Want to manage your taxes better and protect your wealth? Diversifying your tax residency is a legal strategy that helps reduce tax burdens, safeguard assets, and increase global mobility. Here’s why it matters:

- Tax Savings: Countries like the UAE and Panama offer low or zero personal income tax rates.

- Wealth Protection: Spreading assets across multiple jurisdictions reduces exposure to local risks like sudden tax hikes or political instability.

- Flexibility: Multiple residencies provide options for living, working, and traveling internationally.

- Avoid Double Taxation: Proper planning and treaties can prevent being taxed twice on the same income. This includes understanding how tax residency and CRS impact your global accounts.

This approach isn’t about evasion – it’s about using international laws to your advantage. Learn how to pick the right jurisdictions, set up legal structures, and manage your tax obligations while optimizing your financial setup.

Risks of Relying on a Single Tax Jurisdiction

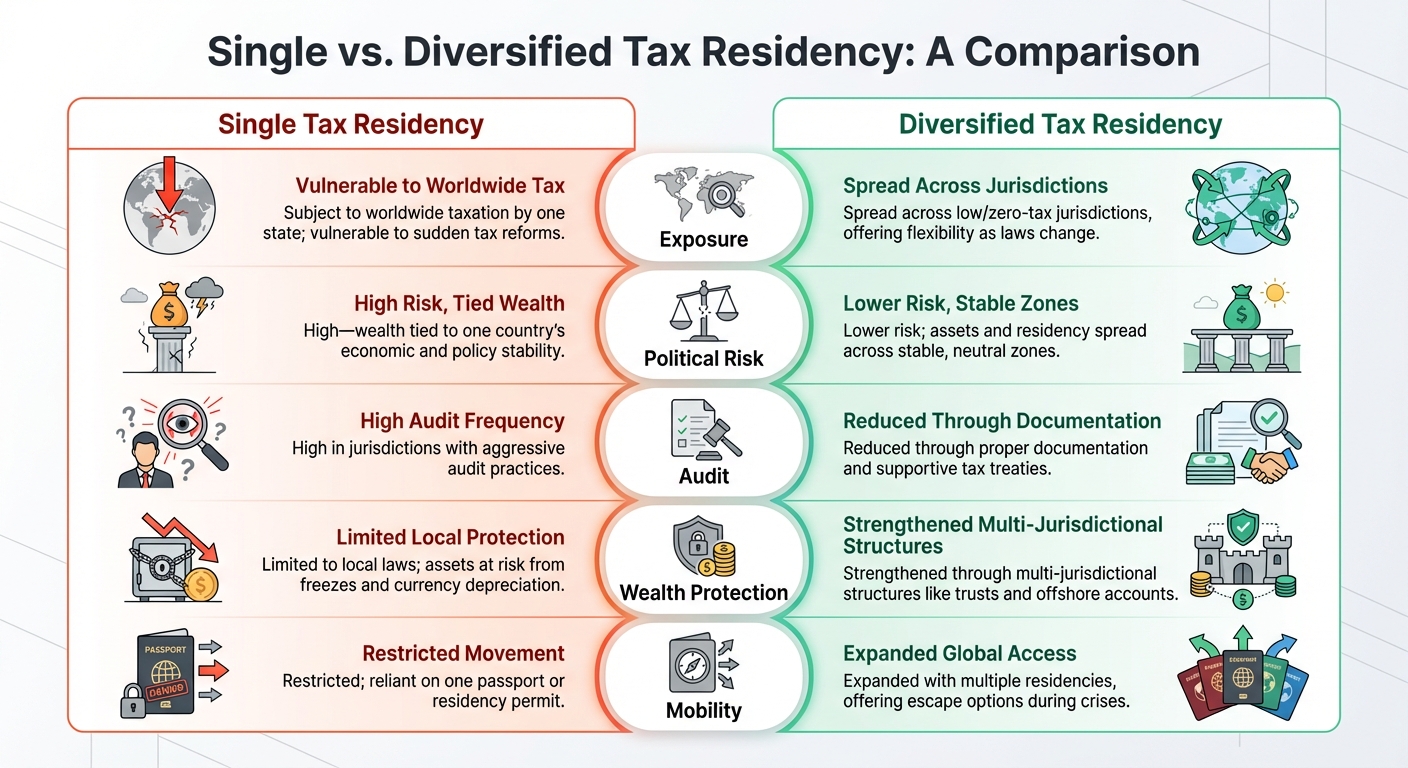

Single vs Diversified Tax Residency Comparison

Depending on just one tax jurisdiction can leave you exposed to serious risks. A sudden change in tax policies could force you to act quickly, often with limited alternatives.

