Protecting your wealth in 2026 requires more than traditional investment strategies. With stabilizing inflation, shifting interest rates, and global uncertainties, the focus is on reducing concentration risk, diversifying internationally, and leveraging legal structures. Key takeaways:

- Concentration Risk Matters: Relying solely on domestic markets exposes you to fiscal pressures, regulatory changes, and geopolitical risks.

- Global Diversification: International equities may outperform U.S. equities, with projected returns of 6.9%-8.9% vs. 3.7%-5.7%. Adding currencies like the euro or Swiss franc can hedge against a weakening U.S. dollar.

- Asset Classes: Mix equities, bonds, REITs, and commodities like gold to balance growth and stability.

- Offshore Accounts: Secure assets under foreign laws, reduce creditor risks, and hedge currency exposure. Compliance with U.S. tax laws is essential.

- Trusts and LLCs: [Offshore trusts in jurisdictions like Anguilla provide creditor protection, while private U.S. LLCs enhance domestic privacy.

- Offshore Companies: Ideal for global operations, they offer tax neutrality and confidentiality in jurisdictions like Anguilla or the Cayman Islands.

Act early. Setting up these structures proactively avoids legal complications and ensures better protection. Tailor your approach to your risks and goals, combining international diversification with legal safeguards.

Diversifying Across Global Markets to Reduce Risk

Why International Diversification Matters

Spreading investments across multiple countries acts as a safeguard against localized economic downturns. For instance, if U.S. markets face a rough patch, markets in Europe or Asia might still thrive, helping to steady your portfolio. This is because financial markets in different regions don’t move in perfect harmony. By looking beyond local markets, you not only reduce risks tied to one region but also gain access to a broader range of investment opportunities and asset classes.

The data backs this up. Vanguard projects international equities to yield annualized returns of 6.9% to 8.9% over the next decade, compared to 3.7% to 5.7% for U.S. equities.

Currency diversification is another often-overlooked benefit. Holding assets in currencies like the euro, Swiss franc, or Japanese yen can act as a hedge against a weakening U.S. dollar and domestic inflation.

Vanguard suggests allocating at least 20% of your portfolio to international investments. For optimal diversification, they recommend targeting 40% for stocks and 30% for bonds. Christian Mueller-Glissmann, Head of Asset Allocation at Goldman Sachs Research, highlights:

It might be difficult for US equities to sustain their outperformance with less of a tailwind from valuations, earnings, and the dollar.

Asset Classes for a Balanced Portfolio

Global diversification is just the starting point. To build a truly resilient portfolio, you need a mix of asset classes that respond differently to market conditions. Equities fuel long-term growth, bonds add income and stability, and REITs (real estate investment trusts) provide both diversification and protection against inflation.

Gold and commodities deserve a closer look in 2026. While standard portfolios allocate around 5% to gold, increasing this percentage could strengthen your defense against inflation and a declining dollar. With gold expected to rise by 6% by mid-2026, it’s a timely addition for preserving wealth.

For convenient access to global investments, low-cost international ETFs or mutual funds are hard to beat. They give you exposure to thousands of foreign securities without the hassle of trading on individual foreign exchanges. These funds allow you to tap into stable developed markets like the UK and Japan, fast-growing emerging markets like India and Brazil, and even frontier markets in Africa and the Middle East, offering early-stage growth opportunities.

To keep your portfolio on track, regular rebalancing is key. Financial advisors recommend revisiting your allocations whenever an asset class drifts more than 5% to 10% from its target. This disciplined approach ensures you sell high-performing assets and buy those that are underrepresented – a proven way to buy low and sell high.

sbb-itb-39d39a6

Using Offshore Accounts for Asset Protection

Benefits of Offshore Accounts

Offshore accounts provide a way to protect your assets by placing them under foreign laws, making it more expensive and complicated for creditors in your home country to pursue them. Creditors often face the daunting task of navigating foreign legal systems, which can involve re-litigation and significant costs. This added layer of difficulty can act as a strong deterrent.

In early 2025, the U.S. dollar saw a drop of over 10% against the DXY index, which tracks a basket of major global currencies. With U.S. national debt exceeding $31 trillion, many investors are turning to multi-currency accounts to hedge their exposure. These accounts often include currencies like the Swiss franc, euro, or Singapore dollar.

