Financial privacy is disappearing fast. Governments and corporations now monitor financial activity more closely than ever, from bank accounts to cryptocurrency holdings. Automated systems like FATCA, CRS, and the Crypto-Asset Reporting Framework allow authorities to collect and share financial data globally, leaving little room for secrecy. Even corporations collaborate with agencies like the FBI, using transaction data to flag activities.

To protect your wealth, consider these key strategies:

- Offshore Trusts & Companies: Jurisdictions like the Cook Islands or Nevis offer legal tools to shield assets from lawsuits and creditors.

- Digital Privacy Tools: Use encryption, VPNs, and hardware wallets to secure your communications and cryptocurrency.

- Compliance: Always meet reporting requirements (e.g., FBAR, FATCA) to avoid penalties.

Timing is critical – establish protective measures before legal or financial issues arise. With proper planning, you can safeguard your assets in today’s surveillance-heavy environment.

How Digital Surveillance Exposes Your Financial Assets

Government programs and corporate systems play a significant role in exposing financial assets through automated data collection and monitoring.

Government Surveillance: PRISM, FATCA, and CRS Reporting

FATCA and CRS have reshaped how tax enforcement operates. Instead of relying on specific information requests tied to suspected wrongdoing, these programs enable automatic, yearly exchanges of financial data between countries. Foreign banks are required to scrutinize their records for indicators of U.S. connections – such as U.S. birthplaces or phone numbers – and report relevant accounts to the IRS.

The penalties for non-compliance are steep. Banks that fail to comply face a 30% withholding tax, while individuals may encounter multiple fines. The IRS employs AI to cross-check reported data with tax returns, flagging inconsistencies automatically. FATCA alone was projected to generate $8.7 billion in additional tax revenue over 11 years.

These measures significantly erode traditional privacy norms. Both FATCA and CRS require trusts and foundations to disclose "Controlling Persons", which include settlors, trustees, protectors, and beneficiaries. This effectively unveils the individuals behind private wealth structures. The IRS then uses AI to compare this electronic data with tax returns and FBAR reports, quickly identifying discrepancies. Attorney Janathan Allen explains:

"The IRS is receiving direct electronic information from FFIs, cryptocurrency exchanges, and wallets here in the U.S. and around the world, providing information about U.S. taxpayers, including their account information, balances, and transactions".

The reach of FATCA is vast, affecting an estimated 5.7 to 9 million U.S. citizens living abroad. The resulting pressure has driven record levels of citizenship renunciations, with 6,707 cases recorded in 2020 alone.

But it doesn’t stop with government oversight – corporate data practices add another layer of complexity to financial privacy.

Corporate Data Collection and Security Breaches

Corporations also play a role in financial surveillance. Alongside complying with government reporting requirements, financial institutions often actively assist in monitoring efforts. For example, a March 2024 House Judiciary Committee report revealed how banks like Bank of America, Charles Schwab, HSBC, Barclays, U.S. Bank, and PayPal collaborated with FinCEN and the FBI. They used keyword filters to track transactions involving terms like "MAGA" and "TRUMP", as well as purchases at retailers such as Cabela’s and Dick’s Sporting Goods. This was done under the third-party doctrine, which allows government agencies to access financial data held by banks without needing a warrant.

The House Judiciary Committee criticized this practice, stating:

"The FBI has manipulated the Suspicious Activity Report (SAR) filing process to treat financial institutions as de facto arms of law enforcement".

Cryptocurrency platforms face even more intense scrutiny. In 2021, the IRS obtained court approval for "John Doe summonses" targeting Kraken and Circle users who had transacted $20,000 or more between 2016 and 2020. This followed a similar 2016 summons against Coinbase, which sought records for 14,000 accounts. In fiscal year 2021 alone, the IRS Criminal Investigation Division seized $3.5 billion in cryptocurrency – 93% of the agency’s total asset seizures. By mid-2023, nearly 15,000 "soft letters" had been sent to crypto users flagged through exchange data.

Beyond government surveillance, corporate data collection poses its own risks. Financial platforms and tech companies gather extensive personal information, including marital status, family details, education, income levels, and even religious affiliation. Samuel Levine, Director of the FTC’s Bureau of Consumer Protection, commented:

"The tech industry’s monetization of personal data has created a market for commercial surveillance… with inadequate guardrails to protect consumers".

