Financial stability can disappear faster than you think. From the collapse of banks in 2023 to a $36.8 trillion U.S. national debt by 2025, the risks are mounting. With currency devaluation, natural disasters, and political instability becoming more frequent, having a financial contingency plan is no longer optional – it’s essential for safeguarding your wealth and access to funds.

Here’s the key takeaway: diversify your assets, prepare for emergencies, and act before a crisis hits. This means spreading your wealth across currencies, jurisdictions, and asset types, while also keeping cash reserves and essential insurance in place. Offshore trusts, second passports, and foreign investments can offer additional layers of protection. The goal is to ensure your finances remain accessible and secure, no matter what challenges arise.

Quick Tips for Financial Preparedness:

- Emergency Fund: Save 3–6 months of living expenses in cash and high-yield savings accounts.

- Diversify Assets: Invest in precious metals, foreign currencies, and offshore accounts.

- Protect Legal Vulnerabilities: Use offshore trusts and LLCs to shield assets from lawsuits and government overreach.

- Plan for Natural Disasters: Keep physical cash, backup documents, and specialized insurance (e.g., flood coverage).

- Stay Compliant: Follow all U.S. tax and reporting rules for offshore accounts and structures.

Timing matters – set up protections before legal or financial trouble arises. Acting now ensures you’ll have options when others don’t.

Understanding Different Worst-Case Scenarios

Grasping these scenarios highlights how customized financial strategies can help protect your wealth during challenging times.

Economic Collapses and Currency Devaluation

Market crashes can wipe out years of savings in a matter of hours. For instance, Black Monday in 1987 saw the Dow plummet by 22.6%, and during the Iranian Revolution, GDP dropped to -20% by 1980. Inflation in Iran then remained between 12% and 20% for three decades. These examples illustrate how quickly financial stability can unravel.

Economic collapses often bring bank failures, widespread foreclosures, skyrocketing unemployment, and a freeze on new investments. In response, governments may introduce capital controls, restricting or outright banning the movement of money across borders.

Currency devaluation further erodes purchasing power. To counter this, holding "safe-haven" currencies like the Singapore dollar or Swiss franc can provide a buffer when the U.S. dollar weakens. Additionally, diversifying into assets like gold, silver, and cryptocurrency offers protection against the risks of fiat currency instability. Offshore protections, when properly set up, can also ensure access to funds if domestic financial systems falter. These strategies emphasize the importance of looking beyond traditional banking to safeguard wealth during economic turmoil.

Political Instability and Asset Seizure Risks

Political unrest can pose immediate dangers to personal wealth. Emergency policies may lead to asset freezes, nationalization of industries, or sudden tax hikes to cover government deficits. Concentrating all assets in a single country increases vulnerability to abrupt legal or policy changes.

Consider this: in 2023, around 5 million new court cases were filed in the U.S.. High-net-worth individuals often become targets during economic crises. Establishing offshore trusts and LLCs can create a legal separation for your assets, placing them under foreign jurisdictions. Foreign courts typically refuse to enforce U.S. court orders without requiring a fresh legal process under stricter standards.

"When all your assets are in one country, you’re completely at the mercy of that country’s laws and economy." – The Nestmann Group

This underscores the importance of jurisdictional diversification. However, these structures must be in place before any legal disputes or crises arise, as courts can later invalidate them as fraudulent transfers.

Natural Disasters and Their Financial Impact

Natural disasters can cause immediate financial strain. In 2024, the U.S. faced 27 disaster events, each with economic losses exceeding $1 billion. FEMA‘s 2023 National Household Survey revealed that 54% of respondents had been personally affected by a natural disaster or had family members who were.

