Opening an offshore bank account is no longer just for the ultra-wealthy. With minimum deposits as low as $1,000, individuals with modest budgets – like freelancers, small business owners, and expats – can take advantage of offshore banking benefits, including currency diversification, protection from economic instability, and better interest rates.

Here’s what you need to know:

- Affordable Options: Jurisdictions like Belize and Seychelles offer low deposit requirements, starting at $1,000 for personal accounts.

- Remote Setup: Many banks now allow accounts to be opened entirely online, often within 2–4 weeks.

- Key Documents: You’ll need a valid passport, proof of address, bank reference letter, and evidence of fund origin.

- Compliance: U.S. citizens must report offshore accounts through FBAR (if balances exceed $10,000) and FATCA.

For those seeking cost-effective solutions, fintech platforms like Wise or Statrys offer multi-currency accounts with no deposit requirements and streamlined digital onboarding. By understanding jurisdiction-specific requirements and adhering to tax obligations, offshore banking can be a practical tool for managing international finances.

Selecting Affordable Offshore Jurisdictions

Finding an offshore jurisdiction with low deposit requirements can simplify the process for individuals and small businesses. Factors like minimum deposits, fees, and account accessibility are key considerations when making a choice.

Belize is one of the most cost-effective options. For instance, Caye International Bank offers personal accounts with a minimum deposit of $1,000 and corporate accounts starting at $2,000. The account opening fee is about $100, with a monthly maintenance fee of $14.50. These accounts can be opened remotely, typically within 7–10 days for personal accounts, and are available in multiple currencies, including USD, CAD, EUR, GBP, and CHF. Belizean banks operate under the International Banking Act, requiring a 24% liquidity rate – significantly higher than the 5% standard for U.S. banks.

Seychelles is another appealing option, especially for corporate structures. While traditional banks, like Al Salam Bank, require a $25,000 initial deposit, pairing a Seychelles International Business Company (IBC) with Electronic Money Institutions (EMIs) can dramatically reduce costs. Maintaining a Seychelles IBC costs under $1,200 annually – 40–60% less than a comparable entity in the British Virgin Islands. Additionally, services like Wise Business offer multi-currency accounts for Seychelles entities at approximately $50 per year.

The British Virgin Islands (BVI) is better known for company formation than direct banking. Most BVI companies choose to open accounts in other jurisdictions due to the limited availability of local banks. However, BVI companies benefit from easy access to international EMIs, with annual maintenance costs ranging from $1,500 to $3,000. They also offer flexibility, with no restrictions on fund movements.

When choosing a jurisdiction, it’s essential to align your decision with your financial goals. Belize is ideal for those seeking low-deposit personal or corporate accounts. Seychelles offers cost-efficient corporate structures with fintech integration. Meanwhile, the BVI is a strong choice for international business operations, even if banking occurs outside the jurisdiction. Understanding these options lays the groundwork for navigating the documentation and KYC requirements ahead.

sbb-itb-39d39a6

Documentation and KYC Requirements

Opening an offshore account involves verifying your identity and financial history. Fortunately, most banks ask for similar documents, so you can prepare in advance without incurring extra expenses. This process aligns with global KYC (Know Your Customer) standards, ensuring compliance with international banking regulations.

Required Documents for Account Opening

To get started, you’ll need a valid passport with a minimum of 6–18 months of remaining validity. Many banks also require a secondary ID, such as a national ID card or driver’s license. For proof of residence, you’ll need a utility bill (electricity, water, or gas) or a bank statement showing your full name and address, dated within the last three months.

Banks also assess your financial history. A reference letter from your current bank, confirming a positive banking relationship, is typically required. Additionally, you’ll need to provide documents proving the legal origin of your funds, such as tax returns from the past 1–3 years, recent pay stubs, or investment account statements.

| Document Type | Typical Requirements | Validity/Recency |

|---|---|---|

| Passport | Certified/Notarized copy | 6–18 months remaining |

| Address Proof | Utility bill or bank statement | Under 3 months old |

| Tax Returns | Complete returns with schedules | Past 1–3 years |

| Bank Statements | Personal or business accounts | Past 6–12 months |

| Reference Letter | Letter from current bank manager | Recent (within 3 months) |

"The application stage that takes the longest is not document gathering; it is the business profile. Banks want to understand what you actually do, who pays you, and how funds flow through the account." – Statrys

Once your documents are ready, there are cost-effective ways to complete the KYC process smoothly.

How to Complete KYC Without Extra Costs

To save money, focus on digital submission options offered by many banks. This eliminates the need for international courier services. When submitting documents digitally, using the bank’s mobile app is often more reliable than a web browser, as apps are optimized for real-time image capture.

