Offshore banking in 2026 is entirely legal for U.S. citizens – as long as you comply with IRS reporting requirements like FATCA (Form 8938) and FBAR (FinCEN Form 114). These accounts offer benefits like asset protection, currency diversification, and financial flexibility, especially for expats, digital nomads, and international entrepreneurs. However, the landscape has shifted toward strict transparency, with global regulations like CRS 2.0 expanding oversight to include digital wallets and Central Bank Digital Currencies.

Key steps to open an offshore account:

- Understand Reporting Obligations: U.S. citizens must disclose foreign accounts with balances exceeding $10,000 (FBAR) or $50,000–$400,000 (FATCA thresholds vary by residency and filing status).

- Choose a Suitable Jurisdiction: Switzerland, Singapore, and the Cayman Islands remain top options, offering political stability, strong legal protections, and FATCA compliance.

- Prepare Documentation: Gather a valid passport, proof of address, tax forms (e.g., W-9), and source-of-funds evidence.

- Select a Compliant Bank: Work with banks that comply with FATCA and have experience handling U.S. clients.

- Complete the KYC Process: Transparency is critical – be ready to explain your financial background and plans.

Offshore accounts are not about secrecy but about legally managing global assets while meeting all U.S. tax obligations. Non-compliance can result in steep penalties, so consult a tax advisor before proceeding.

US Reporting Requirements and Legal Compliance

The IRS and FinCEN have strict rules for reporting foreign financial assets, and failing to comply can lead to hefty penalties. As international tax attorney Lawrence Brown explains:

"Under federal law, U.S. taxpayers, whether residing in the U.S. or abroad, are required to disclose their offshore accounts to the federal government annually".

