When you invest internationally, tax treaties can help you avoid paying taxes twice on the same income. These agreements, known as Double Tax Agreements (DTAs), clarify which country can tax specific types of income and often reduce tax rates for cross-border investors. Here’s what you need to know:

- What They Are: Tax treaties are agreements between two countries that prevent double taxation on income like dividends, interest, and business profits.

- Key Benefits: They lower withholding tax rates, provide tax credits or exemptions, and ensure legal clarity for international investors.

- How They Work: Treaties allocate taxing rights, establish rules for permanent establishments (PEs), and include provisions to prevent tax abuse.

- Important Documents: Forms like W-8BEN, W-8BEN-E, and Form 8833 are essential for claiming treaty benefits.

Understanding these treaties is crucial for keeping more of your investment earnings while staying compliant with tax laws. Always check treaty details and file the right documentation to avoid penalties.

How Tax Treaties Prevent Double Taxation

Tax treaties work through three key mechanisms to ensure you’re not taxed twice on the same income. These treaties allocate taxing rights between countries, provide relief methods to avoid double taxation, and reduce withholding rates on certain types of income. Let’s break down how these processes work, starting with the allocation of taxing rights.

How Taxing Rights Are Allocated

Tax treaties establish clear rules about which country can tax specific types of income, such as dividends, interest, royalties, or business profits. These rules are reciprocal, meaning they apply equally to both countries in the treaty. For instance, a treaty might specify that business profits are taxable only in the country where the business operates, unless the company has a permanent establishment in the other country.

Most U.S. treaties also include a "saving clause", which allows the U.S. to tax its citizens and residents on their worldwide income, even if the treaty allocates taxing rights to another country.

Two Methods for Eliminating Double Taxation

Tax treaties provide two primary methods to avoid taxing the same income twice: the credit method and the exemption method.

- The Credit Method: This approach is commonly used by U.S. taxpayers. First, you pay taxes to the foreign country where the income is earned. Then, you can claim a Foreign Tax Credit on your U.S. tax return, offsetting your U.S. tax liability by the amount already paid abroad. Individuals use Form 1116, while corporations use Form 1118 to claim this credit. However, the credit is limited to the reduced tax rate specified in the treaty. If you pay more than the treaty rate, you’ll need to request a refund from the foreign country, as the excess cannot be claimed as a U.S. credit. The IRS clarifies:

"If you are entitled to a reduced rate of foreign tax based on an income tax treaty between the United States and a foreign country, only that reduced tax qualifies for the [Foreign Tax] credit."

- The Exemption Method: Under this method, specific foreign income is excluded from U.S. taxable income altogether, as outlined in certain treaty provisions. This means you only pay tax in the country where the income originates, with no U.S. tax liability on that income.

