The 2026 updates to the Common Reporting Standard (CRS), known as CRS 2.0, introduce major changes that impact financial privacy and tax reporting. Here’s what you need to know:

- Crypto and Digital Assets Now Reportable: Starting January 1, 2026, financial institutions must report on crypto-assets, e-money, and Central Bank Digital Currencies (CBDCs). Reporting begins in 2027.

- No More $250,000 Threshold: All accounts, regardless of balance, are now subject to CRS reporting.

- Increased Data Collection: Banks must report detailed information, including roles in trusts (e.g., trustee, settlor, beneficiary) and joint account details.

- Stricter Compliance Rules: Institutions must validate Tax Identification Numbers (TINs) and other data, with penalties for errors or missing forms.

- Privacy Concerns: Expanded data sharing raises risks of exposure, with governments collecting more personal financial details than ever.

These changes aim to close loopholes and improve transparency, but they significantly reduce financial privacy. To navigate this, ensure compliance, review your offshore asset protection structures, and consider privacy-focused jurisdictions like the U.S., which doesn’t participate in CRS.

Major CRS Changes in 2026

The 2026 updates bring the most sweeping changes to the Common Reporting Standard (CRS) since it was first introduced. These updates broaden the scope of reportable assets, tighten self-certification protocols, and introduce new technical requirements that impact both financial institutions and account holders. This is particularly relevant for digital nomads and location-independent entrepreneurs who manage accounts across multiple jurisdictions. These changes aim to address gaps in the existing framework, particularly in the treatment of digital assets alongside traditional accounts.

Crypto-Assets and Digital Currencies Now Included

For the first time, digital assets like crypto-asset derivatives are classified as "Financial Assets", while electronic money (e-money) and Central Bank Digital Currencies (CBDCs) are categorized as "Depository Accounts". If you use a centralized exchange or custodial provider for digital wallets, this information will now be shared with tax authorities, similar to traditional banking data.

Entities that invest in crypto-assets are now categorized as "Investment Entities", and those holding e-money or CBDCs for customers are labeled as "Depository Institutions". Reporting for these digital assets will begin in 2027.

"The myth ‘crypto is outside the system’ officially ends" – Azola Legal Services

These new classifications come with rigorous reporting standards, as outlined in the updated technical guidelines.

Updated Data Requirements and XML Schema

Financial institutions will now need to collect and report far more detailed information. This includes the number of joint account holders, whether an account is "new" or "pre-existing", the account type (Depository, Custodial, or Equity/Debt Interest), and the role of each reportable person, such as whether they are a beneficial owner, trustee, settlor, or senior managing official.

The updated XML schema (CRS 3.0) introduces stricter validation rules for Tax Identification Numbers (TINs) and address formats. Institutions can no longer rely solely on self-certifications if they suspect the information provided is inaccurate. If valid forms are missing, they must report this annually.

"The amended CRS rules mark a step change in how tax reporting obligations apply in practice… CRS compliance must be embedded into onboarding, customer data management, and ongoing monitoring" – Fiona Jelly, Founder & CEO of Complyfirst

Modified Reporting Thresholds for High-Value Accounts

Under the new rules, all accounts – regardless of balance – are subject to review, and tax authorities will now receive data for most clients, even those with relatively small balances. The inclusion of crypto-asset derivatives under Financial Assets means that holdings previously considered "low-value" could now trigger reporting requirements when aggregated. The focus has shifted to tax residency as the main criterion for reporting, rather than account balance. This shift highlights how the updated definitions prioritize residency over financial thresholds, further diminishing financial privacy.

