Living and earning across borders can be liberating, but tax laws can make it complicated. Here’s what you need to know:

- U.S. citizens are taxed on their worldwide income, no matter where they live. This includes reporting foreign bank accounts and digital assets.

- Tax residency rules vary by country. Many use the 183-day rule, but factors like permanent home and family ties also play a role.

- Double taxation is a risk, but treaties and tools like the Foreign Tax Credit (FTC) and Foreign Earned Income Exclusion (FEIE) can help reduce your burden.

- Offshore planning requires compliance with strict reporting rules, especially for U.S. citizens.

- Digital nomads and expats should carefully choose residency locations, manage income sources, and avoid triggering tax residency in multiple countries.

Failing to comply with tax laws can lead to penalties, double taxation, or even passport issues for U.S. citizens. Planning ahead and understanding your obligations is essential to staying in the clear.

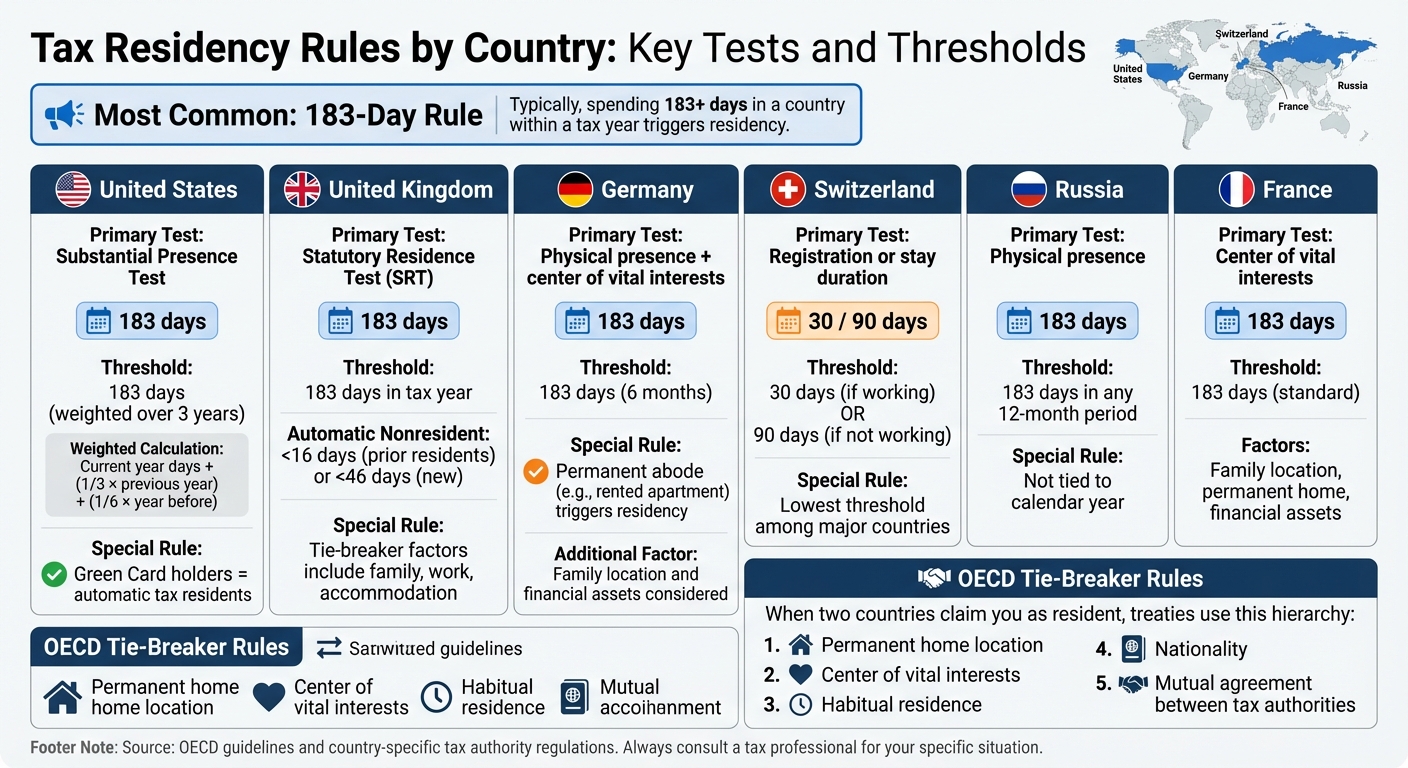

Tax Residency Rules Explained

Global Tax Residency Rules: Country-by-Country Comparison Guide

Tax residency isn’t about where you were born, your citizenship, or even where you feel most at home. It’s a legal status that determines which country (or countries) has the authority to tax your income. Getting this wrong can lead to double taxation or penalties for unreported earnings. Each country has its own approach to defining tax residency, often using specific tests to make this determination.

Common Tax Residency Tests

One of the most widely used benchmarks is the 183-day rule. If you spend 183 days or more in a country during a calendar year, you’re generally considered a tax resident there. That said, the way this rule is applied varies across countries.

The U.S. Substantial Presence Test, for example, uses a more detailed formula. To qualify as a tax resident, you must meet two criteria: spend at least 31 days in the U.S. during the current year and meet a weighted 183-day total over the past three years. This total is calculated by adding all the days from the current year, one-third of the days from the previous year, and one-sixth of the days from the year before that. Importantly, even partial days count, though there are exceptions for emergencies, short transit stays, and some border commutes. Additionally, Green Card holders automatically qualify as tax residents under the Green Card Test, regardless of how many days they spend in the U.S.

