Offshore banking can be a smart way to safeguard and grow your wealth. But not all jurisdictions are created equal. Here’s a quick summary of the 10 safest countries for offshore banking, based on financial stability, deposit protection, and regulatory oversight:

- Switzerland: Known for its stability, privacy laws, and robust deposit protection. Minimum deposit: $500,000.

- Singapore: AAA-rated, strong regulations, and tax advantages. Minimum deposit: $200,000–$1,000,000.

- Cayman Islands: A major hub for hedge funds with strong regulatory oversight. Minimum deposit: $25,000–$50,000.

- Luxembourg: AAA-rated with strong investor protections and EU-compliant regulations. Deposit protection: €100,000.

- Netherlands: Offers solid deposit protection up to €100,000 and strong banking supervision.

- Germany: High safety rankings, with deposit protection up to €100,000 and voluntary schemes covering up to €3 million.

- Sweden: Stable banking system with deposit protection up to SEK 1,150,000 (~$107,000).

- Hong Kong: A financial hub with strong regulatory frameworks and deposit insurance.

- United Arab Emirates: Known for tax efficiency and strict compliance standards. Minimum deposit: Varies.

- Bermuda: Transparent regulations and deposit insurance up to $25,000.

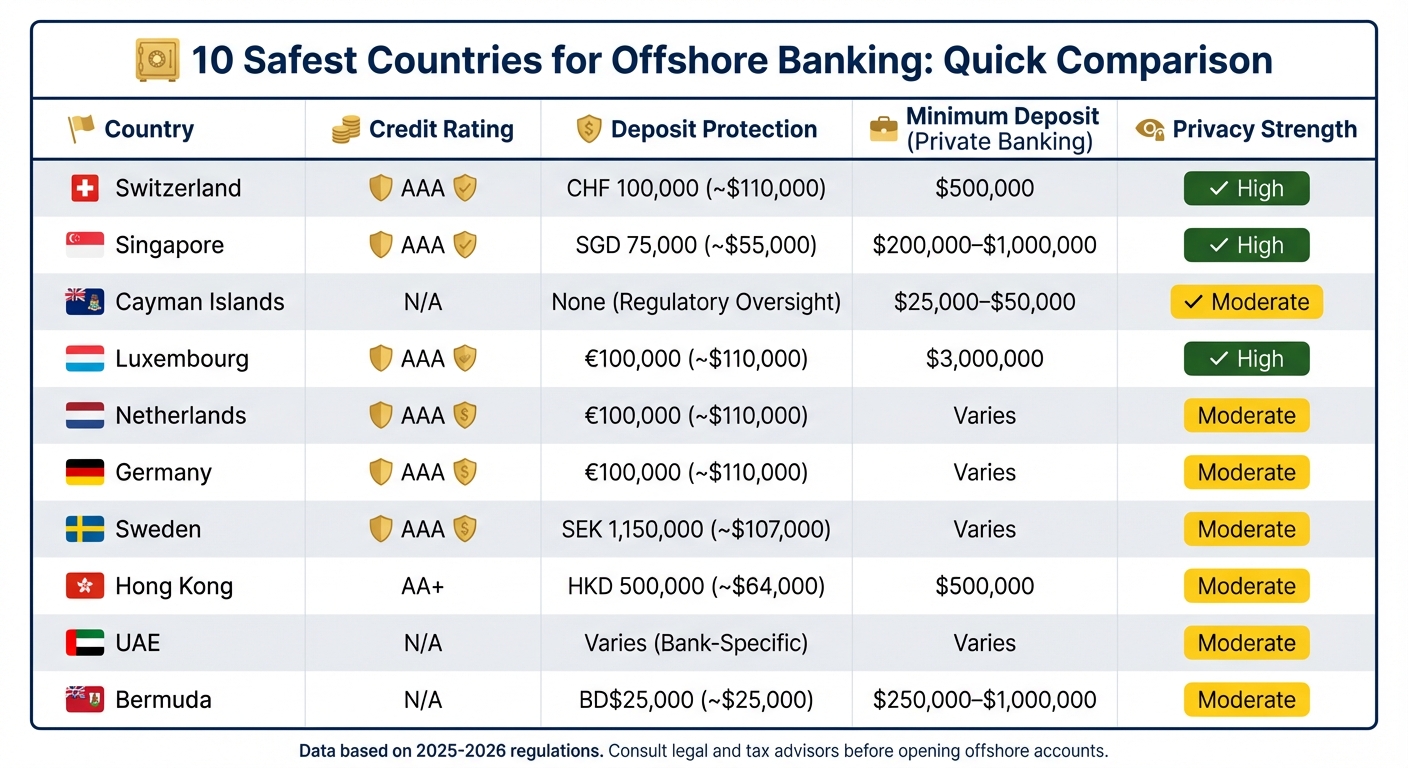

Quick Comparison:

| Country | Credit Rating | Deposit Protection | Minimum Deposit (Private Banking) | Privacy Strength |