Here are some tips for digital submissions:

- Use natural light to capture clear, glare-free photos of your documents.

- Ensure all four corners of the document are visible in the frame.

- Make sure the machine-readable zone (MRZ) is clearly legible.

- Opt for PDF bank statements for address proof, as these are less likely to fail automated verification compared to scanned utility bills.

For reference letters, request them early from your current bank – many banks provide these for free or for a small fee. If certification is required, check if notarized copies are acceptable instead of an apostille stamp. Local notarization is usually faster and more affordable than international apostille certification. Some banks now even offer video conferencing for identity verification, which can further reduce costs by eliminating the need for physical certifications.

Statrys, a licensed payment service provider, has helped over 10,000 SMEs open offshore business accounts in Hong Kong and Singapore as of April 2026. They report that 96% of applications are approved within three business days through an entirely online process that requires no account opening fees or initial deposits.

How to Open an Offshore Bank Account: Step-by-Step Process

Opening an offshore bank account has become much simpler, especially with the rise of digital onboarding. Many banks now allow you to complete the entire process online, saving you the trouble and expense of traveling.

Researching and Comparing Banks

Start by identifying jurisdictions that align with your financial situation. For example, Panama and the UAE often require minimum deposits of around US$25,000, with some UAE accounts needing as much as US$100,000. On the other hand, Belize typically has lower or even minimal deposit requirements. If your budget is under US$10,000, you might explore fintech options like Wise or Airwallex, which offer multi-currency accounts without strict deposit thresholds.

Take a close look at fee structures in addition to deposit requirements. Monthly maintenance fees can range from US$50 to US$500, and banks with no deposit requirements may charge higher service fees – for example, for SWIFT tracing or issuing debit cards. It’s also worth checking if the bank supports multiple currencies (e.g., USD, EUR, GBP) to avoid steep foreign exchange fees on international transactions.

Regulatory frameworks are another key factor. Jurisdictions like Singapore and Hong Kong have strong reputations, with regulators such as the Monetary Authority of Singapore (MAS) and Hong Kong Monetary Authority (HKMA) providing oversight. In Singapore, deposit insurance through the SDIC covers up to SGD 75,000. While traditional offshore banks offer stability and wealth management services, they often require higher deposits. In contrast, Electronic Money Institutions (EMIs) provide quicker onboarding at lower costs, though deposit insurance might be limited.

"Banks that allow online opening aren’t always cheaper. In fact, some may hit you with other fees that make it more expensive than in-person account opening options in the long run." – GlobalBanks

Here’s a quick comparison of common jurisdictions:

| Jurisdiction | Typical Min. Deposit | Timeline | Remote Opening |

|---|---|---|---|

| Panama | US$25,000 | 1–2 weeks | Medium |

| Belize | Low/Minimal | 1–2 weeks | High |

| UAE (Dubai) | US$25,000–US$100,000 | 1–2 weeks | Medium |

| Hong Kong | US$25,000–US$100,000 | 2–3 weeks | Medium |

| Singapore | US$200,000–US$500,000 | 3–6 weeks | Medium |

Once you’ve selected a jurisdiction and bank, you’re ready to move on to the application process.

Completing and Submitting Your Application

Most banks now provide digital platforms for submitting applications. Before starting, prepare a detailed personal or business profile that outlines your income sources, payment flows, and how you intend to use the account. This step can help speed up the Know Your Customer (KYC) process and avoid delays.

Ensure you have all necessary documents ready. High-quality PDFs are preferred over scanned images, as they are easier for automated systems to verify. For personal accounts, approval typically takes 2 to 4 weeks, while corporate accounts with complex structures might require up to 20 weeks.

Some payment service providers, like Statrys, boast a 96% approval rate within three business days for online applications. They use video KYC for identity verification, eliminating the need for notarized or mailed documents. Additionally, they don’t charge account opening fees or require initial deposits.

"For entrepreneurs, Hong Kong offers the right mix of credibility and accessibility." – Sneha Patwari, Corporate Secretary Lead, Statrys

Once your application is submitted, most banks allow you to complete the process entirely online.

Opening Accounts Remotely

Remote account opening is now a practical solution for many clients, especially those looking to save on travel costs. Jurisdictions like Belize, Mauritius, and Panama are particularly accommodating, with banks offering secure document upload portals and video calls for identity verification.

If notarized documents are required, check if local notarization is acceptable instead of an apostille stamp. Local notarization is often faster and less expensive.

