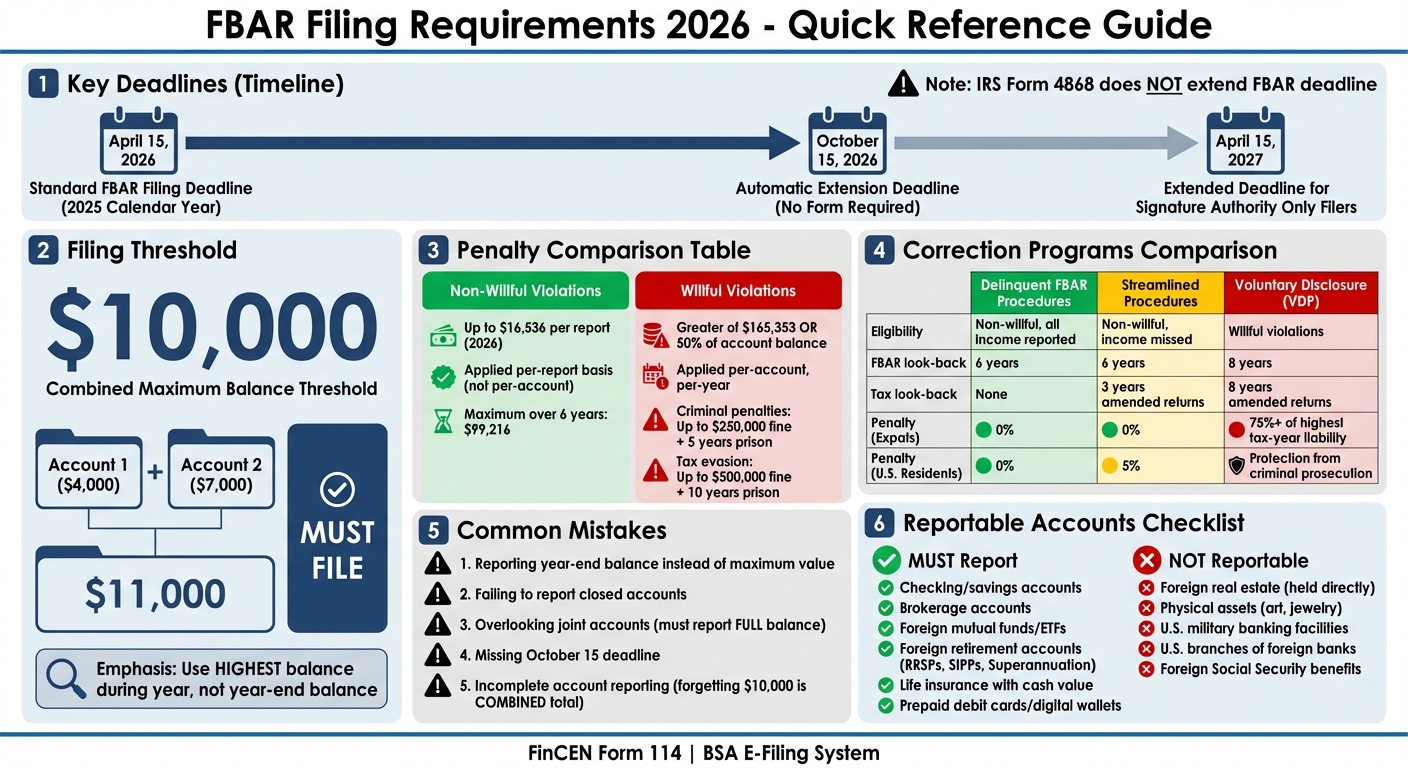

If you’re a U.S. citizen or resident with foreign financial accounts totaling over $10,000 at any point in 2025, you must file an FBAR (FinCEN Form 114) by April 15, 2026. Missing this deadline? You get an automatic extension until October 15, 2026 – no extra forms needed. Penalties for non-compliance are steep: up to $16,536 per violation for non-willful errors and $165,353 or 50% of the account balance for willful violations.

Common mistakes include reporting year-end balances instead of the highest balance, failing to report closed accounts, and missing the October deadline. Fixing errors is possible through IRS programs like Streamlined Filing or Delinquent FBAR Submission Procedures, but act fast to avoid penalties.

To stay compliant:

- Report all qualifying accounts (e.g., savings, brokerage, foreign retirement accounts).

- Use the highest balance during the year, not the year-end balance.

- File electronically via the BSA E-Filing System and keep records for at least five years.