This creates a twofold risk: your financial data is automatically reported to tax authorities while also being stored by corporations with varying levels of security. For those aiming to protect their assets – especially high-net-worth individuals – it’s crucial to recognize that any activity conducted through centralized platforms is likely visible to regulatory bodies.

sbb-itb-39d39a6

Offshore Strategies to Protect Your Wealth

In today’s world of constant digital oversight, offshore structures offer a legal way to shield your assets from prying eyes. By creating jurisdictional separation, these strategies make it much harder for creditors or litigants to gain access to your wealth.

For example, a creditor who wins a U.S. court judgment can’t automatically enforce it in places like the Cook Islands, Nevis, or Anguilla. They’d need to file a new lawsuit in the foreign jurisdiction, facing stricter evidence requirements and much shorter statutes of limitations – often just one or two years for claims like fraudulent conveyance.

Offshore Trusts: Privacy and Asset Protection

An offshore asset protection trust is a powerful tool for safeguarding assets. These irrevocable trusts are set up in foreign jurisdictions and managed by independent trustees with no U.S. connections. Since the trustee legally owns the assets and operates under foreign laws, U.S. courts can’t compel them to make distributions.

To be effective, an offshore trust must meet specific criteria: it must be irrevocable, have an independent trustee, include a spendthrift clause, and allow the trustee to control distributions. Jurisdictions like the Cook Islands are well-known for their strong legal frameworks, experienced trustees, and courts that rigorously protect these trusts from creditor challenges. Other locations such as Nevis, Belize, and Anguilla have adopted similar laws to bolster asset protection.

From a tax perspective, offshore trusts classified as foreign grantor trusts remain neutral. Contributions are not taxed, but any income generated is reported on Form 1040 and taxed accordingly. However, under FATCA regulations, the trust’s existence must be disclosed to the IRS annually.

One standout feature of these trusts is the anti-duress clause. This provision prevents trustees from making distributions if you’re under creditor pressure or a court judgment. Some trusts even include a "flee provision", requiring assets to be moved to another jurisdiction if a creditor files a claim, adding another layer of protection.

That said, offshore trusts are best suited for individuals with significant assets. The setup costs and ongoing trustee fees can be substantial, making them impractical for smaller estates. However, you don’t have to overhaul your entire financial strategy. You can keep your current U.S.-based money manager for investment decisions, while the offshore trustee retains the final say on distributions.

To enhance the privacy and functionality of these trusts, many people pair them with offshore companies.

Setting Up Privacy-Focused Offshore Companies

Offshore companies, such as Anguilla International Business Companies (IBCs), add another layer of privacy, especially when combined with offshore trusts. These companies are often established in jurisdictions that don’t participate in the Common Reporting Standard (CRS), avoiding automatic financial data sharing that most global banks are required to follow.

When you pair an offshore company with a non-CRS bank, you create a structure that significantly limits your financial visibility. For a deeper dive into selecting the right institution, consult our offshore banking report. This reduces your exposure to digital surveillance and protects your financial activities from being easily tracked.

Setting up an offshore company involves selecting a jurisdiction, filing the necessary formation documents, appointing directors (professional nominees can be used for added privacy), and funding the entity. These companies can directly hold assets or act as the operational arm of an offshore trust, giving you control over day-to-day management while the trust provides legal protection.

Timing is critical. These structures must be established in good faith before any creditor issues arise. Setting them up after a lawsuit or creditor claim has been filed can lead to fraudulent conveyance challenges, potentially unraveling the entire arrangement.

Digital Tools to Protect Your Financial Privacy

While offshore structures provide legal protection for your assets, digital tools focus on securing your financial communications and data. Together, they form a strong barrier against surveillance.

Encryption and Secure Communication Tools

To protect your communications, start with email encryption tools like PGP (accessible through utilities like Kleopatra) or the more user-friendly, cross-platform Keybase. However, keep in mind that Keybase’s ownership may raise privacy concerns.