In the U.K., the Statutory Residence Test (SRT) takes a layered approach. If you spend fewer than 16 days in the U.K. (as a prior resident) or fewer than 46 days (if you’re new), you’re automatically classified as a nonresident. If you’re on the borderline, other factors – like family ties, work commitments, and access to accommodation – come into play.

Some countries go beyond counting days. For example, France and Germany evaluate your "center of vital interests", which includes where your family lives, where your financial assets are located, and where you maintain a permanent home. Germany also considers maintaining a "permanent abode" (such as a rented apartment) as a trigger for tax residency. Switzerland has an even lower threshold: 30 days if you’re working or 90 days if you’re not.

When two countries claim you as a resident, OECD tie-breaker rules – often part of double taxation treaties – help resolve the conflict. These rules prioritize factors like permanent home, center of vital interests, habitual residence, nationality, and, if needed, mutual agreements between the countries’ tax authorities.

| Country/Region | Primary Test | Threshold | Special Notes |

|---|---|---|---|

| United States | Substantial Presence Test | 183 days (weighted over 3 years) | Green Card holders are automatic residents |

| United Kingdom | Statutory Residence Test | 183 days | Automatic nonresident if under 16 or 46 days |

| Germany | Physical presence | 183 days (6 months) | Permanent abode triggers residency |

| Switzerland | Registration or stay duration | 30 days (working) or 90 days (not working) | Lower threshold than most countries |

| Russia | Physical presence | 183 days in any 12-month period | Not tied to calendar year |

Next, let’s explore how being classified as a tax resident impacts your financial obligations.

What Tax Residency Means for Your Obligations

Once you’re deemed a tax resident, your responsibilities grow. For example, in the U.S., residents are taxed on their worldwide income, just like U.S. citizens. Nonresidents, by contrast, are taxed only on income derived from U.S. sources. The IRS explains: "U.S. residents are taxed in the same manner as U.S. citizens on their worldwide income, and nonresidents… are subject to federal income tax only on income derived from sources within the United States".

Take digital nomad taxes for an individual earning Take a digital nomad earning $150,000 globally.50,000 globally. If they’re a U.S. tax resident, their entire income could be taxable in the U.S., even if earned abroad. On the other hand, a nonresident alien would only owe taxes on income linked to U.S. activities.