|---|---|---|---|---|

| Switzerland | AAA | CHF 100,000 (~$110,000) | $500,000 | High |

| Singapore | AAA | SGD 75,000 (~$55,000) | $200,000–$1,000,000 | High |

| Cayman Islands | N/A | None (Regulatory Oversight) | $25,000–$50,000 | Moderate |

| Luxembourg | AAA | €100,000 (~$110,000) | $3,000,000 | High |

| Netherlands | AAA | €100,000 (~$110,000) | Varies | Moderate |

| Germany | AAA | €100,000 (~$110,000) | Varies | Moderate |

| Sweden | AAA | SEK 1,150,000 (~$107,000) | Varies | Moderate |

| Hong Kong | AA+ | HKD 500,000 (~$64,000) | $500,000 | Moderate |

| UAE | N/A | Varies (Bank-Specific) | Varies | Moderate |

| Bermuda | N/A | BD$25,000 (~$25,000) | $250,000–$1,000,000 | Moderate |

Each jurisdiction offers unique benefits. Your choice depends on your financial goals, risk tolerance, and compliance needs. Always consult legal and tax advisors and review frequently asked questions about offshore banking before opening an offshore account.

1. Switzerland

Financial Stability and Economic Resilience

Switzerland holds a prestigious AAA rating, underscoring its ability to protect long-term capital even during global uncertainty. The Swiss franc (CHF) is widely regarded as one of the most stable currencies, offering a dependable hedge in volatile markets.

In 2022, Swiss banks managed $2.4 trillion (CHF 2.1 trillion) in assets for international clients, more than any other country worldwide. Banking assets in Switzerland are equivalent to 467% of its GDP, and about 25% of all global cross-border assets are handled by Swiss institutions. This combination of financial strength and rigorous oversight makes Switzerland a cornerstone of offshore wealth protection. Additionally, the nation’s long-standing neutrality has kept its banking sector insulated from international conflicts, further solidifying its reputation for wealth preservation.

Banking Regulations and Oversight

Switzerland’s banking system is closely monitored by the Swiss Financial Market Supervisory Authority (FINMA), while the Swiss National Bank (SNB) manages monetary policy and identifies systemically important banks. Banks must comply with strict requirements, including maintaining a minimum fully paid-up capital of CHF 10 million and adhering to "fit and proper" standards for management. The Capital Adequacy Ordinance and Liquidity Ordinance ensure banks manage risks effectively. For systemically important banks, additional "too-big-to-fail" capital buffers are required.

In March 2023, a significant intervention by the Swiss government, SNB, and FINMA led to UBS acquiring Credit Suisse for $3.25 billion (CHF 3 billion), averting a potential systemic collapse and reinforcing the country’s reputation as a stable financial hub. A new senior managers’ regime, set to take effect in late 2025, will enhance accountability within bank governance. FINMA has also prioritized cyber risk management, with 47% of reported cyber incidents in 2025 involving third-party service providers. New regulations, effective January 1, 2026, will require banks to incorporate climate and nature-related financial risks into their overall risk strategies. These comprehensive measures ensure strong deposit protection and bolster trust in the Swiss banking system.

Deposit Protection and Security Measures

Opening a private banking relationship in Switzerland typically requires a minimum deposit of $500,000. This is far more accessible than the $3 million often required in places like Luxembourg or Singapore. The onboarding process, which includes compliance and anti-money laundering checks, usually takes 4–8 weeks. Many Swiss banks also secure tangible assets in specialized underground facilities located in the Alps. The Swiss Bankers Association manages the Depositor’s Protection Agreement, ensuring depositors have legally prioritized claims in the event of a bank failure.

For U.S. citizens, it’s critical to work with FATCA-compliant banks, as many Swiss institutions are cautious about accepting American clients due to stringent compliance requirements. Providing clear and well-documented evidence of one’s source of wealth is essential, as inadequate documentation is a common reason for account rejections. These measures are designed to ensure the security and integrity of offshore accounts.

Confidentiality and Privacy Policies

Swiss banking secrecy, established under the Federal Act on Banks and Savings Banks of 1934, makes unauthorized disclosure of client information a federal criminal offense. Violations can result in penalties of up to five years in prison and fines as high as 250,000 Swiss francs ($250,000).

"If there is anything the Swiss take more seriously than the precision of their watches or the quality of their chocolate, it’s the secrecy of their banks." – Steve Kroft, Host of Banking: A Crack In the Swiss Vault

Modern privacy measures in Switzerland emphasize protecting clients from commercial data breaches, cyberattacks, and unauthorized surveillance, rather than enabling tax evasion. Since 2017, Switzerland has participated in the Common Reporting Standard (CRS), sharing limited financial data for tax compliance purposes. In 2023, information on 3.6 million accounts was shared internationally. However, banking secrecy remains intact for individuals who reside in and are solely taxable in Switzerland, with exceptions made only for criminal activities like money laundering or terrorism financing. To enhance privacy, experts suggest working with Swiss banks that do not have branches in the client’s home country, reducing exposure to domestic regulatory scrutiny.

sbb-itb-39d39a6

2. Singapore

Financial Stability and Economic Resilience

Singapore stands out with its AAA sovereign credit rating and an impressive 0% net debt-to-GDP ratio, making it a net creditor. By March 2025, the nation’s official foreign reserves reached $419.1 billion, while the Monetary Authority of Singapore (MAS) managed assets totaling approximately $629 billion.