For real-time messaging, opt for end-to-end encrypted platforms like Signal. Unlike Telegram or X (formerly Twitter), which only encrypt data in transit, Signal encrypts everything by default and avoids collecting metadata about who’s communicating. Harlo Holmes, Director of Digital Security at the Freedom of the Press Foundation, emphasizes the importance of metadata:

"Metadata matters".

Signal also offers disappearing messages, which can self-delete in as little as five seconds – an added layer of privacy.

When it comes to securing local data, use full disk encryption tools like FileVault (macOS), BitLocker (Windows), or VeraCrypt (Windows/Linux). For highly sensitive tasks, specialized operating systems like Tails (which routes all traffic through Tor and leaves no trace) or Qubes OS (which isolates tasks in virtual compartments) offer advanced security. These tools lay the groundwork for a secure digital environment, complementing other privacy measures.

VPNs and Hardware Wallets

Beyond encrypted communication, tools like VPNs and hardware wallets add extra layers of protection for your online and financial activities.

A VPN with a strict no-logging policy acts as a secure intermediary, masking your IP address and reducing digital profiling. Harlo Holmes highlights the importance of VPNs:

"Having a VPN in your pocket that doesn’t do any logging at all of your activity and also provides robust controls is the next best thing [to Tor]".

For cryptocurrency security, hardware wallets keep your private keys offline, safeguarding them from malware or phishing attacks. Devices like the Ledger Nano X, which uses CC EAL5+ certified chips, support over 5,500 coins and tokens. Meanwhile, the Trezor Safe 7 boasts quantum-ready architecture to prepare for future threats from quantum computing. To ensure maximum safety, always store your hardware wallet’s recovery seed phrase offline in a secure physical location.

Multi-Jurisdictional Diversification

Diversifying your assets across multiple jurisdictions adds a layer of protection against localized risks like aggressive regulations or surveillance. For example, if one country bans cryptocurrency transactions or imposes strict capital controls, assets in other jurisdictions remain unaffected.

In February 2026, an investor successfully transferred a multi-million-dollar Bitcoin portfolio to a Cook Islands trust using an offshore LLC. This move ensured asset segregation and protection from local legal challenges.

To further protect your holdings, consider combining trusts, offshore LLCs, and nominee services to keep beneficial ownership out of public registries. Jurisdictions like Nevis, Singapore, Liechtenstein, and the Cook Islands are known for offering strong legal protections tailored to digital assets. Pairing these legal structures with tools like hardware wallets and VPNs creates a comprehensive defense system. As Offshore Protection aptly states:

"Establishing an offshore structure today means reducing panic tomorrow".

Creating Your Asset Protection Plan

After exploring offshore structures and digital security tools, the next step is designing a customized asset protection plan. Start by reviewing your current financial assets before initiating any offshore transfers. For U.S. citizens, ensure compliance with mandatory reporting requirements like FBAR (FinCEN Form 114) and FATCA (Form 8938) if you hold foreign accounts. Keep detailed records of all offshore transfers, completing them before any potential creditor claims arise.

Consider domestic options as well. Tools like umbrella liability insurance, homestead exemptions, or Domestic Asset Protection Trusts (DAPTs) can address immediate needs. At the same time, ensure you maintain enough onshore liquidity to cover operating expenses, legal fees, or potential settlements. As one expert aptly put it:

"The most durable plans combine domestic protection (insurance, estate planning, entity structure) with limited, carefully documented offshore elements only after full legal and tax review." – Author Note, finhelp.io