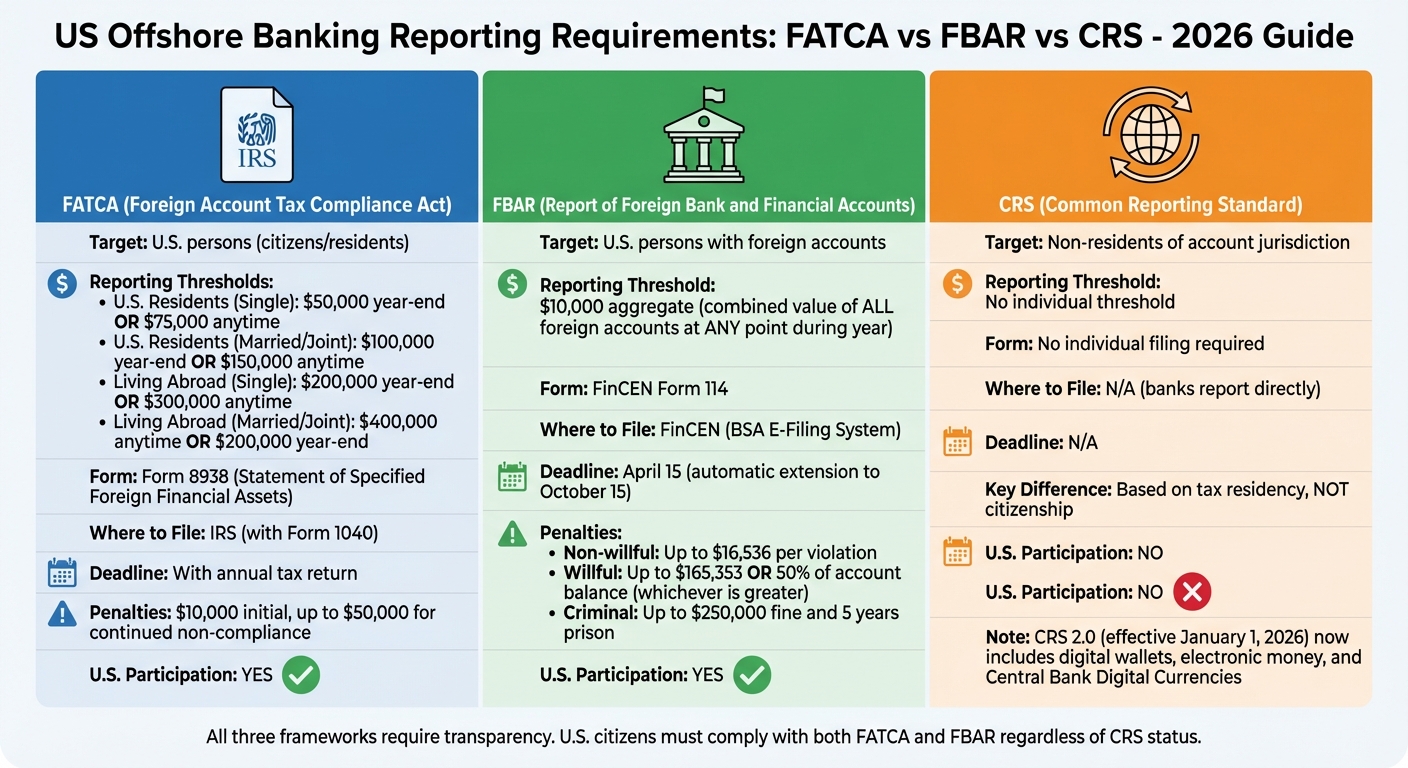

Three key frameworks shape the reporting landscape for offshore accounts: FATCA (Foreign Account Tax Compliance Act), FBAR (Report of Foreign Bank and Financial Accounts), and CRS (Common Reporting Standard). Each has its own rules, thresholds, and deadlines, which are outlined below.

FATCA: What US Citizens Need to Know

FATCA, introduced in 2010, aims to combat tax evasion through foreign accounts. It requires both individuals and foreign financial institutions to report details of U.S. account holders to the IRS. Foreign banks are obligated to identify U.S. clients, collect their Social Security Numbers, and share this information with the IRS under Intergovernmental Agreements.

For individuals, filing Form 8938 (Statement of Specified Foreign Financial Assets) is mandatory if foreign financial assets exceed certain thresholds. For 2026, the thresholds are:

- U.S. residents: Single filers must report if assets exceed $50,000 at year-end or $75,000 at any point. For married couples filing jointly, the limits increase to $100,000 and $150,000, respectively.

- U.S. citizens living abroad: Single filers must report assets over $200,000 at year-end or $300,000 at any time. For joint filers, the limits are $400,000 at any time or $200,000 at year-end.

Assets that must be reported include foreign bank accounts, investments, and interests in foreign entities. As Katelynn Minott, CEO of Bright!Tax, humorously notes:

"In 2026? Your bank is practically CC’ing the IRS – and its international cousins – before you’ve even filed your own taxes".

Failing to file Form 8938 can result in penalties starting at $10,000, escalating to $50,000 for continued non-compliance. Non-compliant foreign banks may also face a 30% withholding tax on U.S.-sourced income. With over 100 countries participating in FATCA agreements, enforcement is nearly universal.

FBAR: Filing Requirements for Offshore Accounts

The FBAR, governed by the Bank Secrecy Act, is another critical reporting obligation. If the combined value of all foreign financial accounts exceeds $10,000 at any point during the year, you must file FinCEN Form 114 through the BSA E-Filing System. This threshold applies to the total value across all accounts, not individual accounts.

Accounts requiring disclosure include savings, checking, and brokerage accounts. The filing deadline is April 15, with an automatic extension to October 15. The IRS clarifies the purpose of the FBAR:

"The FBAR is also a tool used by the U.S. government to identify persons who may be using foreign financial accounts to circumvent U.S. law".

Non-compliance can result in severe penalties. For non-willful violations, fines can reach $16,536 per violation. Willful violations carry penalties of up to $165,353 or 50% of the account balance, whichever is greater. Criminal penalties include fines up to $250,000 and up to five years in prison. Additionally, those with signature authority over accounts they do not own – like corporate accounts or accounts of elderly relatives – must also file and retain records for at least five years.

CRS: How It Differs from FATCA

The Common Reporting Standard (CRS), developed by the OECD, facilitates the exchange of financial information between participating countries. However, the United States is not part of CRS. As Alex Recouso points out:

"The United States remaining outside CRS is the most significant structural anomaly in the system and shows no signs of changing".

CRS focuses on tax residency rather than citizenship. While FATCA targets U.S. citizens globally, CRS applies to non-residents of the account’s jurisdiction. Unlike FATCA, CRS does not require individuals to file forms. Reporting is handled exclusively by financial institutions.