The country’s banking sector is a powerhouse, with DBS, OCBC, and UOB ranked among the world’s safest banks. These institutions lead the ASEAN region in reputation and performance. Acting as a vital link between Western and Eastern financial markets, Singapore’s banks are known for their strong capital reserves and a tax-neutral environment, thanks to the absence of capital gains tax.

"Singapore has become the preferred choice for many Asian high-net-worth individuals and family offices, cementing its rising appeal among high-net-worth individuals." – Savory & Partners

This solid financial foundation is further reinforced by Singapore’s stringent regulatory framework, detailed below.

Banking Regulations and Oversight

The Monetary Authority of Singapore (MAS) functions as a centralized regulator, overseeing all financial institutions and enforcing laws related to banking, insurance, and securities. MAS has implemented strict Anti-Money Laundering (AML) and Countering the Financing of Terrorism (CFT) measures, requiring banks to verify both the Source of Wealth (SoW) and Source of Funds (SoF) for their clients. Banks must also file Suspicious Transaction Reports within five business days of detecting any irregularities.

As of 2026, Singapore has introduced more stringent economic substance requirements for non-resident accounts, often necessitating proof of business activity or physical presence. Additionally, in June 2025, Phase 3 of the Financial Services Markets Act 2022 took effect, tightening rules for digital token service providers. MAS is also working with local banks to utilize AI for real-time scam detection by pooling interbank data.

Deposit Protection and Security Measures

Wealth management accounts in Singapore typically require minimum deposits ranging from $200,000 to $1,000,000, while corporate accounts demand $100,000 to $500,000. To safeguard customer funds, Singapore relies on a government-backed deposit insurance scheme, similar to the FDIC in the United States.

Opening an account involves an in-person visit and a due diligence process that can take anywhere from 2 to 8 weeks. Detailed source-of-wealth documentation is essential, as applications are often rejected due to insufficient evidence. For U.S. citizens, it’s worth noting that institutions like DBS Treasures may offer limited account options, such as savings accounts, due to FATCA compliance requirements.

Confidentiality and Privacy Policies

Singapore strikes a balance between regulatory transparency and client confidentiality. While it participates in the Common Reporting Standard (CRS) and FATCA, ensuring account details are shared with relevant tax authorities, the country upholds strict bank-client confidentiality for legally declared assets. Unlike jurisdictions that focus on secrecy, Singapore emphasizes regulatory rigor alongside privacy.

"The key distinction of modern offshore banking isn’t privacy – it’s financial sophistication and regulatory efficiency." – Project Black Ledger

Banks in Singapore enforce rigorous Know Your Customer (KYC) protocols, requiring extensive documentation such as apostilled identification, proof of address, and bank references. The onboarding process may also involve video calls and clear declarations of the source of wealth to meet international compliance standards. Singapore’s approach prioritizes advanced digital security and comprehensive wealth management over secrecy, ensuring clients benefit from both protection and efficiency.

3. Cayman Islands

Financial Stability and Economic Resilience

The Cayman Islands holds its place as the fifth-largest banking center globally, with banking assets surpassing $500 billion. With a GDP per capita of $109,684 in 2023 and a growth rate of 4.0% that same year, the territory demonstrates strong economic health. Unemployment and poverty rates remain exceptionally low, showcasing its resilience. The economy thrives on two main sectors: international finance and luxury tourism, which together account for 50–60% of its GDP. By late 2025, the Cayman Islands hosted around 13,000 mutual funds and 18,000 private funds. As of December 2024, it ranked 20th worldwide for cross-border assets, totaling $306.2 billion. This robust economic foundation supports the stringent regulatory measures detailed below.

Banking Regulations and Oversight

The Cayman Islands’ financial system benefits from strict oversight, primarily enforced by the Cayman Islands Monetary Authority (CIMA). CIMA’s regulatory standards go beyond international recommendations. For example, while Basel guidelines suggest an 8% minimum risk asset ratio, CIMA enforces a 10% minimum, with actual requirements reaching 12% for subsidiaries and 15% for unsupervised banks. Banks operating under unrestricted licenses must maintain a minimum net worth of KYD 400,000 (approximately $500,000), and all directors undergo rigorous "fit and proper" evaluations.

As of late 2025, CIMA supervised 77 bank and trust licensees through a combination of off-site analysis and on-site inspections. Shell banks are prohibited, and annual audits conducted by CIMA-approved auditors are mandatory. Financial statements must be submitted within three months of the fiscal year-end, with serious violations incurring fines of up to CI$1 million. Recent regulatory updates, including amendments to the Beneficial Ownership Transparency Act in 2025 and the National Risk Assessment for 2025–2026, further enhance the jurisdiction’s oversight framework.

