May 2, 2016

By: Bobby Casey, Managing Director GWP

Well, 2016 has not been kind to the music industry thus far. David Bowie, Merle Haggard, and now Prince. That’s tough!

Well, 2016 has not been kind to the music industry thus far. David Bowie, Merle Haggard, and now Prince. That’s tough!

There isn’t much on Haggard’s estate one way or another, but Bowie looked to have had very specific instructions in his will, and put trusts to use for his daughter Alexandria. Meanwhile, Prince didn’t even have a will!

You don’t need to be a financial wizard to understand the sense behind having a basic will. Even having a will has its complications with probate, but still. Some understanding that you would like your estate to be given to certain parties is just good sense!

What’s the big deal? Well, in Prince’s case, about half his multimillion dollar estate is at stake. I’d say that’s kind of a big deal. Right now, it is very likely that half of Prince’s estate will be going to the government. That the state becomes some de facto beneficiary in anyone’s death is a little sick to begin with, but I have to assume that someone on Prince’s financial management team knew this. Maybe not? Either way, I’m baffled as to how someone who has exhibited such genius in his trade, was so aware of what was going on around him, and managed to keep his nose clean in such a dirty industry as music never signed a damn thing to protect the empire he built!

“Both the federal government, and Minnesota’s state government, will assess so-called “death taxes”, or estate taxes, on Prince’s assets, taking away more than half his estate. Between his physical assets—cash, investments, home, etc.—and his future royalties, Prince’s estate has been estimated to be between $300 and $500 million.

“If Prince were married, he could have passed on the entirety of his estate to his spouse tax free. However, without a spouse, only $1.6 million of Prince’s estate will be free from Minnesota’s death tax and only $5.45 million will escape the federal death tax.” (Source: The Daily Signal)

Had he even a simple will, this would not be the case. But having a trust is an extra layer of protection for those hard earned assets. A trust isn’t like a savings account where you stash your money. Much like a corporate structure it is about removing ownership, while giving you control over assets. It’s not the same in that you have a designated trustee who is in fact responsible for managing the assets of the trust, and that you can decide who has access to the assets (i.e. included or excluded parties), under what conditions the assets are released or not (e.g. duress clauses), and when said assets can or should be released as well as in what installments.

Very important to note: ALL TRUSTS ARE NOT CREATED EQUALLY.

Not only are there different kinds of trusts that offer different benefits based on your needs and goals, but there are different jurisdictions which offer various levels of legal protection. We did a two part series on the Cook Islands that shows what a powerful line of defense a trust can be: “The Cook Islands: Your Assets’ Best Friend” and “The Cook Islands: STILL Your Assets’ Best Friend”.

Each type of trust offers something a little different, so it’s important to first know what you are looking to accomplish. Are you trying to protect your assets from estate taxes when you pass? Are you looking for a seamless transfer of control of assets from when you are alive to long after you’re gone? Are you trying to keep your assets out of the reach of greedy litigants? There are revocable trusts, irrevocable trusts, testamentary trusts, special needs and charitable trusts, all of which fulfill a certain need.

If you’re thinking you need to be Prince-level rich to get a trust, think again. I am trying my best to dispel this terrible myth that asset protection is some exclusive benefit for the extremely wealthy. It most certainly is not. It’s for people with assets that want to keep them under their control and out of the hands of certain parties.

I get it. Death isn’t something people like to talk, much less think about. But getting your affairs in order has to do with not just the assets you leave behind… but the obligations you might be leaving behind. The death tax is no joke. It is predatory and destructive.

It’s one thing for me to tell you about trusts and how they can protect your assets, but perhaps it’s likewise important to understand the very real threats out there circling over your assets right now… literally waiting for you to kick the bucket before you sign on the line.

Truth be told, while I find the idea of government benefiting off the death of the productive to be disgusting, no one was hurt. No one benefited as much as they could have, but no one is any worse for wear either. This, believe it or not, is a BEST case scenario, I’m sad to say.

Not only are trusts NOT exclusive to the rich, neither are death taxes.

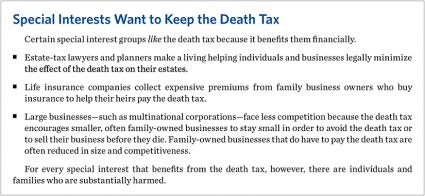

Have a look at who benefits from death taxes, and you tell me who the real victims are (Source: Heritage Foundation):

(You can click on this image to make it bigger and easier to read.)

(You can click on this image to make it bigger and easier to read.)

The amount of cronyism involved in even our deaths gives me reflux. Certainly, society doesn’t benefit from any of this. As usual only a handful do.

This is a more real depiction of what the death tax can do and has done:

“When the owner of a family business dies without leaving behind a large pile of cash or other liquid assets, the family often has to sell the business to pay the death tax. That can have devastating employment consequences. A 2014 analysis of the death tax by The Heritage Foundation found that its harmful effects on savings, investment, and capital reduces employment by 18,000 jobs each year.” (Source: The Daily Signal)

The death tax applies a 40% tax to all accumulated wealth above $5.34 million, but this isn’t just monetary. This is assessed wealth, as Prince’s estate is finding. How much is that house worth? How much are his yet-to-be-released songs worth? This isn’t just about how much he had in his bank account when he died.

Small businesses can hit that mark fairly easily. Entrepreneur offered a little profile of small businesses back in 2005. That’s over 10 years ago, and the average revenues of a small business with a website broke the $5 million mark. Imagine what that figure is today.

There are structures and trusts out there that keep your money in the private sector, in the hands of the people YOU trust, going toward things you condone. Protect not just your assets, but your legacy, and more importantly spare your beneficiaries the heartache of probate and fending off the government. Sure there are people fighting to overturn these laws, but the odds of the government giving up even this tiny portion of its revenues is highly unlikely.

This is absolutely a conversation worth having. Prince had a lot to offer in the way of musical talent. But the most important lesson should honestly be to get a will and a trust, if for no other reason than to keep your wealth out of the hands of government. Click here now to schedule an appointment to discuss your concerns and goals.