Some visa holders enjoy temporary relief. For instance, students on F, M, or Q visas and teachers on J or Q visas are classified as "exempt individuals" in the U.S. Their days in the country don’t count toward the Substantial Presence Test for up to five years.

In some cases, you might face a dual-status scenario during the year you arrive in or depart from a country. This requires a split-year tax return, dividing income between resident and nonresident periods. Additionally, if you spend fewer than 183 days in the U.S. but still meet the weighted test over three years, you might qualify for the "Closer Connection" exception by proving stronger ties to another country.

Navigating these rules is essential to avoid penalties, double taxation, or missed deadlines. Missteps can lead to costly consequences, making it critical to classify your residency accurately. In the next sections, we’ll discuss double taxation treaties and strategies to legally minimize your tax burden.

sbb-itb-39d39a6

Citizenship-Based vs Residency-Based Taxation

Tax systems around the world generally fall into two categories: residency-based taxation (RBT) and citizenship-based taxation (CBT). While over 190 countries use RBT, only the United States and Eritrea follow CBT. The distinction is straightforward: under RBT, your tax obligations depend on where you live and maintain economic ties. With CBT, your citizenship dictates your tax responsibilities, regardless of where you reside. The IRS clarifies this in Publication 54:

"If you are a U.S. citizen or resident alien, your worldwide income is generally subject to U.S. income tax, regardless of where you are living".

For example, a Canadian or German citizen who moves abroad generally stops filing taxes in their home country once they establish residency elsewhere. This stark difference highlights the unique challenges faced by U.S. citizens living abroad.

How the US Taxes Citizens on Worldwide Income

U.S. citizens must navigate complex tax obligations, even when living outside the country. They are required to file Form 1040 annually, report all worldwide income, and comply with FBAR and FATCA rules if their foreign bank accounts exceed $10,000 or meet other thresholds.

Take James, a U.S. citizen who moved to Spain in 2010. He earns €65,000 annually working for a Spanish company. Despite having no income from U.S. sources, James must report his Spanish salary to the IRS every year. By using the Foreign Earned Income Exclusion (FEIE) – which allows him to exclude up to $130,000 (for the 2025 tax year) – he can reduce his U.S. tax liability to $0. However, he still has to file the necessary forms and report his Spanish bank accounts if their balances exceed $10,000.

This system creates unique hurdles. Many foreign banks turn away U.S. citizens to avoid the compliance burden imposed by FATCA reporting requirements. Additionally, U.S. expats often face steeper tax preparation costs due to the intricacies of dual filing requirements.

"The difference between citizenship-based taxation and residency-based taxation determines whether you file taxes based on your passport or your physical location".

Failure to meet filing obligations can have serious repercussions. For instance, the IRS can notify the State Department about individuals with significant unpaid tax debts, potentially leading to passport denial or revocation. Notably, Green Card holders face the same requirements as U.S. citizens – they must report worldwide income regardless of where they live.

How Residency-Based Tax Systems Work

Countries like Canada, the United Kingdom, Germany, and Australia use residency-based taxation, tying tax obligations to where you live rather than your citizenship. Once you move abroad and sever residential ties, you generally stop filing tax returns in your home country.

Consider Maria, a Canadian citizen who moved to Germany for work. Under Canada’s RBT system, once Maria establishes residency in Germany, she only files taxes in Germany. Her tax responsibilities shifted entirely when her physical location changed.

Residency under these systems is often determined by spending 183 or more days in a country or maintaining other significant ties, such as a permanent home. For example, in the U.K., staying 183 days or more in a tax year automatically makes you a resident for tax purposes.

This approach has its perks. Expats don’t have to report foreign bank accounts to their home country, making banking relationships simpler. Foreign financial institutions also don’t face the same compliance burdens they do with U.S. citizens. Additionally, once you’re no longer a resident, you’re typically taxed only on income earned within that country.