For U.S. citizens, CRS indirectly affects offshore banking. Banks will still request Social Security Numbers and self-certification forms, like the W-9, to comply with FATCA. Under FATCA, the bank reports the account to the IRS. CRS 2.0, effective January 1, 2026, expands its scope to include digital wallets, electronic money, and Central Bank Digital Currencies, further tightening financial transparency.

| Feature | FATCA | FBAR | CRS |

|---|---|---|---|

| Target | U.S. persons (citizens/residents) | U.S. persons with foreign accounts | Non-residents of account jurisdiction |

| Threshold | $50,000–$400,000 (varies by status) | $10,000 aggregate | No individual threshold |

| Where to File | IRS (with Form 1040) | FinCEN (BSA E-Filing System) | No individual filing required |

| Deadline | With annual tax return | April 15 (auto-extension to Oct 15) | N/A |

| U.S. Participation | Yes | Yes | No |

sbb-itb-39d39a6

Best Offshore Banking Jurisdictions for US Citizens in 2026

Not every offshore banking jurisdiction is open to US citizens. Thanks to the strict requirements of FATCA, many foreign banks shy away from dealing with US passport holders due to the administrative burden. However, some jurisdictions not only accept US citizens but also offer a blend of political stability, strong legal protections, and adherence to international transparency standards.

Choosing the right jurisdiction depends on your financial goals. If you’re focused on safeguarding wealth for the long term, Switzerland remains a top choice. For those engaged in business across the Asia-Pacific region, Singapore stands out with its advanced digital banking services and multi-currency options. Meanwhile, the Cayman Islands are ideal for structuring investment funds or Special Purpose Vehicles (SPVs), thanks to their tax-neutral framework under English common law.

As Bertrand Theaud, Founder of Statrys, notes:

"Offshore banking is transparent by design in 2026".

This highlights that offshore banking today isn’t about avoiding taxes but about protecting assets from lawsuits, creditor claims, and economic or political instability – all while staying compliant with US tax reporting rules.

Here’s a closer look at three standout jurisdictions for US citizens:

Switzerland: A Long-Standing Leader in Banking Privacy

Switzerland manages an impressive $7 trillion in cross-border assets, accounting for roughly 25% of the global offshore wealth. Its reputation for banking discretion, political neutrality, and economic stability has made it a trusted choice for decades.

While Swiss banking secrecy laws have been scaled back since 2010, they still provide strong protections against civil lawsuits and creditor claims. According to OffshoreCompany.com:

"The secret for the law-abiding citizen is to open a bank account in a Swiss bank that does not have branches back home".

For US citizens, Swiss banks do report account details to the IRS under FATCA, but they also ensure your information is shielded from unwarranted legal actions. Account setup requires a Social Security Number and a completed Form W-9.

However, the entry requirements are steep. Private banks like UBS often require minimum deposits ranging from $250,000 to $1,000,000, depending on the service level. Most Swiss banks prefer in-person account openings, though some work through licensed intermediaries. Annual fees can range from a few hundred to several thousand dollars, and detailed KYC documentation is mandatory to verify the source of funds.

Switzerland is an excellent choice for high-net-worth individuals focused on wealth management, estate planning, or safeguarding assets in uncertain times.

Singapore: A Financial Security Hub in Asia

Singapore has earned its place as a leading offshore banking destination in Asia, with over 150 licensed banks and a reputation for financial stability. Its regulatory framework, managed by the Monetary Authority of Singapore (MAS), combines strict oversight with support for innovation, especially in digital banking.

One of Singapore’s standout features is its advanced digital infrastructure. Unlike many Swiss banks, which often require in-person visits, digital-first providers in Singapore allow remote account openings, sometimes completing the process in as little as three business days. Banks like DBS and OCBC offer multi-currency accounts (USD, SGD, EUR, CNH), making them ideal for international entrepreneurs.

Minimum deposit requirements are relatively accessible, starting at $750 to $3,700 for standard accounts. Wealth management tiers, however, typically require $200,000 or more. Digital-first providers often charge foreign exchange fees as low as 0.1%, significantly undercutting traditional banks.

Although Singapore operates on a territorial tax system – meaning offshore income is generally not taxed locally – US citizens must still file an FBAR if account balances exceed $10,000. Singaporean banks fully comply with FATCA, reporting account details annually as required.

