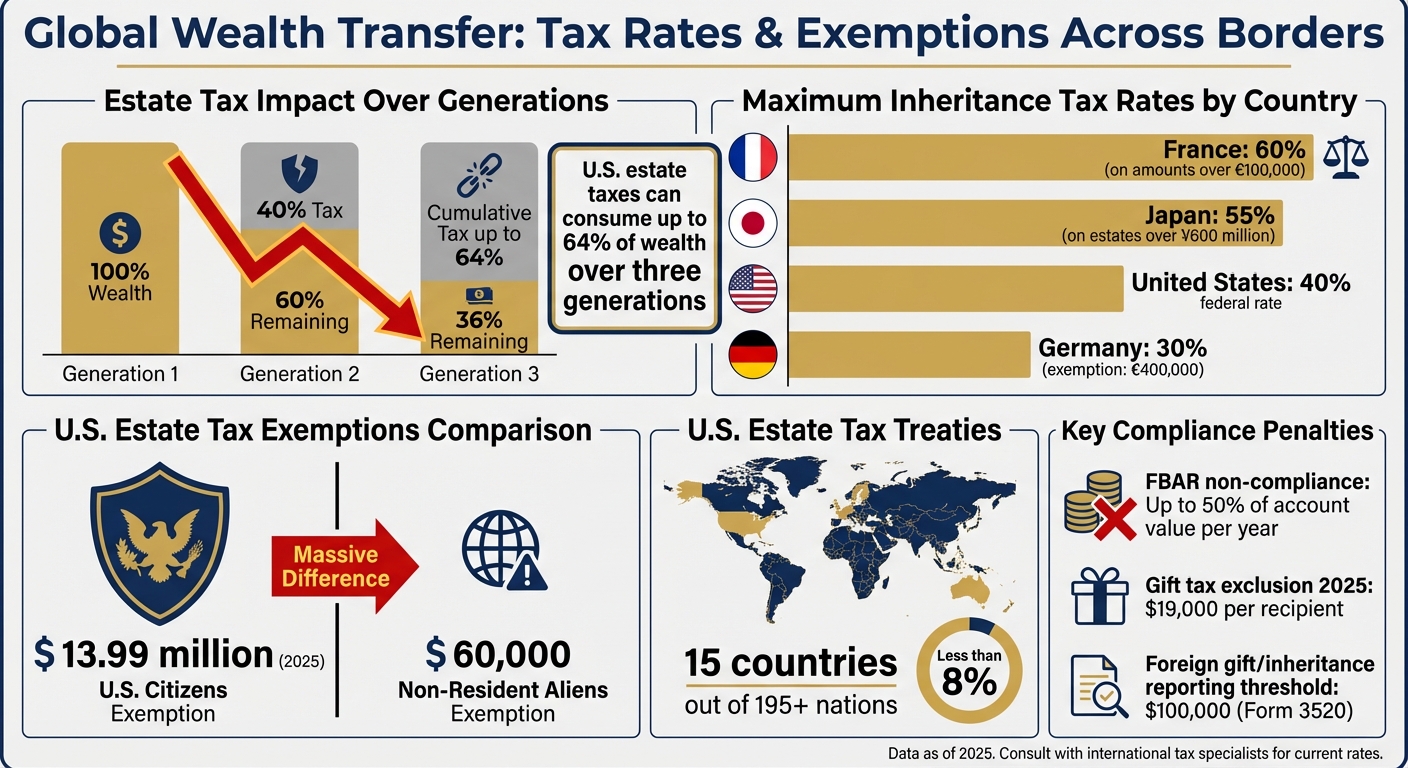

Transferring wealth internationally is more complex than ever, especially with families and assets spread across multiple countries. Without proper planning, you risk double taxation, legal disputes, and losing a significant portion of your wealth to taxes. For example, U.S. estate taxes can consume up to 64% of wealth over three generations, and countries like France and Japan impose inheritance taxes as high as 60% and 55%, respectively.

Key Challenges:

- Legal Differences: Common law countries (e.g., U.S., U.K.) allow inheritance flexibility, while civil law countries (e.g., France, Germany) enforce strict "forced heirship" rules.

- Tax Issues: Cross-border wealth transfers can trigger double taxation, with varying exemptions and tax rates.

- Compliance Risks: Failing to meet reporting requirements like FATCA or FBAR can lead to severe penalties.