However, residency-based systems aren’t without challenges. If you maintain ties to multiple countries, you might unintentionally trigger tax residency in more than one jurisdiction. Resolving such conflicts often requires applying treaty "tie-breaker" rules to determine which country holds primary taxing rights. Understanding these nuances is crucial for effective global tax planning.

| Factor | U.S. (Citizenship-Based) | Most Countries (Residency-Based) |

|---|---|---|

| Primary Filing Trigger | Citizenship or Green Card | Physical presence (typically 183+ days) |

| Worldwide Income | Always reportable to home country | Only reportable if you are a resident |

| Moving Abroad | Filing obligations continue indefinitely | Filing obligations generally end upon departure |

| Foreign Account Reporting | Required (FBAR/FATCA) | Usually not required by home country |

| Banking Access | Often restricted due to FATCA | Generally unrestricted |

Using Double Taxation Treaties and Relief Options

Earning income in one country while being taxed in another can lead to the frustrating scenario of paying taxes twice on the same earnings. Double taxation treaties, also known as Double Tax Agreements (DTAs), are bilateral arrangements that decide which country has the primary right to tax different types of income, such as wages, dividends, interest, or pensions.

"A tax treaty is a bilateral agreement made by two countries to resolve issues involving double taxation of passive and active income." – Investopedia

Under these treaties, the country where the income originates usually reduces withholding taxes, while the taxpayer’s country of residence provides a credit for taxes paid abroad. These agreements are typically reciprocal, ensuring that residents of both countries benefit. However, U.S. treaties include a "Saving Clause", which allows the U.S. to tax its citizens and residents as if the treaty didn’t exist, with a few exceptions.

The U.S. has tax treaties with many countries, though these agreements can change over time. For instance, the U.S.-Chile treaty came into effect for tax years starting January 1, 2024, while the U.S.-Hungary treaty was terminated on the same date. Additionally, significant portions of the U.S.-Russia treaty were suspended as of August 16, 2024. If you plan to claim treaty benefits, you must file Form 8833 (Treaty-Based Return Position Disclosure) with your tax return. Failing to do so can result in penalties – $1,000 for individuals or $10,000 for corporations.

How Double Taxation Treaties Work

These treaties allocate taxing rights based on income type and residency. For example, if you’re a U.S. citizen working in Germany, the U.S.-Germany treaty outlines how each country can tax your wages, investment income, or pension distributions. Often, the country where you work has the first right to tax your wages, while your home country provides a credit for the taxes you’ve already paid abroad.

If you meet the residency criteria in both countries, the treaty’s residency article resolves the conflict by considering factors like your permanent home, where your vital interests lie, and your habitual abode. To ensure eligibility, you must also meet the treaty’s Limitation on Benefits provisions, which are designed to prevent misuse of treaty benefits. Beyond treaty advantages, additional relief options are available through the Foreign Earned Income Exclusion (FEIE) and the Foreign Tax Credit (FTC), which we’ll discuss further.

To claim treaty benefits from a foreign tax authority, you’ll need Form 6166 (Certification of U.S. Tax Residency), which is obtained by filing Form 8802 with the IRS. Keep in mind that not all U.S. states honor federal tax treaties, so it’s important to check your state’s stance on such agreements.

Foreign Earned Income Exclusion and Tax Credits

In addition to treaties, the U.S. offers relief through the FEIE and FTC. For the 2025 tax year, the FEIE allows you to exclude up to $130,000 of foreign earnings from U.S. taxable income. To qualify, you need a tax home in a foreign country and must pass either the physical presence test (spending at least 330 full days in a foreign country within a 12-month period) or the bona fide residence test.

The FTC, on the other hand, provides a direct offset against your U.S. tax liability based on the income taxes you’ve already paid to a foreign government. In high-tax countries like France or Germany, the FTC can sometimes reduce your U.S. tax bill to zero while allowing you to carry forward any unused credits.

For example, a U.S. citizen in France earning $136,000 could use the $130,000 FEIE, leaving $6,000 taxable. By applying a proportional FTC, their U.S. tax liability could drop from $1,320 to $544. However, relying solely on the FTC might have eliminated the tax bill entirely.