As Tunde Aladeloba of Grey.co explains:

"Holding part of your funds in a stable jurisdiction adds balance and resilience, especially when your income depends on cross-border work".

Singapore is a strong fit for digital nomads, tech entrepreneurs, and those involved in Asia-Pacific business activities.

Cayman Islands: Tax-Neutral Solutions for US Clients

The Cayman Islands are a key player in global finance, known for their expertise in investment fund structures, SPVs, and asset protection. Operating under English common law, the jurisdiction imposes no direct taxes on income, capital gains, or corporate profits.

This tax-neutral status makes the Cayman Islands a popular choice for hedge funds, private equity vehicles, and family offices. However, US citizens are still required to report worldwide income to the IRS and pay applicable taxes.

Cayman banks are fully FATCA-compliant, ensuring account details are reported to relevant tax authorities. Following past data breaches, the jurisdiction has tightened its due diligence processes, resulting in more rigorous KYC requirements.

Minimum deposits typically range from $10,000 to $100,000, although specialized fund services may demand higher amounts. Some banks allow remote account setups through licensed intermediaries, but many still require at least one in-person meeting.

The Cayman Islands are ideal for investors managing complex financial structures, family offices handling multi-generational wealth, or business owners seeking legal asset protection.

| Jurisdiction | Primary Strength | Minimum Deposit | Remote Opening | Best For |

|---|---|---|---|---|

| Switzerland | Wealth preservation & stability | $250,000–$1,000,000 | Limited | High-net-worth individuals, estate planning |

| Singapore | Digital services & ASEAN access | $750–$200,000+ | Yes | Entrepreneurs, cross-border business |

| Cayman Islands | Tax neutrality & fund structures | $10,000–$100,000 | Partial | Investment funds, SPVs, family offices |

All three jurisdictions comply with FATCA, but each offers unique advantages, whether you’re looking to protect assets from lawsuits, manage cross-border business, or structure complex investment vehicles.

How to Open an Offshore Bank Account: Step-by-Step Guide

Opening an offshore bank account as a US citizen in 2026 requires careful planning and adherence to strict compliance standards. Today, transparency is the cornerstone of the process, with banks requiring detailed information about your financial background, tax obligations, and the source of your funds. Here’s a step-by-step guide to help you navigate this process while staying within legal boundaries.

Step 1: Determine Your Financial Goals

Before reaching out to a bank, define your financial objectives. This clarity will not only speed up the approval process but also help you select the right jurisdiction. Common reasons for opening offshore accounts include:

- Protecting assets from domestic legal risks

- Diversifying currency holdings to guard against inflation

- Simplifying finances for expats or digital nomads receiving global payments

- Gaining access to international investment opportunities unavailable in the US

Your goals will influence the structure of your account. For example, passive wealth holders face stricter reporting requirements, while active businesses may enjoy greater corporate privacy. If you own a foreign-incorporated business, opening an account in the same jurisdiction can simplify the bank’s Know Your Customer (KYC) process and reduce scrutiny.

It’s also a good idea to maintain your domestic account for routine transactions and tax purposes. As of 2026, the IRS no longer issues paper refund checks, and tax refunds cannot be deposited into foreign accounts.

Step 2: Gather Required Documentation

Offshore banks require extensive documentation to confirm your identity, tax status, and the legitimacy of your funds. For personal accounts, you’ll typically need:

- A valid passport with at least six months remaining

- Proof of residential address and income (e.g., utility bills, bank statements, wage slips, or tax returns from the past three months)

- US tax documents, such as a signed W-9 form and FATCA self-certification

Many jurisdictions also require notarized documents or an Apostille stamp, an international certification mark. Additionally, you’ll need to verify the source of your funds with documents like wage slips, investment records, sales contracts, or inheritance letters.

For corporate accounts, the requirements are more extensive. You’ll need:

- A Certificate of Incorporation

- Memorandum and Articles of Association (M&AA)

- A Register of Directors and Shareholders

- A concise business profile outlining your activities, client types, and expected transaction volumes

Obtaining a reference letter from your current bank or a professional, such as an attorney or accountant, can also help meet due diligence requirements.

Once your documentation is ready, you can focus on finding a bank that aligns with these compliance standards.