Unpredictable Tax Law Changes

Tax laws can change without warning, throwing even the best-laid plans into chaos. For instance, in 2024, the UK government announced the elimination of its long-standing non-domicile tax regime. This decision jeopardized family wealth that had been built over generations. Peter Ferrigno, Director of Tax Services at Henley & Partners, described the uncertainty:

"Calculating the hidden cost of expensive or unpredictable tax policy is like trying to find the proverbial dog that didn’t bark – how do you know which investment projects didn’t materialize because investors felt that moving to that country would put family wealth accumulated over generations at risk to the whims of a government that may not be around for long…?"

Sudden policy shifts like the OECD‘s Pillar Two minimum tax framework can also disrupt carefully crafted tax strategies. In another example, Switzerland narrowly avoided a referendum that would have introduced one of the highest inheritance tax rates globally, a move that could have damaged its reputation for fiscal stability. These changes aren’t just theoretical – they can force wealthy individuals to relocate quickly to safeguard their assets.

Economic and Political Instability

Tying your tax residency to one country also exposes your wealth to that nation’s economic and political environment. Issues like currency depreciation, inflation, and policy shifts can quietly erode your purchasing power, often going unnoticed until it’s too late. Samuel Grange, an International Asset Protection Lawyer, puts it succinctly:

"Jurisdictional diversification isn’t about panic. It’s about pacing. It’s about being one step ahead, so you don’t have to run."

Concerns over instability are driving a growing number of millionaires to relocate. By 2026, around 165,000 millionaires are expected to move internationally. In 2025 alone, the UAE welcomed a net inflow of nearly 10,000 millionaires, while Singapore is projected to gain between 1,800 and 2,300 high-net-worth individuals in 2026.

This instability often leads to stricter tax audits. High-tax jurisdictions like New York State aggressively target high earners, conducting over 3,500 residency audits annually. About half of those audited fail, with unsuccessful cases resulting in average assessments of $100,000 or more in back taxes, interest, and penalties. When you’re tied to a single jurisdiction with a combined tax rate of 15% (NYC + NYS), your ability to adapt is limited.

Single vs. Diversified Tax Residency: A Comparison

| Feature | Single Tax Residency | Diversified Tax Residency |

|---|---|---|

| Exposure | Subject to worldwide taxation by one state; vulnerable to sudden tax reforms. | Spread across low/zero-tax jurisdictions, offering flexibility as laws change. |

| Political Risk | High – wealth tied to one country’s economic and policy stability. | Lower risk; assets and residency spread across stable, neutral zones. |

| Audit | High in jurisdictions with aggressive audit practices. | Reduced through proper documentation and supportive tax treaties. |

| Wealth Protection | Limited to local laws; assets at risk from freezes and currency depreciation. | Strengthened through multi-jurisdictional structures like trusts and offshore accounts. |

| Mobility | Restricted; reliant on one passport or residency permit. | Expanded with multiple residencies, offering escape options during crises. |

This comparison highlights how spreading your tax residency across multiple jurisdictions can protect against sudden regulatory changes and economic instability.

Borders, once seen as a safeguard, can now act as barriers to financial freedom. Even digital nomads aren’t immune – working in a co-working space abroad for just a few months could trigger corporate tax obligations in that country. These risks underline the importance of diversifying your tax residency as we explore strategies and jurisdictions for achieving this flexibility.

sbb-itb-39d39a6

Benefits of Diversifying Your Tax Residency

Diversifying your tax residency can help you create a financial setup that’s more efficient, secure, and adaptable.