- Asset Protection: Without proper structures, heirs may face liquidity problems or lose access to assets like cryptocurrency.

Key Strategies:

- Use offshore trusts or foundations to protect assets and bypass forced heirship laws.

- Draft international wills tailored to each jurisdiction to avoid legal conflicts.

- Plan residency and domicile carefully to reduce tax exposure.

- Leverage tax treaties and choose jurisdictions with favorable tax laws.

- Maintain liquidity through cash reserves or life insurance to cover taxes and fees.

To secure your wealth across borders, work with experts familiar with international laws and update your plan regularly as laws and circumstances change.

International Inheritance Tax Rates and Estate Tax Exemptions by Country

Key Challenges in International Wealth Transfer

Owning assets across multiple countries brings a maze of legal systems, tax rules, and regulations. Simply drafting a will isn’t enough – effective planning must address jurisdictional gaps and regulatory pitfalls that could derail even the most carefully thought-out strategies.

Legal Complexities Across Jurisdictions

One major challenge is the contrast between common law, which allows for flexible inheritance planning, and civil law systems, where forced heirship rules dictate fixed shares of an estate. For example, a trust set up in Texas might be ignored or treated differently in countries like France, Spain, or Germany, where trusts are either unrecognized or taxed as separate entities.

"The structure that works seamlessly in Dallas may create chaos in Dubai." – Suzanne L. Shier, Partner, Levenfeld Pearlstein, LLC

Legal documents like powers of attorney or wills often face enforcement issues when crossing borders due to varying execution requirements. The situation becomes even more complicated because the U.S. has estate and gift tax treaties with only 15 countries. Determining your legal domicile can also trigger disputes when multiple countries claim residency, potentially exposing your estate to double taxation.

These legal inconsistencies only magnify the tax issues tied to international wealth transfers.

Tax Implications and Cross-Border Compliance

Taxation becomes a minefield when transferring wealth across borders. In the U.S., the entire estate is taxed before distribution, while many other countries impose taxes on heirs as they receive their inheritance. This mismatch can lead to the same assets being taxed in different ways. For instance, non-resident aliens are allowed only a $60,000 estate tax exemption, a stark contrast to the $13.99 million exemption available to U.S. citizens in 2025. Assets like U.S. real estate or shares in American corporations are considered "U.S. situs" and are subject to federal estate tax.

Compliance adds another layer of complexity. Families must navigate FATCA (Foreign Account Tax Compliance Act) and the Common Reporting Standard, both of which require detailed reporting. Failing to file the FBAR (Report of Foreign Bank and Financial Accounts) can lead to penalties of up to 50% of the account’s value per year. Furthermore, the annual gift tax exclusion for 2025 is $19,000 per recipient, and any gifts or inheritances exceeding $100,000 from foreign sources require filing Form 3520.

Asset Protection Risks

Beyond legal and tax hurdles, protecting assets from claims and liquidity issues is critical. Assets held in personal names or traditional holding companies are vulnerable to creditor claims and civil judgments. Liquidity issues can also force heirs to sell off assets to cover tax bills. For example, in France, inheritance taxes on amounts exceeding €100,000 can climb to 60%, while in Japan, estates valued over ¥600 million face inheritance tax rates as high as 55%.

Cryptocurrencies and digital assets present their own risks – without proper key management, heirs could lose access permanently. Meanwhile, increasing adoption of public trust registries and aggressive information-sharing agreements is chipping away at the privacy that once shielded international wealth transfers.

sbb-itb-39d39a6

Strategies for Protecting Wealth Across Generations

Navigating international legal systems, tax obligations, and asset risks can be complex. To safeguard your wealth, consider strategies like establishing cross-border legal entities, preparing detailed succession documents, and planning residency carefully. These approaches create a layered defense for your assets.

Offshore Trusts and Foundations

Offshore trusts and family foundations are tailored solutions depending on your goals and the type of assets you hold. Trusts, common in jurisdictions following common law, are versatile for managing business holdings. Foundations, on the other hand, work well in civil law countries where trusts may not be recognized, making them ideal for long-term legacy planning. Both structures separate legal ownership from beneficial ownership, offering protection against lawsuits, judgments, and forced heirship claims.

