April 14, 2014

By: Kelly Diamond, Publisher

This past Saturday, I got a personal taste of fractional reserve banking.

This past Saturday, I got a personal taste of fractional reserve banking.

I recently switched car insurance companies, so my former policy prorated the monthly premium, and paid me out the balance. They issued me a check in the amount of $86.50. I went to deposit it at my credit union, but they wouldn’t cash it out or deposit it because for whatever reason, the damn insurance company decided to put my boyfriend’s name on it as well. He’s a member at a different credit union.

The teller told me to take it to the bank on the check… which was Bank of America… to cash it out. Fair enough. If my bank won’t collect that money, then I’ll do it myself.

So I go to Bank of America, and what happens? The lady says there is a $5 fee for cashing out the check.

*Insert loud screeching sound of brakes here*

What? I said, “Wait just a second. Does this same fee apply if my bank collected it on my behalf?”

“No,” the lady said, “I think the fee is there to encourage you to either bank here, or use your bank for such services.”

So I said, “But the check itself directs me HERE to collect on this debt. This is YOUR debt. You have to honor this check for your client.”

“And we will… for a $5 fee.”

“Interesting. Can someone who is repaying their mortgage do that as well? I mean, they would send you a notice, and just let you know that if you want to collect on their monthly mortgage payment, they are happy to pay it… but for a nominal fee. A change in policy to encourage you to go directly to their house and spare them the cost of a stamp and envelope or the hassle of setting up autopay.”

She chuckled.

I said, “So, your account holders give you money… FOR FREE… and often even pay fees for the privilege of lending you money so that you can lend it out at an interest rate. The money becomes yours, with the understanding that if the account holder needs it, you will honor their debt in good faith. So they use their checks and debit cards, expecting you to pay their debts via the debt you have with them… and you do… for only for a fee to the person collecting? You do realize this is YOUR debt… not the debt of my insurance company. Your check was not accepted at my bank, so it’s worthless there. And you just deflated the value of this check by $5 in order to honor it.”

At which point my boyfriend chimes in and says, “Ooooooh… it’s because you are taking physical, hold-‘em-in-your-hands FRNs (Federal Reserve Notes) from the bank.”

The teller gave an uncomfortable half-smile.

“What do you mean?” I asked.

“Think about it,” he replied. “It’s one thing to just update the numbers on a computer and play in 1’s and 0’s. It’s a different story when you actually come to collect on the money. When a loan shark lends money, he can sell his mark to someone else to pay off his own debts. But money still hasn’t had to change hands yet. It’s still just a floating IOU. Knee caps don’t get busted until real, tangible money comes into play. If you were to just go to your credit union and cash the check there, then all Bank of America has to do is delete $86.50 from its ledgers, and all your credit union has to do is add $86.50 to theirs. Bank of America hasn’t lost any physical FRNs yet. Your credit union has, but it has replaced it with a debt from Bank of America, so it feels satisfied because it bought the mark.”

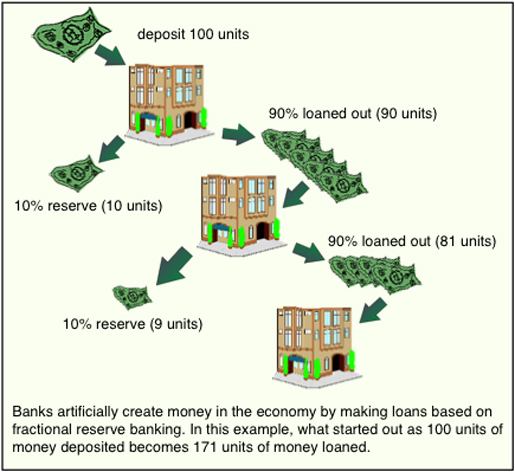

It hit me at that point that there is a serious scare regarding a run on the banks. IF every bank were to just honor a request to cash a check, or if everyone insisted upon paying all their debts in cash that would put the banks in quite a little pickle. The real irresponsibility of American banks isn’t just that they unscrupulously lent to sub-prime borrowers. That is irresponsible, but not totally uncorrectable. The irresponsibility of the banks is that they continue to circulate money that doesn’t really exist!

That we came off the gold standard and no longer have anything tangible backing the FRN is one thing. A very bad thing, but only one thing. But that we now do not have the FRNs to back up the 1’s and 0’s takes things to an entirely new threat level. What next when the 1’s and 0’s can no longer be supported? Am I meant to just take their word for it?!

You might be asking, “Well, isn’t that the same as bitcoin?” And I would then answer, “Absolutely not.”

- Bitcoin NEVER sold itself as anything BUT 1’s and 0’s.

- It is also an optional currency. You don’t have to use it, because typically those who accept bitcoin, accept various other forms of currency as well.

- More importantly, bitcoin is finite. It cannot be mined ad infinitum. So, much like gold, once it’s been fully mined, that’s it. Now the value just starts to go up, and we start to deal in things like micro or milli-bitcoins or out 8 decimal places to what is called a “Satoshi”.

There’s nothing stopping someone from irresponsibly lending to another. I lent my favorite CDs to people and never got them back. Lesson learned. And that doesn’t collapse my personal economy. I’ve even trusted people to honor financial agreements, and they haven’t… but I can still recover from that. What I cannot do is take out so many lines of credit, that I cannot offset it with income. That’s a problem.

I knew for a while that FRNs were nothing more than IOUs. We have all been buying and selling marks. But just when you thought your money couldn’t be any more worthless… well… check out this quick run-down of the history of the FRN inscriptions:

1913 . . . TO . . . 1934

“Redeemable in Gold on demand at the United States Treasury or in Lawful money, at any Federal Reserve Bank.” “Will pay to the bearer on demand one dollar.”

1934 . . . TO . . . 1968

“This note is legal tender for all debts public and private and is redeemable in lawful money at the United States Treasury, or any Federal Reserve Bank.” “Will pay to the bearer on demand one dollar.”

1968 . . . TO . . . 1998

“This note is legal tender for all debts, public and private”

So basically, the FRN is only good for one thing: paying off debts. It’s not actually redeemable for anything because in point of fact, it is worthless. So if only 8% of the world’s money exists as PHYSICAL cash, of course there will be a fee for removing FRNs from a bank you don’t patron.

We’re just trading marks. Nothing more. We can never cash in. Not on anything that backs the FRN, and in some cases you can’t even cash in your 1’s and 0’s for FRNs. People are waking up. The dream will soon end. And the imagination that is currently propping up this system will eventually cease to do so.

I think at this point, it’s more apparent and obvious than it is the crumbs off the table of some foil hat conspiracy theorist. It’s not hype to say that the FRN has nothing backing it like gold or silver. It’s just documented, historic fact. It’s not hype that there are more 1’s and 0’s than physical money in circulation. It’s the educated estimation and consensus of most economists. It’s not hype that China was once the country that bought the most US Treasuries and has since started to back off. It’s not even hype, but rather verifiable fact, that the FDIC doesn’t have sufficient funds to insure every account holder in the US should there be a run on the banks tomorrow. But all these things put together makes for a VERY grim economic future for the US. Can anyone even demonstrate how this could end well? Or how these are the indicators of a STABLE monetary system?

What is the solution? Well, I don’t care to “fix” the entire monetary system. But what can each individual do? They can diversify their holdings out of the US Dollar. There are not only other valuable stores of wealth, there are better banks. You aren’t stuck. You always have choices. And no, there is nothing patriotic about staying on a sinking ship.