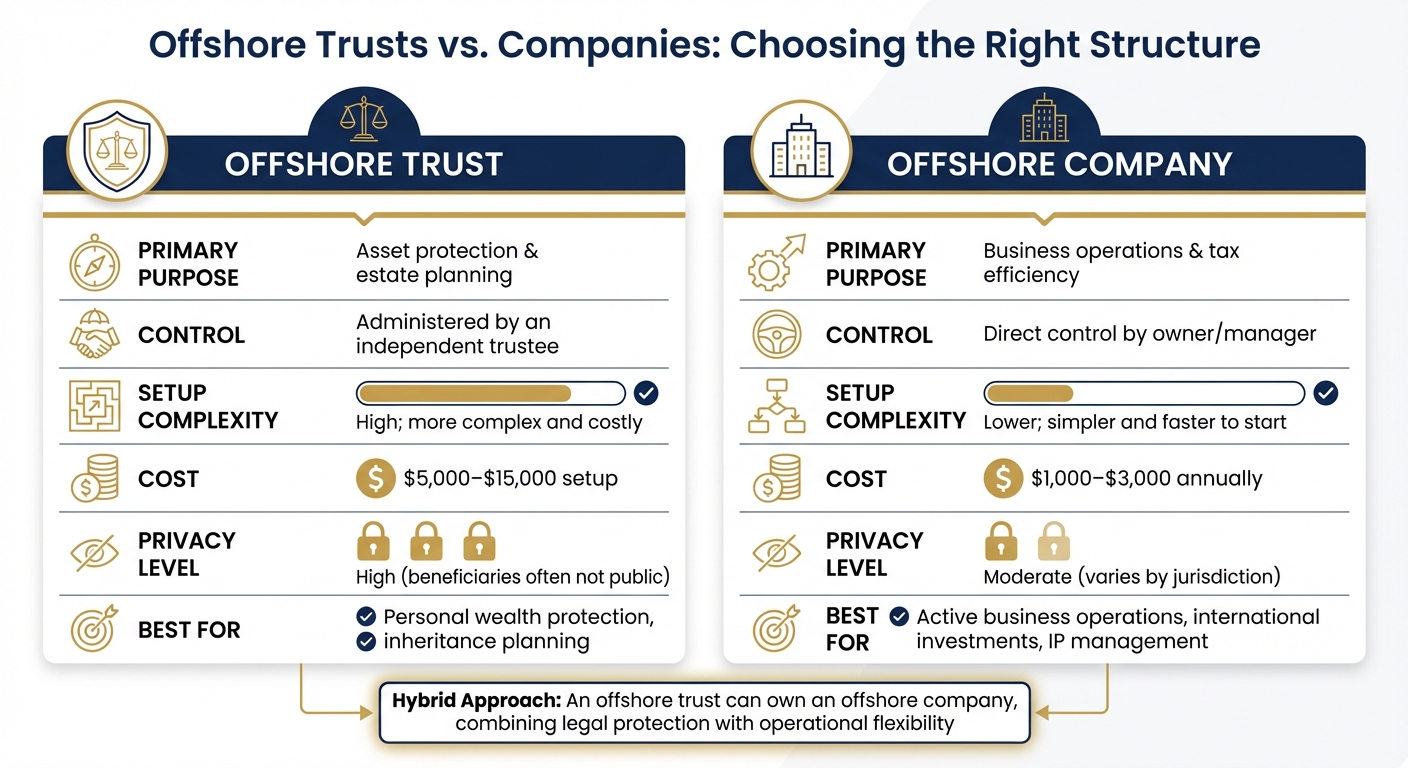

Comparing Offshore Trusts and Companies

When deciding between an offshore trust and an offshore company, your goals will guide the choice. Offshore trusts are ideal for safeguarding personal wealth and inheritance, as they legally separate assets from the settlor through an independent trustee. Offshore companies, such as LLCs or IBCs, are better suited for active business operations, managing intellectual property, or handling international investments. In some cases, a layered approach is used – an offshore trust may own an offshore company, combining the trust’s legal protection with the company’s operational flexibility.

| Feature | Offshore Trust | Offshore Company |

|---|---|---|

| Primary Purpose | Asset protection & estate planning | Business operations & tax efficiency |

| Control | Administered by an independent trustee | Direct control by owner/manager |

| Setup Complexity | High; more complex and costly | Lower; simpler and faster to start |

| Cost | $5,000–$15,000 setup | $1,000–$3,000 annually |

| Privacy Level | High (beneficiaries often not public) | Moderate (varies by jurisdiction) |

For U.S. citizens, the Bridge Trust® model offers a practical solution. It begins as a domestic grantor trust for tax simplicity and transitions to a full offshore structure in the Cook Islands if legal threats arise. A notable example of offshore protection’s effectiveness is the 2008–2013 case of United States v. Grant. In this case, the IRS was unable to recover $36 million held in Cook Islands and Jersey trusts, highlighting how properly structured offshore plans can withstand legal challenges.

Once you’ve selected the right structure, securing professional guidance is crucial for long-term success.