The financial benefits can be substantial. For instance, an Anguilla trust can help heirs avoid up to 40% in estate taxes. Under current U.S. law, the combined lifetime gift and estate tax exemption will increase from $13.99 million per individual in 2025 to $15 million in 2026 (or $30 million for married couples). Additionally, these structures often bypass probate, giving heirs immediate access to assets without needing to liquidate property to cover taxes.

"The key distinction between basic estate planning and true wealth preservation lies in the architectural complexity of the structure. Modern wealth protection requires multiple layers of legitimate safeguards." – Project Black Ledger

Setting up these structures isn’t cheap. Initial costs range from $10,000 to $50,000, with annual maintenance fees between $3,000 and $15,000. Implementation, including due diligence and asset migration, can take 3 to 21 months. Jurisdiction matters: Singapore is often chosen for active business assets, New Zealand for passive investments, and Liechtenstein for multi-generational planning. Many families now combine trusts for business operations with foundations for personal legacies. It’s also important to align your succession documents with local laws to ensure seamless execution.

International Wills and Succession Documents

For assets held in different countries, drafting situs wills for each jurisdiction is essential. These wills ensure compliance with local laws, especially for real estate. However, coordination is critical, as a new will in one country can unintentionally revoke an earlier will elsewhere unless it includes explicit "non-revocation" clauses.

U.S. citizens with assets in the European Union (except Denmark and Ireland) can use the EU Succession Regulation (Brussels IV) to elect U.S. law for their estate, avoiding forced heirship rules. This is particularly useful in countries like France, where inheritance taxes can reach 60% on amounts over €100,000, or Germany, where exemptions are capped at €400,000 before taxes of up to 30% apply.

"A will that disposes of real property must usually comply with the law where the property is located. A home in Spain or a cottage in Ontario will be subject to local succession law regardless of a U.S. will’s terms." – Finhelp.io

For foreign real estate, draft situs wills and appoint local executors to navigate complex certification processes. To cover potential inheritance taxes and probate fees, consider setting aside cash reserves or purchasing life insurance. Modern succession documents should also address digital assets like cryptocurrency and online business credentials, which often bypass traditional probate systems.

Residency and Jurisdiction Planning

Your legal domicile plays a crucial role in determining tax and inheritance outcomes. The country where you reside – and where you are legally domiciled – affects which jurisdiction can tax your estate. The U.S. has estate tax treaties with only 15 countries, so understanding these treaties and local laws is vital when selecting a jurisdiction. While common law countries like the U.S. and U.K. allow testamentary freedom, civil law jurisdictions often enforce strict heirship rules.

Clearly document your domicile, as transfer taxes are tied to your permanent home. Evidence such as a marital residence can support your domicile claim. Before moving to a new country, ensure your existing trust structures are recognized there; otherwise, they could be taxed as resident entities or face high individual tax rates on distributions.

For U.S. citizens with non-citizen spouses, a Qualified Domestic Trust (QDOT) is necessary to defer estate taxes. Non-resident aliens, however, receive only a $60,000 U.S. estate tax exclusion for assets located in the U.S., compared to the $13.99 million exemption available to citizens. If you’re considering expatriation, be aware of the U.S. "exit tax", which applies if your net worth exceeds $2 million or if your average income tax over the last five years has been more than $206,000.

Reducing Taxes Through International Tax Planning

Navigating the complexities of cross-border wealth transfer is no small feat, especially when it comes to minimizing tax liabilities. Without proper planning, transferring wealth internationally can result in hefty tax obligations across multiple countries. The key to preserving wealth lies in understanding international treaties and identifying jurisdictions that legally offer tax advantages for estate planning. This knowledge forms the backbone of effective tax strategies.

Double Taxation Avoidance Agreements (DTAA)

Double taxation occurs when two countries impose taxes on the same asset or inheritance. DTAAs help resolve this by assigning primary taxing rights based on factors like the asset’s location (its situs) or your legal domicile. They also allow for foreign tax credits, so taxes paid in one country can offset liabilities in another.

