Relocating abroad means your insurance needs will change significantly. Many expats mistakenly assume their domestic policies will cover them overseas, but most don’t. Medicare, for example, offers no coverage abroad except in rare emergencies near U.S. borders. Without proper insurance, you risk massive out-of-pocket expenses – emergency medical evacuations alone can exceed $100,000.

Here’s what you need to know to secure the right coverage:

- Health Insurance: Domestic plans don’t work abroad. International health insurance offers broader, portable coverage for routine care, emergencies, and chronic conditions across multiple countries. Look for plans with direct billing, high annual limits (at least $1M), and portability to avoid re-underwriting when relocating.

- Liability Insurance: Protects against lawsuits for accidental injury or property damage. Global liability coverage is essential for expats, as U.S. policies rarely apply overseas.

- Property Insurance: Covers belongings and homes abroad. Includes risks like theft, fire, and natural disasters. Check for transit coverage during moves and exclusions for vacant properties.

Key tips: Always disclose pre-existing conditions, confirm your policy’s geographical scope, and test the insurer’s 24/7 support. For comprehensive financial protection, pair insurance with asset management tools like trusts or LLCs.

The right insurance ensures you’re prepared for health, legal, and financial challenges abroad. Don’t leave gaps in your coverage.

Health Insurance with International Coverage

If you’re traveling or living abroad, you might be surprised to learn that most U.S. health insurance plans don’t cover you outside the country. That’s where international health insurance comes in. Unlike travel insurance, which mainly handles emergencies, international health insurance offers broader medical coverage across multiple countries.

Coverage Across Multiple Countries

International health insurance works on a tiered system, offering options like "Worldwide", "Worldwide excluding USA", or coverage tailored to specific regions. This means you’re covered whether you need routine checkups in Singapore or urgent care in Spain. Unlike domestic plans, these policies ensure uninterrupted protection no matter where you go.

The costs of healthcare abroad can be staggering. For instance, a cardiac bypass in Singapore might set you back $180,000, while annual cancer treatments in Europe can exceed $300,000. To safeguard yourself, experts suggest a minimum annual coverage of $1,000,000. Be cautious of policies with hidden sub-limits – a plan might boast a $2 million cap but restrict critical treatments like cancer care to just $50,000.

"A robust direct-billing network is your shield against financial shock. It transforms a potentially catastrophic out-of-pocket expense into a manageable administrative process handled by your insurer." – ExpatInsurance.com

Direct billing is a lifesaver. It allows your insurer to pay hospitals directly, sparing you from hefty upfront costs (often around $20,000) and long reimbursement waits. Before signing up, check the insurer’s provider directory and confirm with hospitals in your target area that they accept direct billing.

Another key feature to review is policy portability, ensuring your coverage stays intact as you move across borders.

Policy Portability Between Jurisdictions

A good international health insurance plan doesn’t just cover you globally – it also moves with you. Policy portability ensures you don’t face re-underwriting when relocating, which could otherwise result in new exclusions for conditions diagnosed during your previous coverage period. For example, if you develop diabetes in Thailand and later move to Germany, a portable plan continues to cover your condition without new restrictions.

"Portable health insurance avoids [underwriting issues] because you don’t have to undergo the underwriting process again when moving abroad. Your coverage stays intact, ensuring continuous coverage of any medical condition that may have arisen during your coverage period." – APRIL International

It’s also worth checking your policy’s home country limits, as many plans cap visits to your home country at 90 days per year. Additionally, confirm that your destinations aren’t excluded due to risks like political instability or war.

If you don’t anticipate needing care in the U.S., opting for "Worldwide excluding USA" coverage can reduce premiums by 30% to 50%. This makes financial sense, considering the U.S. accounts for 40% of global health insurance premiums and has the highest average individual costs – $15,296 per year compared to $3,900 in Poland or $5,485 in Mexico.

Pre-Existing Conditions and Mental Health Coverage

Once you’ve secured broad and portable coverage, it’s time to focus on pre-existing conditions and mental health care. International plans don’t automatically cover pre-existing conditions. Insurers generally use one of two approaches:

- Full Medical Underwriting (FMU): Requires a detailed health history to avoid gaps in coverage.