Some jurisdictions, such as Anguilla and Nevis, offer the added advantage of lacking public registries. This reduces your visibility in litigation, which is particularly relevant considering that approximately 5 million new court cases were filed in the United States in 2023 alone.

Modern offshore banking also helps shield wealth from risks like bank failures, capital controls, and political instability. By 2023, 108 countries were automatically sharing data on 123 million offshore accounts, representing assets worth over €12 trillion. This shift toward transparency means today’s offshore banking relies on legal structures and strict compliance, rather than secrecy. As attorney Jon Alper explains:

Offshore asset protection is not a tax strategy. It requires full compliance with all U.S. tax and reporting obligations.

Up next, let’s explore the jurisdictions where these protections are most effectively implemented.

Top Jurisdictions for Offshore Banking

Choosing the right jurisdiction for offshore banking is crucial to maximizing the benefits of asset protection.

Switzerland is a top choice for long-term wealth preservation. Known for its conservative banking culture and the stability of the Swiss franc, Swiss banks often require a minimum of $1 million to begin asset management services. This country is ideal for high-net-worth individuals looking to preserve wealth across generations, with a strong emphasis on discretion and professional service.

Singapore has become the leading hub for Asia-focused portfolios. Combining tight financial regulation with efficient operations, Singapore offers robust multi-currency capabilities and a respected financial infrastructure. Its common law system makes it particularly appealing to entrepreneurs and investors seeking stability and access to emerging Asian markets.

For those interested in asset protection trusts, the Cook Islands and Nevis are standout options. The Cook Islands has a strong track record of legal protections against creditor claims, while Nevis offers similar protections with lower setup and maintenance costs. The Cayman Islands, on the other hand, is known for its expertise in investment funds and trusts, with courts that do not automatically enforce foreign civil judgments.

Anguilla is worth considering for its zero corporate tax structure and lack of public registries, making it particularly attractive to crypto and digital businesses. Meanwhile, Luxembourg is a prime destination for institutional-grade wealth management within the EU regulatory framework, offering strong options for cross-border financial structures. The United Arab Emirates, through its DIFC and ADGM zones, has also gained popularity for international trade and business operations, thanks to its independent common-law systems.

It’s important to note that U.S. taxpayers are required to file an FBAR (FinCEN Form 114) if their combined offshore account value exceeds $10,000 at any point during the calendar year. Additionally, establishing offshore structures should be done before any legal threats arise, as transfers made afterward could be reversed as fraudulent.