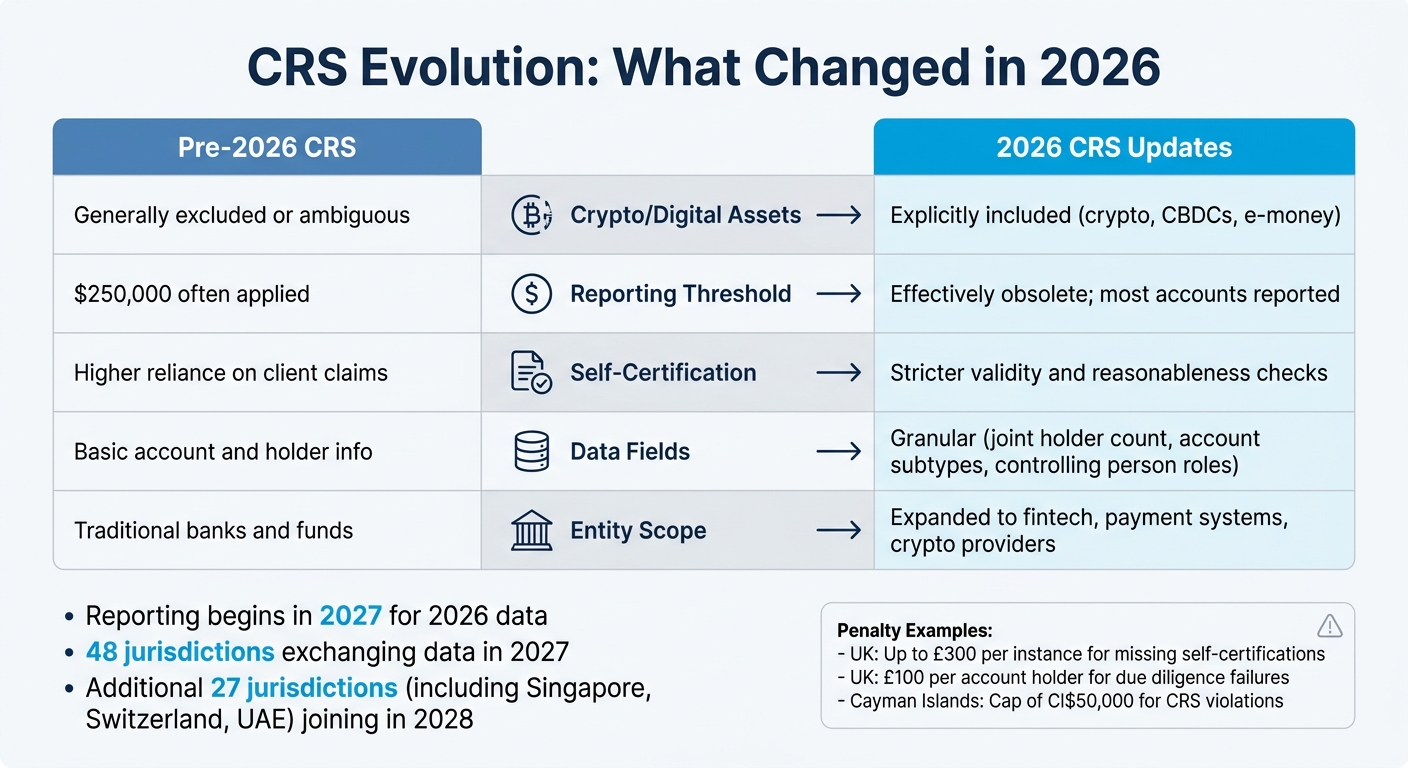

Here’s how the 2026 changes compare to the previous CRS framework:

| Feature | Pre-2026 CRS | 2026 CRS Updates |

|---|---|---|

| Crypto/Digital Assets | Generally excluded or ambiguous | Explicitly included (crypto, CBDCs, e-money) |

| Reporting Threshold | $250,000 often applied | Effectively obsolete; most accounts reported |

| Self-Certification | Higher reliance on client claims | Stricter validity and reasonableness checks |

| Data Fields | Basic account and holder info | Granular (joint holder count, account subtypes, controlling person roles) |

| Entity Scope | Traditional banks and funds | Expanded to fintech, payment systems, crypto providers |

In terms of penalties, the UK has introduced fines of up to £300 per instance for failing to obtain valid self-certifications and £100 per account holder for due diligence failures. Meanwhile, the Cayman Islands has capped penalties for CRS violations at CI$50,000.