Late filings? Don’t quietly submit them – use official IRS programs to avoid harsher consequences.

FBAR Basics and Filing Requirements

What FBAR Is and Why It Exists

The Report of Foreign Bank and Financial Accounts (FBAR), officially known as FinCEN Form 114, is an annual report mandated by the Bank Secrecy Act. Unlike your federal tax return, this form is submitted electronically to FinCEN. Its main goal? To help the U.S. government uncover individuals who might be using foreign accounts for illegal activities like tax evasion or money laundering. Even inactive accounts must be reported if their combined value crosses the set threshold. Understanding who needs to file is the next step.

Who Must File FBAR

The FBAR filing requirement applies to "U.S. persons", which includes U.S. citizens (even if they live abroad or hold dual citizenship), resident aliens (green card holders or those meeting the substantial presence test), and domestic entities like corporations, partnerships, LLCs, trusts, and estates. If you have a financial interest in or authority over foreign accounts and the combined maximum balance exceeds $10,000 at any point during the year, you must file.

For instance, if you hold three accounts with balances of $4,000 each, the total of $12,000 exceeds the threshold, triggering the filing requirement. Filing ensures compliance and shields you from potential penalties.

"Each United States person who has a financial interest in, or signature authority over, any financial accounts… must report that relationship… if the aggregate value of these financial accounts exceeds $10,000 at any time during the calendar year." – FinCEN

Reportable Account Types

If the combined value of your foreign accounts exceeds $10,000, you’ll need to report every qualifying account, no matter its balance or activity level. The types of accounts you must report include:

- Checking, savings, and time deposits (like certificates of deposit)

- Brokerage accounts holding stocks, bonds, or derivatives

- Foreign mutual funds and ETFs

- Foreign retirement accounts (e.g., Canadian RRSPs, UK SIPPs, Australian Superannuation)

- Life insurance policies and annuities with a cash surrender value

- Prepaid debit cards and digital wallets (e.g., Revolut, Wise)

However, not all assets fall under FBAR reporting. You won’t need to report:

- Foreign real estate held directly (not through a foreign entity)

- Physical assets like art, jewelry, or collectibles

- Accounts at U.S. military banking facilities

- U.S. branches of foreign banks (e.g., HSBC in New York)

- Social Security benefits from foreign governments

When calculating the total value of your accounts, use the highest balance reached during the year – not the year-end balance. Be sure to convert foreign currencies using the Treasury’s official exchange rate as of December 31. Keep records of your foreign accounts for at least five years to ensure accurate filing and avoid mistakes. Proper documentation is your best defense against filing errors.

sbb-itb-39d39a6

2026 FBAR Filing Deadlines

The FBAR for the 2025 calendar year is due on April 15, 2026. While this date coincides with the federal income tax filing deadline, it’s important to remember that FBAR submissions are handled differently. Instead of the IRS, you’ll submit FinCEN Form 114 electronically through the BSA E-Filing System to the Financial Crimes Enforcement Network (FinCEN).

If you miss the April 15 deadline, don’t panic. There’s an automatic six-month extension that gives you until October 15, 2026, to file. This extension is granted by law (31 CFR 1010.306(c)) and doesn’t require any additional forms or requests. As long as you file by October 15, your submission will be considered on time, with no penalties or adverse consequences.

"The October 15 extension is automatic – you don’t need to file any form or request it. If you miss April 15, you still have until October 15 with no penalty." – Chip Moreno, Expat Tax Expert

Here’s an important clarification: IRS Form 4868 only extends your tax return deadline – it does NOT apply to FBAR filings. The FBAR extension is automatic, while tax extensions require you to file a formal request. Keep in mind that these are entirely separate obligations submitted to different agencies.

There’s one exception worth noting. For individuals who have signature authority only (and no financial interest) over foreign accounts, the deadline for the 2025 reporting year is extended further to April 15, 2027. After filing electronically, ensure you save your BSA ID confirmation number (formatted as 31X-XXXXXXXXX) as proof that your submission was timely.

Understanding these deadlines is essential to avoid the severe penalties covered in the next sections.

FBAR Penalties for Non-Compliance

Missing FBAR filing deadlines or submitting incorrect reports can result in steep penalties. The IRS takes non-compliance seriously, with penalties varying based on whether the violation is deemed non-willful (an honest mistake) or willful (intentional or recklessly negligent). Knowing the difference is crucial, as it significantly impacts the penalties you might face.