Power outages from these events can disable ATMs and credit card systems, leaving those reliant on digital access to funds in a bind. Banks may freeze or limit Home Equity Lines of Credit (HELOCs) after disasters due to uncertainty about the value of damaged collateral. Matt Franks, Head of Wealth Management Lending at RBC Wealth Management–U.S., cautions:

"HELOCs often get shut down or limited. Relying on them for liquidity is imprudent at best"

Additionally, disrupted mail services can delay or lose paper checks. Many homeowners are also caught off guard by the fact that standard insurance policies exclude flooding, requiring separate coverage through programs like the National Flood Insurance Program. With only 54% of Americans having enough savings to cover three months of expenses, a significant portion of households remains financially vulnerable when disaster strikes. Recognizing these risks is key to implementing measures that ensure liquidity and protect assets during such crises.

sbb-itb-39d39a6

How Offshore Asset Protection Works

Offshore asset protection involves transferring your wealth to foreign jurisdictions where U.S. court orders don’t automatically apply. The key idea here is jurisdictional separation – placing assets under the control of foreign laws and trustees, creating a legal barrier that shields your wealth from domestic risks.

When you set up an offshore structure, creditors can’t simply enforce a U.S. judgment against your assets. They would need to hire local lawyers, re-litigate the case under the foreign jurisdiction’s laws, and meet stricter legal requirements. This process is expensive and time-consuming, often discouraging potential lawsuits or claims.

"The fundamental principle is jurisdictional separation: assets are owned by foreign entities, administered by independent foreign trustees, and governed by foreign law." – Jon Alper, Attorney

For this strategy to work effectively, there must be a genuine separation of control. Independent trustees should have real authority over the assets, though a protector role can sometimes be added to veto trustee decisions without taking over control.

A common approach involves layering. For instance, an offshore trust might own an offshore LLC, which then holds bank accounts or investments. Each layer adds another legal obstacle, making it increasingly difficult for creditors to access the assets.

Advantages of Offshore Asset Protection

One of the biggest advantages is protection from lawsuits and creditor claims. In 2023, around 5 million new court cases were filed in the U.S.. High-net-worth individuals are often targeted, especially during economic downturns or disputes. Offshore structures force anyone pursuing your assets to start over in a foreign legal system, which can be a major deterrent.

Another benefit is privacy. While all foreign accounts must be reported to the IRS, offshore structures can help keep financial details out of public records, creating a layer of separation from domestic databases.

Currency diversification is another plus. Offshore accounts allow you to hold foreign currencies, such as the Swiss franc, as a hedge against dollar devaluation. For example, the U.S. dollar experienced a significant drop of over 10% against the DXY in the first half of 2025, marking its worst start since 1973.

Certain jurisdictions, like the Cook Islands and Nevis, make it especially hard for creditors to succeed. They impose high burdens of proof, sometimes requiring claims to be proven "beyond a reasonable doubt" instead of the lower "preponderance of evidence" standard used in the U.S. They also enforce shorter statutes of limitations – often one or two years – for challenging asset transfers as fraudulent.

Offshore LLCs offer charging order protection. If a creditor wins a judgment, they are typically limited to receiving distributions you choose to make, rather than being able to seize assets, force a sale, or take over the business.

While these benefits are compelling, offshore asset protection comes with strict compliance requirements for U.S. citizens.

Legal Requirements for US Citizens

It’s important to note that offshore asset protection is not a tax avoidance tool. U.S. citizens are required to pay taxes on their worldwide income, regardless of where their assets are located. The IRS also mandates full disclosure of all foreign accounts and entities.

"Offshore asset protection is not a tax strategy. It requires full compliance with all U.S. tax and reporting obligations." – Jon Alper, Attorney

Here are the key reporting requirements:

- FBAR (FinCEN Form 114): Must be filed annually if the total value of your foreign accounts exceeds $10,000 at any point during the year. Failure to comply can lead to severe penalties.

- IRS Form 8938: Used to report certain foreign financial assets, with thresholds varying based on your filing status and residency.

- Forms 3520 and 3520-A: These apply to foreign trusts. Form 3520 reports transactions, while Form 3520-A serves as the trust’s annual information return.

