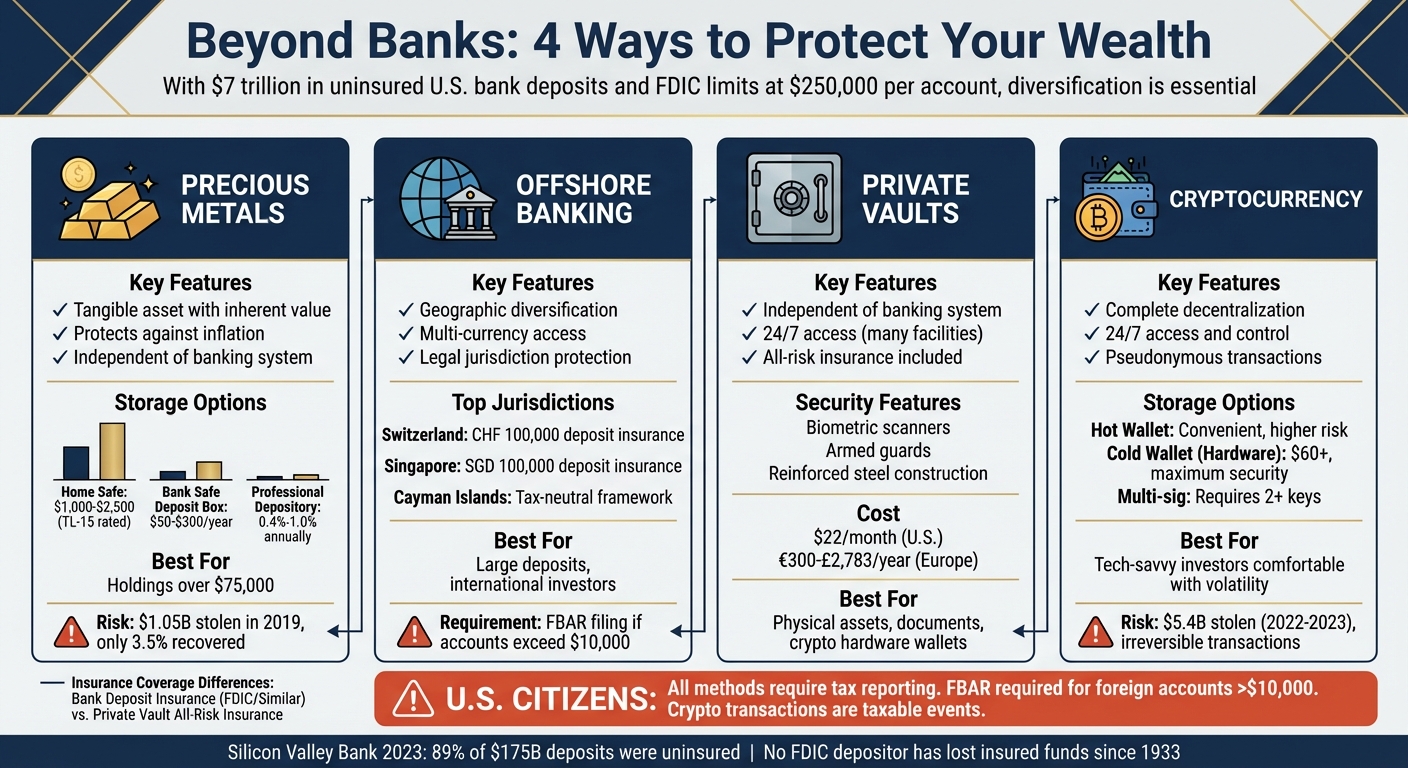

When banks fail, accessing your money can become a problem. The Federal Deposit Insurance Corporation (FDIC) only insures up to $250,000 per depositor, per bank, leaving any excess funds at risk. As of late 2024, $7 trillion of U.S. bank deposits were uninsured, highlighting the need for alternative ways to secure wealth. Recent collapses like Silicon Valley Bank in 2023 show how quickly a stable institution can crumble, especially in the digital age.

Here are some alternatives to safeguard your wealth:

- Precious Metals: Gold and silver are reliable stores of value but require secure storage.

- Offshore Banking: Accounts in stable countries like Switzerland or Singapore can protect against domestic risks.

