April 22, 2013

By: Kelly Diamond, Editor

Before we cry for more government oversight in the financial industry, we should be asking: “Who will regulate the regulators over at the SEC?”

And before we look to more money, or more staff, or more rules, we should be asking: “Would any of those things address the root of the gaping holes in our regulatory system over at the SEC?”

Aside from the economic burdens associated with centralized regulations, there exist some SERIOUS ethical issues. On a small scale, you have these regulations calling for licenses in “flower arranging” or “hair braiding” or “interior design” which are really just meant to be economic inconveniences – or ideally obstacles — for those wishing to pose a competitive threat to the existing purveyors out there. But you also have regulations which lead to instances where 1,600 pounds of venison is confiscated and destroyed after being donated by a private owner to a homeless shelter because the meat wasn’t properly shipped. There was no actual poison or toxin, nor were there any victims or casualties from said meat. It just wasn’t properly shipped. So in the name of safety, the homeless will not receive that meat, but instead will dig around in a dumpster for food.

Aside from the economic burdens associated with centralized regulations, there exist some SERIOUS ethical issues. On a small scale, you have these regulations calling for licenses in “flower arranging” or “hair braiding” or “interior design” which are really just meant to be economic inconveniences – or ideally obstacles — for those wishing to pose a competitive threat to the existing purveyors out there. But you also have regulations which lead to instances where 1,600 pounds of venison is confiscated and destroyed after being donated by a private owner to a homeless shelter because the meat wasn’t properly shipped. There was no actual poison or toxin, nor were there any victims or casualties from said meat. It just wasn’t properly shipped. So in the name of safety, the homeless will not receive that meat, but instead will dig around in a dumpster for food.

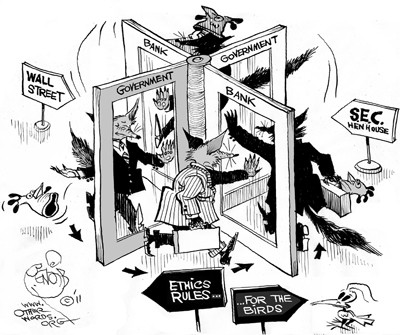

Indeed, economic burdens and ethical issues are woven throughout our regulatory culture. But those stories are small potatoes compared to the elites over at the federal government agencies like the SEC (Securities and Exchange Commission). The SEC is who supposedly oversees our “too-big-to-fail” banks. They make the rules and enforce them within the financial industry. Having the agency is all well and good, if you’re into that sort of thing, but having an agency is no difference than having insurance: it doesn’t actually entail meaningful action. An agency is a means of creating protections, presumably, for individuals operating within the markets. Insurance is a means of paying for services which could help you fix what’s ailing you. But if no one actually enforces the rules consistently, then that’s the same as bleeding out in a hospital waiting room. Insurance isn’t the same as care any more than a regulatory agency is the same as actually regulating.

An investigation conducted by POGO (Projects on Government Oversight) through a Freedom of Information Act request found that 419 former SEC employees filed at least 1,949 disclosure statements indicating they planned to represent a private sector client with an SEC business. These disclosures are requisite in the first TWO years upon leaving the SEC. So between 2001 and 2010, over four hundred regulators filed nearly two thousand disclosure statements?

My first inclination is to call shenanigans: Conflict of Interest! You have people drafting regulations for the SEC just convoluted enough to where only this select few know the loopholes… which they then use as a lucrative in into the private sector? Or worse yet, you have this incestuous group who wind up lobbying on behalf of the banks to the newbies over at their old stomping grounds to the point where exemptions are made, a blind eye is turned, and waivers are issued. So the rules on the books aren’t enforced, and new rules are not made… I gotta ask: What exactly is your purpose here, SEC?

Here are a few examples found by POGO:

- UBS one of the giants of Swiss banking, was charged on three different occasions for violating the SAME anti-fraud laws… and in each of those times was also granted a waiver.

- “Since 2003, the SEC granted exemptions to JPMorgan and its subsidiaries when charged with alleged misconduct relating to mortgage securities products, transactions with Enron, initial product offerings, and research analyst conflicts of interest.”

- When former SEC Chair, Mary Shapiro tried to regulate money market mutual funds after the 2008 crisis, she was approached by six different SEC top executives including an SEC Commissioner and an SEC lawyer. She backed down.

You’ll be happy to know that Mary Shapiro now works for Promontory Financial Group, LLC. She received a hearty bonus when she left the self-appointed Wall Street watchdog group, Financial Industry Regulatory Authority, for the Securities and Exchange Commission (SEC). She was useless in the SEC, but she might very well come in handy for her new private employers. The good news is, as she clarified, the door isn’t revolving since she has no intention of going back into government service. Why don’t I feel consoled by this?

If over half the waivers issued and granted were petitioned by former SEC regulators now working in the private sector, how on earth are we meant to rely on this agency to prevent future crises?

SEC spokesman, John Nester, admits the Government Accountability Office studied the SEC’s revolving door, as required under Dodd-Frank, “and described the SEC’s controls as strong and consistent with those of other agencies.” Are we meant to feel better about this? So should we be scrutinizing the Environmental Protection Agency, to see if former regulators wind up working for factories? Or even the Department of Defense, to see if high ranking veterans make their way into places like Haliburton?

Can we expect that ALL regulatory agencies provide redacted or incomplete information? There’s this lukewarm requirement for SEC employees to “cool off” prior to joining the ranks of SEC businesses in the private sector. So there would be a period of time where the SEC alumni would abstain from working with entities which potentially pose a conflict of interest. OR NOT! Evidently, this “cooling off” period is about as arbitrary as its regulatory enforcement. Middle managers, analysts, economists and attorneys may be exempt.

One of the reporters responsible for bringing this corruption to light is Zach Carter from the Huffington Post. He suggests making the regulatory position MORE prestigious by offering more compensation to its employees. He claims that the folks at the SEC are stretched thin and have this reputation of being a dorky group. Make regulators feel better about themselves, give them better compensation, and this revolving door thing will fizzle away? He realistically acknowledges how ill-received such a solution would be to the American public, but still… I have a hard time believing that low compensation and self-esteem are the root to this insidious problem.

Earlier this month, both the House and Senate voted to gut out one of the major provisions in the STOCK (Stop Trading on Congressional Knowledge) Act. This provision would’ve made about 28,000 federal officials’ financial records available through an online searchable database, ultimately holding them accountable for any insider trading. For example, when Nancy Pelosi and her husband made over a 200% return on a VISA IPO. That sort of thing. Wait, searchable databases with personal financial information sounds really familiar… I’m wondering why elected PUBLIC SERVANTS don’t want their information out there for individuals to see, but think it’s okay to do so with private citizens.

I don’t think this has anything to do with self-esteem issues or compensation packages. This has to do with personal gains through public means. They build their careers on the public dime, rig it in such a way that they can later sell their knowledge of and influence within a given agency to make their money… or make investments based on information they know about a given piece of legislation and how that will affect a given stock.

Zach Carter, like so many others, think it’s still about money… or worse still about feelings! I said this before, but here is the actual movie quote which sums up quite nicely the reality of all this corruption:

“There’s a war out there, old friend. A world war. And it’s not about who’s got the most bullets. It’s about who controls the information. What we see and hear, how we work, what we think… it’s all about the information! The world isn’t run by weapons anymore, or energy, or money. It’s run by little ones and zeroes, little bits of data.” ~ Cosmo (played by Ben Kingsley in the 1992 movie Sneakers)