- Form 5471: Required for U.S. persons who are officers, directors, or shareholders of foreign corporations.

Timing is critical. These structures must be set up before any legal issues arise. Courts can undo transfers made after a lawsuit is filed, labeling them as "fraudulent conveyances". Planning years in advance, when no specific threats exist, offers the strongest protection.

"The best plan is to set up protection years before any trouble. This way, no one can say you were trying to dodge a specific person who’s after your money." – The Nestmann Group

Professional guidance is essential. Working with a U.S. tax attorney, a CPA experienced in international reporting, and legal experts in the chosen offshore jurisdiction ensures your structure is both effective and fully compliant with U.S. laws.

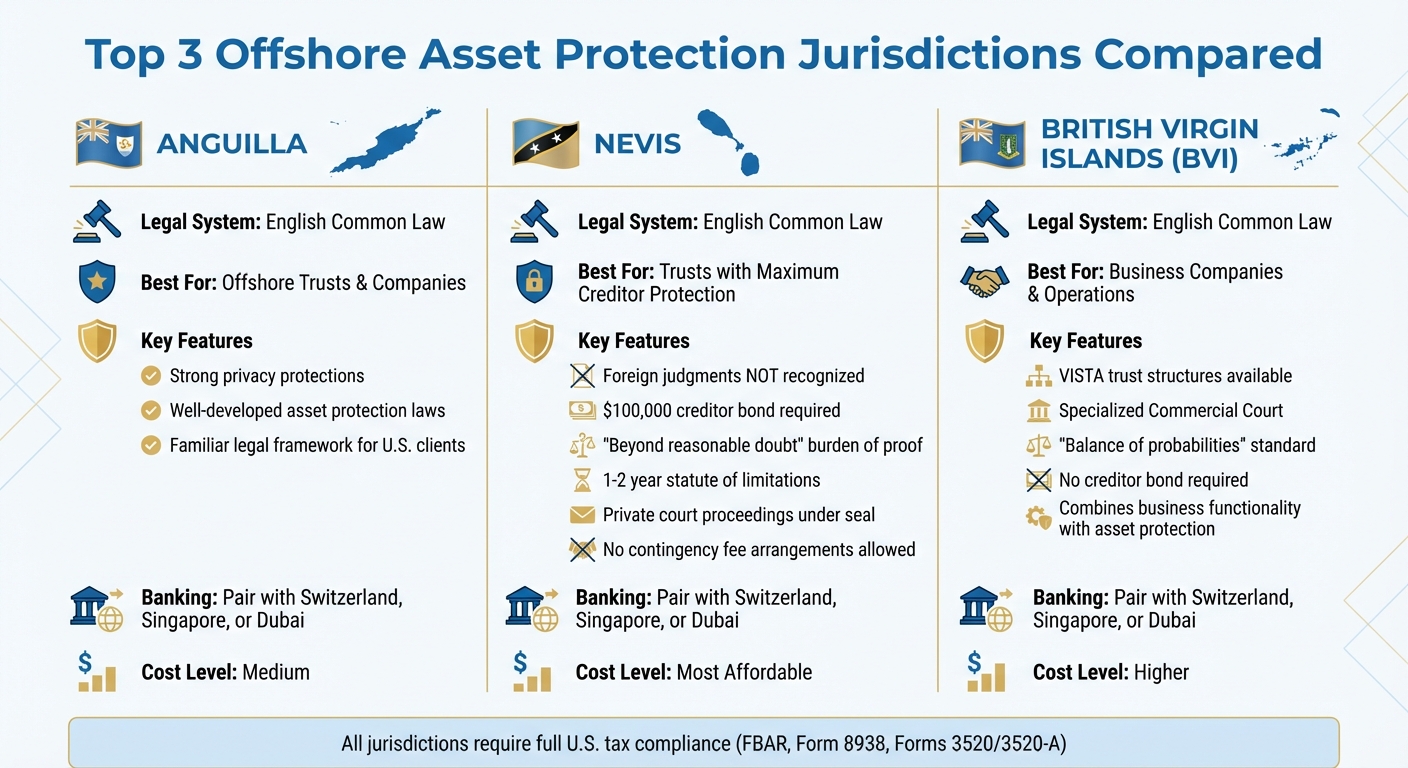

Best Jurisdictions for Asset Protection

Offshore Asset Protection Jurisdictions Comparison: Anguilla vs Nevis vs BVI

Picking the right jurisdiction is a key step when setting up an asset protection strategy, especially in worst-case scenarios. Different offshore jurisdictions offer varying levels of protection, so the best choice depends on your priorities – whether you’re focusing on legal barriers for creditors, affordability, or seamless business operations. Among the top choices are Anguilla, Nevis, and the British Virgin Islands (BVI).

These jurisdictions operate under English common law, a legal framework that’s familiar and predictable for U.S. clients. They’re designed to protect wealth from lawsuits, creditors, and even government agencies through clear legal safeguards. That said, establishing banking relationships in these regions has become trickier due to stricter Anti-Money Laundering (AML) and Know-Your-Client (KYC) requirements. For this reason, it’s often recommended to pair an offshore structure from one of these jurisdictions with a bank account in a different location, such as Switzerland, Singapore, or Dubai. Let’s dive into the unique benefits and legal protections each jurisdiction offers.

Anguilla: Offshore Trusts and Companies

Anguilla is a favorite for setting up offshore trusts and companies, thanks to its combination of privacy and strong legal protections. Its asset protection laws are well-developed, offering a familiar framework for U.S. clients.

Nevis: Trusts with Strong Legal Safeguards