- Private Vaults: Independent vaults provide high security and insurance, avoiding banking system vulnerabilities.

- Cryptocurrency: Digital assets offer control and decentralization but demand careful management of private keys.

Diversifying your assets across these options can reduce risks. However, each method has its own challenges, such as theft, legal compliance, and market volatility. Stay within FDIC-insured limits, plan ahead, and ensure you meet tax and reporting requirements to protect your wealth effectively.

Comparison of Wealth Storage Methods: Security, Access, and Insurance

Banking System Risks and FDIC Insurance Limits

Banks can fail for several reasons, including insolvency, liquidity crises, or asset devaluation. One of the most dramatic scenarios is a bank run, where depositors rush to withdraw their funds all at once, overwhelming the bank’s ability to pay. Even financially stable banks can collapse under this pressure. Modern technology has made this risk even greater. Take the 2023 Silicon Valley Bank collapse, for example: social media played a significant role in amplifying panic, leading to faster withdrawals and, ultimately, the bank’s downfall.

How FDIC Insurance Works

The FDIC insures up to $250,000 per depositor, per insured bank, per account ownership category. This means you can expand your coverage at a single institution by using different ownership types, like single accounts, joint accounts, IRAs, or trust accounts. Each ownership category is treated separately for insurance purposes.

FDIC insurance covers a range of deposit products, including checking accounts, savings accounts, money market deposit accounts, and certificates of deposit. However, it does not extend to investments like stocks, bonds, mutual funds, cryptocurrency, or the contents of safe deposit boxes.

The guarantees provided by the FDIC are backed by the Deposit Insurance Fund, which is funded by premiums paid by banks – not taxpayer dollars. Since its inception in 1933, no depositor with FDIC-insured funds has lost money. That said, the $250,000 cap is a hard limit. For example, if you have $1 million in a single account category at one bank, only $250,000 is protected. The remaining $750,000 is uninsured and at risk.

Because of these limits, relying solely on traditional bank deposits to safeguard large sums of money may not be enough.

Why You Need to Diversify Beyond Banks

When deposits exceed FDIC insurance limits, your funds become vulnerable during a financial crisis. The collapse of Silicon Valley Bank highlighted this issue: nearly 89% of its $175 billion in deposits were uninsured when it failed in March 2023. While regulators stepped in to protect all depositors in that instance, Treasury Secretary Janet Yellen emphasized that this was an extraordinary measure – not a guarantee for future bank failures.

Relying exclusively on banks also comes with operational risks. Even when regulators secure your deposits during a bank failure, you may still face disruptions like bounced checks or failed automatic payments. For businesses or individuals who need quick access to large sums for payroll, investments, or emergencies, the $250,000 insurance limit can fall short. Managing large deposits by spreading funds across multiple banks to stay within coverage limits adds complexity and administrative challenges.

Diversifying where and how you store your assets can help reduce these risks and ensure greater financial stability.

sbb-itb-39d39a6

Precious Metals for Wealth Protection

Gold and silver have been trusted for centuries as safeguards against economic uncertainty and inflation. Unlike money in a bank account, these metals are tangible assets with inherent value that remains steady even when financial institutions falter or currencies lose their purchasing power.

"Gold is a physical asset that can be lost, stolen, or damaged. Unlike stocks and bonds, which usually exist only in digital form, gold’s value is directly tied to its physical integrity. Without secure storage, investors risk losing a portion, or even all, of their investment."

- Ben Nadelstein, Head of Content, Monetary Metals

The main challenge with precious metals is ensuring their security. In 2019 alone, over $1.05 billion worth of jewelry and metals were stolen in the U.S., with a recovery rate of just 3.5%. Clearly, how and where you store your metals plays a critical role in protecting your investment.

Where to Store Precious Metals

When it comes to storing gold and silver, you have three main options: home safes, bank safe deposit boxes, and professional depositories. Each has its own advantages and drawbacks in terms of security, accessibility, and cost.

Home storage allows for round-the-clock access and complete privacy, but it carries the highest risk of theft. If you go this route, invest in a TL-15 burglary-rated safe and bolt it to a concrete slab for added security. These safes typically cost between $1,000 and $2,500. To protect your metals from moisture damage – especially silver, which tarnishes easily in humid environments – use desiccant packs.

"The first rule of storing precious metals at home: never talk about storing precious metals at home."