Using Trusts and LLCs for Asset Protection

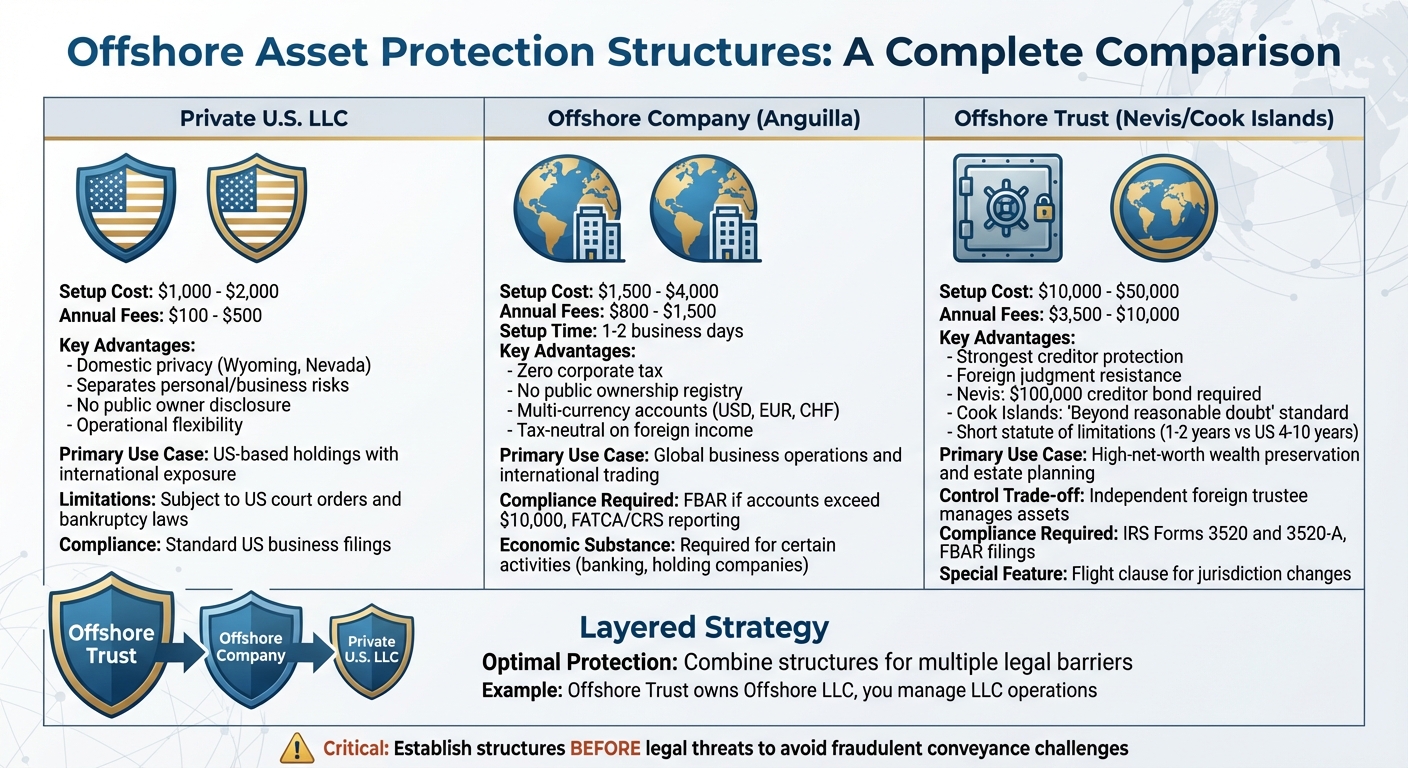

Offshore Asset Protection Structures Comparison: Trusts, LLCs, and Companies

Legal tools like trusts and LLCs create an extra layer of defense between your assets and potential creditors. alongside offshore bank accounts, these structures can help safeguard your portfolio from unexpected legal claims. Essentially, they work by shifting legal ownership of assets while still allowing you to benefit from them. The main distinction lies in where these entities are established and how they interact with U.S. legal systems.

Offshore Trusts: A Barrier Against Creditors

Offshore trusts operate under foreign laws, often making it difficult for U.S. court judgments to apply. Creditors are forced to re-litigate claims in another country, which can be both costly and complex. For example, Nevis requires creditors to post a $100,000 bond before they can even begin legal proceedings. In the Cook Islands, creditors face the daunting task of proving fraudulent intent "beyond a reasonable doubt", significantly raising the bar for litigation. Additionally, these jurisdictions often impose shorter time limits for challenging transfers – typically 1–2 years – compared to the 4+ years allowed in most U.S. states or the 10 years under federal bankruptcy law.

"FAPTs aren’t magic shields that make you ‘judgment proof.’ What they do is create massive economic disincentives for creditors to pursue trust assets."

- Terms.law

Setting up an offshore trust can cost anywhere from $10,000 to $50,000, with annual maintenance fees ranging between $3,500 and $10,000. The Cook Islands, which introduced the first modern asset protection trust law in 1984, is often regarded as the "gold standard" for protecting high-value estates. A common strategy involves combining an offshore trust with an LLC – where the trust owns 100% of the LLC, often based in Nevis or the Cook Islands. In this arrangement, you manage the LLC for day-to-day operations, while the trustee holds the membership interests, adding another layer of security.

Important compliance note: U.S. citizens must disclose offshore trusts to the IRS using Forms 3520 and 3520-A and report foreign accounts via FBAR filings.

Now, let’s look at how private U.S. LLCs can enhance domestic privacy while complementing offshore strategies.

Private U.S. LLCs for Privacy at Home

Unlike offshore trusts, which focus on international asset protection, private U.S. LLCs offer a straightforward way to maintain privacy domestically. States like Wyoming and Nevada allow LLC formation without requiring the public disclosure of owner names, ensuring a degree of anonymity.