It’s important to note that you cannot claim both the FEIE and an FTC on the same income. The FTC must be calculated only on the portion of income that isn’t excluded under the FEIE. Additionally, if you revoke the FEIE to switch to the FTC, you generally can’t claim the FEIE again for six years without IRS approval.

| Relief Method | Primary Benefit | Key Requirement |

|---|---|---|

| Tax Treaty | Reduced withholding or exemptions | Residency in a treaty country |

| FEIE | Excludes up to $130,000 (2025) | Tax home abroad + 330-day or bona fide test |

| Foreign Tax Credit | Offsets U.S. tax with foreign taxes | Proof of foreign taxes paid on the same income |

Another option to consider is the Foreign Housing Exclusion (or deduction), which covers certain housing expenses paid by your employer or incurred through self-employment. When deciding between the FEIE and FTC, weigh the benefits carefully. In countries with higher tax rates than the U.S., relying solely on the FTC might eliminate your U.S. tax entirely while allowing you to carry forward excess credits to future years.

Offshore Asset Protection Methods

Moving assets offshore is a legal approach often used by high-net-worth individuals and business owners to safeguard their wealth and optimize tax strategies. By leveraging offshore structures, individuals can separate themselves from their assets and benefit from jurisdictions with more favorable tax laws. However, modern offshore planning demands more than just establishing shell companies – there must be real economic activity to meet regulatory requirements.

"The most sophisticated tax strategies don’t rely on loopholes or aggressive schemes – they leverage fundamental differences in how tax systems treat global income." – Project Black Ledger

For U.S. citizens, offshore planning comes with extra hurdles. Since the U.S. taxes its citizens on worldwide income, simply setting up an offshore company doesn’t eliminate tax obligations. You’ll still need to file forms like 5471 (foreign corporations), 8865 (foreign partnerships), and 8938 (foreign financial assets). Offshore trusts require additional filings, such as Forms 3520 and 3520-A. Missing these filings can lead to steep penalties.

Let’s dive into the practical steps for creating offshore companies and trusts that align with legal standards.

Setting Up Offshore Companies and Trusts

Offshore companies are designed to separate your assets while strategically placing operations, intellectual property, or investments in jurisdictions with lower tax rates. To meet compliance standards, these companies typically need a physical office, local employees, and decision-making processes based in the jurisdiction.

For example, you might use a UAE holding company for global coordination, a Singapore-based entity for delivering services, and a separate company for intellectual property management. This multi-entity approach allows each part to benefit from the specific advantages of its jurisdiction. In Singapore, for instance, services performed outside the country are often treated as foreign-sourced income, even if the client is local. To ensure compliance, contracts should clearly outline where the services are performed.

Offshore trusts, on the other hand, are primarily about asset protection and privacy rather than tax reduction. For U.S. taxpayers, these trusts don’t eliminate tax responsibilities but can create strong barriers against creditors when structured correctly. Jurisdictions like the Cook Islands, Anguilla, and Samoa offer legal frameworks that make it difficult for foreign courts to access trust assets. However, it’s crucial to establish these trusts well before any creditor claims arise to avoid accusations of fraudulent transfers.

Territorial Tax Jurisdictions

Another layer of offshore planning involves choosing territorial tax jurisdictions, which only tax income earned within their borders. This means foreign-sourced income remains untaxed. Countries like Singapore, Hong Kong, Panama, and Malaysia operate under this model, making them attractive for entrepreneurs with global operations. The UAE, while still offering 0% personal income tax, introduced a 9% corporate tax in 2025.

The success of these systems depends on understanding income sourcing rules. For services, the focus is on where the work is physically done; for trading, it’s about where contracts are negotiated and executed. In countries like Malaysia, maintaining tax-exempt status often requires keeping banking activities abroad or ensuring foreign-sourced funds are separate from domestic accounts.