"Cayman offshore banking is best understood as institutional offshore banking, not secrecy banking." – Steven James, Offshore Structures Researcher

Deposit Protection and Security Measures

The Cayman Islands’ reputation as a leading destination for asset protection stems from its robust regulatory framework. Opening an offshore account involves a thorough vetting process, requiring extensive documentation and verified professional references. Minimum deposits typically range from $25,000 to $50,000 for basic accounts, while private banking services often require at least $100,000, with some institutions setting thresholds as high as $500,000 or more. For more complex financial structures, the minimum deposit can exceed $1,000,000.

Applicants must provide certified identity documents, professional references from law or accounting firms, and detailed proof of the source of funds. Non-residents must also present a valid economic rationale for banking in the jurisdiction. While proof of a local connection, such as property ownership or business activity, may be required, this is often waived for accounts with high balances.

Confidentiality and Privacy Policies

The Cayman Islands maintains strict confidentiality laws to protect client information. The Confidential Relationships (Preservation) Law, revised in 2009, criminalizes unauthorized disclosure of confidential information, except when required by legal or regulatory obligations. The jurisdiction fully complies with CRS, FATCA, and the OECD’s Crypto-Asset Reporting Framework. Updates to the Beneficial Ownership Transparency Act in 2025 have modernized the beneficial ownership register, ensuring access is restricted to regulators and law enforcement while withholding public access. Additionally, the local legal system enhances asset protection by not automatically enforcing foreign judgments. These privacy measures reinforce the Cayman Islands’ appeal as a secure location for offshore banking and asset protection.

4. Luxembourg

Financial Stability and Economic Resilience

Luxembourg is recognized as one of the most financially stable countries in the world, boasting a AAA credit rating – a status achieved by only a select few nations. At the end of 2022, its debt-to-GDP ratio stood at just 24%, significantly below the EU average of 86.4%. This cautious fiscal approach fosters a highly secure environment for offshore banking.

The country is also the global leader in cross-border asset management and ranks as the second-largest fund center worldwide, following the United States. The Luxembourg Stock Exchange lists over 39,000 securities in more than 60 currencies, representing issuers from over 100 countries. This level of global financial integration reflects its expertise in areas such as private banking, wealth management, sustainable finance, and insurance. Additionally, Luxembourg benefits from a stable political and social climate, which further reduces jurisdictional risks.

Banking Regulations and Oversight

Luxembourg’s banking sector is closely monitored by the Financial Sector Supervisory Commission (CSSF), which enforces stringent oversight based on European Union laws. This regulatory framework ensures high levels of financial supervision and investor protection. By adopting EU regulations and directives ahead of other countries, Luxembourg gains a "first-mover advantage" in compliance, strengthening its position in the global financial market.

The banking industry in Luxembourg is also embracing innovation. For example, the country has introduced blockchain-friendly capital markets legislation and established the Luxembourg House of Financial Technology (LHoFT), a hub for Fintech innovation. These initiatives place Luxembourg at the cutting edge of digital transformation in banking. For those interested in banks operating under these rigorous standards, the ABBL (The Luxembourg Bankers’ Association) represents the leading institutions in the country. This strong regulatory framework also supports Luxembourg’s robust deposit protection measures.

Deposit Protection and Security Measures

Luxembourg offers extensive deposit protection through two primary schemes. The Fonds de garantie des dépôts Luxembourg (FGDL) safeguards cash deposits up to €100,000 per person, per bank, while the Système d’indemnisation des investisseurs Luxembourg (SIIL) covers securities and financial instruments up to €20,000 per eligible investor. To further strengthen these protections, Luxembourg has been collecting additional contributions between 2019 and 2026 to create a financial buffer that doubles the EU-mandated minimum protection fund, targeting a total of 1.6% of covered deposits.

Account holders should confirm whether their bank is Luxembourg-incorporated or a branch of an EU-based institution, as this determines which national guarantee scheme applies. Banks are required to provide an annual standardized depositor information sheet detailing coverage limits and repayment terms.

"The FGDL will thus reach a level of contributions which represents twice the minimum assets required for by the DGSD." – CSSF

Confidentiality and Privacy Policies

In addition to its deposit guarantees, Luxembourg enforces strict confidentiality measures to protect client information. While privacy is a priority, the country balances this with full compliance with international transparency standards. The FGDL operates independently of individual banks and only accesses customer files in the event of a bank failure, ensuring depositor information remains secure under normal conditions.

Luxembourg’s legal framework, grounded in EU legislation, ensures consistent privacy protections while adhering to global transparency requirements. This shift from traditional banking secrecy to a focus on regulatory efficiency and financial innovation has attracted clients seeking advanced wealth management solutions rather than simple confidentiality.

5. Netherlands

Financial Stability and Economic Resilience

The Netherlands boasts a well-established banking system and a top-tier financial hub in Amsterdam. Dutch banks rank among the safest globally, holding fifth and sixth positions on Global Finance‘s safety list, which evaluates asset and credit ratings. Unlike conventional tax havens, the Netherlands builds its reputation on advanced infrastructure and strong safety standards. As part of the EU, it benefits from European regulatory frameworks, further cementing its role as a secure and sophisticated offshore banking destination.