- Moratorium Underwriting: Skips the questionnaire but excludes conditions from the past 2–5 years until you’ve been symptom- and treatment-free for about 24 months.

Always disclose pre-existing conditions to avoid voiding your policy. Some insurers might cover conditions deemed "stable" (no symptoms or treatment changes) for 6–12 months, while others may charge extra or exclude them permanently.

Mental health coverage is becoming a standard part of comprehensive international plans, covering both inpatient and outpatient care. Many plans now offer 24/7 telehealth access to licensed doctors and mental health professionals via apps – a convenient feature when navigating language barriers or time zones.

For those planning a family, note that pregnancy is often treated as a pre-existing condition. Most plans enforce a waiting period of 10–24 months before maternity benefits kick in, and coverage won’t apply if you’re already pregnant when you apply. Planning ahead is key.

Liability Insurance for International Risks

Living abroad comes with legal and financial risks that your U.S. home insurance likely doesn’t address. Personal liability insurance acts as a safeguard, protecting your assets if you accidentally cause injury to someone or damage their property. This type of insurance ensures compensation goes directly to the injured party, sparing you from potentially draining your savings over a single mishap.

"Liability insurance protects you if you are held responsible for injuring someone else or damaging their property. Instead of paying benefits to you, it pays the person who experienced the loss." – International Insurance

Most U.S. policies offer little to no coverage outside the U.S. or Canada, leaving expats vulnerable. That’s why specialized global liability insurance is essential. These policies are designed to work across different legal systems and often include legal defense costs without reducing your coverage limits. Basic plans start with coverage as low as $10,000, but you can opt for higher limits, up to $100,000, depending on your needs.

Personal Liability Coverage

Personal liability insurance typically covers three key areas: bodily injury (causing physical harm to someone), third-party property damage (damaging someone else’s belongings), and personal injury claims (such as defamation or slander). For expats, these protections are crucial, especially when navigating the legal complexities of different countries. Imagine scenarios like your child accidentally injuring a classmate at an international school or your dog biting someone in a country with strict pet liability laws – these are real risks.

In some nations, liability coverage is mandatory for specific situations, such as for school-age children or pets. If you’re involved in activities like charity work or civic projects, check your policy carefully, as many basic plans exclude coverage for these. For higher-risk scenarios, you might want to consider umbrella or excess liability insurance, which provides extra protection if a lawsuit exceeds your primary policy limits.

"Finding a travel medical policy that includes personal liability coverage is challenging. It presents an additional layer of risk for the underwriters and is difficult to determine, making it challenging to assign a price." – Joe Cronin, President, International Citizens Insurance

Be sure your policy extends to all family members, including adult children, and confirm whether it covers damages caused by pets. Personal liability insurance is often relatively inexpensive compared to other types of expat coverage. Adding it to an existing travel medical plan usually comes with only a small additional cost. Don’t overlook rental-related liabilities either, which we’ll discuss next.

Third-Party Property Damage Protection

While personal liability insurance addresses individual accidents or injuries, expats also face risks tied to rental property use. Accidental damage to rental properties is one of the most frequent liability claims for expats. In fact, many landlords abroad require proof of liability insurance before they’ll sign a lease. Specialized rental liability benefits can cover up to $25,000 for accidental damage to a landlord’s property.

Keep in mind, however, that standard policies often exclude contractual liabilities, such as lease obligations. If your rental agreement requires you to repair damages, a basic liability plan might not suffice. In such cases, you may need specific "Liability Coverage When Renting Property" to meet your landlord’s requirements. Additionally, most policies won’t cover intentional damage or certain high-risk situations, like acts of war or nuclear incidents.

Property Insurance for International Assets

International property and contents insurance is designed to protect assets located outside the U.S., where domestic policies typically don’t offer coverage. Expat home insurance caters specifically to properties abroad, safeguarding against risks like fire, storms, theft, floods, and vandalism. On the other hand, international personal property insurance – often referred to as "home contents" or "household effects" insurance – covers your belongings inside your residence, stored items, and even possessions you carry when traveling. Together, these policies form an essential part of protecting your global assets.