Bank safe deposit boxes offer strong physical security at an annual cost of $50 to $300. However, your access is limited to the bank’s operating hours, and in cases of bank failure or legal complications, you could temporarily or permanently lose access to your assets.

Professional depositories provide the highest level of security, with features like armed guards, biometric scanners, and 24/7 surveillance. Storage fees range from 0.4% to 1.0% of your asset’s value annually, and insurance is typically included. For example, the Texas Bullion Depository offers full insurance coverage underwritten by Lloyd’s of London. These facilities are ideal for holdings exceeding $75,000.

If you choose a professional depository, ensure your metals are stored as "allocated" rather than "unallocated." Allocated storage means specific bars or coins are held in your name, while unallocated storage pools your assets with others, increasing counterparty risk if the depository faces financial trouble.

"It’s absolutely critical if you are storing with a third party that you vet them carefully and only work with a trustworthy company that is fully allocated, insured, and third-party audited."

- Brett Elliott, Marketing Director, APMEX

| Feature | Home Safe | Bank Safe Deposit Box | Professional Depository |

|---|---|---|---|

| Access | Immediate (24/7) | Limited to branch hours | Business hours (often requires notice) |

| Theft Risk | High (assumed by owner) | Low (vault security) | Minimal (institutional security) |

| Insurance | Requires separate rider | Not provided by bank | Usually included in fee |

| Privacy | Maximum | Moderate | Requires KYC/AML paperwork |

| Best For | Small emergency reserves | Small to medium holdings | Large holdings ($75,000+) and IRAs |

Once you’ve chosen a storage method, evaluate the insurance options available to ensure your assets are fully safeguarded. Diversifying your storage locations can also help minimize risks and reduce dependence on any single institution.

Insurance and Access to Your Metals

Securing proper insurance is essential, no matter where you store your metals. Home storage and bank safe deposit boxes typically don’t include comprehensive insurance. Standard homeowners’ policies either exclude bullion entirely or cap coverage at very low amounts. To fully protect your investment, you may need to purchase a specialized insurance rider, which usually costs 0.5% to 2% of the insured value annually.

Professional depositories simplify this issue by including "all-risk" insurance in their fees. This type of coverage protects against theft, fire, natural disasters, and even mysterious disappearances. Always request written proof of insurance from the depository, and review details like policy limits, deductibles, and the definition of "physical loss".

For larger holdings, consider splitting your metals across multiple storage locations. Keep a small emergency reserve at home for immediate access, while storing the majority in a professional depository. This approach reduces the risk of losing everything in a single event while maintaining liquidity.

To safeguard your investment further, maintain detailed records of your holdings. This includes invoices, assay reports, and serial numbers for bars or coins. Such documentation can streamline insurance claims and make resale easier. For succession planning, prepare a packet for your heirs with vault details, bar lists, and contact information for the storage facility.

Offshore Banking for Geographic Diversification

Opening a bank account in a stable foreign country can act as a safeguard if the U.S. banking system faces significant challenges. By spreading your financial exposure across multiple legal and economic systems, you reduce the risk of being overly reliant on one nation’s financial health. For instance, if domestic banks collapse or the government enforces capital controls, your offshore funds remain accessible under the jurisdiction where they are held. This approach aligns with the broader goal of diversifying financial risks.

Offshore accounts also make it possible to hold multiple currencies – like Swiss Francs or Singapore Dollars – offering protection against a potential decline in the U.S. dollar. Additionally, these accounts provide access to international investment options, such as foreign government bonds or emerging market funds, which might not be available through U.S. financial institutions. Since assets in offshore accounts are governed by local laws, they are generally less vulnerable to claims from domestic creditors.

"Keeping your assets in an offshore account controlled by a foreign trust is the surest way to protect them."

- Blake Harris, Attorney

However, using offshore banking to avoid taxes is not an option. U.S. citizens are taxed on their global income, regardless of where the funds are located. Detailed reporting to the IRS and FinCEN is mandatory, and failure to comply can lead to severe penalties, including criminal charges. Before transferring assets, it’s crucial to consult with an asset protection attorney and a tax expert. Now, let’s examine how to choose the best jurisdictions for offshore accounts.