Here’s an important distinction: estate and gift tax treaties are separate from income tax treaties. While the U.S. has around 60 income tax treaties, it has only about 15 estate and gift tax treaties with countries like Australia, Germany, Japan, and the United Kingdom. Some agreements, such as the U.S.–Canada Income Tax Treaty, include estate tax provisions within broader income tax treaties.

| Country | Type of U.S. Treaty |

|---|---|

| Australia | Estate & Gift |

| Canada | Estate (via Income Tax Treaty) |

| France | Estate & Gift |

| Germany | Estate & Gift |

| Japan | Estate & Gift |

| United Kingdom | Estate & Gift |

| Switzerland | Estate |

| Italy | Estate |

Without treaty protection, the tax burden can be severe. For instance, France imposes inheritance taxes of up to 60% on estates exceeding €100,000, while Japan’s inheritance tax can reach 55% on estates over ¥600 million.

Important note: Treaty benefits don’t apply automatically. You must actively claim them in your tax filings to take advantage of the protections. Additionally, confirm where your assets are registered – a "Canadian" account might actually be held in Jersey, potentially altering your tax exposure.

Tax-Advantaged Jurisdictions

While treaties help avoid double taxation, selecting the right jurisdiction can further reduce tax liabilities. Some jurisdictions are known for their favorable tax regimes and are legitimate tools for wealth transfer when used responsibly and in compliance with the law.

Caribbean jurisdictions like the Cayman Islands and St. Kitts & Nevis impose no inheritance, estate, or death taxes. They also offer strong asset protection laws, shielding wealth from creditors and forced heirship claims. The Cook Islands is particularly noteworthy – properly structured trusts there can save heirs up to 40% in estate taxes.

In Europe, Monaco has no inheritance tax for direct descendants, and Liechtenstein uses family foundations to support multi-generational planning with tax efficiency. These jurisdictions often work best when combined with treaty planning.

The type of legal system also plays a role. Common law jurisdictions (like the Cayman Islands and British Virgin Islands) recognize trusts and allow testamentary freedom. In contrast, civil law jurisdictions (such as many in Europe) enforce forced heirship rules but may permit foundations as an alternative.

"Estate planning across borders is a complex game that can cost millions in unnecessary taxes and legal headaches if not done correctly." – Harvey Law Group

Before committing to a jurisdiction, consider its treaty networks with countries where your assets are located, whether it recognizes your chosen trust or foundation structure, and compliance with FATCA and Common Reporting Standard requirements. Political and legal stability also matter to ensure your plan stands the test of time.

Don’t overlook U.S. domestic options. States like Nevada, South Dakota, and Delaware offer tax neutrality, advanced trust features, and strong privacy protections, all without the complications of offshore structures. For U.S. citizens, these states can deliver similar benefits with simpler compliance requirements.

Lastly, setting aside cash reserves or obtaining life insurance can help cover unavoidable foreign taxes and probate fees. This ensures that heirs won’t need to sell assets to access liquidity when it’s most needed. Successful tax planning involves collaboration between estate attorneys, local counsel in asset jurisdictions, and tax experts familiar with international treaties.

Monitoring and Updating Your Wealth Transfer Plan

A wealth transfer plan isn’t a "set it and forget it" arrangement. As tax laws evolve and personal circumstances shift, keeping your plan up-to-date is essential. Without regular reviews, you could face unexpected tax bills, compliance issues, or find that your carefully designed structure no longer works as intended.

Staying Compliant with Changing Regulations

Tax laws and reporting requirements are constantly in flux, especially across different jurisdictions. For example, the U.S. federal estate tax exemption is set to increase to $15,000,000 per person in 2026, up from $13,990,000 in 2025. Similarly, the annual gift tax exclusion will hold steady at $19,000 for 2025 and 2026, while the non-citizen spouse annual gift exclusion will rise from $190,000 to $194,000.

To stay ahead, review your wealth transfer plan annually or after major life changes like moving, getting married, divorcing, or acquiring international assets. For instance, relocating from a common law jurisdiction like the U.S. to a civil law country in Europe could mean your revocable trust is no longer recognized – or worse, it might trigger immediate taxes.

It’s also important to maintain a detailed, jurisdiction-specific inventory of your assets, including bank accounts, real estate, intellectual property, and digital assets like cryptocurrency. This helps you understand which jurisdictions have taxing authority over your holdings and ensures compliance with reporting requirements. For example, U.S. persons must file an FBAR for foreign accounts exceeding $10,000 and meet FATCA reporting thresholds for foreign financial assets.