Be mindful of inactivity fees. Some providers charge monthly fees if you don’t meet a minimum number of transactions. For example, Statrys imposes a fee of HKD 88 per month if fewer than five outbound payments are made. To manage costs, consider keeping a domestic account alongside your offshore one. Use the domestic account for larger wire transfers and reserve the offshore account for international transactions.

Reducing Costs and Comparing Banking Options

Now that we’ve covered the steps to open an account, let’s dive into how you can cut ongoing expenses and evaluate banking options effectively.

How to Lower Your Banking Fees

When it comes to costs, the real burden often lies in the ongoing fees – not the initial account setup. While opening fees are usually small, monthly maintenance charges, foreign exchange (FX) spreads, and penalties for not maintaining minimum deposits can quickly add up. Dropping below the required balance can trigger fines that eat away at your funds.

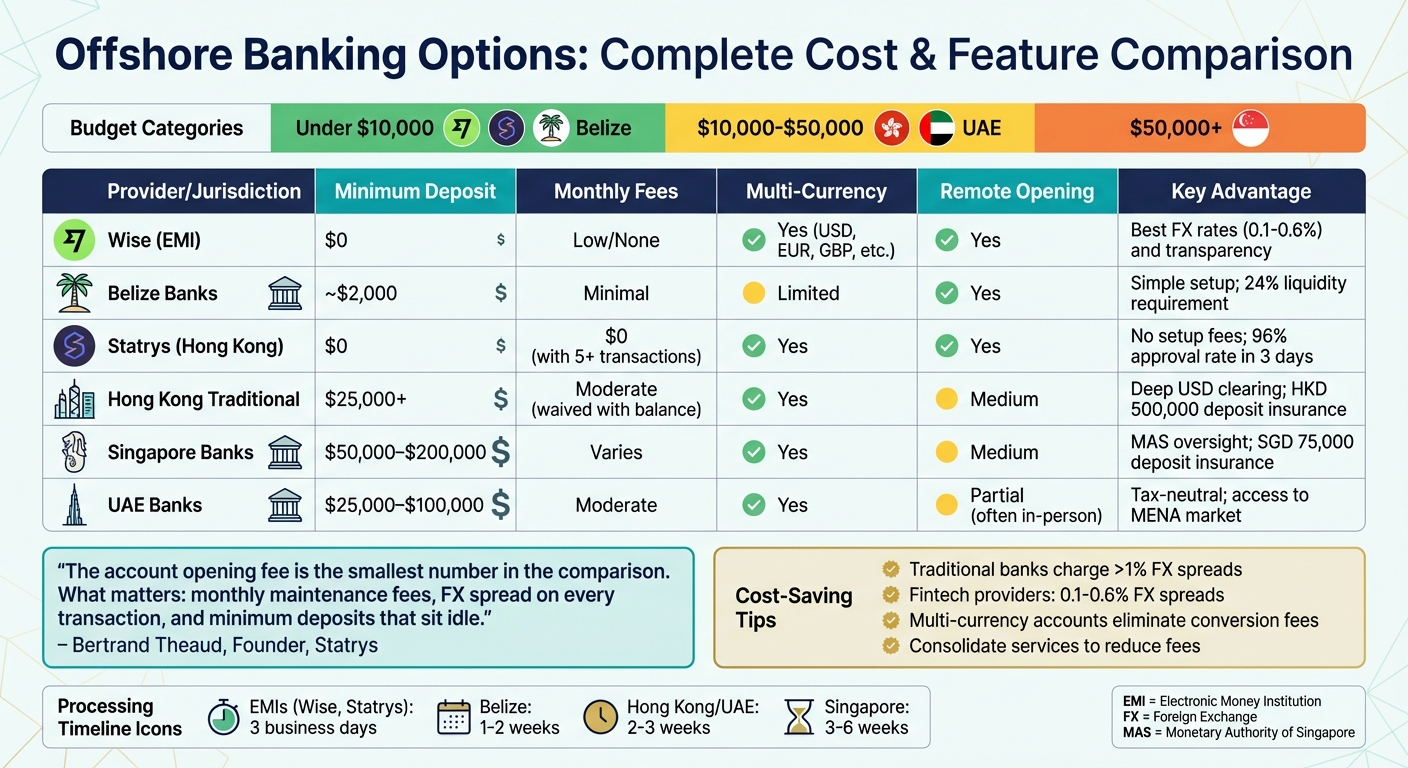

"The account opening fee is the smallest number in the comparison. What matters: monthly maintenance fees… FX spread on every transaction, and minimum deposits that sit idle." – Bertrand Theaud, Founder, Statrys

One way to save is by using multi-currency accounts, which help avoid expensive FX markups. For example, traditional banks often charge over 1% for currency conversions, whereas fintech providers like Wise offer much lower spreads, typically between 0.1% and 0.6%. Holding balances in multiple currencies – like USD, EUR, or GBP – can eliminate the need for constant conversions.