These updates address long-standing gaps in CRS reporting and significantly alter the dynamics of financial privacy in offshore accounts.

sbb-itb-39d39a6

How CRS Changes Affect Financial Privacy

The 2026 updates to the Common Reporting Standard (CRS) bring major shifts to the way financial privacy is handled, particularly for those holding assets outside their home country. These changes expand reporting requirements beyond traditional bank accounts to include crypto-assets, electronic money, and even real estate ownership. As a result, governments are now collecting, storing, and exchanging a far greater volume of personal data than ever before – raising concerns that go beyond tax compliance.

Greater Risk of Data Exposure

With the updated CRS, the amount and type of data being shared increase the risk of exposure. Financial institutions are now required to collect more detailed information, which heightens the chances of accidental leaks or breaches. For trusts and foundations, the new rules require disclosure of fiduciary roles, effectively removing layers of anonymity by detailing who serves in these capacities.

The technical updates also pose challenges. Banks and crypto platforms are upgrading their systems to comply with the CRS 3.0 XML schema and stricter Tax Identification Number validation protocols. However, missteps during these transitions could lead to vulnerabilities, making breaches or unauthorized access more likely. To put this into perspective, 48 jurisdictions will start exchanging this expanded data in 2027, with another 27 – including Singapore, Switzerland, and the UAE – joining in 2028.

Adding to the complexity, the Crypto-Asset Reporting Framework (CARF) introduces transaction-level reporting for digital assets. Unlike traditional CRS reporting, which focused on year-end balances, CARF requires detailed records of every transaction. If you use centralized exchanges or custodial wallets, tax authorities will now receive a comprehensive view of your activity, not just a snapshot of balances. This level of reporting makes maintaining privacy within offshore structures increasingly difficult.

Privacy Challenges for Offshore Structures

The enhanced reporting requirements also make it harder to shield assets through offshore structures. The obligation to identify ultimate beneficial owners (UBOs) of trusts, funds, and shell companies means individuals can no longer rely on complex legal arrangements for anonymity. Financial institutions are taking a cautious approach, often requesting extensive Know Your Customer (KYC) details, such as the source of funds and tax residency documents.

Real estate is now under the microscope as well. The Immovable Property Information (IPI MCAA) framework allows countries to automatically share ownership data for apartments, houses, and land, including income generated from these properties. Even jurisdictions known for strong privacy protections, like Nevis and Belize, are adapting to these changes. While they may not have public ownership registers, they now report beneficial ownership details directly to governments. Essentially, offshore structures might still shield information from the public, but they no longer offer the same level of protection from government oversight.

"The allure of using offshore banking purely to hide assets has effectively disappeared." – OVZA Legal Affairs

How to Reduce Privacy Risks

To navigate these changes, it’s essential to move away from secrecy and toward a strategy of compliant transparency. Start by ensuring all foreign accounts and income are properly declared. Closing accounts won’t erase past data, as it remains accessible to tax authorities. Also, update your tax residency information with financial institutions, as this determines where your data is sent.

Review your financial structures to ensure they serve a legitimate business purpose. Tax authorities are now using advanced analytics and AI to cross-reference CRS data with domestic filings, making it easier to spot inconsistencies. Structures without genuine business substance are likely to attract more scrutiny.

When selecting jurisdictions, prioritize those with strong data protection laws rather than focusing solely on tax benefits. While all CRS-participating countries share financial information with tax authorities, some enforce stricter safeguards against unauthorized access. For instance, Swiss law imposes penalties, including prison time and fines, on bankers who violate privacy outside of mandatory reporting.

Proactively update self-certification forms, as financial institutions are now required to apply a "reasonableness test." Any missing or inaccurate forms can result in annual reporting to tax authorities. Keep detailed records of due diligence steps to prepare for possible regulatory reviews.