If you hold assets in multiple countries, coordinate your wills to avoid accidental revocations. For example, a new will in one jurisdiction could unintentionally override provisions in another. To navigate these complexities, work with a cross-border team that includes an estate attorney in your primary domicile, local counsel in countries where you hold assets, and a tax specialist familiar with international treaties. This is particularly crucial in civil law countries like France, Italy, or Spain, where forced heirship rules may override provisions in a U.S. will.

On top of these legal and regulatory reviews, technology offers powerful tools to keep your wealth transfer plan current.

Using Technology for Plan Monitoring

Technology can simplify the management of your wealth transfer plan, especially as digital assets become more common. For instance, digital vaults can securely store cloud credentials, cryptocurrency keys, and legal instructions, ensuring executors have access to critical assets no matter where they’re located. This reduces the risk of heirs being locked out of online accounts or losing access to valuable digital property.

In May 2025, platforms like Casa and Unchained introduced features allowing users to set automated triggers. These triggers transfer digital assets to trust companies after a defined period of inactivity, ensuring a smooth transition if the account holder becomes incapacitated. As Harvey Law Group explained:

"Triggers, alerts, automations, and plans like this could protect online persons’ money and property without compromising security during their lifetime." – Harvey Law Group

Automated alerts can also help you stay on top of tax law and treaty changes, enabling quicker responses to shifting regulations. For added security, keep both digital and physical copies of your documents, with one set stored outside your primary country of residence. Regularly updating your digital asset inventory ensures your plan reflects changes in residency, domicile, or global regulations like FATCA and FBAR.

Finally, consider appointing a "digital executor" specifically to manage online accounts and passwords. This role is separate from your general estate executor and requires someone with technical expertise to handle cryptocurrency wallets, online businesses, and cloud-based assets, which often have unique recovery procedures.

Conclusion

Transferring wealth across borders is no small feat – it requires a well-thought-out strategy to navigate conflicting legal systems, heavy tax liabilities, and ever-changing regulations. As Suzanne L. Shier aptly noted, "The structure that works seamlessly in Dallas may create chaos in Dubai". Without careful planning, families risk double taxation, forced heirship complications, and severe financial penalties.

Estate taxes can be especially steep in many major jurisdictions. The challenge is compounded by the fact that the U.S. has estate tax treaties with only 15 countries, leaving most families exposed to the possibility of double taxation. Add to that the complexity of managing globally dispersed assets, and it’s clear why proper planning is essential.

To address these challenges, three key strategies are critical: assembling a multi-jurisdictional team (including an estate attorney, local counsel, and cross-border tax specialist), keeping an up-to-date inventory of assets, and conducting annual reviews. This level of coordination ensures, for example, that a revocable trust won’t inadvertently trigger taxes when relocating or that a U.S. will doesn’t conflict with a French estate plan. Beyond legal and tax planning, having immediate access to funds is equally important.

Liquidity plays a vital role in wealth transfers. Setting aside cash reserves or securing life insurance can help cover foreign probate fees and inheritance taxes, avoiding the need to sell family assets under pressure. As Gabriele Di Girolamo of Julius Baer puts it, "The core objective should be to ensure that the family’s wealth is passed in line with the wishes of the wealth creators". With diligent planning, expert advice, and regular updates, families can protect their legacy and ensure it endures across borders and generations.

FAQs

Which country gets to tax my estate if I live and hold assets in multiple countries?

Your estate might be taxed in the country where you are domiciled. Domicile refers to the place you intend to live indefinitely. Additionally, taxes may apply in countries where your assets are located. For U.S. citizens or residents, estate tax applies to worldwide assets. It’s important to review local laws to fully understand your tax responsibilities across different jurisdictions.

Do I need separate wills for each country where I own property?

Yes, it’s a good idea to have separate wills for each country where you own property. This approach helps ensure your wishes are carried out according to the specific legal requirements of each jurisdiction. Laws governing wills can vary widely between countries, and having a localized will can make the process smoother and more straightforward. To avoid complications or conflicting provisions, consult an experienced legal professional who can guide you through the process and help manage your estate effectively across different countries.

How can my heirs access my cryptocurrency if something happens to me?

To make sure your heirs can access your cryptocurrency, it’s crucial to include clear, detailed instructions in your estate plan. This should cover the location of your wallets, private keys, and seed phrases. Keep this information in a secure place and only share it with people you trust completely. You can also use tools like multi-signature wallets or smart contracts to streamline and automate the transfer of these assets, ensuring your digital wealth remains both accessible and secure after your passing.