Selecting a Stable Banking Jurisdiction

Countries like Switzerland, Singapore, and the Cayman Islands are often regarded as top choices for offshore banking due to their political stability, strong regulatory systems, and legal protections. For example, in 2022, Switzerland had 15 banks featured on Forbes’ list of the world’s best banks, and Singapore was home to three of the 15 safest banks globally. Both countries also offer deposit insurance: Switzerland’s esisuisse covers up to CHF 100,000 per client per bank, while Singapore’s SDIC insures up to SGD 100,000 per depositor.

When evaluating a jurisdiction, factors such as political neutrality, regulatory strength, and deposit insurance are key. Switzerland’s neutrality and its Swiss Banking Act ensure a secure financial environment, while Singapore’s Monetary Authority enforces strict compliance standards. The Cayman Islands, on the other hand, operates under English Common Law and offers a tax-neutral framework, with no income, capital gains, or inheritance taxes.

Opening an offshore account often involves meeting specific requirements, such as minimum deposits and extensive documentation. Many banks require proof of the source of your wealth, which might include tax returns or audited financial statements, as part of their Know Your Customer (KYC) protocols.

A multi-jurisdictional approach can further enhance financial security. For example, you might use Singapore for daily banking needs, Switzerland for long-term investments, and the Cook Islands for asset protection structures. This strategy helps ensure that if one jurisdiction faces political or economic instability, your assets in other locations remain secure.

FATCA and CRS Reporting Requirements

U.S. citizens must file an FBAR (FinCEN Form 114) if the total value of their foreign financial accounts exceeds $10,000 at any point during the year. This form must be submitted electronically by April 15, with an automatic extension to October 15. Additionally, taxpayers need to attach Schedule B to their tax returns to disclose foreign accounts and their locations.

Under the Foreign Account Tax Compliance Act (FATCA), individuals must file IRS Form 8938 if their foreign financial assets surpass specific thresholds, which vary based on residency and filing status.

Non-compliance carries serious consequences, including hefty fines for non-willful violations and even imprisonment for willful violations. Moreover, foreign banks are required to report account details directly to the IRS under FATCA. The U.S. Treasury has agreements with 113 jurisdictions, including Switzerland, Singapore, and the Cayman Islands, to ensure proper sharing of account information.

To stay compliant, retain records of your foreign accounts for at least five years. These records should include account numbers, bank details, and the highest account values during the reporting period. For joint accounts, each account holder must report the entire account value on their individual FBAR filings. When converting foreign currency to U.S. dollars, use the Treasury Bureau of the Fiscal Service exchange rate as of December 31. Properly navigating these reporting requirements is a key part of maintaining legality while safeguarding your wealth across multiple jurisdictions.

Private Vaults and Secure Depositories

Adding private vaults to your wealth storage strategy is a smart way to protect physical assets like precious metals, important documents, or cryptocurrency hardware wallets. These vaults operate independently of banks, giving you greater control and security. They also use segregated storage, meaning your belongings are individually recorded and remain under your legal ownership – unlike pooled storage, which can blur ownership lines.

One of the biggest advantages of private vaults is their separation from the banking system. This makes them a safeguard against systemic risks like bank runs, bail-ins, or insolvencies. For context, banks in the U.S. operate at about 10X leverage, while in the EU, it’s closer to 20X. This kind of leverage introduces significant counterparty risk. By using private vaults, you reduce reliance on any single financial institution, much like offshore accounts or precious metals storage.

State-of-the-art private vaults often outdo banks in security. Think biometric scanners, reinforced steel walls, and round-the-clock armed guards. Plus, unlike bank safe deposit boxes – which aren’t covered by FDIC insurance – many private vaults offer all-risk insurance. For instance, the Texas Bullion Depository, the only state-run precious metals storage facility in the U.S., provides full insurance coverage for all stored items.

"Cash that’s not in a deposit account isn’t protected by FDIC insurance… A safe deposit box is not a deposit account. It is storage space provided by the bank, so the contents… are not insured by FDIC deposit insurance if damaged or stolen."

- Luke W. Reynolds, Chief of the FDIC’s Community Outreach Section

Benefits of Using Private Vaults

Private vaults offer several clear advantages over traditional bank storage. First, they shield you from the vulnerabilities tied to the banking system. Your valuables remain accessible even if banks face closures or operational disruptions.