Lastly, explore privacy-focused tools and methods that align with compliance standards. While the United States does not participate in CRS, it offers certain structures that protect privacy from foreign governments while adhering to U.S. regulations. These options will be discussed in more detail in the following sections.

CRS Implementation Differences by Country in 2026

The way countries handle the Common Reporting Standard (CRS) isn’t uniform, and these differences can significantly influence privacy strategies. As of 2026, 116 jurisdictions are part of the CRS network, covering over 171 million accounts and managing approximately €13 trillion in assets. However, enforcement levels, reporting timelines, and reciprocity vary greatly. Understanding these distinctions is key to aligning your financial arrangements with both compliance and privacy goals.

Why the US Doesn’t Participate in CRS

The United States takes a different route from CRS, offering unique privacy advantages for non-U.S. persons. Instead of CRS, the U.S. uses the Foreign Account Tax Compliance Act (FATCA). FATCA is a unilateral system requiring foreign banks to report American account holders to the IRS, but it provides very limited data in return. This imbalance exists because the U.S. doesn’t have the legal framework to support full reciprocity. As a result, foreign governments share extensive data with Washington, while U.S. reporting remains minimal.

States like Delaware, Nevada, Wyoming, and South Dakota have become popular destinations for financial privacy. Non-U.S. residents can take advantage of U.S. domestic trusts and LLCs, which offer privacy benefits not found in other major economies.

"The U.S. banking system offers privacy features that virtually no other major economy provides [for non-U.S. persons]." – CitizenX

For non-U.S. citizens and residents, using U.S.-based structures means financial information isn’t automatically shared with their home country under CRS. However, they still need to comply with local tax reporting laws.

Other countries also adopt CRS policies that offer privacy-oriented benefits. Many of these locations also provide attractive tax and residency solutions for those looking to relocate.

Countries with More Flexible CRS Policies

Beyond the U.S., some jurisdictions tailor their CRS implementation to balance transparency with privacy.

- Paraguay: Paraguay uses Exchange of Information on Request (EOIR), meaning data is shared only if a foreign government makes a specific, justified request. This, combined with its territorial tax system that exempts foreign-source income, makes it appealing for those seeking privacy.

- El Salvador: El Salvador remains outside both CRS and the Crypto-Asset Reporting Framework (CARF). Under Decree 969/2024, Bitcoin capital gains are tax-free, and all foreign-source income is exempt from taxation. While Bitcoin adoption fell to 8.1% of the population by 2025, the country’s legal framework still attracts privacy-focused investors. Citizenship through the El Salvador Freedom Visa requires a $1,000,000 donation, payable in BTC or USDT.

- Philippines and Cambodia: These countries are classified as developing nations and haven’t committed to CRS as of January 2026. However, their status could change under international pressure, making them less reliable for long-term privacy strategies.

| Country | 2026 CRS Status | Key Privacy Feature |

|---|---|---|

| United States | Non-Participating | No reciprocal reporting for non-U.S. persons |

| Paraguay | EOIR Only | Data shared on specific request; territorial tax |

| El Salvador | Non-Participating | Zero Bitcoin capital gains; no CRS/CARF |

| Philippines | Non-Participating | CRS not implemented; large economy |

| Cambodia | Non-Participating | Dollarized banking; no imminent CRS commitment |

CRS-Compliant Jurisdictions: Variations in Privacy Protections

Many CRS-participating jurisdictions, such as the Cayman Islands, Hong Kong, Malta, and Mauritius, adopted CRS 2.0 on January 1, 2026, with the first data exchanges planned for 2027. Monaco took an early lead by reporting 2025 data in 2026, while Singapore delayed implementation until January 1, 2027, giving account holders extra time to adapt.

Even within CRS-compliant regions, privacy protections vary. For instance, Jersey complies fully with CRS and shares financial data with tax authorities. However, its "firewall" laws prevent foreign civil judgments from accessing local trust assets. This is particularly important for individuals more concerned with shielding assets from litigation or creditors than with tax-related issues.