Lower Tax Obligations

One of the main advantages of diversifying your tax residency is the potential to legally reduce your tax burden. Countries with territorial tax systems, such as Hong Kong, Singapore, and Panama, only tax income earned within their borders. This means foreign-sourced income, capital gains, and dividends often go untaxed. For instance, Hong Kong’s personal income tax rates range from 2% to 17%, with a corporate tax rate of 16.5%. Similarly, Singapore offers personal tax rates between 0% and 20% and a corporate tax rate of 17%. Compare this to high-tax countries where combined rates can exceed 50%, and the difference becomes clear.

Relocation to certain jurisdictions can also eliminate specific taxes altogether. The UAE, for example, has no personal income or capital gains tax, while Monaco doesn’t impose personal income tax on residents. By establishing tax residency in these places, you can avoid inheritance, estate, gift, and wealth taxes that might otherwise take a significant chunk of your assets.

"With the right immigration strategy, changing tax residence often proves to be the most efficient and effective method to handling tax burdens in the long run." – Harvey Law Group

Double tax treaties add another layer of benefit, ensuring that the same income isn’t taxed twice. With careful planning, you can earn income in one jurisdiction, hold assets in another, and live in a third – all while staying compliant and minimizing your tax exposure.

But beyond tax savings, diversifying residency offers added protection for your wealth.

Better Asset Protection and Wealth Distribution

Spreading your assets across multiple jurisdictions with distinct legal frameworks helps reduce risk and protect your wealth from local economic crises or aggressive legal claims.

Structures like offshore LLCs, trusts, and foundations not only provide legal protection but can also offer tax advantages. A smart banking setup is equally important. This might include a local account for daily needs, a tax residency account for business dealings, and an international account in a financial hub like Switzerland or Singapore for long-term asset preservation. This approach ensures no single government or banking system has control over your entire financial portfolio.

"True financial privacy isn’t about hiding – it’s about structuring your wealth so that it remains secure, compliant, and beyond the reach of unnecessary risk." – Project Black Ledger

However, compliance is key. Over 100 countries participate in the Common Reporting Standard (CRS), which facilitates the automatic exchange of financial information. To defend your tax residency structure, you’ll need to demonstrate genuine substance, like maintaining local office space, appointing directors, and documenting business activities.

Greater Lifestyle and Travel Freedom

Beyond financial benefits, diversifying your tax residency offers greater personal freedom. Multiple residencies act as a safeguard against instability, giving you options if political unrest, economic challenges, or government actions disrupt your home country. This ensures you’re not entirely dependent on one country’s systems, regulations, or currency.

Take passports as an example. A Portuguese passport ranks as one of the strongest globally, offering visa-free travel to 191 countries, while a Singaporean passport grants access to 195 countries. This kind of mobility opens doors to new business ventures, international partnerships, and expanded market access.

You can also establish a "lifestyle base" in a country with a high quality of life while keeping your tax residency elsewhere. EU residency programs in Portugal, Greece, and Malta, for instance, grant full mobility within the Schengen Area.

"True mobility isn’t about passports – it’s about positioning yourself where capital, opportunities, and influence intersect." – Project Black Ledger

This flexibility extends to business as well. Relocating your residency allows you to optimize where you live, work, and bank. For example, a tech executive moving to Singapore could lower the tax rate on equity compensation from 37% to about 22%. This isn’t about avoiding taxes – it’s about structuring your finances intelligently to stay compliant while safeguarding your assets.

Best Jurisdictions for Tax Residency Diversification

When considering the advantages of diversified tax residency, picking the right jurisdiction is a vital step. The ideal choice depends on your income, lifestyle, and long-term plans, requiring a balance between tax benefits, travel flexibility, and overall quality of life. Let’s break down four standout options that consistently appeal to globally mobile individuals.

Portugal

Portugal’s tax framework saw a major shift on January 1, 2024, when the Non-Habitual Resident (NHR) program closed to new applicants. It was replaced by the Tax Incentive for Scientific Research and Innovation (IFICI), which offers a 20% flat tax rate on qualifying income for 10 years. The popular Golden Visa program remains, requiring a minimum contribution of €250,000 (about $271,000) through donation or €500,000 (about $542,000) via investment funds. Citizenship becomes an option after five years. Portugal ranks 3rd globally in the 2026 Global Residence Program Index.