Step 3: Choose a Compliant Offshore Bank

Not every offshore bank accepts US citizens. Due to the complexities of FATCA, many smaller banks avoid working with Americans altogether. Larger institutions, equipped with legal teams and compliance officers, are more likely to accommodate US clients.

Look for banks that are Participating Foreign Financial Institutions (PFFIs) under FATCA and ensure they adhere to established KYC protocols. Confirm whether they require a W-9 form and choose jurisdictions accustomed to handling international clients.

If traveling for an in-person meeting is not an option, consider banks in Belize, Mauritius, or the Cayman Islands, which often allow remote account setup. Traditional banks may take two to eight weeks to onboard new clients, while fintech providers can approve accounts within one to five business days. Ensure the bank has strong correspondent banking relationships to avoid disruptions in international transfers. Consulting a tax professional is also crucial to understanding how the bank’s reporting requirements align with your US tax obligations.

Step 4: Submit Your Application and Complete KYC

After selecting a bank, you’ll need to submit your application and go through the KYC process. Many banks now offer digital onboarding, using video verification and online document uploads, especially in fintech hubs like Hong Kong and Singapore. However, traditional banks may still require at least one in-person meeting.

During the KYC process, you’ll be asked detailed questions about your source of funds and expected transactions. Transparency is a priority for banks in 2026, as compliance with regulations takes precedence over client secrecy.

Step 5: Fund Your Account and Set Up Services

Once your application is approved, you’ll need to fund your account and configure additional services. Initial deposit requirements vary widely depending on the jurisdiction and account type. For instance, Swiss private banks often require deposits ranging from $100,000 to $500,000, while some fintech providers have no minimum deposit requirement.

Funds can be transferred via international wire transfers, which typically cost $25 to $75 per transaction. Some banks also allow transfers from other offshore accounts or investment portfolios. To avoid delays, notify your US bank in advance of large international transfers.

After funding your account, you can set up multi-currency accounts to hold USD, EUR, GBP, or other currencies as needed. Many offshore banks also offer investment accounts to access foreign markets or funds.

Be mindful of the costs associated with offshore accounts. Annual fees typically range from $500 to $2,500, and some providers may charge inactivity fees if you don’t meet a minimum number of transactions.

Lastly, remember your US reporting obligations. If the combined value of your foreign accounts exceeds $10,000 at any point during the year, you must file an FBAR (FinCEN Form 114). Additionally, Form 8938 is required if your foreign assets surpass $200,000 at year-end or $300,000 at any time during the year (for single expats). Failing to file an FBAR can result in penalties of up to $10,000 or 50% of the account balance per violation.

Common Mistakes and How to Avoid Them

One of the biggest missteps U.S. citizens make in 2026 is pursuing secrecy in offshore banking. Today, the industry prioritizes transparency over anonymity. Banks are more focused on complying with regulations than hiding client information. Any attempt to obscure your citizenship or assets is not only illegal but also counterproductive. Compliance and clear financial records are now the cornerstones of modern offshore banking.

Another frequent issue is incomplete documentation, which can derail your application process. Missing physical copies, certified translations, or clear source-of-funds documentation often leads to rejections. To avoid delays, provide a detailed explanation of your funds’ origin – whether they come from a business sale, inheritance, or salary. This helps streamline the onboarding process and ensures smoother interactions with compliance officers.

Keep your U.S. bank account open. The IRS does not deposit tax refunds into foreign accounts, so maintaining a domestic account is essential. It’s also a good idea to have a local account for daily expenses and a separate account for currency conversions when handling international transactions.

Be mindful of threshold calculations, especially when it comes to the $10,000 FBAR (Foreign Bank Account Report) requirement. This threshold applies to the combined value of all your foreign accounts at any point during the year – even if the balance exceeds $10,000 for just one day. Use the Treasury’s official year-end exchange rates to determine if you meet the reporting requirement. Additionally, if you have signature authority over accounts you don’t personally own, such as corporate accounts, those must also be reported.

Lastly, only work with banks that require your Taxpayer Identification Number (TIN) and FATCA self-certification forms. Institutions that skip these steps are likely non-compliant, which could lead to severe penalties or even account closures. To protect yourself, confirm that your bank is a Participating Foreign Financial Institution (PFFI) under FATCA, ensuring they report correctly to the IRS.