Working with Experts for Long‑Term Solutions

Attempting to set up offshore structures without professional assistance can lead to serious legal and tax risks. It’s essential to work with dual‑jurisdictional legal counsel – attorneys familiar with both U.S. and offshore laws – to draft documents and ensure compliance with local regulations. A qualified tax attorney or CPA is equally important for navigating global tax obligations and reporting requirements. Always seek formal, written opinions from both domestic and offshore advisors before funding any offshore structure.

Collaborate with reputable service providers, including trustworthy trustees, independent directors, and regulated banks. Avoid unverified providers that focus solely on secrecy. Banking is another critical factor – verify that financial institutions in your chosen jurisdiction will accept your type of income, particularly if it involves cryptocurrency, before forming an offshore entity. Global Wealth Protection offers tailored strategies, specializing in offshore company formation in Anguilla, offshore trusts for high-net-worth clients, and private consultations. As one advisor noted:

"Without banking, your company is a shell. With both, it becomes a powerful tool for privacy, asset protection, and global operations." – OCBF Consulting

Keep in mind that lawful offshore planning is entirely legitimate, but hiding assets or failing to report them is not. By working with experienced advisors, you can ensure tax transparency, regulatory compliance, and long-lasting legal protection.

Conclusion: Taking Action to Protect Your Financial Privacy

Now is the time to put protective strategies into motion. In an age of increasing digital surveillance, safeguarding your wealth requires a fresh approach. The old methods of offshore secrecy have evolved into legally compliant strategies that emphasize jurisdictional diversification and smart structuring practices.

A solid protection plan should include three key components: offshore structures like trusts or LLCs in jurisdictions such as the Cook Islands or Nevis, digital security tools like hardware wallets and encryption, and strict compliance with reporting regulations.

As The Nestmann Group explains:

"It’s not about hiding money; it’s about using internationally recognized legal and financial tools to build stronger, more resilient barriers around what you’ve worked hard to earn."

This layered approach – blending strategic offshore solutions with strong digital security – offers a practical way to shield your assets in today’s surveillance-heavy environment.

Timing is critical. Setting up offshore structures before legal troubles arise can help you avoid complications like fraudulent transfer claims. Consider this: in 2023 alone, U.S. courts saw about 5 million new lawsuits, highlighting the constant risk of litigation for anyone with substantial assets.

Seek guidance from legal and tax professionals who are well-versed in both U.S. and offshore regulations. Firms like Global Wealth Protection specialize in creating offshore companies in Anguilla, establishing trusts for high-net-worth individuals, and providing private consultations to navigate these complex waters. While the upfront cost of a Cook Islands trust – around $29,000 – may seem steep, it’s a small price to pay compared to the potential financial and legal pitfalls of going it alone.

Don’t wait until restrictions limit your options. Acting now ensures you can secure your wealth while you still have the flexibility to do so.

FAQs

Can I use offshore trusts legally and still stay compliant?

Yes, offshore trusts are legal as long as they are established and managed in line with the relevant laws and regulations. To stay compliant, you’ll need to fulfill U.S. tax reporting obligations, such as FATCA (Foreign Account Tax Compliance Act) and FBAR (Report of Foreign Bank and Financial Accounts) requirements. Careful management and strict adherence to these rules are crucial to avoid any legal complications.

What’s the best time to set up an offshore structure?

The ideal moment to set up an offshore structure is as early as you can – preferably before encountering risks like legal disputes, economic uncertainty, or political changes. Taking action early helps safeguard your assets and minimizes exposure to unexpected challenges.

How do I protect crypto from tracking and hacks?

To keep your cryptocurrency safe, it’s crucial to avoid reusing wallet addresses. Since blockchain transactions are publicly recorded and traceable, reusing addresses can make it easier for others to link your transactions. To maintain anonymity, consider using privacy tools like CoinJoin or opting for privacy-focused coins.

For better security, store your cryptocurrency in cold wallets – these are offline and much harder for hackers to access. Always enable multi-factor authentication (MFA) for an added layer of protection and keep your private keys secure. Additionally, multi-signature wallets can offer extra security by requiring multiple approvals for transactions. Lastly, regularly update your security protocols to stay ahead of potential tracking methods and cyber threats.