The global home insurance market is expanding rapidly. By 2025, it is expected to grow by 7% to 8.6%, with total premiums projected between $6.3 and $7 trillion. In Europe alone, the property insurance market reached approximately $196.6 billion in 2024 and is forecasted to grow at an annual rate of 7.0% through 2031.

"Lacking proper expat home insurance exposes your overseas property and investment to potentially devastating financial losses." – Allianz

When choosing coverage, "All Risks" policies offer broader protection than "named perils" policies. All Risks insurance covers any loss or damage unless explicitly excluded, while named perils policies limit coverage to specific events like fire or theft. For high-value items – like jewelry, fine art, or musical instruments – scheduled personal property coverage is essential. Insurers often require professional appraisals for items valued over $10,000, typically updated every three years.

If you’re relocating, transit and shipping insurance is a must. This coverage protects your household goods during the move, whether by truck, ship, or plane. In February 2026, Clements International introduced a "Worldwide Pet Accidental Reimbursement Benefit", which reimburses eligible veterinary costs for accidental injuries to pets during the first 90 days of relocation.

"Your items are protected from the moment they are shipped from your home. Coverage extends throughout transit, your location overseas, and throughout your return trip home." – Clements International

Home and Contents Insurance for Foreign Properties

Whether you own or rent abroad, your insurance should address the specific risks and regulations of your location. Homeowners insurance typically covers the physical structure against damage from fire, storms, and other hazards, while renters insurance focuses on personal belongings and liability within a leased space. Both types of insurance must comply with the legal requirements of the host country to ensure they remain valid.

Standard international personal property policies often include up to $10,000 in medical expense coverage for guests injured at your residence. Many also provide personal liability protection of up to $500,000, covering legal responsibilities for third-party injuries or property damage.

Before moving, take the time to inventory your belongings. Document items with photos and receipts, store these records digitally, and classify them as unscheduled everyday items (e.g., clothing, small electronics) or scheduled valuables that require itemized lists and appraisals. Keep in mind that unscheduled claims usually involve a deductible, while scheduled items often do not [29, 30]. Be aware of policy exclusions for unoccupied properties – many policies won’t cover homes left vacant for over 60 consecutive days. Additionally, confirm whether your coverage extends to items in storage. While many international policies cover goods in commercial storage facilities, self-storage units are often excluded due to higher security risks.

"Failing to carefully compare policy coverages can cause expensive surprises. Many expats only discover gaps in their coverage when filing a claim, often when it’s too late." – Allianz

You’ll also need to decide between "Full Replacement Cost" and "Indemnity" (Actual Cash Value) coverage. Replacement Cost policies pay for new items of similar quality, while Indemnity coverage deducts depreciation from the payout. If avoiding out-of-pocket expenses is a priority, Replacement Cost coverage is worth the slightly higher premiums.

For those managing properties across multiple regions, additional coverage options simplify the process.

Multi-Property Coverage Options

Owning or renting properties in multiple countries can make managing separate insurance policies both complicated and expensive. Fortunately, some insurers offer multi-property coverage, bundling all residences into one policy. This simplifies administration and often provides cost savings through multi-policy discounts.

When selecting a multi-property plan, verify its geographical scope. Many so-called "worldwide" policies exclude the U.S., Canada, and countries under international sanctions [29, 32]. If you own property in these locations, you may need additional coverage or a policy that explicitly includes them. Worldwide coverage typically comes with higher premiums compared to region-specific policies.

Even with a bundled plan, each property must meet the legal and regulatory standards of its country. For instance, a home in France and an apartment in Thailand may require different minimum levels of fire insurance or liability protection.

Transit coverage is especially valuable for those moving belongings between homes. Look for policies that provide all-risk transit protection across air, sea, and land, ensuring there are no coverage gaps. This is crucial whether you’re shipping furniture internationally or relocating personal items between properties.

Standard sub-limits in expat policies often include caps, such as $3,000 for unscheduled jewelry, $200 for cash, and $1,000 for fragile items like glassware. If you own valuables at multiple properties, consider scheduling them individually to ensure full coverage. Keep appraisals up to date for any item worth $10,000 or more.