Reduced Withholding Tax Rates

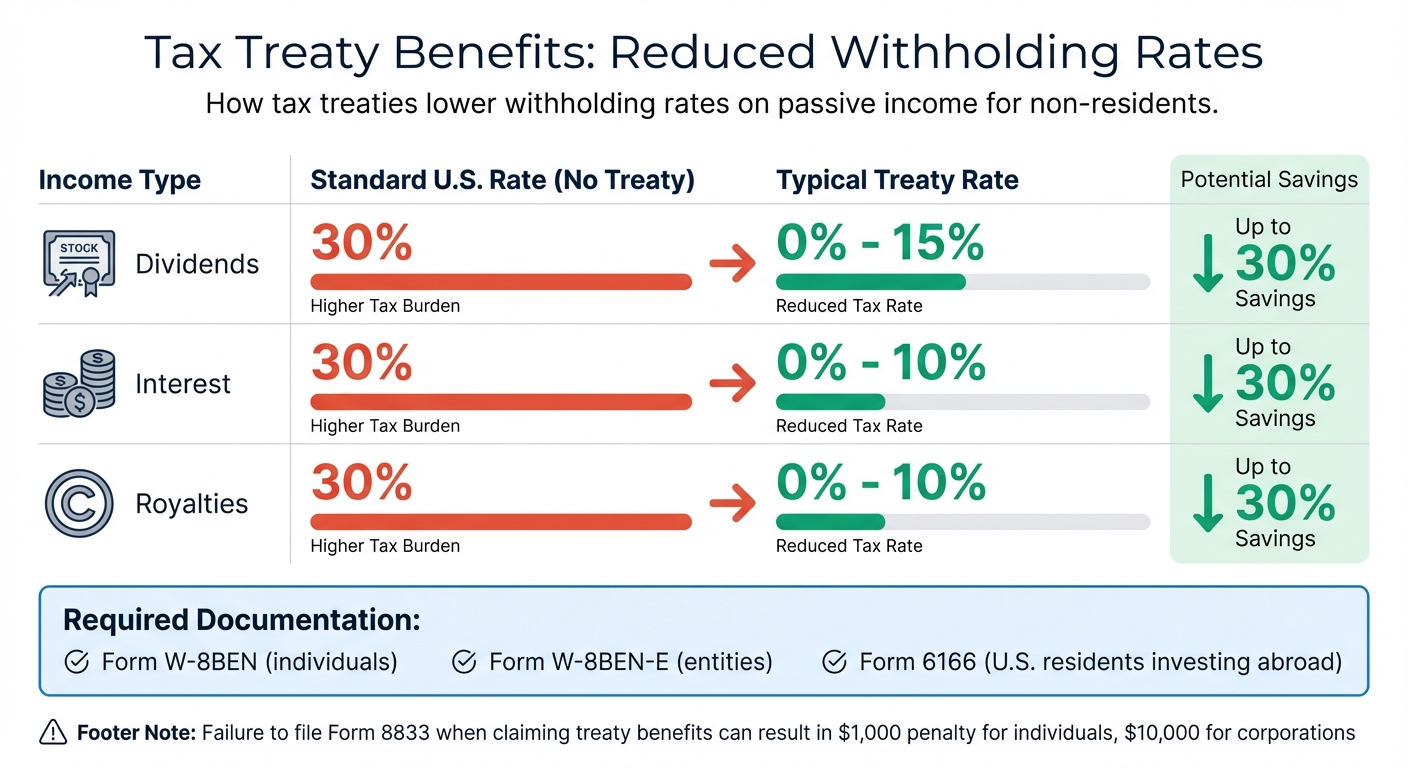

Another benefit of tax treaties is reduced withholding rates on passive income earned by non-residents. Without a treaty, the standard U.S. withholding rate is 30% on dividends, interest, and royalties. Treaties often lower these rates significantly, sometimes to as little as 0%, depending on the type of income and the treaty terms.

| Income Type | Standard U.S. Rate | Typical Treaty Rate |

|---|---|---|

| Dividends | 30% | 0% – 15% |

| Interest | 30% | 0% – 10% |

| Royalties | 30% | 0% – 10% |

To qualify for these reduced rates, proper documentation is essential. U.S. residents investing abroad may need Form 6166 (U.S. Residency Certification) to prove their status to foreign tax authorities. Foreign investors in U.S. assets typically submit Form W-8BEN (for individuals) or W-8BEN-E (for entities) to the withholding agent.

If you claim treaty benefits that override standard tax rules, you’re required to attach Form 8833 (Treaty-Based Return Position Disclosure) to your tax return. Failure to disclose these benefits can result in a $1,000 penalty per violation. Additionally, if you later discover you overpaid foreign taxes, you generally have up to 10 years to file an amended return and claim a refund.

sbb-itb-39d39a6

Important Tax Treaty Provisions for Investors

Tax treaties often include clauses that can significantly influence how you structure and manage investments across borders. Below, we break down key provisions that investors should be familiar with.

Permanent Establishment (PE) Rules

Permanent establishment (PE) rules help determine whether your foreign business activities create a taxable presence in another country. A PE typically involves a fixed business location, such as an office, branch, or warehouse. Additionally, an Agency PE can arise if a dependent agent regularly concludes contracts on your behalf.

However, many treaties carve out exceptions for preparatory or ancillary activities, like storing inventory, which generally won’t trigger taxable presence.

