December 26, 2013

By: Kelly Diamond, Publisher

Obamacare was supposed to be the crown jewel of the Obama administration. But as time has passed and the law incrementally unfolds, it is becoming clear that this precious stone is really just worthless gravel.

The only thing propping up the ACA right now are a bunch of executive orders and exceptions!

There’s an adage used by some libertarians which goes: “Statism: Ideas so awesome, they have to be mandatory”. As it turns out, the ideas that ooze out of the rotting gash known as the U.S. Federal Government aren’t quite as self-selling as the wheel or electricity. That’s why government either makes participation mandatory (or lack of participation criminal) or assumes a monopoly over certain services so that only certain people can get an alternative.

There’s an adage used by some libertarians which goes: “Statism: Ideas so awesome, they have to be mandatory”. As it turns out, the ideas that ooze out of the rotting gash known as the U.S. Federal Government aren’t quite as self-selling as the wheel or electricity. That’s why government either makes participation mandatory (or lack of participation criminal) or assumes a monopoly over certain services so that only certain people can get an alternative.

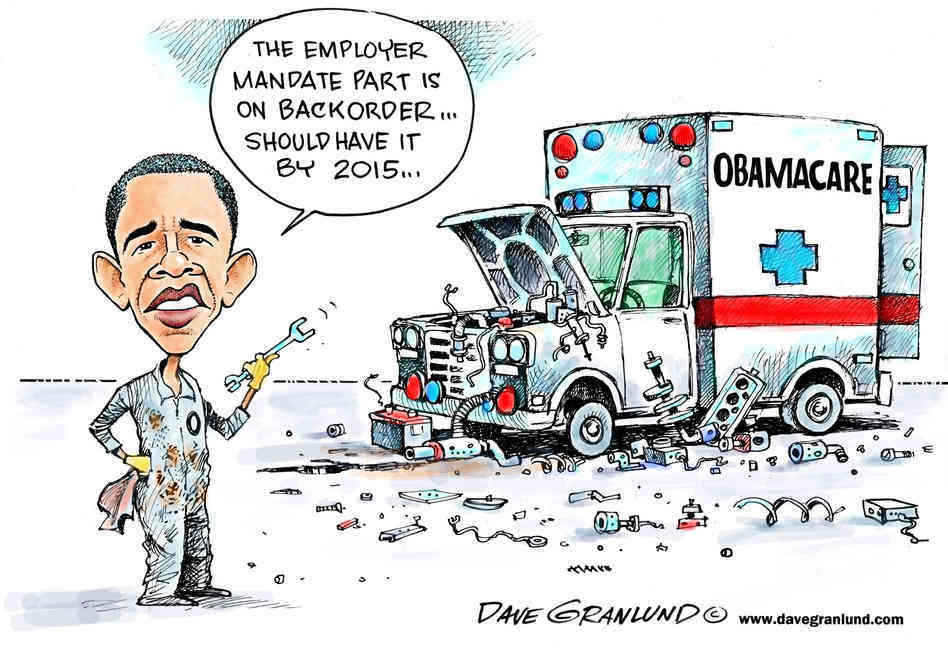

The ACA (i.e. Affordable Care Act) is obviously no exception… except for all its recent exceptions! First we needed to pass the law before reading it so that we could find out what was in it. Then certain corporations were exempt from having to participate. Then unions were exempt. Then we got an extension because the website was a failure.

The deadline for enrollment was Monday, December 23rd, 2013. Four days prior to this crucial date, millions more received their very own exemption: a hardship exemption to be specific. Originally, this exception was reserved for people who were homeless, bankrupt, or victims of domestic abuse. Now added to the roster of hardship exemptions are those who lost their once affordable plan due to Obamacare itself. So victims of Obamacare are now eligible for a one year stay on any penalties for non-enrollment.

As the Wall Street Journal puts it: “…HHS rushed out a bulletin noting that exemptions are available to those who “experienced financial or domestic circumstances, including an unexpected natural or human-caused event, such that he or she had a significant, unexpected increase in essential expenses that prevented him or her from obtaining coverage under a qualified health plan.” A tornado destroys the neighborhood or ObamaCare blows up the individual insurance market, what’s the difference?”

If people who are being kicked off their previous plans are finding the exchange’s alternatives to be such a hardship that they qualify for an exemption, it’s pretty difficult to continue denying rate-shock.

There’s an “under 30” catastrophic plan that opened up. Proponents of Obamacare begrudgingly allowed it, but because it is subject to less mandates it is 20% cheaper than other exchange policies (albeit more expensive than its pre-ACA counterpart on the open market) and therefore ineligible for subsidies. It’s also cheaper because the assumption is people under 30 are a lower risk than those over 30.

The nature of insurance, by definition, is that it is a hedge: a hedge that you WON’T get sick. Well, imagine everyone’s surprise when this category was opened up to 55 year olds! The “math” behind Obamacare (which in itself requires government subsidized benefit-of-the-doubt) relies upon a certain population purchasing various tiers of insurance. So when the anticipated number of people aren’t enrolling in each tier, the numbers no longer work. 55 year olds aren’t supposed to be buying low-risk policies at cheaper rates… but they are.

Part of what made Obamacare “work” (if in fact it was ever going to work as it was passed) was the individual mandate. Well, clearly, those lines have been obscured. Time will tell how that will affect the economics of Obamacare, but one thing is for sure: the whimsical alterations to Obamacare will affect the premiums in 2015. Add to this recent exemption the following: “Earlier this month he ordered insurers to backdate policies to compensate for the federal exchange meltdown, and before that HHS declared that it would not enforce for a year the mandates responsible for policy cancellations. Mr. Obama’s team has also by fiat abandoned the small-business exchanges, delayed the employer mandate and scaled back income verification.”

Obamacare is collapsing into its own untenable footprint. More people are without insurance than with it. As this law unrolls, more exemptions and exceptions are being issued by executive order. That alone is constitutionally questionable since Obamacare is THE LAW. Can the executive really disagree with the law and order that people not follow it? Or turn a blind eye to those who don’t follow it? Or decriminalize the lack of adherence to it?

It’s a sad testament to American society that President Obama can say that the crux of the law hasn’t been disrupted or that the law is working, and that there are people who believe this. The law at this point is utterly unrecognizable when juxtaposed with the original act that was passed/deemed into law.

It’s an even sadder reflection of our system and how broken it must be that Representatives and Senators don’t debate the finer point of bills prior to passing them, but instead leave the citizenry to be the unsuspecting guinea pigs for their political experiments. Clearly they knew enough about the bill to exempt themselves.

The debate surrounding Obamacare is no longer about whether people should have access to affordable healthcare or health insurance. That ship has clearly sailed from the Obamacare dock. The debate now is about whether Obamacare is any good? The Congressional Budget Office (CBO) at one point had some promising analysis (albeit making some best-case scenario assumptions). What would the CBO say now? Is this still a debt neutral policy? Is this really going to bring down the net cost of health insurance?