Combining Offshore Banking with Asset Protection Strategies

Offshore bank accounts by themselves offer limited protection, as U.S. courts can demand the repatriation of funds held in your name. To address this vulnerability, a three-tier structure is often recommended: an offshore trust owning a foundation, which in turn owns an offshore LLC that holds the bank account. This setup ensures that funds are legally controlled by a foreign trustee, making it difficult for U.S. courts to compel their transfer.

When the foreign trustee has authority over the trust and the power to remove you as the LLC manager or withhold distributions, you can argue in a U.S. court that you lack the legal capacity to move the funds. Attorney Gideon Alper explains this principle clearly:

"A court cannot order the individual to do something the individual lacks the legal power to do".

Interestingly, the jurisdictions involved in this structure don’t need to match. For instance, a Cook Islands trust can own a Nevis LLC, which then holds a bank account in Switzerland or Singapore. This approach spreads risk across multiple legal systems, boosting protection. For domestic assets, like real estate that can’t be moved offshore, an offshore entity can register a mortgage or "charge" against the property, stripping its equity and reducing its appeal to creditors.

Financial Considerations

This level of protection comes with financial commitments. Setting up such a structure typically costs between $13,000 and $40,000, with trusts costing $10,000 to $30,000 and LLCs adding another $3,000 to $10,000. Annual maintenance expenses are generally $6,000 to $13,000, plus $3,000 to $5,500 for tax preparation to comply with FBAR, FATCA, and trust reporting requirements. Additionally, many asset protection banks require initial deposits ranging from $100,000 to $500,000.

Key Considerations

It’s important to note that these structures do not provide any tax advantages for U.S. citizens – you’re still taxed on your worldwide income. Their true value lies in creating legal hurdles that make it harder for creditors to access your assets. To avoid accusations of fraudulent conveyance, it’s crucial to establish these protections well before any legal threats emerge.

Conclusion

This article has explored the legal and practical aspects of offshore banking in 2026. For U.S. citizens, offshore banking remains a lawful and practical option – provided it’s done transparently and in full compliance with regulations. These days, offshore banking emphasizes openness, with millions of accounts globally now part of automatic information exchange systems. The aim isn’t to evade the IRS but to diversify risk, access better financial tools, and support a global lifestyle.

Compliance with the law is absolutely essential. This means meeting all U.S. reporting requirements, such as filing FBAR and Form 8938. Since 2009, global offshore compliance efforts have brought in over €135 billion in taxes, interest, and penalties, proving that enforcement is both active and effective.

Picking the right jurisdiction is key to meeting your financial goals. Your offshore banking strategy should align with your objectives, whether you’re focusing on preserving wealth, utilizing digital banking services, or pursuing tax-neutral investment opportunities.

As offshore structures expert Steven James puts it:

"The challenge is no longer finding a bank that will look the other way; it is finding a bank that will look you in the eye and say, ‘We can work with you, as long as you are prepared to work with the law’".

FAQs

Do I need to file both FBAR and FATCA?

Yes, as a U.S. citizen, you are required to file both FBAR (FinCEN Form 114) and FATCA (Form 8938) if your foreign financial accounts and assets meet specific thresholds. If the total value of all your foreign accounts exceeds $10,000 at any point during the year, you must file FBAR. Additionally, FATCA filing is necessary to report foreign financial assets, depending on their value. These filings are essential to stay compliant with U.S. tax laws and avoid potential penalties.

Will an offshore account reduce my U.S. taxes?

Having an offshore account doesn’t automatically lower your U.S. taxes. If the combined value of your offshore accounts goes over $10,000, you’re required to report it and follow the disclosure rules under FATCA and the BSA. Accurate reporting is crucial to avoid penalties and stay compliant with U.S. tax laws.

Can I open an offshore account remotely as a U.S. citizen?

Yes, U.S. citizens can open offshore accounts without needing to visit in person, but there are a few important points to keep in mind. Many banks that comply with FATCA, like those in Singapore or the UK, offer the option to set up accounts remotely. Typically, this involves providing proof of identity, proof of residence, and completing any necessary verification steps. That said, some banks might have more stringent rules or even refuse U.S. applicants altogether. It’s important to focus on banks that explicitly state they accept U.S. clients.