"True privacy in 2026 is not about hiding from the government. It’s about protection from everyone else." – Ipanema Partners

Understanding these global differences is essential for structuring assets in a way that prioritizes privacy while remaining compliant with applicable laws.

Asset Protection Strategies That Comply with 2026 CRS

With increasing demands for transparency and stricter reporting rules, protecting your assets while staying within legal boundaries is more important than ever. The Common Reporting Standard (CRS) doesn’t have to mean giving up privacy or asset security. The key lies in understanding how different structures align with these regulations, allowing you to maintain compliance while safeguarding your financial interests.

Using Private US LLCs for Privacy

For non-U.S. individuals, setting up a private LLC in states like Delaware, Nevada, or Wyoming can offer a strong layer of privacy. Since the United States isn’t a participant in CRS, American banks aren’t required to report account details of non-U.S. residents to foreign tax authorities. This creates a privacy advantage compared to the 116 jurisdictions that automatically exchange financial information under CRS.

While the U.S. uses FATCA to gather data on its own taxpayers from foreign banks, it provides minimal reciprocal reporting on non-U.S. residents. This makes U.S.-based LLCs an attractive option for capital from Europe, Asia, and Latin America. However, to ensure compliance, your LLC should meet local tax reporting rules and qualify as an Active Non-Financial Entity (NFE). This approach aligns with privacy goals while adhering to CRS 2026 requirements.

Offshore Trusts and Foundations

Offshore trusts and private foundations remain effective tools for asset protection under CRS 2.0, provided they are structured properly. While CRS now mandates the reporting of trust roles, these structures excel at shielding assets from civil claims, such as those from litigants, ex-spouses, or creditors.

Some jurisdictions include "firewall" provisions, which prevent foreign civil judgments from being enforced against trust assets. To maximize the effectiveness of a trust, it should be established well in advance – ideally at least five years before any potential claims – and managed by independent, professional trustees with genuine discretionary authority. Avoid retaining direct control over the trust to prevent it from being labeled a "sham trust".

Global Wealth Protection‘s CRS Compliance Services

Navigating CRS 2026 compliance can be complex, but expert support simplifies the process. Global Wealth Protection (GWP) offers personalized consultations to help structure your assets in ways that meet CRS requirements while protecting your privacy.

Their services include forming U.S.-based private LLCs with complete documentation and registered agent support, establishing offshore trusts and private interest foundations (with a focus on Anguilla), and offering strategic advice through their GWP Insiders membership program. They also assist with securing Active NFE status, Tax Residency Certificates, and ensuring economic substance compliance. The aim isn’t to conceal assets but to organize them within the legal framework, safeguarding them from civil threats while preserving as much privacy as legally possible.

2026 CRS Compliance Checklist

With the expanded CRS 2.0 reporting scope, it’s essential to take steps to protect your privacy while staying compliant. The updated rules now include crypto-assets, e-money, and digital currencies, meaning outdated structures could expose you to unnecessary risks. Here’s how to prepare.

Review and Update Your Current Structures

Start by comparing your existing asset structures against the new CRS XML Schema v4.0 requirements. Financial institutions are now required to collect additional data points, such as whether accounts are "pre-existing" or "new", joint account indicators, and specific roles within trusts and foundations. If you hold assets through an offshore company, make sure to classify it as either Active or Passive. Passive NFEs (Non-Financial Entities) trigger look-through reporting of all Ultimate Beneficial Owners, while Active NFEs typically report only the entity’s residency, offering better privacy protection.

Update your self-certification forms to include the new mandatory fields, such as time spent abroad, to meet enhanced reasonableness tests set by banks. If you’ve recently relocated or changed your tax residency, obtaining a Tax Residency Certificate (TRC) from your current jurisdiction ensures your data is reported accurately.

Once your structures are updated, focus on implementing tools to minimize reporting errors.