Banking Regulations and Oversight

The Dutch banking system operates under a dual-regulator model. De Nederlandsche Bank (DNB) focuses on prudential oversight to ensure financial stability, while the Netherlands Authority for the Financial Markets (AFM) monitors market conduct and transparency. Larger banks fall under the European Central Bank‘s (ECB) supervision through the Single Supervisory Mechanism (SSM), with DNB overseeing smaller institutions under ECB guidelines.

The Netherlands has implemented strict risk-control measures, including a bonus cap that limits variable pay to 20% of fixed salaries – much lower than in many other EU countries. Additionally, management and supervisory board members undergo rigorous fit-and-proper assessments, and a mandatory two-tier governance structure separates daily operations from oversight responsibilities. These measures contribute significantly to the country’s strong financial security.

Deposit Protection and Security Measures

The Netherlands’ robust regulatory framework is complemented by the Dutch Deposit Guarantee Scheme, which protects deposits ranging from as little as 1 cent to €100,000 (about $110,000) per person, per bank. For joint accounts, the protection doubles to €200,000 (about $220,000). Temporary high balances, such as real estate sale proceeds, are safeguarded up to €500,000 (about $550,000) for six months.

In May 2022, following the bankruptcy of Amsterdam Trade Bank, DNB efficiently managed the payout process, disbursing 95% of guaranteed deposits within one month. Around 80% of eligible customers received their compensation during this period. Starting January 2024, the statutory payout period will be reduced to just 7 business days, ensuring quick access to funds in case of bank failures.

Here’s an overview of the Dutch Deposit Guarantee Scheme:

| Account Type | Protection Limit | Duration |

|---|---|---|

| Individual Account | €100,000 (≈ $110,000) | Permanent |

| Joint Account | €200,000 (≈ $220,000) | Permanent |

| Temporary High Balance | €500,000 (≈ $550,000) | 6 months |

To confirm eligibility, ensure your bank operates under a Dutch banking license, as this determines coverage under the scheme. Keep in mind that the Deposit Guarantee Scheme does not extend to investment products like stocks, bonds, insurance, or cryptocurrencies. Additionally, the system is funded entirely by banks through quarterly premiums, ensuring its sustainability without relying on taxpayer money.

6. Germany

Financial Stability and Economic Resilience

Germany’s banking system is among the safest in the world, with its banks consistently ranking at the top of Global Finance’s list of secure institutions – holding the 1st, 3rd, 4th, and 7th spots globally. This stability is rooted in Germany’s strong national economy and its distinctive multi-pillar banking structure. The system includes private banks, public banks, savings banks, and credit cooperatives, each with their own protection mechanisms. Additionally, Germany imposes limited capital controls and allows high-denomination banknotes, making it easier for individuals and businesses to hold hard currency. Together, these factors create a resilient banking environment that has proven its ability to endure financial challenges. This economic strength is complemented by a rigorous regulatory framework.

Banking Regulations and Oversight

Germany’s financial system is backed by a robust regulatory structure designed to protect its banks and depositors. Under the Single Supervisory Mechanism (SSM), the European Central Bank (ECB) oversees major institutions, while smaller banks are monitored by the Federal Financial Supervisory Authority (BaFin) and the Deutsche Bundesbank. The German Banking Act (KWG) requires banks to maintain a minimum capital of €5 million, have two qualified managing directors, and operate from a registered office in Germany. Additionally, the mandatory two-tier board system ensures a clear separation between management and supervisory roles.

Strict anti-money laundering standards are enforced under the German Money Laundering Act (GwG), requiring banks to conduct thorough customer due diligence and monitor business relationships continuously. A notable example of Germany’s regulatory efficiency occurred in 2025 when BaFin ordered the closure of Bankhaus Obotritia GmbH. This action triggered the Compensation Scheme of German Private Banks (EdB), which promptly began reimbursing depositors under statutory protection rules.

Deposit Protection and Security Measures

Germany offers a three-tier deposit protection system, providing a high level of security for depositors.

- The statutory Deposit Guarantee Act (EinSiG) protects deposits up to €100,000 (approximately $110,000) per depositor, per bank, with compensation issued within seven working days.

- For temporary high balances, such as proceeds from property sales or insurance payouts, the protection increases to €500,000 (approximately $550,000) for six months.

- Many private banks also participate in voluntary protection funds through the Association of German Banks (BdB), currently covering up to €3 million (approximately $3.3 million) for private savers. However, this limit will decrease to €1 million by 2030.

Savings banks and credit cooperatives use Institutional Protection Schemes (IPS), which focus on preventing insolvency altogether. These schemes effectively guarantee 100% of deposits.