To establish tax residency in territorial jurisdictions such as Singapore or Malaysia, you’ll typically need to meet the 183-day rule. Keeping detailed records – like boarding passes, hotel receipts, and travel logs – can help avoid unintentionally triggering residency in high-tax transit countries. Panama also offers an accessible option through its "Friendly Nations" visa, which requires just a $5,000 bank deposit to demonstrate economic stability.

"The strength of a territorial tax structure lies not in its complexity, but in the clarity and completeness of its documentation." – Project Black Ledger

Tax Planning for Digital Nomads and Expats

For digital nomads and expats, tax planning goes beyond just following the rules – it’s about aligning your financial strategy with your lifestyle and income sources. The goal? Position yourself in jurisdictions that suit your income patterns while steering clear of unintentional tax residency in high-tax countries you might pass through.

Choosing Low-Tax Residency Locations

Picking the right tax residency starts with understanding how different countries define income, physical presence, and economic activity requirements.

Countries with territorial tax systems are particularly appealing for mobile professionals. For instance:

- Panama taxes only domestic income, meaning foreign earnings are untaxed. Its Friendly Nations visa requires just a $5,000 bank deposit.

- Malaysia’s MM2H program offers similar benefits but typically requires 182 days of residency and proper management of foreign funds.

- The UAE has no personal income tax, even with a corporate tax introduction in 2025. However, setting up a company there costs between $4,000 and $15,000 annually.

- Georgia offers an effective tax rate as low as 1% for those earning over $50,000 annually or purchasing property worth at least $100,000.

Residency rules vary. While many countries use the 183-day rule, others look at your "center of vital interests" or "habitual abode", which consider your family and economic ties. You’ll need to show that your life genuinely revolves around your chosen jurisdiction.

"The most sophisticated tax strategies don’t rely on loopholes or aggressive schemes – they leverage fundamental differences in how tax systems treat global income."

– Project Blackledger

Leaving a high-tax country requires careful planning. Countries like Canada, Australia, and many European nations won’t automatically release you from tax obligations. You may need to sell or rent out your home, cancel memberships, close local bank accounts, and inform tax authorities formally. In some cases, such as in Germany or the UK, "extended limited tax liability" can linger for years.

Organizing Income Across Multiple Countries

Once you’ve secured your residency, the next challenge is managing your income across borders while staying compliant.

A three-part strategy can help you stay ahead:

- Choose a tax-efficient residency.

- Set up an optimized corporate structure.

- Build a reliable international banking system.

For example, you could establish tax residency in Panama, run your business through a Singapore-based company, and manage finances using multi-currency banking platforms.

For U.S. citizens, worldwide taxation applies regardless of where you live. However, tools like the Foreign Earned Income Exclusion (FEIE) can help. If you meet the Physical Presence Test (330 days outside the U.S. in 12 months) or the Bona Fide Residence Test, you can exclude up to $126,500 of foreign-earned income for the 2024 tax year. Additionally, the Foreign Tax Credit (FTC) offers dollar-for-dollar relief for taxes paid to foreign governments, which is especially useful in high-tax countries.

Documentation is critical. If you’re self-employed and earn $400 or more, you must file a U.S. return. All foreign income must be reported in U.S. dollars, using the correct exchange rates. You’ll also need to file an FBAR (FinCEN Form 114) if foreign account balances exceed $10,000 at any point. FATCA Form 8938 applies if your foreign assets surpass $300,000 during the year or $200,000 at year-end for single filers living abroad.

Corporate entities can be powerful tools. For instance, setting up a UAE company or a U.S. LLC can help separate personal and business finances, making it easier to manage profits and expenses. But watch out for Controlled Foreign Company (CFC) rules, which may tax undistributed offshore profits as personal income in your residency country.

Tax treaties are another key resource. With over 3,000 global Double Taxation Treaties, you can often reduce withholding tax rates or avoid double taxation entirely. To claim treaty benefits, use IRS Form 8833. Social Security Totalization Agreements are also helpful for self-employed nomads, preventing double payments of social security taxes.