Nevis stands out for its affordability and its aggressive legal barriers against creditors. One of its key advantages is that foreign judgments are not recognized, meaning creditors must start fresh legal proceedings under Nevis law. This process is far from easy:

- Creditors must post a $100,000 bond before filing a claim.

- Contingency fee arrangements are not allowed; creditors must hire local counsel on a fee basis.

- The burden of proof is set at "beyond a reasonable doubt", a criminal standard much stricter than the typical U.S. civil standard.

- The statute of limitations for fraudulent transfer claims is only one to two years.

Additionally, court proceedings related to trusts are held privately, under seal, to protect confidentiality. Nevis also offers flexibility with its multiform foundations.

While Nevis focuses on robust creditor protection, the British Virgin Islands provide a blend of business functionality and asset security.

British Virgin Islands: Business Companies

The British Virgin Islands (BVI) is known for its sophisticated legal system and its ability to integrate business operations with asset protection. A standout feature is its VISTA trust structures, which allow trustees to hold shares without interfering in day-to-day management. This makes the BVI particularly appealing for those seeking to combine business activities with asset security.

The BVI also has a specialized Commercial Court for handling complex trust and business disputes. Unlike Nevis, the BVI operates under a "balance of probabilities" standard and does not require creditors to post a bond. Jacob Stein sums it up well:

"We may use Nevis, the BVI or Hong Kong for legal entities".

Financial Tools and Structures for Asset Protection

Once you’ve chosen your jurisdiction, the next step is selecting the right legal structures and financial tools to shield your assets. These methods add extra layers of security, helping protect your wealth in a variety of situations.

Private US LLCs for Domestic Privacy

If you’re starting with domestic asset protection before considering offshore options, a private US LLC can provide an initial shield. States like Wyoming, Delaware, and New Mexico are popular choices because they keep ownership details out of public records. This means your name won’t pop up in a simple search, making you less visible to potential lawsuits.

One major advantage is charging order protection. If a creditor wins a judgment against you personally, they cannot directly seize the LLC’s assets. Instead, they can only get a charging order, which entitles them to distributions – but only if you decide to make them.