Penalties for Non-Willful Violations

If you unintentionally fail to file or make an error on your FBAR, the IRS can impose a civil penalty of up to $16,536 per report for 2026 (adjusted annually for inflation). This penalty applies per annual report, not per account. A landmark case, Bittner v. United States, highlighted this distinction. Alexandru Bittner failed to report 272 foreign accounts over five years, leading the IRS to initially assess a $2.72 million penalty (about $10,000 per account). However, the Supreme Court reduced it to $50,000, applying the penalty on a per-report basis.

"The Bank Secrecy Act’s $10,000 maximum penalty for the nonwillful failure to file a compliant report accrues on a per-report, not per-account, basis."

– U.S. Supreme Court, Bittner v. United States

Non-willful penalties can accumulate over a six-year period, potentially reaching $99,216 for 2026.

These penalties are far less severe than those for willful violations, which are addressed below.

Penalties for Willful Violations

Willful violations carry much harsher consequences, as penalties are assessed on a per-account, per-year basis. For 2026, the civil penalty for a willful violation is the greater of $165,353 or 50% of the account’s highest balance during the year. For instance, if you had a foreign account with a peak balance of $500,000 and failed to report it willfully, the penalty could be $250,000 for that year. In United States v. Zwerner, a Florida court upheld penalties amounting to 133% of an account’s value due to multi-year violations.

The IRS doesn’t require explicit intent to defraud to establish willfulness. Reckless disregard or deliberate ignorance of FBAR requirements can be enough. For example, checking "No" on Form 1040 Schedule B while holding foreign accounts has been treated as evidence of willfulness, as seen in United States v. Williams.

"Willful blindness – deliberately avoiding learning about FBAR requirements when you should have known to ask – can be treated as willful conduct."

– SDOCPA

Beyond civil penalties, willful violations can lead to criminal charges, including fines up to $250,000 and up to five years in prison. Related offenses, like tax evasion or money laundering, can result in fines of up to $500,000 and imprisonment for up to 10 years.

Understanding these distinctions is essential when exploring corrective measures.

When Penalties May Be Waived

In some cases, the IRS may waive penalties if you can prove that circumstances beyond your control caused the failure to comply. Common examples include:

- Relying on professional advice: If you provided accurate information to a tax preparer who failed to file the FBAR.

- Limited financial knowledge: For instance, inheriting a foreign account without knowing about reporting requirements.

- Immediate correction: Taking prompt action to file once you discover the error.

To qualify for a waiver, you must demonstrate that you exercised ordinary business care and prudence. This includes keeping detailed records of your communications with advisors and documenting your compliance efforts.

The IRS also offers programs to help reduce or eliminate penalties. The Delinquent FBAR Submission Procedures often result in no penalties if you reported all income on your tax returns but neglected to file the FBAR. For non-willful taxpayers with unreported income, the Streamlined Filing Compliance Procedures provide relief, offering a 0% penalty for U.S. taxpayers living abroad and a 5% penalty for U.S. residents. For example, in January 2026, a taxpayer who inherited a $150,000 Swiss account and was unaware of FBAR requirements used the Delinquent FBAR Submission Procedures and faced no penalties.

For willful violations, the IRS Voluntary Disclosure Practice may offer protection from criminal prosecution, although penalties under this program tend to be higher.

5 Common FBAR Filing Mistakes

Filing an FBAR (Foreign Bank Account Report) can be tricky, and even small mistakes can lead to steep penalties. Knowing the common errors taxpayers make can help you stay compliant and avoid unnecessary trouble.

Reporting Year-End Balance Instead of Maximum Value

One common misstep is reporting the year-end balance instead of the highest balance during the year. The FBAR requires you to report the maximum value your account reached at any point during the year. For example, if your foreign account peaked at $75,000 in March but dropped to $35,000 by December 31, you’re required to report $75,000. Understating this amount – even unintentionally – can result in penalties.

Failing to Report Closed Accounts

Even accounts that were closed during the year must be reported if they contributed to the $10,000 threshold. Keeping account statements for at least five years is a good practice to ensure you don’t overlook any reportable accounts.

"That UK savings account from your previous job? If it still had funds during the year and your total exceeded $10,000, it’s reportable".

Overlooking Joint Accounts with Foreign Nationals

If you share a joint account with a foreign spouse, relative, or business partner, you must report the entire account balance, not just your share. This rule applies even if the other account holder isn’t a U.S. person. Each individual with ownership or signature authority is required to file separately, which is a detail many taxpayers overlook.