Some specialized international policies include a minimum earned premium – often around $50.00 – regardless of when the policy is canceled. While this might seem restrictive, the convenience and potential discounts of a bundled policy often outweigh these costs, especially for those managing three or more properties worldwide.

What to Look for in Expat Insurance Policies

When choosing expat insurance, the details in the fine print can make all the difference between being fully protected in a crisis or facing unexpected gaps in coverage. Key factors like renewal terms, emergency support, and provider networks are critical to ensuring your policy delivers when it matters most. These elements go beyond basic coverage and are essential for safeguarding yourself in unfamiliar territories.

Renewal Terms and Premium Predictability

For long-term expats, lifetime renewability is a must. This ensures your policy remains active year after year, regardless of age or changes in your health. Without this feature, you risk losing coverage when you need it most. Another crucial aspect is understanding how premiums will evolve. While insurance costs naturally rise with age, unusually low premiums can be a red flag. They often come with hidden trade-offs like limited provider networks, steep deductibles, or unexpected gaps in coverage that surface when you file a claim.

To avoid surprises, ask for a multi-year premium projection. Reliable insurers typically provide estimates that show how your costs will increase through age 65 and beyond. This transparency helps you plan for the future while ensuring your policy remains effective.

"The real goal is to find a plan that actually works for you in a crisis, not just one that looks good on paper." – Expat Insurance

Such clarity and foresight are essential for acting swiftly in emergencies.

Emergency Evacuation and 24/7 Support Services

Medical evacuation coverage is another non-negotiable feature. Policies should provide at least $1,000,000 in coverage, as emergency air ambulance services can easily exceed $100,000. This benefit ensures you can be transported to the nearest appropriate medical facility if local hospitals lack the required resources. Without it, you could face inadequate care or crippling costs in the event of a serious accident in a remote area.

Equally important is repatriation coverage, which covers the cost of returning to your home country – or transporting your remains – if necessary. This service can cost up to $50,000. Many policies combine evacuation and repatriation, but it’s vital to confirm the specific limits and whether they apply per incident or annually.

Testing the insurer’s 24/7 support line is a smart move. Call with hypothetical scenarios to gauge their responsiveness. Ask how they would handle emergencies in your destination country, whether they provide multilingual support in your preferred language, and how quickly they can arrange direct billing with local hospitals. Some insurers also offer mobile apps for instant claims submissions and real-time assistance. These features can reduce delays in receiving critical care and are a key part of protecting yourself abroad.

Provider Networks and Multilingual Support

Having access to direct billing networks is crucial for expats, as it eliminates the need to pay upfront for medical care. Before signing a policy, ensure that reputable hospitals in your local area – not just in your country – have direct billing agreements with your insurer. A good way to verify this is by contacting the international billing department of your nearest hospital to confirm they work with your provider.

Use the insurer’s online directory to search for in-network hospitals by district or postal code. For example, a policy advertising "coverage in Thailand" is meaningless if the nearest in-network hospital is 200 miles away from your home in Chiang Mai. Additionally, check whether the policy allows for out-of-network claims processing in emergencies.

Multilingual support is another critical factor. It’s not just about having a customer service line in your language. Look for insurers that provide policy documents, claims forms, and online portals in multiple languages. This ensures you can fully understand your coverage terms and navigate claims without needing translations. Miscommunication can lead to costly delays, especially when dealing with pre-approval requirements or denied claims.

sbb-itb-39d39a6

How Insurance Fits with Asset Protection Planning

Insurance alone can’t shield you from every asset risk. For expats managing assets across multiple countries, pairing insurance with offshore trusts and LLCs creates a stronger defense for your wealth. While insurance addresses specific risks like medical emergencies, liability claims, or property damage, trusts and companies establish legal barriers that make it harder for creditors or lawsuits to threaten your assets. Think of insurance as your reactive safety net and trusts as proactive planning tools. Together, they form a comprehensive strategy, paving the way to explore how offshore trusts and Family LLCs play a key role in asset protection.