However, domestic LLCs have their limitations. U.S. courts can still order you to disclose assets or satisfy judgments. If you mix personal and business funds or use company property for personal purposes, you risk "piercing the corporate veil", allowing creditors to go after your personal assets. For high-risk professionals, such as physicians – who face a 31.2% chance of being sued during their careers – a domestic LLC may not be sufficient on its own.

Offshore Banking and Multi-Jurisdiction Accounts

Offshore banking can safeguard your funds when domestic accounts are at risk. If your U.S. accounts are frozen due to legal disputes or other issues, having money in a foreign jurisdiction ensures you remain financially liquid.

Switzerland is often considered the benchmark for banking stability, though most Swiss banks require a minimum of $1 million tied to an asset management account. Austria offers a more accessible entry point, with private banking minimums in the $250,000 to $300,000 range. Both countries also provide multi-currency accounts, which can help hedge against dollar devaluation – something that became evident when the U.S. dollar dropped over 10% against the DXY in early 2025.

Pairing offshore banking with an offshore structure enhances protection. For instance, a Nevis LLC owned by a Cook Islands trust can hold the bank account, creating multiple legal layers. As asset protection attorney Jon Alper explains:

"Offshore asset protection is not a tax strategy. It requires full compliance with all U.S. tax and reporting obligations".

Keep in mind that you must file FBAR (FinCEN Form 114) and Form 8938 if your foreign accounts exceed $10,000 at any point in the year. With offshore banking in place, the next step is spreading your investments across different asset classes to reduce risk.

Diversified Investment Options

Diversifying your investments is another key strategy for protecting your portfolio from market and political risks. Spreading your wealth across asset types can help you weather financial storms. For example:

- If the stock market crashes, foreign real estate may still hold its value.

- If real estate markets decline, precious metals can act as a tangible hedge.

- If inflation surges, international stocks in stronger currencies can help maintain purchasing power.

For high-net-worth individuals with at least $2 million in liquid assets, Private Placement Life Insurance (PPLI) is a sophisticated option. It combines creditor protection, tax-deferred growth, and streamlined wealth transfer into a single structure. For U.S. real estate, equity stripping can be effective: you encumber the property with a senior lien and move the loan proceeds into a secure offshore account.

In 2023 alone, approximately 5 million new lawsuits were filed in the United States. Preparing in advance isn’t overcautious – it’s simply smart planning.

How to Build Your Financial Preparedness Plan

Creating a solid financial preparedness plan involves layering strategies to safeguard your finances. Start with the fundamentals and gradually incorporate more advanced measures as your financial situation evolves.

Setting Up an Emergency Fund

An emergency fund is your financial safety net. Start small by saving $1,000–$2,000 to cover two to four weeks of essential expenses. From there, aim to build a fund that covers three to six months of living expenses. For example, a six-month reserve might require approximately $38,000, depending on your lifestyle and monthly costs. Setting up automatic transfers from your paycheck can help you reach this goal without the temptation to spend.

Keep these savings separate from your day-to-day accounts. A high-yield online savings account is a great option, often offering interest rates above 4%, which can outpace many traditional money market accounts. David Bigelow from Coldstream Wealth Management emphasizes:

"The most valuable first step in emergency proofing your finances is to have a grasp on monthly cash flow".

Additionally, keep some physical cash at home in small denominations. This can be a lifesaver during natural disasters or digital banking outages. With only 54% of Americans having enough savings to cover three months of expenses, this step is especially critical.

Once your emergency fund is in place, you can shift your focus to diversifying your investments to mitigate different types of risks.

Creating a Diversified Asset Portfolio

After securing liquidity, the next step is diversifying your investments. Spread your assets across various classes, currencies, and regions to protect your portfolio from a single point of failure.

Currency diversification is particularly important. Recent fluctuations in currency values highlight the benefits of holding multiple currencies. For instance, if you have significant expenses in Europe, keeping a portion of your liquid assets in Euros could align better with your spending needs.

