or insurance agents – work together seamlessly. If anyone on your team resists collaboration, it might be time to reconsider their role. To keep everything on track, appoint a "quarterback" to oversee the process and ensure nothing is overlooked.

"Asset protection must be undertaken before a claim arises. Transfers made after a lawsuit, judgment, or imminent claim may be set aside as fraudulent conveyances." – Carr Law Firm

Lastly, document every step of the process. Keep a record of who’s responsible for each task, the deadlines, and how each issue is resolved. This creates a clear audit trail and ensures accountability. Plan a follow-up review to confirm that any gaps have been fully addressed, rather than just checked off the list.

Step 6: Refine Your Audit Process for Next Year

After wrapping up this year’s audit, it’s time to look back and evaluate the process. The aim? To make next year’s review smoother, faster, and less stressful while ensuring nothing important gets overlooked.

Review What Worked and What Needs Adjustment

Take a close look at what went well and where there’s room for improvement. Start with your team of advisors. Were they communicating directly with each other, or were you stuck playing middleman? If communication felt clunky or inefficient, you might need better systems – or even a different team.

Next, think about delegation. If certain tasks cost less than 25% of your effective hourly rate, they’re prime candidates to hand off. For example, if your hourly rate is $400, any task that can be outsourced for under $100 per hour should be off your to-do list next year.

Now, evaluate your advisors’ roles. Were they proactive strategists, or did they only show up during tax season? If they weren’t offering forward-thinking advice throughout the year, that’s a red flag. A well-executed audit process should leave you feeling confident, not overwhelmed or drained.

Use these insights to fine-tune your checklist and streamline the process for next year’s audit.

Update Your Checklist for Future Audits

Revise your checklist to include triggers for immediate reviews. Big changes – like expanding into new states, acquiring significant assets, or hitting major personal milestones – should prompt an audit right away. It’s also worth noting that disputes with business partners are five to ten times more common than external lawsuits, so make sure your checklist includes a detailed review of operating agreements and buy-sell provisions.

For high-risk areas, consider shifting from annual audits to quarterly reviews. This way, your strategies stay aligned with fast-moving changes in your business or personal life. To make the process even easier, set up centralized document management and secure communication systems. This ensures all your advisors have access to consistent, up-to-date information.

"The gap between knowing and doing often determines the difference between entrepreneurs who build lasting wealth and those who simply generate impressive revenue." – Dew Wealth Management

Conclusion

Achieving business success doesn’t automatically safeguard your wealth. That’s where the six-step audit process from this checklist comes in. By following these steps – setting a review date, organizing asset records, reviewing legal structures, verifying insurance, addressing gaps with an action plan, and refining the process annually – you can shift from reacting to problems to actively protecting and building wealth. This method turns what might feel like an overwhelming task into a structured and manageable system.

The truth is, families often lose wealth over generations due to poor planning and weak governance, not bad investments. An annual audit ensures that your legal structures, insurance policies, and protection strategies keep pace with your business growth, family dynamics, and changing regulations. It also reinforces the importance of internal governance, keeping your operating agreements and partnership frameworks solid.

Think of this checklist as your financial tune-up. Just like you wouldn’t skip regular maintenance for your car, you can’t afford to neglect your yearly asset protection review. Over time, the process becomes more streamlined as you build stronger systems and delegate responsibilities more effectively. This habit is key to securing wealth that endures.

Make this review an annual priority, conduct immediate audits after significant changes, and ensure your advisors collaborate as a cohesive team. Entrepreneurs who take a systematic approach to asset protection lay the foundation for lasting financial security.

FAQs

What assets should I include in my annual inventory?

Including key assets such as your investment portfolio, digital assets, offshore accounts, legal structures (like trusts and LLCs), and insurance policies is crucial. Taking the time to review these annually ensures your asset protection strategies stay current and effective, adapting to any changes in your financial situation or legal environment.

How do I know if my LLC or trust will actually protect me in a lawsuit?

The success of an LLC or trust largely hinges on how well it’s structured and maintained. Irrevocable trusts tend to provide better protection because the assets are no longer considered the grantor’s property. On the other hand, revocable trusts usually don’t offer the same level of security. For LLCs, it’s essential to focus on proper formation, ongoing maintenance, and strict adherence to legal requirements. Regularly reviewing these arrangements and seeking guidance from an attorney can help ensure they meet your particular needs.

What insurance coverage gaps do entrepreneurs miss most often?

Entrepreneurs often miss critical gaps in their liability limits, umbrella policies, and life insurance. These gaps typically happen when policies aren’t reviewed or updated to reflect life changes or new risks. Conducting regular audits of your coverage can help ensure your policies match your current situation and offer the protection you need.