Insurance in Offshore Trusts and Company Structures

Offshore trusts can hold various assets, including life insurance policies, real estate, and investments, effectively safeguarding them. Jurisdictions such as the Cook Islands and Nevis are favored for their robust legal protections. For instance, in the Cook Islands, creditors face the highest civil burden of proof – proving fraudulent transfer "beyond a reasonable doubt" – to challenge a trust. Nevis adds additional hurdles, requiring creditors to post a $25,000 bond to file a lawsuit and hire a local attorney. Both jurisdictions also have a short two-year statute of limitations, meaning older transfers are quickly protected from legal challenges.

A typical structure might involve a Family LLC holding liquid assets, fully owned by an offshore trust. This setup not only enhances privacy but also allows assets to be moved outside U.S. jurisdiction if legal threats arise. Interestingly, high insurance limits can sometimes attract lawsuits, but having an offshore trust in place often deters litigation by forcing creditors to navigate foreign legal systems.

"At its core, asset protection is nothing more than risk management. Unlike liability or malpractice insurance, asset protection is active planning that covers all sorts of liabilities." – M. Wayne Patton, Attorney

U.S. expats must stay on top of compliance rules. If a trust holds insurance policies classified as "financial accounts", you might need to file Form 3520 when distributions exceed $18,156 or if the trust’s total assets exceed $171,015. Additionally, FBAR filing is required if the combined value of foreign accounts, including trust-held insurance, surpasses $10,000 at any point in the year. Setting up a trust isn’t cheap, with costs ranging from $8,000 in Belize or Nevis to $15,000 in the Cook Islands, plus annual fees of $2,000 to $5,000.

Professional Consultations for Custom Coverage

Standard insurance policies rarely meet the complex needs of expats with assets spread across multiple countries. Consulting with advisors who specialize in cross-border planning ensures your insurance, trusts, and company structures comply with U.S. tax laws and the inheritance rules of your host country. For instance, civil law countries like France or Italy enforce "forced heirship" laws, dictating who inherits your assets regardless of your will. In some cases, structuring insurance within a trust can help bypass these restrictions.

Experienced advisors can also help you avoid pitfalls, like purchasing "insurance-wrapped" foreign investment products that trigger PFIC (Passive Foreign Investment Company) status and lead to hefty U.S. taxes. They’ll ensure your trust documents include Anti-Duress clauses, which stop trustees from making distributions if you’re under legal pressure from foreign courts. To maximize protection, professional trustees should operate independently from you. By taking this integrated approach, you not only protect your assets but also ensure your insurance strategies align with cross-border legal and tax requirements, creating a solid foundation for global asset protection.