Flexibility is another perk. While bank safe deposit boxes are only available during business hours, many private vaults allow 24/7 access. This means you can retrieve your belongings on weekends, holidays, or during emergencies.

Insurance is also a strong point. Many facilities include basic coverage – some up to CHF 25,000 – and others provide full replacement value insurance, often backed by top-tier insurers like Lloyd’s of London. Just make sure you’re listed as the loss-payee on the policy and confirm whether insurance is included in the rental fee or requires an additional rider.

Privacy is enhanced as well. Unlike banks, many private vaults don’t require a Social Security number or driver’s license to rent a space, offering a level of anonymity. However, standard tax reporting rules like FBAR and FATCA still apply.

"Modern banks, however, are not in the silver and gold storage business – they are in the credit and fee-generation business."

Choosing a Vault Location

Picking the right location for your vault is just as important as the vault itself. Stability matters. Countries like Switzerland, Singapore, and New Zealand are known for strong property rights, stable economies, and a history of respecting private ownership. Switzerland, for example, refines over 70% of the world’s gold bars and has a well-established private custody system. Singapore is another excellent choice, with its low crime rates, modern infrastructure, and favorable tax treatment for investment-grade bullion.

When choosing a vault, look for facilities that meet international standards (EN or UL) and offer features like reinforced walls, bulletproof construction, and biometric access. Proximity to major transportation hubs can also make asset relocation easier when needed.

Reputable vault providers often undergo regular third-party audits to confirm that client records match physical inventories. Some even allow you to inspect your holdings, adding an extra layer of transparency and confidence.

Costs can vary significantly. In the U.S., small storage boxes at Safe Haven Private Vaults start at about $22 per month with no long-term contracts. In Europe, fees range from €300 annually with providers like Sparta Safe in Austria to over £2,783 annually in the U.K. Some depositories charge fees based on asset value, typically between 0.4% and 1.0% per year. Weigh these costs against the benefits of enhanced security, insurance, and around-the-clock access.

Avoid unallocated or pooled storage options, which only give you a claim on a shared asset pool rather than direct ownership of specific items. For added protection, diversify your storage locations – such as splitting assets between Texas and Singapore – to reduce risks tied to regional policies or economic events. And always keep detailed records of your storage locations and access procedures to ensure smooth transfers, especially during probate.

Cryptocurrency for Digital Wealth Storage

Cryptocurrency has emerged as a modern alternative to traditional banking, offering a way to store wealth without relying on intermediaries. Unlike banks, which can freeze accounts or impose withdrawal limits during financial crises, digital assets stored in self-custody provide round-the-clock access and complete control.

One of the standout features of cryptocurrency is decentralization. When you hold your private keys, no institution can seize, freeze, or misuse your funds. Decentralized exchanges, powered by smart contracts, never take custody of your assets, eliminating counterparty risk. This structure empowers users to manage their digital wealth securely and independently.

However, while cryptocurrency offers unmatched control, it comes with challenges. The market is highly volatile – Bitcoin, for instance, saw a 75% drop in value during 2018. Transactions are irreversible, and there’s no insurance to fall back on. Between 2022 and 2023, an estimated $5.4 billion worth of cryptocurrencies were stolen. On top of that, losing access to your private keys can have devastating consequences. Programmer Stefan Thomas famously lost 7,002 Bitcoins (worth $203 million at the time) simply because he forgot his wallet password.

Privacy is another key benefit. While wallet addresses are visible on the blockchain, they don’t contain personal information like names or Social Security numbers. This offers a level of anonymity that traditional banks can’t match. However, U.S. citizens must still comply with tax reporting rules like FBAR and FATCA, regardless of how their crypto is stored.

"Not your keys, not your coins."

- Common Industry Proverb

Self-Custody vs. Institutional Custody

A major decision for crypto holders is how to manage their private keys. Self-custody puts you in full control of your digital assets. You’re entirely independent of third parties, but the responsibility for security is also yours. Lose your seed phrase – a 12-to-24-word recovery code – and there’s no way to recover your assets.