Another tip is to consolidate services. Combining savings, investment, and corporate accounts with the same bank can sometimes reduce fees. Additionally, making larger but less frequent international transfers can help minimize cumulative charges.

Bank and EMI Comparison

Here’s a look at how different providers stack up, especially for those working with limited funds:

| Provider/Jurisdiction | Minimum Deposit | Monthly Fees | Multi-Currency | Remote Opening | Key Advantage |

|---|---|---|---|---|---|

| Wise (EMI) | $0 | Low/None | Yes (USD, EUR, GBP, etc.) | Yes | Best FX rates and transparency |

| Belize Banks | ~$2,000 | Minimal | Limited | Yes | Simple setup; 24% liquidity requirement |

| Statrys (Hong Kong) | $0 | $0 (with 5+ transactions) | Yes | Yes | No setup fees; high approval rate |

| Hong Kong Traditional | $25,000+ | Moderate (waived with balance) | Yes | Medium | Deep USD clearing; HKD 500,000 deposit insurance |

| Singapore Banks | $50,000–$200,000 | Varies | Yes | Medium | MAS oversight; SGD 75,000 deposit insurance |

| UAE Banks | $25,000–$100,000 | Moderate | Yes | Partial (often in-person) | Tax-neutral; access to the MENA market |

Electronic Money Institutions (EMIs) like Wise stand out for their low barriers to entry. They don’t require minimum deposits and offer fully digital account setups. On the other hand, traditional banks in regions like Singapore and Hong Kong offer stronger deposit protections and broader financial services, but they come with higher initial deposit requirements and stricter Know Your Customer (KYC) protocols. These options allow clients with limited budgets to manage their funds effectively without overcommitting financially.

Combining Offshore Banking with Company Formation

Pairing offshore banking with company formation can make financial management more efficient, especially when affordable banking options and straightforward documentation are already in place.

Benefits of Corporate Offshore Accounts

Establishing an offshore company before opening a bank account can significantly improve your chances of approval. Banks are more likely to work with accounts that have a clear and structured business framework. By presenting a corporate entity – whether for international trade, consulting, or investment – you demonstrate the kind of organization that aligns with compliance requirements.

"An offshore holding company in a jurisdiction with strong asset protection laws… creates a legal barrier between your business assets and potential creditors." – EasyInc

A corporate structure doesn’t just help with compliance; it also provides access to international payment processors and strengthens asset protection. This setup creates a legal separation between personal finances and business liabilities. Additionally, jurisdictions with confidential ownership regulations can enhance privacy. Many small business owners follow a step-by-step approach: they begin with an EMI (Electronic Money Institution) for immediate operations and later switch to traditional banks after building a transaction history. This strategy lays the groundwork for cost-effective company formation.

Low-Cost Jurisdictions for Company Formation

For entrepreneurs on a budget, certain jurisdictions – like Seychelles, Belize, and the Marshall Islands – offer affordable company formation options with quick processing times and favorable tax benefits. Here’s a quick breakdown:

- Seychelles: Starting at $595, it’s an affordable option.

- Belize: Costs begin at $990, offering a balance of affordability and reputation.

- Marshall Islands: While slightly pricier, it’s well-regarded by traditional banks.

St. Vincent and the Grenadines is another noteworthy option, especially for banking accessibility. Some banks in this jurisdiction allow corporate accounts to be opened with as little as $2,000.

If your business relies on banking credibility – particularly with European or Asian banks – the Marshall Islands is a solid choice. These jurisdictions often provide 100% tax exemption on foreign-sourced income.

However, it’s essential to verify banking access before committing to a jurisdiction. While company formation can be completed quickly, securing a bank account might take up to three months, as banks act as gatekeepers. Don’t base your decision solely on tax rates – ensure the jurisdiction aligns with the banks and payment processors your business will rely on.

US Tax Compliance for Offshore Accounts

Even if you’re opening an offshore account with limited funds, staying compliant with US tax laws is essential for protecting your assets. The IRS demands full transparency about foreign accounts, and understanding the rules can make compliance straightforward and cost-effective.

FATCA and IRS Reporting Requirements

US taxpayers with foreign accounts must navigate two key reporting obligations: FBAR (FinCEN Form 114) and FATCA (Form 8938). Here’s how they differ:

- FBAR applies if the total value of your foreign accounts exceeds $10,000 at any point in the year – even for just a day. If your accounts collectively hit $10,001, you must report all of them. This form is filed electronically through FinCEN’s BSA E-Filing System, and there’s no cost to file. The deadline is April 15, but an automatic extension to October 15 is available.