"Germany has already developed and applied a deposit insurance model for decades that virtually rules out deposit or bank runs like those in the US or Switzerland" – Jan Pieter Krahnen, Founding Director emeritus of SAFE

Germany’s statutory deposit scheme achieved its target level of 0.8% of total covered deposits in July 2024, further solidifying its safety net.

| Protection Type | Coverage Limit | Legal Entitlement | Payout Timeline |

|---|---|---|---|

| Statutory (EinSiG) | €100,000 (≈ $110,000) | Yes | 7 working days |

| Temporary High Balances | €500,000 (≈ $550,000) | Yes | 7 working days |

| Voluntary (BdB) – Private | €3 million (≈ $3.3 million) | No | Varies |

| Institutional Protection (IPS) | Virtually unlimited | De facto | N/A (prevents failure) |

For those with multi-million-dollar deposits, diversifying across Germany’s banking pillars is a smart strategy, especially as voluntary limits are set to decrease by 2030. While German accounts typically offer lower interest rates and limited currency diversification compared to other offshore hubs, the unmatched security and regulatory oversight make Germany an excellent choice for safeguarding wealth. These measures ensure that Germany remains a reliable destination for protecting significant assets.

7. Sweden

Financial Stability and Economic Resilience

Sweden’s banking system stands out for its stability, reflected in its AAA rating and a solid national balance sheet. The Swedish Financial Supervisory Authority (Finansinspektionen) plays a key role in maintaining this stability by enforcing strict capital adequacy requirements and conducting regular stress tests. These measures ensure that Swedish banks can handle economic disruptions effectively. As a member of the European Union, Sweden also adheres to the European Banking Authority (EBA) framework, which provides a standardized and transparent regulatory environment. This combination of national oversight and EU-level regulations creates a banking system that prioritizes long-term security over short-term profits.

Banking Regulations and Oversight

Sweden uses a multi-agency system to oversee its banking sector, dividing responsibilities among four main entities: the Swedish Financial Supervisory Authority (SFSA), the Swedish Central Bank (Riksbanken), the Swedish National Debt Office (Riksgälden), and the Ministry of Finance. These organizations work together through the Financial Stability Council to address potential risks. The legal framework is based on the Banking and Financing Business Act (SFS 2004:297), complemented by EU regulations like the Capital Requirements Regulation (CRR II) and the Bank Recovery and Resolution Directive (BRRD II).

To operate in Sweden, banks must meet several requirements, including presenting a solid business plan, holding initial capital of at least €5 million (around $5.5 million), and passing suitability checks for board members and senior executives. The SFSA also imposes a hefty application fee of SEK 1,500,000 (approximately $140,000) and is required to process complete applications within six months. Additionally, any acquisition of 10% or more of a bank’s capital requires prior approval. The SFSA evaluates the buyer’s reputation and financial stability, typically completing this review within 60 working days. These rigorous practices are supplemented by strong deposit protection measures.

Deposit Protection and Security Measures

The Swedish National Debt Office (Riksgälden) manages the country’s deposit insurance scheme, which will cover up to SEK 1,150,000 (approximately $107,000) per person, per institution starting January 1, 2026. This protection is triggered if a bank goes bankrupt or if the Swedish Financial Supervisory Authority activates the insurance. Sweden also follows the EU Crisis Management Directive, ensuring a coordinated response to banking sector challenges.

For those with deposits exceeding the coverage limit, spreading funds across multiple banks is a simple way to maximize protection, as the limit applies separately to each institution. The Riksgälden provides an official database to confirm if a bank is part of the deposit insurance scheme. Additionally, an investor compensation scheme covers securities and funds up to SEK 250,000 (around $23,300) in case of a bank’s failure.

Swedish banks also comply with CRS and FATCA standards, ensuring a high level of regulatory transparency. This shift from financial secrecy to efficient regulation means account holders must stay compliant with their home-country tax laws while benefiting from Sweden’s advanced financial systems. These include AI-driven compliance tools that streamline KYC processes and monitor transactions effectively.

8. Hong Kong

Financial Stability and Economic Resilience

Hong Kong operates under a common law system with an independent judiciary, which bolsters confidence in its financial framework. As of April 2026, the city holds an AA+ / Stable sovereign credit rating. Acting as a vital link between mainland China and global markets, Hong Kong provides direct access to Renminbi (RMB) clearing services, simplifying trade settlements with China.

The Hong Kong Monetary Authority (HKMA) ensures a strong regulatory environment, including frameworks for virtual assets, stablecoins, and central bank digital currencies (CBDCs). A 2024 HKMA survey highlighted a shortfall of 2,800 professionals in AI and data science. In response, over 70% of banks initiated upskilling programs and recruited 1,500 international fintech experts to strengthen the sector.

"Hong Kong’s reputation as a leading international financial centre rests on widely recognised fundamentals… underpinned by the strong foundation of the rule of law, with the benefits of a common law system, independent judiciary, clean transparency index and trust in the core system." – Paul McSheaffrey, Senior Banking Partner at KPMG China

This solid foundation supports the city’s rigorous regulatory oversight, as outlined below.