While U.S. LLCs don’t offer the same creditor protection as offshore trusts – since they’re still subject to U.S. court orders and federal bankruptcy laws – they are excellent for separating personal and business risks. Establishing a private LLC in the U.S. is relatively inexpensive, with setup costs ranging from $1,000 to $2,000 and annual fees between $100 and $500. This makes them a practical choice for entrepreneurs who need operational flexibility without the additional reporting obligations tied to foreign entities.

Combining an offshore trust with a private U.S. LLC creates a powerful asset protection strategy. This setup leverages the jurisdictional advantages of offshore trusts while maintaining operational control domestically. For example, you can retain signature authority over accounts while the trust acts as the ultimate legal shield. Many trusts include a "flight clause", which allows the trustee to remove you as manager and move assets to another jurisdiction if legal challenges arise. This ensures your assets remain protected, even in rapidly changing legal landscapes.

Timing is crucial. These structures must be established in advance to avoid accusations of fraudulent conveyance.

Offshore Company Formation: Increasing Financial Flexibility

Setting up an offshore company can open up new financial opportunities for investors looking to operate on a global scale. These companies provide a neutral base for managing international transactions, intellectual property, and multi-currency accounts – all while shielding assets from domestic legal challenges. The real advantage lies in jurisdictional separation: U.S. courts typically cannot force foreign entities to violate their own laws, creating a protective barrier against creditors. This approach not only spreads out legal risks but also adds another layer of flexibility to your portfolio.

Offshore companies complement other asset protection strategies by offering operational ease and potential tax savings. In certain jurisdictions, companies can benefit from zero corporate, income, or capital gains taxes. For instance, Anguilla is considered tax-neutral, meaning profits earned outside the country are not taxed locally. This aligns with legal tax strategies, as noted by Global Wealth Protection:

"Going offshore isn’t about secrecy. It’s about control. You control where your company is based, where your money lives, and how much you pay in tax."

Another key benefit is privacy. Many offshore jurisdictions do not require directors or beneficial owners to be listed in public registries, offering a level of confidentiality that is becoming rare in the U.S.. Modern setups are designed to comply with international standards like CRS and FATCA, ensuring transparency and efficiency.

Contrary to popular belief, forming an offshore company is often straightforward. In Anguilla, for example, incorporation takes just 1–2 business days, with initial costs ranging from $1,500 to $4,000 and annual maintenance fees between $800 and $1,500. By mid-2025, Anguilla had over 5,000 active international companies, with 80% structured as International Business Companies (IBCs) – a 10% increase from the previous year.

Acting proactively is essential. Transferring assets after a legal claim arises can expose you to fraudulent conveyance challenges. Additionally, companies involved in certain activities (like banking or holding companies) must meet economic substance requirements, which include maintaining qualified staff and operational expenses within the jurisdiction. Non-compliance can result in penalties up to $50,000.

Best Jurisdictions for Offshore Companies

Choosing the right jurisdiction is crucial for aligning offshore company formation with your overall financial goals.

- Anguilla is ideal for digital businesses and crypto investors. It offers zero corporate tax, no public ownership registry, and advanced e-filing systems with AI-supported anti-money laundering compliance as of 2026. Government fees start at $450, with professional service packages ranging from $1,000 to $2,500.

- The British Virgin Islands (BVI) is a major player, hosting over 400,000 active companies. Known for its VISTA trust regime under the Virgin Islands Special Trust Act 2003, the BVI is particularly suited for holding shares in high-risk investments. Financial services make up over 60% of the BVI’s GDP, reflecting its well-developed infrastructure.

- The Cayman Islands offers STAR trusts for non-charitable purposes and no direct taxation on companies.

- Panama operates on a territorial tax system, exempting foreign-sourced income from taxation while upholding strong asset protection laws.

- The Bahamas provides a tax-neutral environment with no taxes on corporate income, capital gains, or dividends, coupled with strict privacy laws.

- Hong Kong serves as a gateway to Asian markets, offering a low-tax, territorial system.

- Cyprus provides access to the European Union with one of the lowest corporate tax rates in the region.