Missing the October 15 Deadline

Timing is another area where mistakes happen. While the initial deadline is April 15, it automatically extends to October 15 without needing extra paperwork. However, if you miss the October 15 deadline, penalties kick in immediately. It’s worth noting that filing a federal tax extension (Form 4868) does not extend your FBAR deadline. Filing early, by April, gives you time to fix any errors – like incorrect account details or currency conversion mistakes – before the final cutoff.

Incomplete Account Reporting

Many people mistakenly think they only need to report accounts with individual balances over $10,000. In reality, the $10,000 threshold applies to the combined total of all foreign accounts. Even if one account only holds $4,000 and another holds $7,000, you’re required to file an FBAR. Every account must be reported once the combined value exceeds $10,000, even if some accounts have very small balances.

"Even if the balance hits $10,000 for just one day (or one minute)!… if you think that keeping $4,000 in one account and $7,000 in another will enable you to avoid filing, this isn’t the case".

Failing to report even one account can result in penalties of up to $16,536 for non-willful violations in 2026.

Options for Correcting FBAR Errors and Missed Filings

If you’ve discovered mistakes in your FBAR filings – or missed filing them altogether – the IRS provides several ways to fix these issues. The best choice depends on whether the error was non-willful (an honest mistake) or willful (deliberate concealment). It’s important to act quickly and use an official IRS program. Avoid attempting a "quiet disclosure" (filing late reports without following proper procedures), as this can lead to audits and harsher penalties.

Delinquent FBAR Filing Procedures

This option is for taxpayers who missed filing FBARs but accurately reported all foreign income on their tax returns. If unreported income isn’t an issue, this is the most straightforward solution. You’ll need to file up to six years of late FBARs electronically through the BSA E-Filing System and include a statement explaining the missed deadlines. The statement should show that the error was non-willful, such as being unaware of the requirement or relying on a tax preparer who failed to inform you.

"If your tax returns are compliant and your only issue is delinquent FBAR filing, resolving delinquent FBARs through proper submission procedures is typically the safest approach." – Kasia Strzelczyk, EA, 1040 Abroad

For non-willful violations, this process generally avoids penalties, although the IRS may still impose them during an examination. To qualify, you cannot be under an active civil examination or criminal investigation by the IRS.

If unreported income is involved, the Streamlined Filing Procedures might be more appropriate.

Streamlined Filing Procedures

For situations where both foreign accounts and their income were unreported, the Streamlined Filing Compliance Procedures are the way to go. This program requires filing three years of amended tax returns and six years of delinquent FBARs.

- U.S. taxpayers living abroad who meet the physical presence test (spending at least 330 days outside the U.S. in one of the last three years) face 0% penalties.

- U.S. residents using the Streamlined Domestic Offshore Procedures are subject to a 5% penalty on the highest aggregate balance during the six-year period.

| Feature | Delinquent FBAR Procedures | Streamlined Procedures | Voluntary Disclosure (VDP) |

|---|---|---|---|

| Primary Eligibility | Non-willful; all income reported | Non-willful; income missed | Willful violations |

| FBAR Look-back | 6 years | 6 years | 8 years |

| Tax Look-back | None (already current) | 3 years of amended returns | 8 years of amended returns |

| Penalty (Expats) | 0% | 0% | Significant civil penalties |

| Penalty (U.S. Residents) | 0% | 5% offshore penalty | Significant civil penalties |

Voluntary Disclosure for Willful Violations

If your non-compliance was willful – or you’re unsure whether it was – you should consider the IRS Voluntary Disclosure Practice (VDP). This program requires preclearance from the IRS Criminal Investigation division and offers protection from criminal prosecution in exchange for full disclosure.

Participants must:

- File eight years of amended tax returns and delinquent FBARs.

- Pay all back taxes, interest, and typically face civil penalties of 75% or more of the highest tax-year liability.

Willful violations carry serious risks, including criminal investigation, fines of up to $500,000, and up to 10 years in prison. It’s crucial to consult a Board-Certified Tax Law Specialist or offshore tax attorney before moving forward. The VDP is only available if the IRS hasn’t already started a civil examination or criminal investigation.

How to File FBAR Accurately

Follow these steps to ensure your FBAR filing is correct and avoid penalties.

Keep Detailed Records of Foreign Accounts

It’s crucial to maintain thorough records of your foreign accounts for at least five years. These records should include the account name, number, type, financial institution details, and the account’s highest value during the year. Since the IRS can impose civil FBAR penalties for up to six years, keeping records beyond the minimum period can offer extra protection.