Banking Regulations and Oversight

Hong Kong enforces strict anti-money laundering (AML) and Know Your Customer (KYC) protocols. Opening a bank account often requires an in-person visit, along with proof of identity, address, and source of wealth. This process typically takes two to six weeks. Such measures are critical to maintaining Hong Kong’s reputation for secure offshore banking. Additionally, local banks comply with international transparency standards such as the Common Reporting Standard (CRS) and the Foreign Account Tax Compliance Act (FATCA). These practices contribute to the city’s strong safety rankings, such as Hang Seng Bank‘s recognition as the 8th safest bank in Asia by Global Finance Magazine in 2022.

Deposit Protection and Security Measures

To complement its strict regulatory framework, Hong Kong offers robust deposit protection. The HKMA administers a formal deposit insurance program, providing a safety net similar to the FDIC in the United States. Offshore account minimum deposits generally range from $10,000 to $50,000, while private banking relationships typically require a minimum of $500,000. This makes Hong Kong more accessible compared to alternatives like Singapore, where private banking minimums can reach $3,000,000.

Confidentiality and Privacy Policies

Banking confidentiality in Hong Kong is grounded in English common law, as established in Tournier v National Provincial and Union Bank. While banks uphold strict confidentiality, exceptions are made for legal requirements, public interest, or with client consent. Additionally, while privacy policies are designed to protect commercial data and combat cyber threats, client information is shared under international transparency agreements. Hong Kong scored 72 on the Financial Secrecy Index, reflecting its balanced stance between privacy and global transparency. Its territorial tax system exempts offshore income, capital gains, interest, and dividends from taxation, further enhancing its appeal for international banking.

9. United Arab Emirates

Financial Stability and Economic Resilience

The UAE has established itself as a key "East-West bridge" by focusing on innovation and business-friendly regulations. With zero personal income tax and a competitive 9% corporate tax introduced in 2023, the country appeals to free zone and qualifying offshore entities. This tax framework, combined with its strong stability and advanced banking systems, makes it a top choice for offshore banking.

UAE banks take a forward-thinking, digital-first approach by embracing fintech and cutting-edge technologies like blockchain. For instance, blockchain integration in trade finance has slashed processing times from weeks to days, while smart contracts handle routine transactions automatically. This shift has transformed the UAE from a traditional secrecy-based banking hub into a transparent, compliance-oriented center aligned with global standards like CRS. For a deeper dive into global jurisdictions, see our offshore banking report.

"The UAE represents banking’s future: where traditional financial services merge seamlessly with technological innovation." – Project Black Ledger

Banking Regulations and Oversight

The Central Bank of the UAE (CBUAE) strictly regulates licensed financial institutions, including banks, exchange houses, and insurance companies. The framework emphasizes economic substance, requiring banks to focus on clients with active international business rather than passive account holders.

The "Dormant Accounts and Unclaimed Funds Regulation" (C 9/2025) ensures that funds in inactive accounts remain the rightful property of customers or their heirs. Accounts are labeled dormant after three years of inactivity, and after five years, their balances are transferred to an Unclaimed Balances Account at the Central Bank. Banks must reconcile these accounts monthly and undergo annual external audits. No fees are charged for reactivating or closing dormant accounts, and interest continues to accrue on eligible accounts.

Deposit Protection and Security Measures

UAE banks enforce stringent Know Your Customer (KYC) and due diligence protocols. Clients often need to provide detailed documentation, and corporate accounts may require in-person reviews. Access to dormant account records is tightly controlled, with dual authorization required for sensitive operations. Claims for dormant funds are processed within a month of verification, and reactivated accounts are closely monitored to prevent misuse for fraud or money laundering. Companies failing to meet beneficial ownership reporting requirements face penalties of up to 100,000 UAE dirhams. These measures are part of a broader privacy and security framework designed to protect clients.

Confidentiality and Privacy Policies

Article 120 of the CBUAE Rulebook guarantees the confidentiality of all customer data, including accounts, deposits, trusts, and safe deposit boxes. Disclosure to third parties is strictly prohibited without written consent from the account holder or their authorized representative, except in cases authorized by law. This obligation remains binding even after the account is closed and applies to all bank employees.

"All data and information relating to customers’ accounts, deposits, safe deposit boxes and trusts with Licensed Financial Institutions and related transactions shall be considered confidential in nature." – CBUAE Rulebook

Despite these strong protections, the UAE’s privacy rating is lower than that of jurisdictions like Switzerland, as the country prioritizes international transparency and compliance over traditional banking secrecy. While beneficial ownership information is collected, it is not publicly accessible. Exceptions to confidentiality include judicial requests, Central Bank inquiries, audits, and disclosures required for anti-money laundering and counter-terrorism efforts.

10. Bermuda

Financial Stability and Economic Resilience

Bermuda stands out as a secure offshore banking destination, operating under a British legal framework with strong governance. Unlike jurisdictions known for banking secrecy, Bermuda has built its reputation on transparency and compliance, making it a magnet for institutional investors. The island is also a global leader in reinsurance, with its market projected to account for about 35% of global reinsurance capital by 2025. Adding to its appeal, the Bermuda dollar is pegged 1:1 to the U.S. dollar, eliminating currency risks. These factors, combined with rigorous regulatory oversight, make Bermuda a stable and reliable choice.