When selecting a jurisdiction, consider your primary goals – whether they involve tax savings, asset protection, or access to specific markets. Also, check if the jurisdiction and its banks support remote onboarding. Many now allow account setup through video calls and secure portals, eliminating the need for in-person visits.

Offshore Companies vs. Domestic Entities: A Comparison

Comparing offshore companies with domestic structures can help clarify which option suits your financial strategy. Offshore companies deliver unique benefits that complement other asset protection tools:

| Structure | Key Advantages | Primary Use Case |

|---|---|---|

| Private US LLC | Privacy, asset protection, registered agent service | US-based holdings with international exposure |

| Offshore Company (Anguilla) | Tax exemptions, confidentiality, efficient incorporation | Global business operations |

| Offshore Trust (Nevis/Anguilla) | Creditor protection, foreign judgment resistance, estate planning | High-net-worth wealth preservation |

Offshore companies are particularly effective for international trading or consulting, offering multi-currency accounts (USD, EUR, CHF) to mitigate risks tied to local currencies or political instability. By contrast, domestic entities like U.S. LLCs, while offering some privacy in states like Wyoming and Nevada, are still subject to U.S. taxes and court orders.

A layered approach often works best. For instance, combining an offshore trust with an offshore LLC creates multiple legal barriers, making it harder and costlier for creditors to take action. Many investors pair a private U.S. LLC for domestic operations with an offshore company for international dealings, achieving both privacy and global flexibility.

Important compliance note: U.S. taxpayers must file an FBAR (FinCEN Form 114) if their combined offshore account values exceed $10,000. Offshore companies also come with international reporting obligations under FATCA and CRS rules. While company formation is quick, opening international bank accounts can take 2–4 weeks due to strict Know Your Customer (KYC) protocols, so plan accordingly.

Steps to Strengthen Your Portfolio

Start by defining your objectives – whether it’s investment diversification, maintaining privacy, optimizing taxes, or pursuing foreign residency. Then, identify which assets are most vulnerable to threats like currency devaluation, professional liability, or business disputes. Each situation calls for a unique approach. For example, a physician concerned about malpractice claims will need a completely different setup than a real estate developer dealing with project-specific risks.

Timing is everything. Asset protection works best when it’s proactive. It’s crucial to consult experienced advisors early to navigate the complexities involved. The Nestmann Group puts it perfectly:

The best plan is to set up protection years before any trouble. It’s like buying car insurance. You can’t get it after you’ve had an accident.

Once your objectives and risks are clear, it’s time to put tailored global wealth protection measures into action.

Getting Started with Global Wealth Protection

Building on earlier strategies, global wealth protection strengthens your portfolio both at home and abroad. This process typically begins with a private consultation, where you’ll discuss your financial situation, risk profile, and long-term goals. From there, advisors help determine the right combination of structures – such as a private U.S. LLC, offshore company, or offshore trust – to meet your needs.

For those who want ongoing support, the GWP Insiders membership program offers access to strategies on internationalization, tax reduction, jurisdiction selection, and personalized consultations.

Global Wealth Protection also provides comprehensive services, including:

- U.S. LLC Formation: Covers filings and registered agent services.

- Offshore Company Formation: Primarily in Anguilla, but available in other jurisdictions as well. Services include filings, certifications, and bank introductions.

- Offshore Trusts and Foundations: Designed for high-net-worth clients, these include trust administration and asset management, primarily in Anguilla.

One key factor to consider is the minimum investment required for offshore accounts. Most reputable options require between $100,000 and $1 million. For example, Swiss banks typically expect at least $1 million tied to an asset management account, while Austrian private banking starts at $250,000 to $300,000. Knowing these thresholds can help you set realistic expectations during your consultation.

Once your foundational structures are in place, you can refine your strategy to suit your specific needs.

Customizing Your Strategy

With your objectives defined, the next step is to customize your approach by assessing your assets and aligning them with your risk profile. Every investor’s situation is different, so it’s essential to tailor your strategy accordingly. Start by inventorying your assets – this includes personal, business, and digital holdings – to identify which ones need the strongest protection. For instance, a doctor facing licensing risks will require a different setup than a tech entrepreneur safeguarding intellectual property.