To determine the peak value of each account, track monthly balances and convert them to U.S. dollars using the Treasury’s official December 31 exchange rate. If that exchange rate isn’t available for a specific currency, use another reliable rate and document its source. If you’re using quarterly statements, ensure they accurately reflect the highest balances for each month.

Keep permanent copies of all filed FBARs and supporting bank statements. For joint accounts held solely with your spouse, you can file a single consolidated FBAR by completing Form 114a (Record of Authorization to Electronically File FBARs) and keeping it in your records – this form does not need to be submitted with the FBAR. However, if you have separate accounts, each individual must file their own FBAR.

These records are especially important when managing more complex account setups.

Manage Complex Account Structures

When dealing with multiple or joint accounts, accurate record-keeping becomes even more critical. Combine all accounts to determine if their total value surpasses the $10,000 filing threshold, and always report joint accounts in full, regardless of your personal ownership share.

If you have signature authority over an account – such as one belonging to your employer or an elderly relative – you are required to report it, even if you have no financial interest in the funds. Be sure to document your signature authority carefully. Additionally, accounts closed during the year must still be reported if they met the threshold at any point while open.

Work with Tax and Financial Advisors

After organizing your account details, consulting with tax professionals can simplify the filing process. Seek out advisors experienced in international compliance to help distinguish between FBAR and FATCA requirements. They can also identify less obvious reportable items, such as foreign life insurance policies with cash value or overseas pension plans.

When hiring an advisor for offshore disclosures, look for Board-Certified Tax Law Specialists who specialize in international tax amnesty reporting. Any paid preparers, including CPAs, attorneys, or enrolled agents, must be registered with the BSA E-Filing System to file your FBAR electronically. If you authorize someone else to prepare your FBAR, complete and retain Form 114a to grant them filing authority.

Professionals can also align your FBAR filings with your federal tax returns, ensuring all foreign income is reported consistently. They typically use the Treasury Bureau of the Fiscal Service’s December 31 exchange rates to avoid valuation mistakes. If you’ve missed filing in prior years, advisors can guide you through Streamlined Filing Compliance Procedures or Delinquent FBAR Submission Procedures to minimize penalties – as long as you act before the IRS initiates an audit. However, they strongly advise against "quiet disclosure", which involves filing overdue FBARs without using an official amnesty program. This approach risks audits and hefty penalties.

2026 FBAR Compliance Summary

Stay on top of your FBAR requirements by keeping track of deadlines, understanding potential penalties, and ensuring accurate filings.

For the 2025 calendar year, your FBAR is due on April 15, 2026, but there’s an automatic extension to October 15, 2026. If you’re a filer with only signature authority, you have until April 15, 2027 to file. Missing these deadlines can lead to steep penalties: $16,536 for non-willful violations or, for willful violations, the greater of $165,353 or 50% of your account balance.

Start gathering your records as early as January 2026. You’ll need details like account numbers, bank addresses, and the highest balance each account reached during 2025 – not just the year-end balance. Currency conversions must use the official December 31, 2025 Treasury exchange rate. File your FBAR electronically via the BSA E-Filing System and keep your confirmation number on file for at least six years.

If you’ve fallen behind on past filings, address the issue promptly – before the IRS contacts you. Programs like the Streamlined Filing Compliance Procedures and Delinquent FBAR Submission Procedures can help you catch up and possibly avoid penalties. However, once an audit begins, these options are typically no longer available.

FAQs

Do I have to file an FBAR if my foreign accounts only went over $10,000 briefly?

Yes, you need to file an FBAR (FinCEN Form 114) if the combined value of all your foreign accounts exceeded $10,000 at any point during the year, even if it was just for a short time. This requirement is based on the aggregate balance of all your foreign accounts, not individual accounts.

How do I find the highest balance for FBAR if I only have monthly statements?

To figure out the highest balance of your foreign accounts when you only have monthly statements, go through each statement for the year and identify the largest amount listed. The maximum value at any point during the year – not just the year-end balance – must be reported as the maximum account value on your FBAR (FinCEN Form 114). This approach ensures your reporting aligns with FBAR rules.

What should I do if I forgot to file an FBAR for prior years?

If you didn’t file an FBAR in previous years, the IRS offers delinquent FBAR filing procedures. These let you submit up to six years of late FBARs without penalties, as long as the failure to file was non-willful. Start by identifying the years you missed, gather all necessary account details, and submit the filings as soon as possible. It’s a good idea to work with a tax professional who specializes in FBAR compliance to ensure everything is accurate and to handle any potential concerns with the IRS.