"Residence and citizenship rights are increasingly assembled rather than inherited – structured portfolios of access rights built to create resilience across generations." – Dominic Volek, Group Head of Private Clients, Henley & Partners

United Arab Emirates

The UAE has solidified its reputation as a wealth-friendly destination, rising to joint 2nd place in the 2026 Global Residence Program Index. Known for its zero tax regime, the UAE offers the Golden Visa program, which requires a minimum property investment of AED 2 million (about $545,000). This program grants long-term residence with the freedom to live across all seven emirates. The UAE also serves as a strategic hub connecting Africa, the Middle East, Asia, and Europe, with visa-free access to other GCC nations. Its appeal is particularly strong for business owners and investors seeking world-class infrastructure, top international schools, and a streamlined permit system.

"The UAE has firmly established itself as the leading destination for millionaires on the move and is positioning itself as a durable hub for asset management and wealth preservation." – Dr. Juerg Steffen, CEO, Henley & Partners

Anguilla

Anguilla is a standout choice for its zero tax on global income. With no capital gains, inheritance, or wealth taxes, it’s an ideal jurisdiction for asset protection and long-term wealth management. The physical presence requirements are minimal, offering maximum flexibility for high mobility individuals. Anguilla is particularly attractive for those setting up offshore LLCs, trusts, or private interest foundations. Its legal system emphasizes privacy and asset protection, making it a streamlined option for safeguarding wealth.

Malaysia

Malaysia’s My Second Home (MM2H) program continues to draw digital nomads and retirees, earning a 12th-place ranking in the 2026 Global Residence Program Index. Malaysia operates on a territorial tax system, meaning only local income is taxed, leaving foreign-sourced income untouched. The MM2H program offers long-term visas with lower financial thresholds compared to European alternatives. With an English-speaking population, modern infrastructure, and a prime location in the Asia-Pacific region, Malaysia is a practical choice for individuals with international income streams.

The table below highlights key features of these jurisdictions, helping you compare their unique benefits:

| Jurisdiction | Tax Advantage | Minimum Investment | Path to Citizenship | 2026 Global Rank |

|---|---|---|---|---|

| Portugal | 20% flat rate (IFICI) for 10 years | €250,000–€500,000 | 5 years | 3rd |

| UAE | Zero personal income/capital gains tax | AED 2M (≈$545,000) | Long-term residence | 2nd |

| Anguilla | Zero tax on global income | Varies by structure | Not applicable | Not ranked |

| Malaysia | Territorial taxation only | MM2H program | Long-term naturalization | 12th |

Each jurisdiction shines in its own way. Portugal offers EU access and a clear citizenship path. The UAE provides a tax-free business hub with global connectivity. Anguilla emphasizes asset protection with minimal obligations, while Malaysia delivers affordability and territorial taxation ideal for remote income earners. The best choice depends on your income structure, travel habits, and the physical presence you’re willing to maintain.

Next, explore how to put these strategies into action.

How to Diversify Your Tax Residency

Diversifying your tax residency can be an effective way to manage tax obligations and safeguard wealth, but it requires careful planning and expert guidance to avoid missteps. This process generally unfolds in three stages: Strategic Planning (lasting about 2–3 months), Structural Implementation (3–4 months), and Continuous Refinement. Each phase demands precision and compliance with international regulations. Here’s a step-by-step guide to help you navigate this strategy effectively.

Review Your Current Tax Residency

Begin by assessing your existing financial and legal connections. This includes bank accounts, property leases, utility bills, and travel records. Tax authorities don’t just rely on day-counts; they evaluate your center of vital interests, which includes family relationships, economic ties, and business activities. To demonstrate a legitimate relocation, keep detailed documentation such as travel records, entry/exit stamps, and utility bills. These records can help establish your residence in a new jurisdiction.

For U.S. citizens, it’s important to note that you are taxed on worldwide income. Achieving complete tax relief often requires formal expatriation, which is a significant decision.

Choose the Right Jurisdictions

Selecting the right jurisdictions is key to aligning your tax residency with your income, lifestyle, and future goals. A useful approach is the 3-Jurisdiction Model, which involves:

- Residency base: Your primary legal tax home.

- Business hub: The location where your company operates.

- Asset layer: Where your wealth is stored.

For example, a tech executive might choose Singapore as their residency base for its favorable treatment of equity compensation, while using Dubai as a business hub for flexibility in trading. This setup can help minimize overall tax liabilities.