Use Privacy-Focused Tools and Methods

Consider using compliance platforms that verify self-certifications and reduce data inaccuracies before submission to tax authorities. For crypto holdings, decentralized self-custody wallets remain outside the automatic reporting system, unlike centralized exchanges that fall under the new Crypto-Asset Reporting Framework. When setting up new structures, target jurisdictions with statutory "firewall" provisions – such as Jersey – that report to governments but block private litigants or foreign courts from accessing trust assets.

For non-U.S. individuals, private U.S. LLCs can provide privacy advantages due to limited reciprocal reporting obligations. Additionally, e-money accounts with balances under $10,000 (calculated on a rolling 90-day basis) may be excluded from reporting requirements.

Get Professional Advice

After updating your structures and integrating privacy tools, professional guidance becomes essential to navigate the complexities of CRS 2.0. The revised XML schemas and new classifications can be challenging, and implementation timelines differ by jurisdiction. For instance, Singapore won’t adopt the updated CRS until 2027, while most other countries began in 2026. Non-compliance penalties can be steep – financial institutions in Georgia face daily fines of up to 3,000 GEL, and the Cayman Islands imposes penalties ranging from CI$10,000 to CI$100,000 for economic substance violations.

Global Wealth Protection offers tailored consultations to help align your assets with CRS requirements while safeguarding your privacy. Their services include assessing gaps in your current structures, advising on Active NFE status and TRC acquisition, and providing strategic advice through the GWP Insiders membership program. The aim is to ensure your data flows to the correct jurisdictions while protecting your wealth from civil risks like litigation or creditor claims – all within the legal framework.

Conclusion

The 2026 CRS updates mark a major turning point in global financial transparency, introducing broader reporting obligations than ever before. By bringing crypto-assets, e-money, and CBDCs into the fold, alongside stricter oversight of all account types, the framework significantly expands the reach of automatic information exchange.

For asset owners, particularly those with offshore structures or digital holdings, these changes demand a fresh approach to privacy and compliance. The updated XML Schema v4.0 requires institutions to gather and share more granular data with tax authorities, starting in 2027 for the 2026 reporting period. This raises the stakes for safeguarding sensitive information across jurisdictions and mitigating potential data breach risks.

"True privacy in 2026 is not about hiding from the government. It’s about protection from everyone else." – Ipanema Partners

This guide has provided an overview of the shifting regulatory environment and actionable steps to adapt. As transparency requirements grow stricter, aligning your strategies with the new CRS framework is critical. Adjustments like restructuring assets, securing Tax Residency Certificates, and ensuring your entities meet Active NFE criteria can help minimize exposure while staying compliant.

Navigating these complex, multi-jurisdictional requirements calls for expert guidance. Global Wealth Protection offers customized consultations to help you align with CRS 2.0 while protecting your privacy and assets. The objective is clear: ensure your data reaches the appropriate authorities while shielding your wealth from risks like litigation or creditor claims.

FAQs

Will my self-custody crypto be reported under CRS 2.0?

Self-custody crypto assets generally aren’t reported under CRS 2.0 unless they’re tied to financial accounts or managed through services included in the expanded reporting scope. From 2026, this will cover crypto service providers and digital asset accounts as part of the CRS framework. It’s important to evaluate how these updates might affect your particular circumstances.

What happens if my TIN or self-certification is wrong or missing?

If your TIN or self-certification is incomplete or incorrect, you could face penalties for non-compliance, heightened regulatory scrutiny, and potential reporting challenges under CRS regulations. These risks are likely to increase as enforcement measures become stricter in 2026. Providing accurate and complete information is crucial to sidestep these issues.

How do I prove my tax residency so my CRS data goes to the right country?

To make sure your CRS data is sent to the right country, you’ll need to provide official documentation that confirms your tax residency. Typically accepted documents include a tax residency certificate, a certificate of residence, or other official proof issued by your tax authority. Submit these documents to your financial institution, which will handle the verification process and report your residency in line with CRS regulations. It’s important to ensure that the documents you provide are both accurate and current to avoid any issues with proper allocation.