"The most sophisticated digital nomad tax strategies aren’t about evading detection – they’re about creating positions so legally sound that full disclosure poses no risk."

– Project Blackledger

A multi-base approach is becoming increasingly popular. This involves establishing one tax-friendly home base where you’re officially resident, then maintaining two or three secondary bases where you can spend time without triggering residency rules. This setup allows you to enjoy multiple locations throughout the year while keeping a clear and defensible tax position. Keep in mind, 141 countries now share tax information automatically through the Convention on Mutual Administrative Assistance in Tax Matters. Combining multi-base strategies with offshore structures and treaty benefits can create a well-rounded global tax plan.

Conclusion

Navigating global tax planning requires a well-thought-out approach, as even minor errors can lead to severe penalties. Whether you’re considering residency in a territorial tax jurisdiction, creating offshore entities, or leveraging treaty benefits, every decision has long-term implications for your financial well-being and legal compliance.

The stakes are undeniably high. Ensuring your tax position is both legally compliant and fully disclosed is non-negotiable. This highlights the critical need for a solid, forward-thinking tax strategy.

"If you’re a U.S. citizen or resident alien, the rules for filing income tax returns and paying estimated tax are generally the same whether you’re in the United States or abroad. No matter where you live, your worldwide income is subject to U.S. tax." – Taxpayer Advocate Service

Tax laws are constantly evolving. For example, the One Big Beautiful Bill Act of July 2025 introduced significant changes to U.S. international tax policy. Meanwhile, the OECD’s Pillar Two framework now enforces a 15% global minimum tax rate for large multinational corporations. Authorities are also extending their oversight to include digital assets such as cryptocurrency and NFTs in standard tax filings. Additionally, treaties can shift, as demonstrated by the U.S. terminating its treaty with Hungary effective January 1, 2024. These developments underscore the growing need for proactive and adaptable tax planning.

Seeking professional guidance is more important than ever. As Horizons emphasizes, "It makes good sense to consult a tax advisor or global EOR for advice on compliance and international tax". An experienced advisor can help you navigate residency tests, maximize tax credits, and maintain compliance across jurisdictions. By aligning with the strategies discussed earlier, you can secure a tax position that is both consistent and legally sound. With the right planning and expert support, you can safeguard your wealth while meeting all legal obligations, no matter where you operate.

FAQs

How do I prove I’m not a tax resident in a country I visited a lot?

To demonstrate that you’re not a tax resident in a country you visit often, you’ll need to prove you didn’t meet its residency criteria – such as exceeding the allowed number of days or establishing significant ties there. Keep detailed travel records, including flight itineraries, passport stamps, and any other documentation that shows your movements. At the same time, maintain evidence of strong connections to another country, like property ownership, employment, or family ties.

If you’re claiming an exemption under something like the physical presence test, having proper documentation is crucial. Additionally, tax treaties between countries can sometimes provide clarity on residency rules and help avoid double taxation. It’s always wise to consult a tax professional to ensure you meet all legal requirements and avoid complications.

Which is better for me: FEIE or the Foreign Tax Credit?

Choosing between the Foreign Earned Income Exclusion (FEIE) and the Foreign Tax Credit (FTC) hinges on your personal financial situation and objectives. The FEIE allows you to exclude up to a specific amount of foreign-earned income from U.S. taxation, while the FTC provides a credit for taxes paid to a foreign government on income that isn’t excluded.

Key considerations include the type of income you earn, the likelihood of being taxed twice, and your long-term financial plans. It’s essential to review the latest tax guidelines or consult a tax professional to determine which option aligns better with your circumstances.

What forms do I need if I have foreign bank accounts or an offshore company?

To meet U.S. regulations, you’re required to file FinCEN Form 114 (FBAR) to disclose foreign bank accounts and IRS Form 8938 (FATCA) to report offshore financial assets or entities. These forms are essential for staying compliant with the legal obligations tied to international financial holdings.