For construction or service contracts, PE status may apply if the project exceeds a specific duration – usually six months to a year, depending on the treaty. If you’re managing such projects abroad, it’s crucial to monitor these timelines closely to avoid unexpected tax liabilities.

Information Exchange Provisions

Modern tax treaties often include mechanisms for governments to share financial information about taxpayers. These agreements, known as Tax Information Exchange Agreements (TIEAs), empower authorities to verify income declarations and ensure treaty benefits are claimed correctly. While they’re designed to combat tax evasion, they also help legitimate investors secure treaty protections.

The push for mandatory information sharing has gained momentum globally. Over 100 jurisdictions have signed the Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS, creating a network of more than 3,000 tax treaties worldwide. By January 2026, Fiji had joined as the 152nd signatory. For investors, this means tax authorities now have advanced tools to scrutinize cross-border transactions and residency claims.

Anti-Abuse Provisions and BEPS Reforms

To maintain compliance and efficiency in global investments, understanding anti-abuse measures is vital. These provisions aim to prevent treaty shopping – where investors route their activities through jurisdictions with favorable tax rates.

The OECD’s Base Erosion and Profit Shifting (BEPS) Project has established baseline standards to counter such practices. According to the OECD:

"The BEPS MLI offers concrete solutions to close gaps in existing tax treaty tax rules and to implement agreed minimum standards to counter treaty abuse and to improve dispute resolution mechanisms."

One significant reform is the Subject to Tax Rule (STTR). This rule allows developing countries to tax certain intra-group payments if they are subject to low corporate tax rates in the recipient’s jurisdiction. It’s designed to prevent profit-shifting to low-tax countries through artificial arrangements.

The U.S. has also taken steps to address treaty abuse. For instance, it terminated its treaty with Hungary effective January 1, 2024, and suspended key provisions of the U.S.-Russia treaty as of August 16, 2024. These moves highlight the need for ongoing vigilance, as treaty networks can change rapidly.

To comply with anti-abuse provisions, taxpayers must disclose treaty-based positions on their returns. The IRS emphasizes this requirement:

"If you take the position that any U.S. tax is overruled or otherwise reduced by a U.S. treaty (a treaty-based position), you must generally disclose that position on your affected return."

Failing to file Form 8833 when required can lead to penalties: $1,000 for individuals and $10,000 for corporations. Even if no tax is owed, the disclosure is mandatory if you’re claiming treaty benefits that override standard tax rules.

How to Use Tax Treaties for Global Investments

To make the most of international tax treaties, it’s important to follow a few key steps. These include identifying applicable treaties, meeting residency and documentation requirements, and structuring your investments effectively.

Finding Applicable Treaties

Start by confirming whether a tax treaty exists between the U.S. and the country where you plan to invest. The IRS offers a detailed "United States Income Tax Treaties – A to Z" list covering all active agreements. For a quick breakdown of reduced tax rates or exemptions by country, check out IRS Publication 901.

Once you’ve identified a treaty, verify its current status. For example, the U.S.-Chile treaty became effective for withholding taxes on February 1, 2024. On the other hand, the U.S.-China treaty does not extend to Hong Kong, so treaty benefits won’t apply to investments in that region.

For further clarity, refer to Table 3 in the IRS Tax Treaty Tables. This resource provides effective dates and outlines any updates or protocols to existing treaties. If you need to dive deeper, the U.S. Department of the Treasury publishes full treaty texts along with Technical Explanations that detail how specific provisions work in practice. Pay special attention to the Limitation on Benefits (LOB) article in each treaty. This section lays out the tests you need to pass to qualify for benefits and prevents misuse of the treaty.

Once you’ve confirmed the treaty’s existence and status, focus on meeting the residency and documentation requirements to claim your benefits.

Meeting Residency and Documentation Requirements

To access treaty benefits, you’ll need to prove residency in the treaty country and beneficial ownership of the income. Submit the correct forms to the withholding agent before payment to ensure reduced withholding rates. Use Form W-8BEN if you’re an individual or Form W-8BEN-E if you’re an entity. You’ll also need to provide a U.S. Taxpayer Identification Number (SSN or ITIN) or a foreign TIN.