Institutional custody, on the other hand, involves entrusting your keys to an exchange or custodian. While convenient, this approach introduces counterparty risk. For instance, in May 2022, Coinbase disclosed that in the event of bankruptcy, customer assets might be treated as part of the bankruptcy estate, leaving users as unsecured creditors. The collapse of Mt. Gox serves as another cautionary tale – users who relied on the platform lost their funds, while those who moved assets to self-custody were unaffected.

| Feature | Self-Custody | Institutional Custody |

|---|---|---|

| Control | Full – you hold the keys | None – third party holds keys |

| Insurance | None | Varies by provider |

| Recovery | No recovery for lost seed phrases | Password resets available |

| Risk | User error, physical loss | Platform bankruptcy, hacks |

| Privacy | Pseudonymous on-chain | Full KYC required |

For many, a hybrid approach works best. Use a "hot" wallet (connected to the internet) for everyday transactions, and store the bulk of your holdings in a "cold" (offline) hardware wallet. As Johnny Gabriele, Head Analyst at The Lifted Initiative, advises:

"I always tell people to treat their hot wallet like they would their actual wallet – never store more than you’d be okay losing."

Securing Your Cryptocurrency

Once you’ve chosen your custody method, it’s essential to secure your assets. Cold storage is the gold standard for safety. Hardware wallets, which start at around $60, keep your private keys offline, making them immune to phishing, malware, and remote hacking attempts.

Your seed phrase is your ultimate backup. This 12-to-24-word code can regenerate your private keys if your wallet is lost or damaged. Avoid storing it digitally – don’t save it as a screenshot or in cloud storage. Instead, write it down on paper or engrave it on a stainless steel or titanium plate to protect against fire or water damage. Store this backup in a secure location, like a fireproof safe or bank deposit box, ideally separate from your hardware wallet.

For those with substantial holdings, multi-signature (multi-sig) wallets are worth considering. These require multiple private keys – such as 2 out of 3 – to approve transactions, reducing the risk of a single point of failure.

When buying a hardware wallet, always purchase directly from the manufacturer to avoid tampered devices. Enable hardware-based two-factor authentication (2FA) with a physical security key like a Yubikey, as SMS-based 2FA is vulnerable to SIM-swapping attacks. Some wallets even offer a "duress PIN" feature to display a decoy balance.

"Think of hot wallets like your checking account – easy to use but riskier. Cold wallets are your safety deposit box – harder to access but more secure."

- Fei Chen, Founder and CEO, Intellectia

The SEC also highlights the risks of custodial solutions:

"If the third-party custodian is hacked, shuts down, or goes bankrupt, you may lose access to your crypto assets."

- SEC Office of Investor Education and Assistance

Legal and Tax Compliance for Asset Protection

Diversifying how you store your assets doesn’t exempt U.S. citizens from reporting global income. If you’re a U.S. citizen or resident, you’re required to report all worldwide income, no matter where your assets are located or whether they’ve generated taxable income.

Tax Obligations for Different Storage Methods

Each method of protecting assets comes with its own reporting rules. For example, if you maintain foreign financial accounts – like offshore bank accounts, brokerage accounts, or mutual funds – you must file FinCEN Form 114 (FBAR) electronically by April 15 (with an automatic extension to October 15) if the total value of these accounts exceeds $10,000 at any point during the year.

Additionally, Form 8938 (required under FATCA) must be filed if the value of your specified foreign financial assets surpasses certain thresholds. For single filers residing in the U.S., this threshold typically starts at $50,000, though it varies depending on filing status and residency. This form, which is attached to your annual tax return, covers more than just bank accounts – it also includes foreign stocks, securities, and interests in foreign entities. However, tangible assets like gold bullion or real estate are generally not reportable on Form 8938, although foreign-issued gold certificates might be.

When it comes to cryptocurrency, every transaction you make is considered a taxable event. You’ll need to report gains or losses on Form 8949 and Schedule D, and you must also disclose crypto activity on Form 1040.

| Requirement | FBAR (FinCEN Form 114) | FATCA (Form 8938) |

|---|---|---|

| Threshold | Aggregate value > $10,000 anytime | Varies (e.g., > $50,000 for single U.S. residents) |

| Where to File | FinCEN’s BSA E-Filing System | Attached to Federal Income Tax Return |

| Due Date | April 15 (extension to Oct 15) | Same as income tax return |

| Assets Covered | Bank, brokerage, mutual fund accounts | Foreign accounts, foreign stock, securities, and interests in entities |

Knowing these requirements is essential before considering the penalties for non-compliance.