Geographic diversification also helps reduce risk. For instance, non-U.S. equities outperformed U.S. stocks by 12.1% in the first half of 2025. If you’re investing in international real estate, consider using local legal entities to simplify and safeguard your holdings.

For those looking to add hard assets, storing physical gold and silver in secure offshore vaults – such as in Singapore – can provide additional protection. If you have $2 million or more in liquid assets, Private Placement Life Insurance (PPLI) offers options like creditor protection, tax-deferred growth, and efficient wealth transfer.

Reviewing and Updating Your Plan Regularly

Setting up your financial preparedness plan is just the beginning. Regular reviews are essential to keep up with changing circumstances and risks. Aim to revisit your plan annually or after major life events like marriage, divorce, starting a business, or a significant increase in wealth.

Insurance coverage should also be reviewed periodically. Property values can change, and new risks, like flooding (often excluded from standard policies), may arise. With over 5 million new court cases filed in the U.S. in 2023, adding umbrella insurance can offer extra liability protection.

Digitizing and encrypting critical documents – such as bank account details, insurance policies, and property deeds – ensures they’re accessible when needed. Tools like the Emergency Financial First Aid Kit (EFFAK) can help you organize these records effectively.

Timing is another key factor in asset protection. Strategies like offshore trusts or LLCs should be established before any legal claims arise. Transferring assets after a lawsuit begins can be reversed as a "fraudulent transfer". Acting during calm periods is far more effective than scrambling in a crisis.

Conclusion: Building Financial Resilience

Taking steps toward financial resilience means acting well before challenges arise. It’s not about predicting the future but about creating systems that can withstand uncertainty. Often, the ability to navigate crises depends on decisions made long before the storm hits. With mounting legal challenges and national debt, the risks are becoming harder to ignore.

The best time to act is during periods of stability. For example, asset protection structures must be in place before any legal claims surface. Courts can nullify transfers made afterward, labeling them as fraudulent. As The Nestmann Group wisely notes:

"It’s like buying car insurance. You can’t get it after you’ve had an accident. By then, it’s just too late."

Start with the basics: establish a clear cash flow baseline, build liquidity through high-yield savings and physical cash, and eliminate high-interest debt. Once those are in place, consider adding layers of diversification – geographically, through multiple currencies, and even with offshore structures or global mobility options. These steps can put you ahead of the nearly half of Americans who lack sufficient emergency savings.

True financial resilience relies on spreading risk across jurisdictions, currencies, and legal systems. As James Hickman, founder of Sovereign Man, explains:

"A good asset protection strategy is like putting ‘the club’ on your steering wheel… most of the time when they see how protected you are, they’ll just move on to an easier target."

The objective isn’t to create an unbreakable fortress but to make it more difficult for potential threats to succeed. Whether you’re starting with something as simple as an emergency fund or exploring advanced strategies like offshore trusts, the key is to act now. Taking steps today ensures you’ll have choices tomorrow – choices that others may wish they had.

FAQs

How much cash should I keep at home?

In times of emergencies, like natural disasters, it’s wise to have some cash on hand to cover essential expenses. The recommended amount can vary based on your household size and specific needs but typically falls between a few hundred dollars and $1,000 or more. Make sure to store this cash in a secure place and reserve it strictly for urgent situations.

What’s the simplest way to add currency diversification?

Diversifying your currency holdings can be straightforward. One approach is to invest in a combination of stable currencies, like the Swiss Franc, alongside resource-tied currencies. Another option is to use multi-currency accounts, which not only reduce conversion fees but also offer greater flexibility in managing your money.

When is it too late to set up an offshore trust or LLC?

It’s important to understand that once the statute of limitations has passed, setting up an offshore trust or LLC is no longer an option. The exact timeframe depends on the jurisdiction but can include scenarios like 21 years after the grantor’s death or when legal claims are no longer valid – for example, after the IRS audit period ends, which is typically between 3 to 7 years. The key takeaway? Timing is everything. Make sure to act before these deadlines come into play.