Additionally, check for Controlled Foreign Corporation (CFC) rules in your home country. Understanding whether your target jurisdiction uses a territorial tax system (taxing only local income) or a worldwide system is also crucial.

"The best residency strategy isn’t just about where you can go – it’s about where your wealth, business, and legacy can thrive." – Project Black Ledger

Once you’ve selected your jurisdictions, the next step is to establish the necessary legal and financial frameworks.

Set Up Legal and Financial Structures

To establish a legitimate presence, you’ll need to create tangible ties in your chosen jurisdiction. This includes leasing office space, hiring local staff, and ensuring that key decisions, such as board meetings, are conducted locally. Obtaining a Tax Residency Certificate (TRC) from your primary base each year is critical for providing proof to banks and tax authorities. Supporting documents like local leases, utility bills, and bank accounts further strengthen your case.

It’s also wise to establish banking relationships before moving. Many jurisdictions require proof of current residency or evidence of genuine business operations to open accounts. Keeping thorough records can help you avoid risks related to permanent establishment.

Work with Professionals

The complexities of international tax laws make professional advice indispensable. Cross-border tax experts can help you structure your transition, address challenges like CFC rules, and mitigate risks related to permanent establishment. Organizations like Global Wealth Protection offer consultations and membership programs tailored to entrepreneurs and investors, ensuring compliance while implementing these strategies.

"Flag Theory is not about tax evasion or illegal financial activities; it is about legally structuring finances and residency in a way that maximizes benefits while complying with international laws." – OCBF Consulting

Conclusion

Setting up diverse tax residencies acts as a safeguard against economic shifts, political turbulence, and abrupt tax law changes. By establishing residency, managing business operations, and holding assets across various jurisdictions, you can legally lower tax liabilities, protect your wealth from heavy-handed government policies, and enjoy the flexibility to live and work in places that align with your lifestyle and financial priorities.

Looking ahead to 2026, economic substance rules require more than just spending a certain number of days in a country. Establishing legitimate local connections – such as opening bank accounts, securing leases, paying utility bills, and conducting verifiable business activities – is essential to meet tax authority requirements. Whether you’re drawn to the UAE’s 0% personal income tax, Portugal’s appealing lifestyle, or the advantages of territorial tax systems, your approach needs to align with your actual business operations and personal circumstances.

Industry leaders emphasize this point:

"The best residency strategies don’t just save taxes – they unlock new business, banking, and generational wealth opportunities." – Project Black Ledger

Navigating international tax laws, CRS reporting, and risks tied to permanent establishments demands expert advice. Complexities like varying treaties, residency rules, and exit taxes can lead to unforeseen liabilities. Working with skilled cross-border tax advisors ensures your strategy is both compliant and effective.

Organizations such as Global Wealth Protection specialize in guiding entrepreneurs and investors through these intricate processes. With proper planning, thorough documentation, and expert input, you can create a diversified tax residency setup that supports global mobility and safeguards your wealth for the long term. This approach not only protects your financial future but also positions you to seize opportunities worldwide.

FAQs

How do I prove my new tax residency?

To establish your new tax residency, you’ll need to present documents that demonstrate your physical presence, connections, and intent to live in the new location. Key pieces of evidence include a driver’s license, voter registration, and records of the time spent in the area.

You can further support your claim with additional proof, such as financial ties, property ownership, or lease agreements. Consistency is crucial – make sure your actions and documentation clearly reflect your declared residency to reduce the risk of disputes or audits.

Can I have more than one tax residency at once?

Yes, it’s possible to be considered a tax resident in more than one country at the same time. This happens when the laws of multiple countries and your personal situation align in a way that classifies you as a tax resident in each. Known as dual or multiple tax residency, this typically depends on factors such as how much time you spend in each country, your financial connections, and the specific rules of each jurisdiction.

What mistakes trigger residency audits or double tax?

Mistakes that can trigger residency audits or even double taxation often include spending too much time in one country, not keeping thorough travel and income records, misunderstanding tax treaties, or maintaining strong financial or personal connections in multiple places. These missteps can catch the attention of tax authorities, leading to closer examination of your residency status and potentially resulting in compliance headaches or unplanned tax bills.