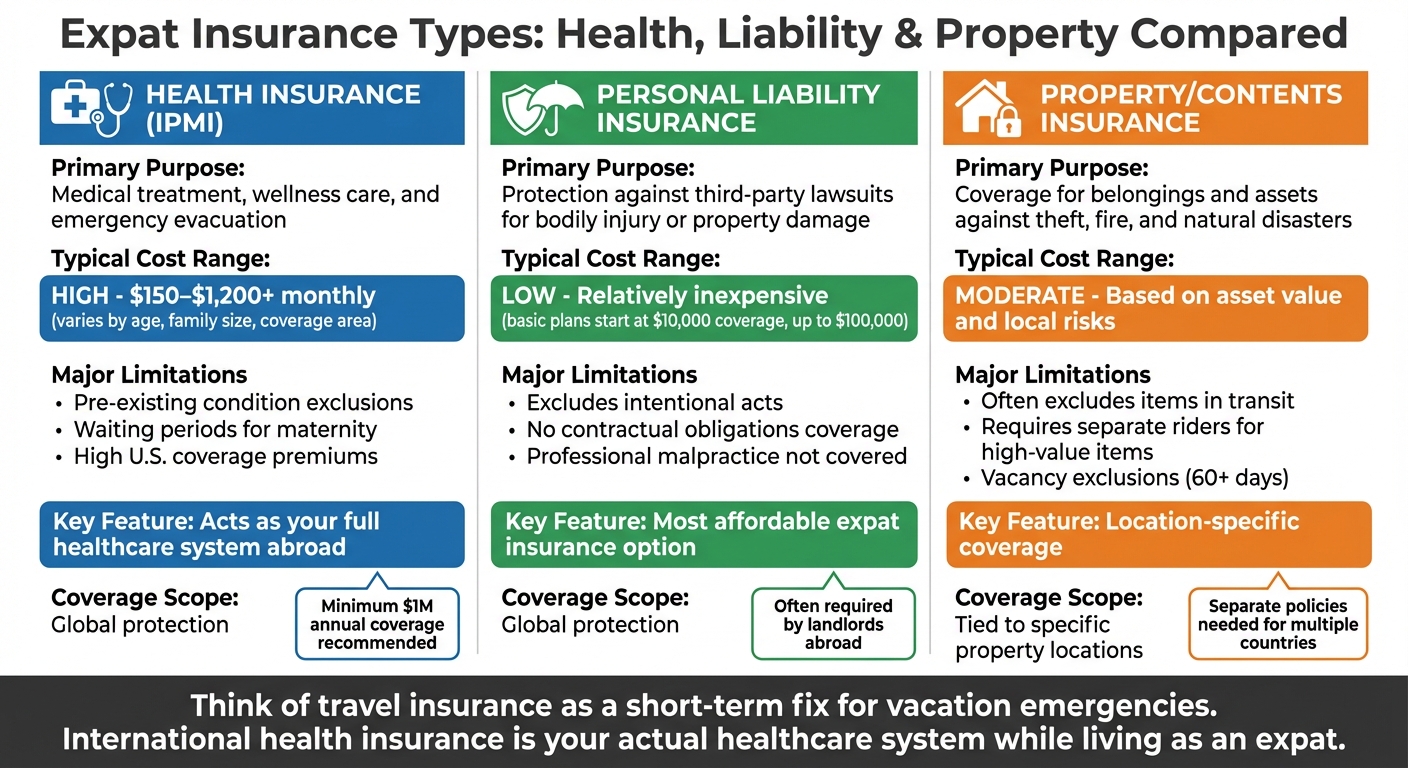

Comparison: Health, Liability, and Property Insurance

Expat Insurance Types Comparison: Health, Liability, and Property Coverage

When expats weigh their insurance options, understanding the differences between health, liability, and property insurance is crucial for managing international risks effectively.

Each type of insurance addresses distinct needs, so knowing their roles helps you allocate your budget wisely. Health insurance typically carries the highest premiums because it serves as your full healthcare system abroad, covering everything from routine check-ups to major procedures. For instance, a 28-year-old digital nomad in Southeast Asia might pay approximately $150 per month for a high-deductible plan, while a 45-year-old executive with a family in Western Europe could be looking at $1,200 monthly for comprehensive coverage. On the other hand, liability insurance is much more affordable, offering protection from third-party lawsuits without the steep recurring costs of health coverage. Property insurance falls between the two, with premiums determined by the value of your assets and the specific risks in your host country. This comparison highlights how these policies differ, helping you make smarter financial decisions.

One key distinction lies in geographical coverage. Health and liability insurance often provide global protection, while property insurance is tied to specific locations. For example, property insurance covers risks like theft, earthquakes, or floods in the country where your assets are located. If you own property or store valuables in multiple countries, you’ll need separate policies for each location.

"Think of travel insurance as a short-term fix for vacation emergencies. International health insurance is your actual healthcare system while living as an expat." – ExpatInsurance.com

Each policy comes with its own set of limitations that could catch you off guard. Liability insurance, for example, doesn’t cover intentional damage or contractual obligations, such as damages you agreed to pay in a rental agreement. Property insurance often excludes items in transit or requires extra riders for high-value possessions like jewelry or artwork. To manage costs effectively, align your deductibles with your emergency savings to balance premiums and out-of-pocket expenses.

| Insurance Type | Primary Purpose | Typical Cost Range | Major Limitations |

|---|---|---|---|

| Health (IPMI) | Medical treatment, wellness care, and emergency evacuation | High; $150–$1,200+ monthly, depending on age, family size, and coverage area | Pre-existing condition exclusions, waiting periods for maternity, high U.S. coverage premiums |

| Personal Liability | Protection against third-party lawsuits for bodily injury or property damage | Relatively low/inexpensive | Excludes intentional acts, contractual obligations, and professional malpractice |

| Property/Contents | Coverage for belongings and assets against theft, fire, and natural disasters | Moderate; based on asset value and local risks | Often excludes items in transit, requires separate riders for high-value items |

Expat Insurance Selection Checklist

When you’re an expat, choosing the right insurance policy isn’t just about ticking boxes – it’s about making sure your coverage truly works when you need it most. Here’s a step-by-step checklist to guide you through the process.