Maintaining Legal Compliance

Staying on the right side of the law isn’t just about filing forms – it’s also about avoiding hefty penalties. For FBAR violations, civil penalties for non-willful violations can go up to $10,000. Willful violations, however, can lead to penalties as high as $100,000 or 50% of the account balance, whichever is greater. On the criminal side, violations can result in fines and up to five years in prison. For Form 8938, failing to file could cost you $10,000, with an extra $10,000 tacked on for every 30 days of continued non-filing after receiving an IRS notice, up to a maximum of $60,000.

"U.S. taxpayers are not permitted to use offshore accounts, such as foreign bank and securities accounts as well as trusts, to avoid paying tax."

- Internal Revenue Service

Keep detailed records for all foreign accounts for at least five years from the FBAR due date. For digital assets, maintain records of every transaction, including purchase dates, times, cost basis, and fair market value at the time of each transaction, for at least three years. When reporting foreign currency values on FBAR, use the Treasury Bureau of the Fiscal Service exchange rate from the last day of the calendar year.

If you haven’t disclosed foreign assets, the IRS provides options like the Streamlined Filing Compliance Procedures or Delinquent FBAR submission procedures to help reduce penalties. To navigate these complexities, consulting a tax attorney or CPA is highly recommended. These steps are a vital part of any asset protection plan , similar to how high-net-worth individuals protect assets like the uber-rich and emphasize the importance of staying compliant with U.S. tax laws.

Conclusion

Diversification is a smart way to manage the risks and challenges tied to relying on a single bank. With FDIC insurance limits and potential threats like cyber-attacks or economic instability, spreading your assets across various options can provide added security.

Consider multiple strategies for safeguarding your wealth:

- Precious metals: Physical gold and silver are tangible assets that retain value outside the banking system.

- Offshore banking: Accounts in stable countries like Switzerland or Singapore can offer protection from domestic financial uncertainties.

- Private vaults: These provide enhanced security and insurance coverage that often surpass what bank safe deposit boxes offer.

- Self-custodied cryptocurrency: While this minimizes counterparty risk, it demands careful management of private keys and seed phrases.

As the Federal Deposit Insurance Corporation states:

"No depositor has ever lost a penny of insured deposits since the FDIC was created in 1933." – Federal Deposit Insurance Corporation

This underscores the importance of staying within insured limits while diversifying your assets. Regularly review your bank balances to avoid overexposure. A tiered approach can work well: keep a small emergency fund at home in a secure safe, store larger sums with fully insured professional depositories, and explore offshore banking as your assets grow.

It’s also critical to stay compliant with tax regulations associated with each method to avoid penalties. Take the time to assess and update your asset protection plan now – before any crisis hits. By doing so, you can strengthen your financial resilience and prepare for whatever the future may bring.

FAQs

How can I get more than $250,000 of FDIC coverage?

To protect deposits exceeding $250,000, you can take a few steps to extend FDIC coverage. One option is to open accounts at multiple FDIC-insured banks. Another approach is to use services that spread your deposits across several institutions. Additionally, structuring accounts under different ownership categories can help you stay within FDIC limits while safeguarding larger sums.

What’s the safest way to store gold and silver?

When it comes to storing gold and silver, the best option depends on your specific needs and the value of your holdings.

Professional vault storage is a top choice for high-value assets. These facilities often include insurance, detailed documentation, and regular audits, giving you peace of mind. Opting for fully allocated, segregated storage ensures your metals are clearly identified as yours, reducing potential risks.

For smaller amounts, private vaults or bank safe deposit boxes can provide a secure alternative. However, these options might come with certain restrictions or limited accessibility.

Home storage, while convenient, carries more risk. Without proper measures to protect against theft or natural disasters, this approach may not be ideal for everyone. If you choose to store metals at home, investing in a high-quality safe and security system is essential.

How do I hold crypto safely if an exchange fails?

To keep your cryptocurrency safe in case an exchange collapses, consider using self-custody options like cold wallets. These include hardware wallets, offline software wallets, or even paper wallets. By storing your private keys offline, you minimize the risk of hacking. Make it a habit to transfer your assets from exchanges to a secure storage option and ensure your seed phrases and private keys are stored offline in a safe place. Relying solely on exchanges for large amounts of crypto can leave your assets vulnerable, so taking control of your storage adds an extra layer of security.