"Bermuda is an established offshore financial centre and has enjoyed a long history of political, economic and social stability." – Simon Benedek, Partner at Kennedys Law

Banking Regulations and Oversight

The Bermuda Monetary Authority (BMA) is the island’s sole financial regulator, overseeing banks under the Banks and Deposit Companies Act 1999. Bermuda adheres to Basel III standards, requiring banks to maintain minimum capital ratios: 4.5% for CET1, 6.0% for Tier 1, and 8.0% for total capital. Banks must also meet a Liquidity Coverage Ratio (LCR) of at least 100%. To address systemic risks, the BMA enforces additional capital surcharges of 0.5% to 3% for Domestic-Systemically Important Banks. Demonstrating its regulatory authority, the BMA revoked the license of 777 Re, a reinsurer, in October 2024 after uncovering financial misconduct and failure to file audited statements.

Deposit Protection and Security Measures

Bermuda offers a deposit insurance scheme that protects eligible deposits up to BD$25,000 (approximately $25,000 USD). The Banking (Special Resolution Regime) Act 2016 provides mechanisms for stabilizing banks in distress, including transferring operations to private buyers or restructuring through a "bridge bank." To combat cyber threats, the BMA enforces an Operational Cyber Risk Management Code of Conduct, requiring banks to appoint a Chief Information Security Officer and implement board-approved cybersecurity policies. However, account holders should be aware that minimum deposit requirements for private and investment banking services often range from $250,000 to $1,000,000.

Confidentiality and Privacy Policies

Bermuda has embraced global transparency standards, moving away from traditional banking secrecy. The jurisdiction complies with CRS and FATCA regulations and was removed from the EU’s tax "grey list" in October 2022, reflecting its commitment to international tax cooperation. At the same time, Bermuda prioritizes client data protection. The Banks and Deposit Companies Code of Conduct includes strict customer protection measures, such as disclosure requirements and internal controls to safeguard client interests. With the world’s 6th highest anti-money laundering (AML) rating, Bermuda emphasizes compliance while ensuring robust privacy measures.

Conclusion

Choosing the right offshore banking jurisdiction requires a clear understanding of your financial goals and the legal framework of each option. From Switzerland’s expertise in wealth management to Bermuda’s transparent regulatory environment, the ten jurisdictions highlighted in this guide offer a variety of benefits. For instance, Switzerland handles approximately 25% of the world’s cross-border private assets, while countries like Singapore and Luxembourg boast AAA credit ratings, ensuring long-term financial security. These examples illustrate how the offshore banking landscape is increasingly shaped by transparency and regulatory changes.

The industry has undergone significant shifts toward compliance and openness. Over 100 nations now participate in the automatic exchange of account information through the Common Reporting Standard (CRS). For U.S. citizens, compliance includes filing an FBAR if foreign financial accounts exceed $10,000 at any point during the year. These developments emphasize the need to choose jurisdictions with strong legal protections that align with international regulations.

Each jurisdiction offers a unique mix of advantages and safeguards. Your choice should depend on whether your priorities lie in asset protection, tax efficiency, digital accessibility, or market access. Minimum deposit requirements range widely – from $250,000 in some regions to as much as $3,000,000 for high-tier private banking options in places like Singapore, Luxembourg, and the UAE. These variations reflect the diverse levels of protection and services available. Consulting experienced tax and legal advisors is essential for navigating multi-entity structures, such as structuring offshore trusts, understanding deposit insurance, and meeting entry requirements for restricted jurisdictions that may require "eligible introducers".

The best jurisdiction for you will depend on your specific needs, objectives, and willingness to manage regulatory complexities. Be sure to evaluate sovereign credit ratings and ensure your choice aligns with both your financial plans and legal responsibilities. A secure offshore banking strategy is built on stability, transparency, and expert guidance – not secrecy.

FAQs

Is offshore banking legal for U.S. citizens?

Yes, offshore banking is completely legal for U.S. citizens. That said, all offshore accounts must be fully reported to the IRS. It’s important to note that having an offshore account doesn’t lower your U.S. tax responsibilities. To avoid penalties, you must ensure strict compliance with all reporting requirements.

How does deposit insurance work offshore?

Offshore deposit insurance works much like domestic systems in safeguarding funds in bank deposit accounts. However, the specifics can differ significantly depending on the country. The level of coverage and protections available are tied to the regulations and banking policies of the jurisdiction where the offshore bank operates. To ensure your assets are protected, it’s crucial to thoroughly review the deposit insurance policies of the country where your offshore account is held.

What documents do I need to open an offshore account?

To set up an offshore account, you’ll generally need a valid passport, proof of address, and documentation verifying your source of funds or wealth. These documents are essential to meet international standards such as AML (Anti-Money Laundering) and KYC (Know Your Customer) regulations, which help ensure compliance and streamline the account opening process. Keep in mind that specific requirements can vary depending on the bank and the jurisdiction involved.