- FATCA (Form 8938) has higher thresholds. For individual US residents, reporting is triggered if foreign assets exceed $50,000 on the last day of the year or $75,000 at any point during the year. For joint filers, the thresholds are $100,000 and $150,000, respectively. Unlike FBAR, FATCA must be filed directly with your annual tax return, and it does not come with an automatic extension.

"The Foreign Account Tax Compliance Act (FATCA) requires offshore banks to report balances and banking activities of American citizens to the IRS." – The Business Guy, Asset Protection Planners

Additionally, all foreign-sourced income – whether it’s interest, dividends, or capital gains – must be reported on your US tax return, even if the funds stay overseas. To calculate the US dollar value of foreign balances, use the Treasury Bureau of the Fiscal Service exchange rate for December 31.

By understanding these rules, you can avoid common compliance mistakes.

Common Compliance Errors to Avoid

Knowing the rules is only half the battle; avoiding common pitfalls is just as important. One frequent mistake is assuming that filing either FBAR or FATCA satisfies both requirements. These are separate obligations under different laws, so filing one does not cover the other.

Another issue arises with dormant accounts. Even if an account is inactive, it must be reported if your total foreign account balances exceed $10,000 at any point during the year. Remember to report the maximum value each account reached during the year, not just the year-end balance.

"Quiet disclosure is when a Taxpayer submits information to the IRS regarding the undisclosed foreign accounts, assets, and income but they do not go through one of the approved offshore disclosure programs. This is illegal." – Golding & Golding, International Tax Law Firm

If you’ve missed filings in the past, don’t simply submit them late. Instead, use approved amnesty programs like the Streamlined Filing Compliance Procedures for non-willful violations. Finally, keep detailed records for at least five years, including account names, numbers, bank addresses, and the maximum values each account reached during the year.

Conclusion

The world of offshore banking has shifted, making it accessible to a broader audience, including those with limited funds. While once seen as a privilege reserved for the wealthy, offshore banking now caters to small businesses and individual entrepreneurs. With global offshore holdings exceeding $7 trillion, it’s clear this market has expanded significantly.

"Opening an offshore bank account isn’t just for large corporations or the ultra-wealthy. With the right planning and support, it’s a smart move for entrepreneurs, global professionals, and anyone managing income across borders." – Pallavi Srivastava, Chartered Company Secretary

Your success largely hinges on choosing the right jurisdiction and account type that fit your financial situation. High-end banking hubs may require significant deposits, but mid-tier options typically start around $25,000. For those on tighter budgets, fintech platforms like Wise or Airwallex offer a practical alternative. These services often require no minimum deposit, provide fully remote onboarding, and boast approval rates as high as 96% within just three business days.

To make the most of offshore banking, start by defining your financial goals – whether it’s currency diversification, asset protection, or something else. Gather essential documents early, such as a certified passport copy, recent proof of residence, and bank statements. Opting for a jurisdiction with remote onboarding can help reduce costs while ensuring compliance with tax laws. Staying transparent with tax authorities is crucial, so be sure to file required reports like FBAR and FATCA to avoid penalties. By combining careful planning with strict adherence to tax regulations, you can create a solid offshore banking strategy.

FAQs

Will an offshore account get frozen if I can’t keep the minimum balance?

If you don’t maintain the minimum balance in an offshore account, it doesn’t always mean your account will be frozen. This largely depends on the policies of the bank and the rules of the jurisdiction where the account is held. Some banks enforce strict deposit requirements, and failing to meet them could affect your account’s status. It’s a good idea to carefully review the terms of the bank and jurisdiction you’re considering – some may have more flexible policies or accounts with lower minimum balance thresholds.

How do I prove the source of funds if I’m a freelancer or self-employed?

As a freelancer or self-employed professional, demonstrating the source of your funds typically involves providing documentation that confirms your income. This can include items like invoices, contracts, payment receipts, or bank statements that reflect deposits from your clients. Maintaining detailed and organized records of your earnings is essential to meet the bank’s due diligence and anti-money laundering standards, ensuring your funds are acknowledged as legitimate.

Are fintech multi-currency accounts treated like “offshore accounts” for FBAR/FATCA?

Fintech multi-currency accounts held within the U.S. or in compliant foreign jurisdictions typically don’t fall under the category of "offshore accounts" for FBAR or FATCA reporting. However, if these accounts are located in foreign jurisdictions outside the U.S., they might be considered reportable foreign financial accounts under FBAR and FATCA rules. It’s crucial to confirm the reporting obligations based on the account’s location and the relevant legal requirements.