Think about the balance between control and protection. Generally, the more control you retain over your assets, the less legal protection they’ll have. Offshore trusts, for example, offer strong protection by separating you from the assets, but that also means an independent foreign trustee will handle certain decisions.

Jurisdictional alignment is another key factor. Your asset currency exposures should match your lifestyle and spending habits. For example, if you spend 40% of your time in Europe, it might make sense to hold a comparable share of your assets in Euros. This is particularly relevant given recent trends, such as the U.S. Dollar dropping over 10% against the DXY index as of September 2025, and non-U.S. equities outperforming U.S. equities by 12.1% in the first half of 2025.

A layered defense often provides the best protection. Combine domestic tools like umbrella insurance and LLCs with offshore structures such as trusts and foreign accounts. This creates multiple hurdles for creditors. For instance, you could use a private U.S. LLC for domestic operations while maintaining an offshore company for international dealings, both potentially owned by an offshore trust for added security.

Lastly, stay compliant. These structures require annual filings, such as FBAR (FinCEN Form 114) for offshore accounts exceeding $10,000, as well as separate bank accounts and proper documentation of decisions. Regular reviews are essential to ensure your strategy evolves with your financial situation and changing regulations. For those considering relocation as part of their strategy, Global Wealth Protection’s Global Escape Hatch action plans offer detailed frameworks to guide the process.

Conclusion: Protecting Wealth in an Uncertain World

The financial landscape in 2026 is marked by challenges like economic pressures, shifting regulations, and fluctuating currencies. In this environment, protecting your assets requires more than just conventional investment strategies – it calls for a proactive and layered approach to safeguard wealth effectively.

The strategies outlined earlier – such as global diversification, offshore banking, legal protections, and aligning with favorable jurisdictions – offer a solid foundation for shielding your assets. These methods help mitigate risks from creditors, currency instability, and political uncertainty. As Luigi Wewege, President of Caye International Bank, highlights:

Jurisdictions such as Belize, St. Kitts & Nevis, and Antigua & Barbuda now offer legal predictability, common-law heritage, and access to global banking systems.

Timing is everything. Building robust structures like private U.S. LLCs for privacy or offshore trusts and foundations for broader protection works best when done proactively. Waiting until a crisis arises can lead to complications, particularly under fraudulent transfer laws.

Global Wealth Protection specializes in guiding individuals through this intricate process, from initial consultations to setting up offshore companies and trusts. Their GWP Insiders membership program provides ongoing support, offering strategies for internationalization, tax optimization, and jurisdiction selection. Idaliz H. Guiraud, Managing Partner at Guiraud Law, emphasizes this shift in wealth management:

The offshore world has matured from opacity to optionality, a shift that rewards transparency, foresight, and diversification. In the coming decade, wealth management will be defined less by secrecy and more by sovereignty.

The resilience of your portfolio hinges on the steps you take today. By diversifying your assets, spreading your holdings across jurisdictions and currencies, and planning ahead, you can secure your financial future. In an unpredictable world, preparation is the ultimate advantage.

FAQs

How much should I invest outside the U.S.?

The portion of your investments allocated outside the U.S. hinges on your personal goals for diversification and how much risk you’re comfortable taking. Experts often suggest dedicating 35% to 55% of your equity portfolio to international assets. This strategy can help balance your portfolio by lowering volatility while tapping into opportunities across global markets.

What must I report to the IRS if I go offshore?

U.S. taxpayers are required to report foreign financial accounts if their total value exceeds $10,000 at any point during the year. This involves submitting FinCEN Form 114 (FBAR) electronically. On top of that, taxpayers may also need to file Form 8938 if their foreign assets go over certain thresholds. These requirements are in place to ensure alignment with IRS regulations.

Do I need an offshore trust, an LLC, or both?

Choosing between an offshore trust, an LLC, or both comes down to your specific asset protection goals. Offshore trusts are known for their strong confidentiality, shielding assets from creditors, and offering estate planning advantages. On the other hand, U.S.-based LLCs provide liability protection and flexible tax options.

For a more secure setup, combining the two can be highly effective. The LLC works to protect assets within the U.S., while the offshore trust adds an extra layer of international protection. To figure out the right strategy for your situation, it’s best to consult with a qualified professional.