Start by checking the insurer’s network reach in your area. Don’t rely solely on polished marketing brochures. Instead, call the international billing department of a major hospital near your new home. Ask if they have a direct billing agreement with your insurer. This single call could save you from having to pay thousands of dollars upfront during a medical emergency.

Next, examine coverage limits and sub-limits. A solid policy should offer an annual maximum of at least $1,000,000 to cover catastrophic events. However, dig into the fine print – some treatments like cancer care, maternity, or organ transplants might have much lower sub-limits than the overall policy cap. Also, think about your deductible. For example, if you have $5,000 set aside for emergencies, opting for a $2,500 deductible can help lower your premium without stretching your finances.

After that, make sure the geographical scope of your policy fits your lifestyle. Decide whether you need "Worldwide" coverage or "Worldwide excluding USA." Excluding the U.S. can reduce your premiums by 30% to 50%. Also, check if the policy covers trips back to your home country and for how long – many plans limit this to 90 days per year. And don’t overlook emergency evacuation coverage – ensure it provides at least $1,000,000, as air ambulance costs can easily exceed $100,000.

Lastly, be upfront when disclosing your medical history during the application process. Withholding information is a common reason for denied claims or even voided policies. Decide between Full Medical Underwriting, which offers upfront clarity, or Moratorium Underwriting, where pre-existing conditions may be covered after 24 months. Before finalizing, test the insurer’s 24/7 support line to confirm they offer multilingual assistance and quick responses.

This checklist can help ensure your insurance policy is ready to protect you when it matters most.

Conclusion

Living abroad comes with its own set of risks: emergency medical services alone can cost tens of thousands of dollars, and many hospitals require upfront payments, which can quickly deplete your savings if you’re not connected to a direct billing network. This is why having insurance tailored specifically for expats isn’t just a good idea – it’s a necessity.

The right international health insurance shields you from unexpected financial burdens while ensuring seamless healthcare access across borders. With the global market for international health insurance projected to hit around $29.04 billion in 2024, it’s clear that more expats are prioritizing features like portability, direct billing, and emergency support. Your coverage should adapt to your global lifestyle, offering the flexibility and protection you need.

"International health insurance is your personal healthcare system that travels with you. It steps in to replace the coverage you left behind in your home country." – Expat Insurance

Selecting the right policy, however, requires careful planning. Mistakes like failing to disclose pre-existing conditions or ignoring residency clauses can lead to voided coverage when you need it most. That’s why working with a specialized broker or fiduciary advisor is critical. They can ensure your policy aligns with your broader financial strategy, complies with local legal requirements, and provides reliable support wherever you are.

When it comes to safeguarding your health and financial well-being abroad, rely on professionals who understand the unique challenges of expat life. Your peace of mind – and that of your family – depends on it.

FAQs

How do I pick the right coverage area for my expat health plan?

When deciding on the right coverage area, think about your destination, lifestyle, and healthcare requirements. Some plans provide global coverage, while others focus on specific regions. Certain plans include the U.S., but others may exclude it or provide limited coverage there. If you live in or often travel to the U.S., selecting a plan with U.S. coverage is essential. However, global coverage tends to come with a higher price tag, so it’s important to balance your budget with your travel habits and healthcare needs.

What should I do if I have a pre-existing condition or need mental health care?

If you have a pre-existing condition or need mental health support, it’s important to find international health insurance plans that address these specific needs. Many insurance providers offer plans designed for expats, which often include coverage for pre-existing conditions and mental health care. Be sure to go through the policy details thoroughly to ensure the coverage matches what you’re looking for.

How much liability and property coverage do expats usually need?

Expatriates often need liability coverage ranging from $100,000 to $300,000 per incident. It’s also important to have property coverage that safeguards personal belongings against risks such as theft, natural disasters, or damage. The specific amount of coverage you need will depend on the value of your possessions and the level of risk you face while living overseas.