If you’re claiming treaty benefits as a U.S. resident in a foreign country, file Form 8802 to request Form 6166, which serves as official proof of U.S. tax residency. When a treaty reduces your tax liability – such as for U.S. real property gains or changes in income source – you must disclose this by filing Form 8833 with your tax return. Failing to disclose can lead to penalties of $1,000 for individuals and $10,000 for corporations.

| Form Number | Purpose | Who Uses It |

|---|---|---|

| W-8BEN | Certify foreign status for withholding on dividends, interest, royalties | Foreign Individuals |

| W-8BEN-E | Certify entity status for withholding on income | Foreign Entities |

| 8833 | Disclose treaty-based return positions | Any taxpayer claiming treaty benefits |

| 8802 | Request U.S. Residency Certification (Form 6166) | U.S. Residents claiming benefits abroad |

Structuring Investments Across Multiple Countries

Once you’ve met the residency and documentation requirements, focus on structuring your investments to maximize treaty benefits while minimizing unintended tax liabilities.

To avoid creating a taxable permanent establishment in the source country, carefully structure your cross-border investments. Ensure that your investment entities meet the LOB provisions, including resident ownership thresholds.

If you’re a resident of two countries, the treaty’s tie-breaker provisions will determine which country has primary taxing rights. However, U.S. citizens and residents should be aware that most U.S. treaties include a saving clause. This clause allows the U.S. to tax worldwide income, regardless of treaty benefits, with only a few exceptions.

Finally, check for state tax compliance. Some states do not honor federal treaty provisions, so it’s important to account for any state-level tax obligations.

Conclusion: Using Tax Treaties to Optimize Your Investment Strategy

International tax treaties can be a powerful way to reduce your global tax obligations, but they demand careful planning and attention to detail. By understanding how these treaties divide taxing rights and offer reduced withholding rates, you can retain more of your investment earnings while staying compliant with U.S. and international tax laws.

Success hinges on being proactive. Before diving into any cross-border investments, confirm the applicable treaty terms, as they can change frequently. Additionally, make sure to file the necessary disclosure forms to avoid costly penalties.

These steps are essential for taking full advantage of treaty benefits. Keep in mind that these advantages work both ways. Just as foreign investors can benefit from reduced rates on U.S.-sourced income, you can tap into similar opportunities for your investments abroad. That said, the "saving clause" in most U.S. treaties means you’ll still owe U.S. taxes on your worldwide income, though foreign tax credits can help offset the risk of double taxation.

Don’t overlook state-level compliance. Even if federal treaty benefits apply, some states may not recognize them, potentially leading to unexpected tax liabilities. Staying informed about treaty updates and anti-abuse provisions will help you maintain a tax-efficient global portfolio while meeting all legal requirements. Regularly reviewing and adjusting your strategy ensures it remains effective as treaty terms evolve.

FAQs

Do I still owe U.S. tax if a treaty reduces foreign taxes?

Even if a tax treaty reduces the amount of foreign taxes you owe, you’re still responsible for paying U.S. taxes on your income. The good news? You might be eligible for a foreign tax credit or other treaty-related benefits to help ease the burden of double taxation. It’s important to carefully review the treaty provisions that apply to your situation and consult reliable resources to determine your eligibility.

When do I have to file Form 8833 for treaty benefits?

If you’re claiming treaty benefits that alter or override U.S. tax law, you’ll need to file Form 8833. This form is used to disclose treaty-based positions on your tax return. Be sure to carefully review the filing requirements to stay compliant with U.S. tax regulations.

How can I avoid creating a permanent establishment abroad?

To steer clear of creating a permanent establishment (PE) in another country, it’s crucial to structure your business activities carefully. Make sure they don’t align with the criteria set out in relevant tax treaties or local laws.

Key steps include avoiding a fixed place of business and refraining from using dependent agents to finalize contracts on your behalf. Instead, stick to activities that are considered preparatory or auxiliary in nature. Familiarize yourself with how PE is defined in applicable treaties, and maintain clear documentation of your operations to show that no taxable presence has been established.